Owner Retirement Income Planning: Securing Your Golden Years

Plan your owner retirement income with strategies to maximize wealth, minimize taxes, and secure financial independence for your future.

Most people overpay their taxes simply because they don’t know what’s available to them. At Sager CPA, we’ve helped countless clients cut their tax bills through legitimate strategies that actually work.

This guide walks you through proven methods for tax liability reduction-from retirement accounts to deductions you might be missing. Start implementing these tactics now, and you’ll see the difference when tax season arrives.

Your tax liability is the actual dollar amount you owe to the federal government after accounting for all income, deductions, and credits. It’s not theoretical-it’s the number that determines whether you get a refund or owe money on April 15th. Understanding what creates this liability is the first step to reducing it.

Your liability stems from taxable income, which includes wages from your W-2 job, self-employment earnings, investment gains, rental income, and other income sources. The IRS doesn’t care how you earned the money; they care that you report it accurately. Most people focus only on their salary, but if you have side income, investment accounts, or rental property, those amounts add to your tax bill.

Not all income gets taxed the same way, and this distinction shapes which reduction strategies actually work for your situation. Long-term capital gains receive preferential tax rates compared to ordinary income. Qualified dividends also get favorable treatment. Self-employment income gets hit with both income tax and self-employment tax, making it substantially more expensive than W-2 wages. Understanding these differences matters because it shows you exactly where tax reduction strategies have the biggest impact.

Tax brackets determine how much of your income gets taxed at each rate, and this is where most people misunderstand their tax situation. The 2025 standard deduction is $15,750 for single filers and $31,500 for married filing jointly, according to the IRS. That means if your income falls below these amounts, you owe zero federal income tax.

Once you exceed the standard deduction, your taxable income gets taxed at progressive rates-10%, 12%, 22%, 24%, 32%, 35%, or 37%. A common misconception is that moving into a higher bracket means all your income gets taxed at that rate. That’s wrong. Only the income within each bracket gets taxed at that rate.

