How to Reduce Your Tax Liability Legally

Reduce your tax liability legally with proven strategies. Discover deductions, credits, and planning techniques to lower your tax bill.

Most business owners spend their days fighting fires instead of building strategy. We at Sager CPA see this pattern constantly-owners neglect financial planning because they’re consumed by operations.

The truth is that financial planning for business owners isn’t optional. It’s the difference between a business that survives and one that thrives.

Most business owners operate in reactive mode. A client demands attention, cash flow tightens, a tax deadline looms-and financial planning disappears. This isn’t laziness. It’s the reality of running a business where immediate problems require immediate solutions. The challenge is that owners treat financial planning as a luxury task rather than a survival tool. They assume it requires hiring expensive consultants, weeks of analysis, or complex spreadsheets they cannot maintain. In reality, effective financial planning starts with three concrete actions: separating personal and business finances, tracking cash flow monthly, and setting aside time quarterly to review numbers. None of these require advanced degrees or specialized software. A basic accounting tool and one afternoon per month can transform your financial visibility. The real barrier isn’t complexity-it’s priority. When you manage daily operations, financial planning feels abstract until a cash crunch forces your hand or tax season arrives with an unexpected bill. This is exactly why the most successful business owners treat financial planning like they treat payroll: non-negotiable and scheduled. They don’t wait until problems emerge.

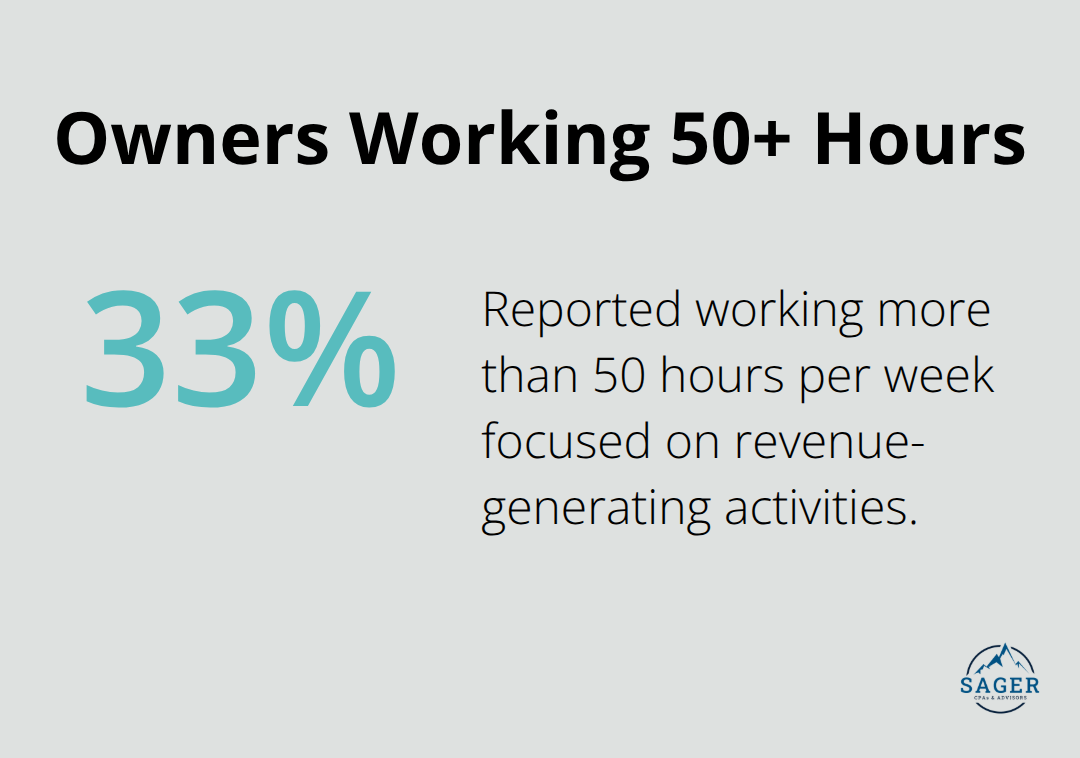

33% of small business owners reported working more than 50 hours per week focused on revenue-generating activities. Adding financial planning to that workload feels impossible.

The solution isn’t finding more hours-it’s recognizing that poor financial planning costs far more time than good planning saves. An owner who spends 10 hours monthly on financial review can catch cash flow problems before they require emergency action, negotiate better vendor terms, and identify tax savings worth thousands. Without that visibility, the same owner spends weeks managing crises, borrowing to cover shortfalls, or paying unnecessary taxes. Automation handles much of this burden now. Monthly bank reconciliations, invoice tracking, and expense categorization run on their own through accounting software. The owner’s job shifts from data entry to decision-making-reviewing what the numbers reveal and adjusting strategy accordingly.

