Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Running a business across borders means navigating complex tax rules in multiple countries. The difference between a smart tax strategy and a costly mistake often comes down to understanding real-world international tax planning examples and how to apply them to your situation.

At Sager CPA, we’ve helped countless businesses reduce their tax burden while staying fully compliant. This guide walks you through proven strategies that actually work.

International tax planning isn’t about finding loopholes. It’s about understanding how tax treaties eliminate double taxation and then structuring your operations to legally minimize what you owe across multiple jurisdictions. Tax treaties between countries form the backbone of this strategy. The US-Canada tax treaty, for example, allows Canadian residents working temporarily in the US to avoid US taxation if they meet specific conditions like the 183-day limit. These agreements reduce withholding taxes on dividends, interest, and royalties, which directly improves cash flow for cross-border operations. The OECD BEPS framework shapes how these treaties work today, and staying aligned with these standards isn’t optional-it’s how you avoid costly disputes with tax authorities.

Compliance requirements vary dramatically by jurisdiction. Jamaica’s experience demonstrates this reality: over a decade of capacity-building strengthened their tax authority’s ability to handle complex transfer pricing cases, increasing compliance and revenue collection. This tells you that tax authorities worldwide are getting better at detecting aggressive planning. Your documentation needs to prove that every intercompany transaction follows the arm’s length principle-meaning related parties price goods and services the same way independent companies would. Coca-Cola faced substantial IRS disputes in 2020 over transfer pricing, underscoring how critical robust documentation becomes during audits.

Identifying tax optimization opportunities requires mapping where your income actually gets taxed. If you earn income in a high-tax country but can shift some to a lower-tax jurisdiction through legitimate business operations, that’s optimization. Transfer pricing between subsidiaries represents the most common lever: a manufacturing subsidiary in one country sells to a distribution subsidiary in another at an intercompany price that reflects real market conditions. The price in your supply chain needs benchmarking against comparable independent transactions to withstand scrutiny.

The practical reality is that customs duties and income tax rates both influence this decision. Country A might have a 25% corporate rate while Country B sits at 15%, but if Country B imposes a 10% tariff on imports, your total cost structure changes. Structuring operations for tax efficiency means aligning your legal entity type, financing method, and location decisions with these rates.

Establishing operations in low-tax jurisdictions only works when substance backs it up. The Dutch Sandwich structure-using holding companies across the Netherlands and Ireland-once offered significant tax savings but has lost viability under BEPS scrutiny. Modern planning requires genuine business operations, not just paper structures. Tax authorities now examine whether your operations in a jurisdiction involve real employees, actual management decisions, and legitimate business functions.

Timing income recognition and deductions across multiple countries demands attention to local rules. Some jurisdictions let you expense research and development immediately; others require capitalization and amortization over years. Section 174 in the US allows full expensing of domestic R&D but requires 15-year amortization of foreign R&D, so mapping your R&D spend between locations directly impacts your tax outcome. These timing differences create planning opportunities when you structure your operations with this knowledge from the start.

The rules governing international tax planning change constantly and interact in ways that aren’t obvious without deep experience across jurisdictions. Understanding transfer pricing documentation, entity structuring, and timing strategies positions you to move forward with confidence into the specific strategies that deliver real results.

Transfer pricing sits at the center of any serious international tax plan, and getting it wrong costs money fast. The arm’s length principle requires that related companies price transactions the same way unrelated companies would, but finding that price demands real transfer pricing benchmarking against comparable independent deals. A manufacturing subsidiary selling to a distribution subsidiary at $1,100 per unit sounds straightforward until you factor in tariffs, local tax rates, and documentation requirements that tax authorities scrutinize heavily.

The manufacturing country might tax corporate income at 25% while the distribution country taxes at 15%, but if tariffs add 10% to the import cost, your total landed expense shifts dramatically. This is where substance matters: Zambia established a dedicated transfer pricing unit and saw significant revenue gains, demonstrating that tax authorities worldwide now possess the expertise to challenge weak pricing justifications. Your intercompany agreements need contemporaneous documentation showing cost structures, market comparables, and the business rationale for your pricing. Without this, you face not just adjustments but penalties that compound quickly.

Map every intercompany transaction, benchmark it against real market data, and document why your price reflects what independent parties would negotiate. This straightforward action protects you far better than any aggressive structure built on paper alone.

Timing income and deductions across jurisdictions creates genuine planning opportunities when you understand the specific rules in each country. The US permits full expensing of domestic research and development costs but requires 15-year amortization of foreign R&D, so a company with both domestic and international research operations can accelerate deductions at home while deferring them abroad. Similarly, some jurisdictions allow immediate expense recognition for certain costs while others mandate capitalization, creating natural timing differences you can leverage.

The OECD BEPS framework and recent reforms like those addressing the Pillar Two global minimum tax at 15% mean that aggressive timing strategies face headwinds, but legitimate timing optimization aligned with real business operations remains viable. The key distinction: timing that follows genuine business decisions withstands scrutiny, while timing designed purely for tax reduction invites challenge.

Establishing operations in low-tax jurisdictions requires actual business substance, not just paper entities. Tax authorities examine whether your operations involve real employees making actual decisions, legitimate management functions, and genuine business activity. The Dutch Sandwich structure once thrived on minimal substance but collapsed under BEPS scrutiny because it lacked real operational depth.

Modern planning succeeds when your location decision aligns with where your actual business happens. If you manufacture in one country, distribute in another, and hold intellectual property in a third, each location needs employees, functions, and decision-making authority that justify its existence to a tax auditor. This substance-first approach protects your structure far better than aggressive strategies built on paper alone.

The complexity of these strategies-transfer pricing, timing optimization, and operational substance-reveals why many businesses struggle to implement them correctly without expert guidance. Understanding what works in theory differs sharply from executing it across multiple jurisdictions with different rules, audit practices, and enforcement priorities.