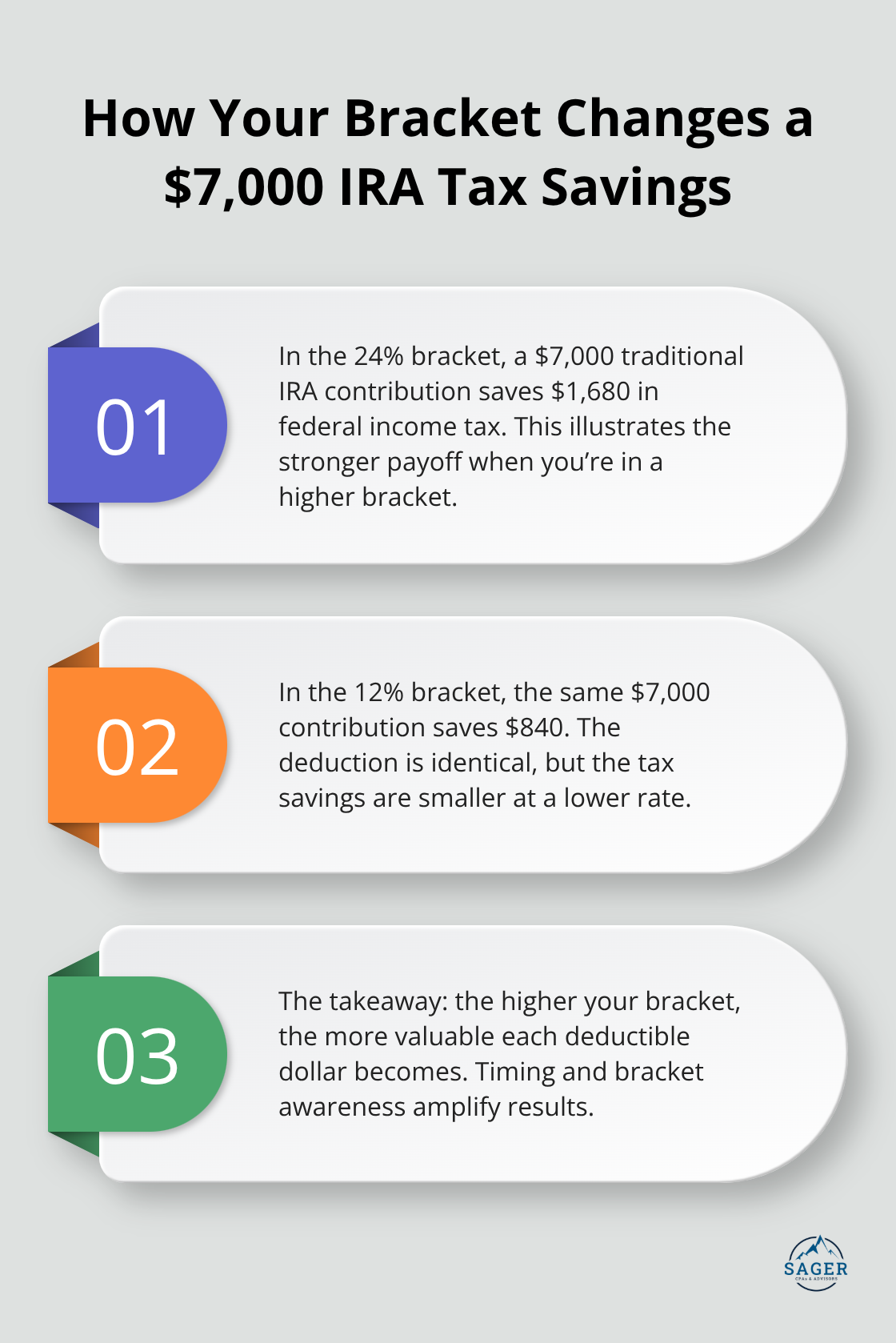

Your bracket position determines your return on tax-reduction moves, which is why timing matters and why strategic planning beats reactive filing. If you’re in the 24% bracket and you contribute $7,000 to a traditional IRA, you save $1,680 in taxes. If you’re in the 12% bracket, the same contribution saves $840.

These numbers show that the higher your bracket, the more valuable each deduction becomes.

This is exactly why maximizing retirement account contributions and claiming all eligible deductions should be your next focus.

The gap between what people owe and what they could legally reduce comes down to action, not luck. Traditional IRAs and 401(k)s remain the most direct way to shrink your taxable income. For 2025, you can contribute up to $23,500 to a 401(k), or $31,000 if you’re 50 or older. According to the IRS, contributions reduce your taxable income dollar-for-dollar, which means a $7,000 traditional IRA contribution saves you between $840 and $1,680 depending on your tax bracket. If your employer offers matching contributions, you’re leaving free money on the table by not maximizing this first.

Health Savings Accounts work similarly to retirement accounts but with triple tax advantages: contributions are tax-deductible, growth is tax-free, and withdrawals for qualified medical expenses avoid taxation entirely. For 2025, you can contribute $4,300 for self-only coverage or $8,550 for family coverage. This account compounds over decades, making it far superior to a regular savings account for healthcare costs. The combination of retirement and health savings accounts creates a powerful foundation for tax reduction that most people ignore until their 50s.

Tax credits reduce liability dollar-for-dollar, while deductions only reduce your taxable income. This distinction matters enormously. The Earned Income Tax Credit returns up to $3,733 for eligible workers with one qualifying child, according to IRS data. The American Opportunity Tax Credit provides up to $2,500 per student for education expenses in the first four years of college, with 40% of the credit refundable. If you have dependents, the Child Tax Credit reduces your liability by $2,000 per child under 17. Many eligible filers simply don’t claim these credits because they assume they don’t qualify. Use the IRS Interactive Tax Assistant to verify your eligibility-it takes minutes and often reveals credits worth thousands.