Try one day per month. Block it on your calendar and treat it as immovable. Most owners find this single habit reveals opportunities they never see when flying blind through operations. The first month, you’ll likely notice patterns in spending, identify slow payment cycles, or spot duplicate vendor charges. The second month, you’ll catch seasonal revenue dips before they create cash shortfalls. The third month, you’ll have enough data to forecast the next quarter with confidence. This isn’t complicated work-it’s consistent work. You don’t need perfect systems or advanced financial knowledge. You need a commitment to look at your numbers regularly and act on what you find. Many owners resist this step because they fear what they’ll discover. Poor cash flow, tax exposure, or inefficient spending patterns often hide in the shadows. But that ignorance doesn’t protect you-it exposes you. The owners who face their numbers head-on gain control over their finances instead of letting their finances control them.

An owner without financial visibility operates on assumptions. You assume cash will cover next month’s payroll. You assume your tax liability won’t spike. You assume your business is profitable because revenue looks strong. These assumptions fail regularly, and when they do, the costs multiply. A cash flow crisis forces you to borrow at high rates, miss growth opportunities, or cut corners on quality. An unexpected tax bill strains your reserves or forces you to defer investments. A profitability problem that you discover too late means you’ve already wasted months on an unprofitable strategy. Financial planning prevents these scenarios. It replaces assumptions with facts. You know exactly when cash arrives and when it leaves. You understand your tax obligations months in advance, not days before the deadline. You see which products, services, or clients actually generate profit and which ones drain resources. This clarity costs time upfront but saves far more time later. The owner who invests five hours monthly in financial review typically avoids the crisis that consumes 40 hours of emergency problem-solving. The math is simple: good planning pays for itself many times over.

Financial planning fails not because it’s hard but because owners don’t schedule it. Revenue-generating work always feels more urgent. A prospect call, a customer complaint, or a project deadline will always seem to demand your attention right now. Financial planning demands attention too-just not right now. This is the trap. You can postpone financial planning indefinitely because nothing breaks immediately when you skip it. But the damage accumulates quietly. Cash flow deteriorates. Tax exposure grows. Opportunities vanish. Then one day, a real crisis hits, and you realize you’ve been flying blind for months. The owners who succeed treat financial planning like payroll. They don’t debate whether to do it. They don’t wait until they feel like it. They schedule it, protect that time, and execute. This single shift-from “I’ll do financial planning when I have time” to “I do financial planning every month, period”-separates owners who control their finances from owners who react to them. The next step is understanding what financial planning actually requires. Cash flow management, tax optimization, and succession planning form the foundation. Each one addresses a specific vulnerability that threatens business survival. Avoiding common budgeting mistakes strengthens your financial foundation and prevents costly errors.