Business owners and self-employed workers should maximize deductible expenses without hesitation. Home office deductions allow you to write off either actual expenses proportional to your workspace or a simplified $5 per square foot method up to 300 square feet. Vehicle expenses, supplies, professional development, and insurance all reduce your net profit, which directly lowers both income tax and self-employment tax. The self-employment tax alone runs 15.3%, so every legitimate business expense provides significant relief.

How you organize your business shapes your tax outcome dramatically. A sole proprietorship files on Schedule C and pays self-employment tax on all net profit. An S-corporation allows you to take a reasonable salary and distribute the remainder as a dividend, avoiding self-employment tax on that portion. An accountant’s analysis often shows that S-corp status makes sense once net business income exceeds $60,000 to $80,000 annually. LLCs taxed as S-corporations, partnerships, and C-corporations each carry different tax consequences depending on your specific situation. This isn’t a one-size-fits-all decision, and choosing wrong costs thousands annually. The decision should be revisited annually since your income changes and tax laws shift.

Investment accounts also deserve attention. Tax-loss harvesting lets you sell investments at a loss to offset capital gains, reducing your taxable gain by up to $3,000 per year against ordinary income, with unlimited carryforward of excess losses. 529 college savings plans grow tax-free and allow tax-free withdrawals for qualified education expenses, with state deductions available in many states. These accounts separate from your regular brokerage and shield your education savings from current-year taxation. The complexity of choosing the right business structure and investment strategy makes professional guidance valuable-this is where a tax professional helps you avoid costly mistakes and identify opportunities specific to your situation.

Tax planning that happens only in December or January costs you thousands in missed opportunities. Your tax situation shifts throughout the year as income fluctuates, major expenses arise, and new legislation takes effect. Treat tax planning as an ongoing process rather than an annual event. Your W-2 income might be predictable, but bonus payments, investment gains, or business income shifts your bracket position and changes which strategies actually benefit you.

Check your withholdings quarterly by reviewing your recent pay stubs and calculating whether you’re on track to owe or receive a refund. If you consistently receive large refunds above $1,000, you’re giving the government an interest-free loan. Increase your W-4 withholding allowances to keep more money in your paycheck now. If you face an unexpected tax bill in April, adjust your withholding immediately rather than waiting until next year.

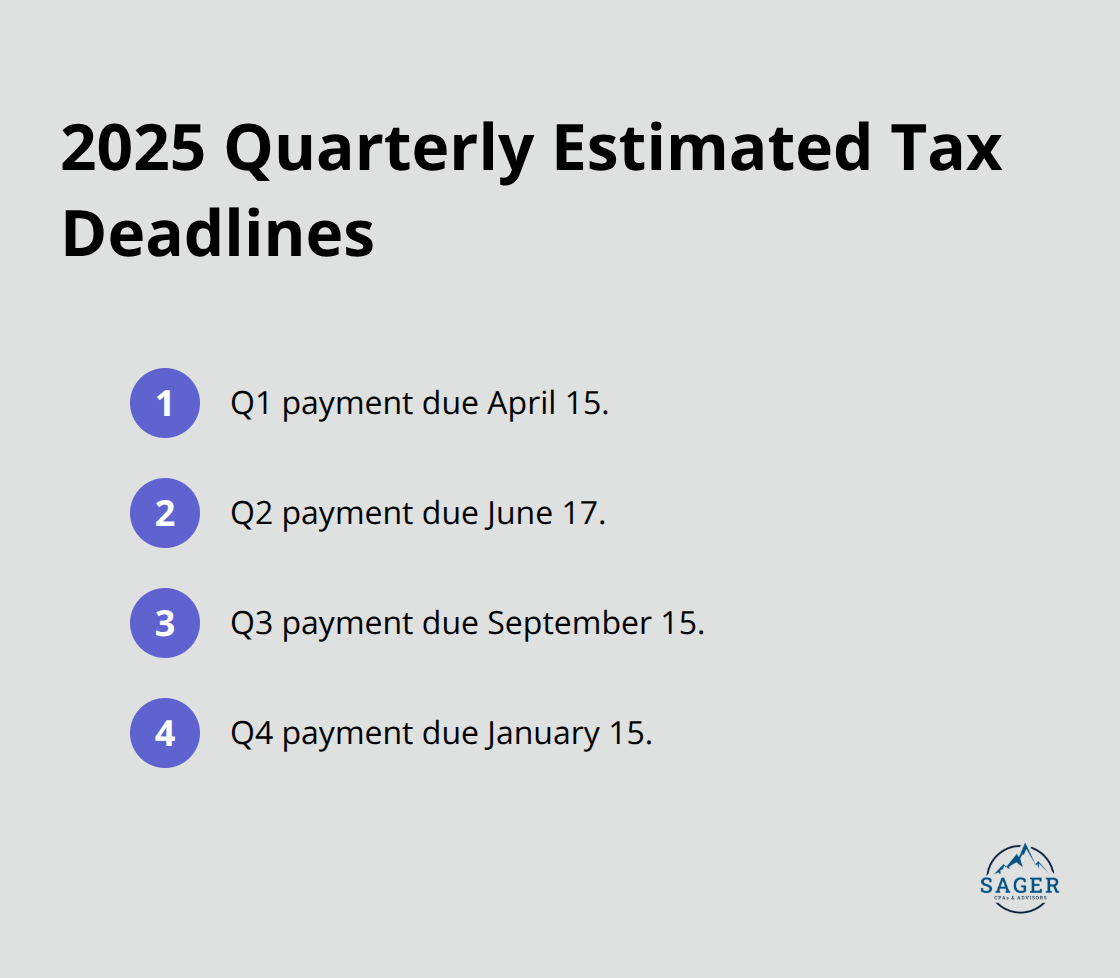

Self-employed workers and those with variable income must make estimated tax payments quarterly on April 15, June 17, September 15, and January 15. The IRS assesses penalties and interest charges on underpayments, so these deadlines matter. Skipping even one payment triggers unnecessary costs that reduce your bottom line.

Major expenses and purchases deserve strategic timing because their tax impact depends entirely on when you claim them. Charitable donations, medical procedures, property tax payments, and business equipment purchases can shift between years to maximize deductions in high-income years. If you’re self-employed and plan to buy office equipment in late December, accelerate that purchase into the current year to claim the deduction sooner and reduce your current-year profit. If you face an unusually high income year due to a bonus or investment gain, delay discretionary business expenses until January to position yourself better overall.

State tax law changes happen throughout the year. The recent One Big Beautiful Bill permanently extended certain tax cuts and increased the SALT deduction cap to $40,000 total for state and local taxes. These shifts affect which strategies work for your specific situation.

Document every deductible expense as it occurs rather than scrambling to reconstruct receipts in March. Keep digital copies of charitable donation confirmations, medical expense receipts, home office utility bills, and vehicle mileage logs. The IRS expects documentation to support any deduction you claim, and lacking it means losing the benefit entirely.

Set up a simple system now-a folder on your computer or a spreadsheet-that captures expenses in real time. This approach takes five minutes per week and eliminates the panic of tax season. You’ll have everything organized when you file, and you’ll spot additional deduction opportunities you might otherwise miss.

Reducing your tax liability legally comes down to three things: knowing what’s available, acting before year-end, and getting professional guidance tailored to your situation. The strategies in this guide work because they rest on actual tax law, not guesswork. Retirement contributions, tax credits, business deductions, and strategic timing compound over years to create substantial savings.

Proactive tax planning means reviewing your situation quarterly, not just in April. You need to understand your bracket position and how each deduction or credit affects your bottom line. You must document expenses as they happen and stay aware of tax law changes that shift which strategies benefit you most. The difference between someone who saves $2,000 and someone who saves $8,000 often comes down to whether they planned ahead or waited until the last minute.

Your specific situation is unique, and your income sources, family structure, business organization, and financial goals all shape which tax liability reduction strategies deliver the biggest impact. We at Sager CPA help individuals and businesses navigate this complexity through strategic tax planning and customized action plans. Schedule a consultation with us to create a personalized financial strategy that reduces your tax burden while keeping everything legal and documented.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.