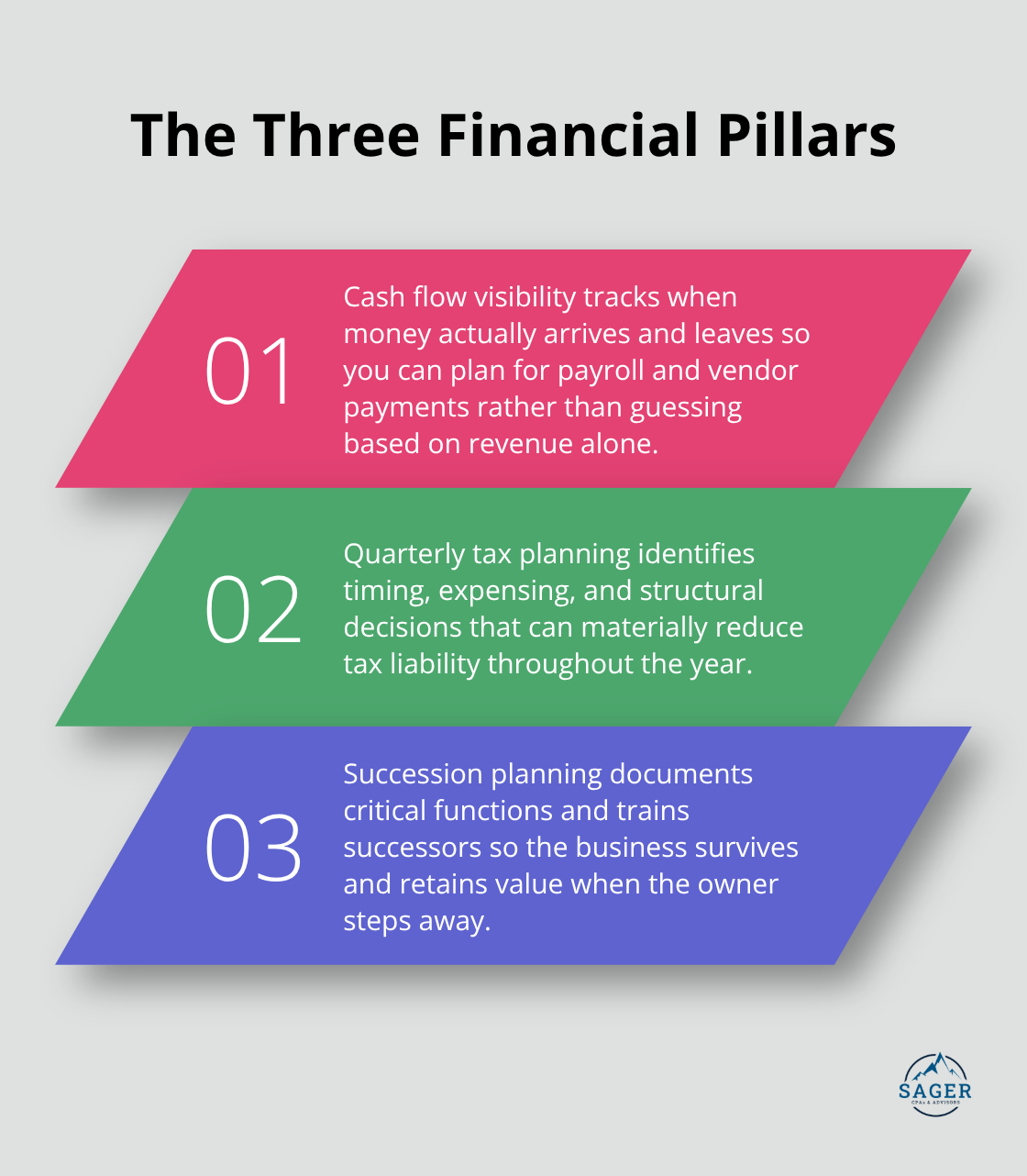

Cash flow is oxygen. Tax planning is strategy. Succession planning is insurance.

These three elements form the operational backbone of any business that survives beyond the founder’s tenure. Most owners handle one reasonably well and ignore the other two, which is why they end up stressed, overtaxed, and unable to exit their business without chaos. We see owners who’ve built successful operations but have no idea whether they’ll have cash next month, how much they actually owe in taxes, or what happens to the business when they step away. The fix requires action in all three areas simultaneously, not someday, but starting this quarter.

An owner with $500,000 in annual revenue and 30% margins feels wealthy on paper. That same owner can run out of cash in March if clients pay in 60 days and vendors demand payment in 30. This gap between profit and cash flow destroys more businesses than poor sales ever will. Profitable companies go bankrupt regularly because they can’t cover payroll. The solution starts with a simple monthly cash flow statement that tracks when money actually arrives and leaves your account. Not revenue recognized, not expenses accrued, but real cash in and out.

Build this forecast for the next 12 months using historical data. If you invoice clients, when do they actually pay? If you have seasonal revenue, when do the peaks and valleys hit? If you carry inventory or have vendor payment terms, when do those dollars leave your account? Once you see the real pattern, you can plan. A business with a March cash dip can negotiate extended terms with vendors in February, accelerate collections in January, or arrange a credit line before the problem hits. Without this visibility, March arrives as a crisis.

Most accounting software automates this work now. You feed in invoices and bills, and the system tracks cash timing automatically. Your job is reviewing the forecast monthly and adjusting strategy. If the forecast shows a $50,000 shortfall in June, you have five months to fix it through pricing changes, payment term negotiations, or expense cuts. If you discover it in June, your options are borrowing at emergency rates or cutting payroll immediately.

A business that waits until tax season to understand its liability typically pays 20% to 40% more than necessary. The owners who minimize taxes act throughout the year. In 2025, the landscape shifted dramatically. Under the One Big Beautiful Bill Act, bonus depreciation was restored to 100% and made permanent starting in 2025. Manufacturing structures placed in service before 2031 now qualify for full expensing if construction begins between January 20, 2025 and the end of 2028. Immediate expensing of domestic research and development expenses also begins in 2025, with retroactive expensing available for small businesses back to 2022.

These changes mean equipment purchases, facility investments, and R&D spending generate massive tax deductions in 2025 and beyond. A business that doesn’t plan around this misses substantial savings. Quarterly tax planning with a CPA identifies these opportunities before you make spending decisions. You learn whether a $100,000 equipment purchase saves you $21,000 in federal taxes this year. You understand whether timing that investment in January versus December changes your tax bracket. You know whether your business structure (S-corp, C-corp, or pass-through) positions you for maximum deductions and minimum exposure.

This isn’t theoretical. A business owner in the 32% federal bracket plus 8% state taxes saves $4,000 on a $10,000 equipment purchase if it qualifies for expensing versus depreciation. Multiply that across all capital decisions in a year, and the savings dwarf the cost of quarterly tax planning. Additionally, for pass-through entities, explore whether a PTE tax election makes sense for your situation. This election allows paying state taxes at the entity level, creating a federal deduction for owners that sometimes generates significant savings. The mechanics are complex and state-specific, which is why this conversation belongs with a tax advisor in Q1, not Q4.

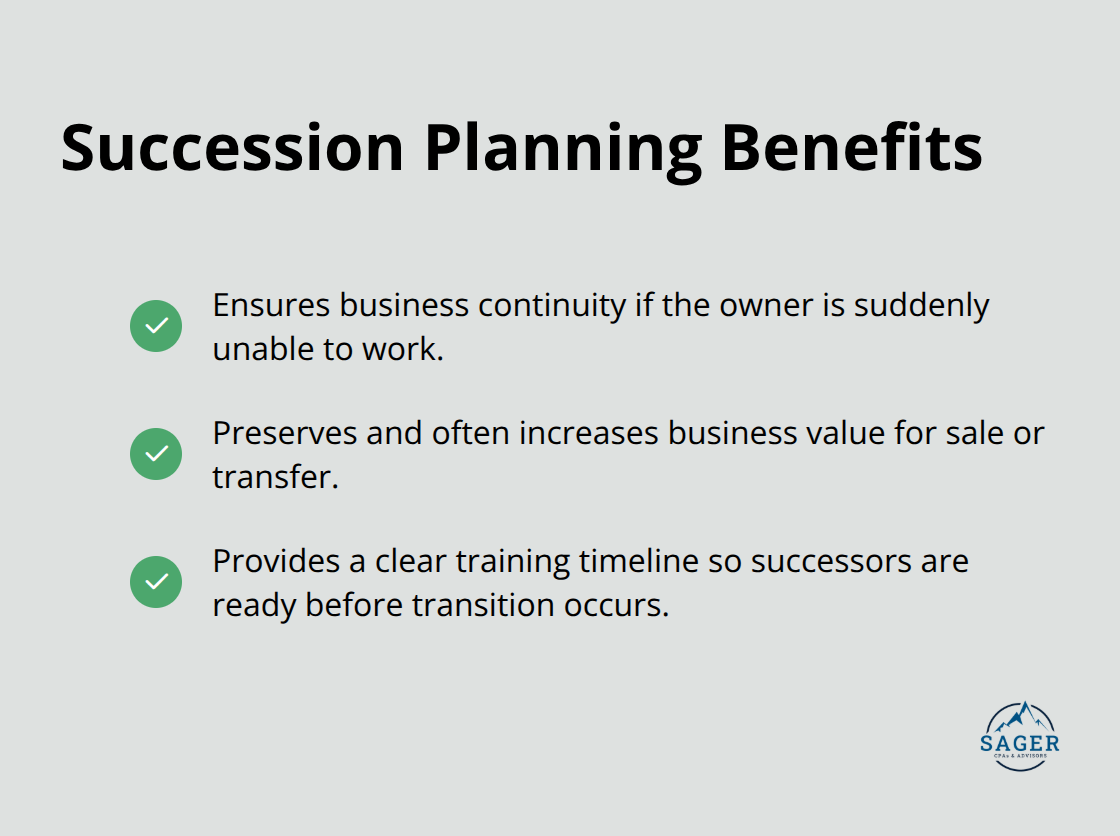

Research found only 4% of business owners have completed their succession plan. This gap creates risk. An owner who leaves suddenly through illness, death, or burnout leaves a business in chaos.

An owner who wants to sell has nothing to sell if operations depend entirely on them. An owner who wants to hand the business to a child or employee discovers too late that the successor isn’t ready.

Succession planning begins with a brutal inventory of what you actually do. Map every critical function. Who manages client relationships? Who handles operations? Who makes financial decisions? Who oversees quality? For each function, identify whether your business would survive if you disappeared tomorrow. Most owners realize they are single points of failure. The solution requires documenting processes, training a successor, and gradually shifting responsibility before you need to leave. This takes years, not months.

If you have a child interested in the business, start now. If you want to sell to a competitor or private equity firm, they will value a business that runs without you far more highly than one that stops functioning the day you step away. If you plan to hand operations to a trusted employee, that person needs 18 to 36 months to learn the job properly. Waiting until you’re burned out or sick means forcing a rushed transition that costs money and creates operational damage.

Start with a conversation. What happens to the business in five years? Do you want to sell, hand it to family, transfer it to employees, or wind it down? Once you answer that, the succession requirements become clear. Each path requires different preparation. The conversation starts with a consultation to map your situation and identify the steps that matter most. With these three pillars in place, you’re ready to address the specific mistakes that derail most owners-mistakes that cost thousands in taxes, cash, and lost opportunities.

Most owners operate with one checking account, one credit card, and a vague sense that they should separate things someday. This arrangement creates immediate problems. You cannot see what the business actually costs to run because personal expenses mix with operational spending. You cannot track profitability accurately because you don’t know which dollars belong to the business and which belong to your household. You cannot defend your tax deductions during an audit because the IRS sees commingled accounts and assumes you’re hiding something.

The fix is straightforward: open a separate business checking account and business credit card today, not next month. Move all business revenue into the business account. Pay all business expenses from the business account. Keep personal spending completely separate. This single action transforms your financial visibility and audit readiness.

You’ll see immediately how much cash the business generates monthly, what your true operating costs are, and whether you’re actually making money. Without separation, you’re operating blind. One owner had $800,000 in annual revenue but couldn’t answer whether the business was profitable. Revenue looked strong, but personal expenses were buried in business accounts. Once separated, they discovered the business was barely breaking even after accounting for actual operating costs. That clarity changed everything about their strategy and pricing.

Most owners assume they understand what they owe until April arrives with a bill 30% larger than expected. The gap comes from three mistakes: underestimating self-employment taxes, missing deductible expenses, and failing to plan for estimated payments.

A self-employed owner earning $100,000 owes approximately $15,300 in self-employment taxes alone, plus income tax. Many owners budget for income tax only and get blindsided. To figure your estimated tax, you must figure your expected adjusted gross income, taxable income, taxes, deductions, and credits for the year. Miss these payments and you face penalties and interest. A business owner earning $150,000 with no estimated payments can owe $2,000 to $4,000 in penalties alone when they file.

This is avoidable. Set aside 25% to 35% of net profit monthly for taxes, depending on your business structure and income level. Deposit that money into a separate tax savings account immediately. When tax season arrives, you’ll have the cash available instead of scrambling. Quarterly tax planning with a CPA identifies deductions you missed and ensures your estimated payments align with your actual liability.

Most owners have no cash buffer beyond next month’s payroll. One client loss, one major equipment failure, or one slow season creates panic. A cash crisis forces you to borrow at high rates, cut quality to save money, or miss growth investments.

The standard recommendation is maintaining three to six months of operating expenses in reserve. For a business with $30,000 monthly expenses, that’s $90,000 to $180,000 set aside. This feels impossible when cash is tight, but it builds gradually. Start with one month of expenses. Once you reach that, add another month. Most owners reach a full emergency reserve within two to three years of consistent saving.

The businesses that survive downturns are those with this buffer. The ones that don’t often fail not from lack of demand but from inability to cover payroll during a temporary revenue dip. A separate savings account (distinct from your operating account) makes this discipline automatic. Transfer a fixed percentage of monthly revenue into this account before you spend anything else. Treat it as non-negotiable, like payroll or rent.

Financial planning for business owners isn’t a one-time project-it’s a rhythm that separates owners who control their finances from those who react to them. The three pillars of cash flow visibility, tax optimization, and succession readiness address the vulnerabilities that threaten most businesses. Cash flow management prevents the profitable company from running out of money, tax planning captures thousands in deductions that owners miss by waiting until April, and succession planning protects the value you’ve built and ensures the business survives beyond your involvement.

The owners who implement these practices gain immediate advantages: they catch cash shortfalls months before they become crises, they reduce tax liability through strategic timing and structure decisions, and they build a business that functions without them, which increases its value and their options for exit. The cost of this planning is modest-a few hours monthly and professional guidance from a CPA. The return is substantial: reduced stress, lower taxes, better cash management, and a business worth selling or handing to the next generation.

Start this quarter by opening a separate business account if you haven’t already, scheduling a monthly review of your cash flow forecast, and setting aside tax reserves based on your actual liability rather than guesses. We at Sager CPA help business owners implement these practices through strategic tax planning and financial advisory services tailored to your specific situation. The first step is a conversation about where you are now and where you want to be, and from there, we build a personalized action plan that addresses your cash flow, tax exposure, and succession needs.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.