Most businesses that stumble in international tax planning fail not because they lack ambition-they fail because they treat tax law as static when it constantly changes. Tax regulations shift across jurisdictions, and what worked last year may trigger penalties this year. The OECD BEPS framework continues to evolve, countries implement new rules like Pillar Two’s 15% global minimum tax across more than 135 jurisdictions, and anti-hybrid regulations like Germany’s Zinsschranke and Italy’s guidance issued in 2025 reshape how cross-border financing works. A company that structured operations around 2023 rules without monitoring 2025 changes now faces exposure it never anticipated.

Tax authorities in Jamaica, Zambia, Uganda, and across West Africa spent the last decade building specialized units specifically to detect transfer pricing manipulation and international tax avoidance. Your competitor’s aggressive structure from three years ago doesn’t just fail under current scrutiny-it invites examination of your entire operation. The only defense is systematic monitoring of rule changes in every jurisdiction where you operate and immediate reassessment of your structure when regulations shift.

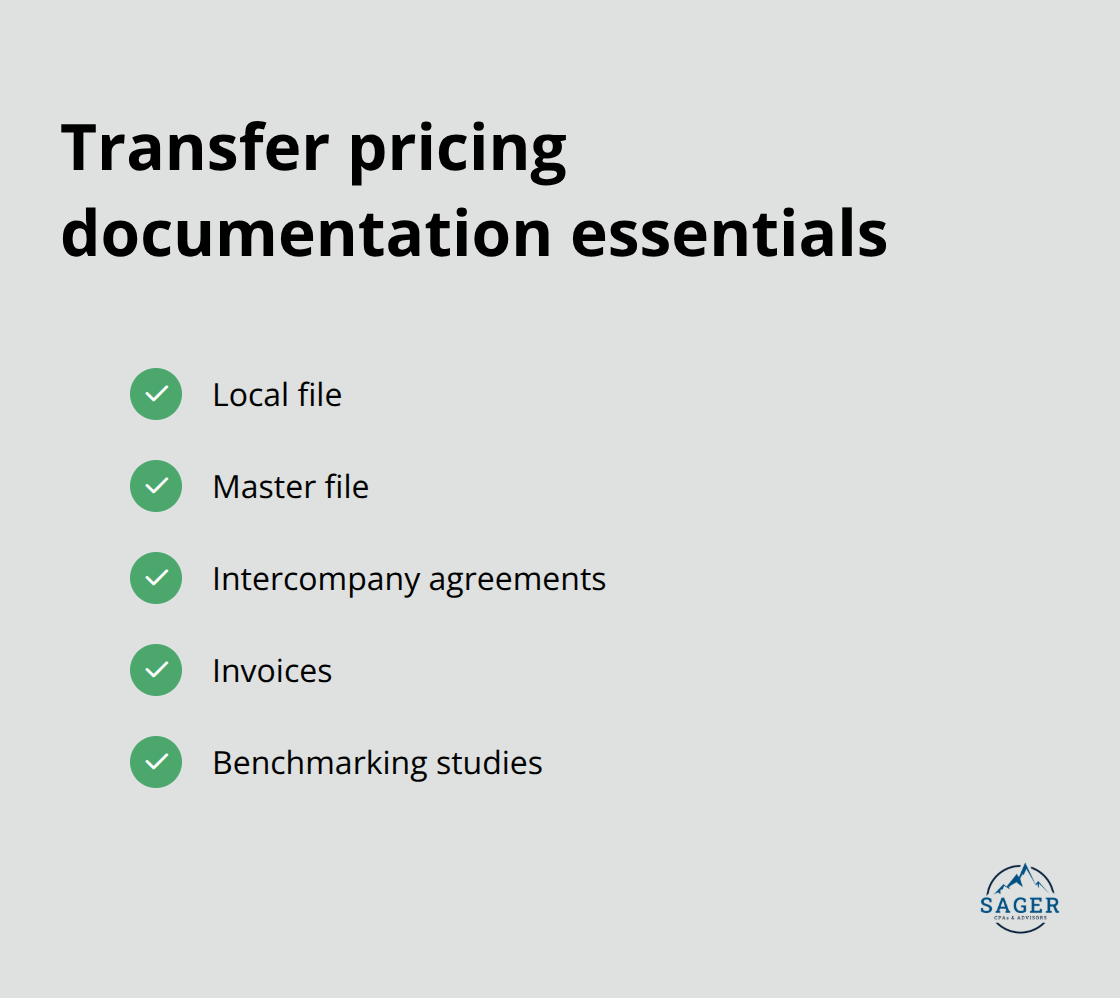

Hidden compliance costs and documentation failures destroy more international tax plans than any single aggressive strategy. When the IRS audited Coca-Cola’s transfer pricing, the dispute didn’t hinge on whether the company intended to avoid taxes-it hinged on whether contemporaneous transfer pricing documentation proved the pricing reflected arm’s length standards. Tax authorities worldwide now require contemporaneous transfer pricing documentation including local files, master files, intercompany agreements, invoices, and benchmarking studies that prove your prices match what independent parties would negotiate.

Penalties for missing or inadequate documentation run steep: the IRS can assess 40% accuracy-related penalties on transfer pricing adjustments, and some jurisdictions impose even harsher consequences. The real cost isn’t just the tax bill-it’s the accounting fees to reconstruct documentation after the fact, the penalties that compound the adjustment, and the years consumed in dispute resolution. A manufacturing company that failed to maintain benchmarking studies for intercompany pricing discovered during audit that reconstructing comparable market data cost $80,000 in professional fees alone before penalties were even calculated.

The solution demands discipline: establish intercompany agreements before transactions occur, commission benchmarking studies annually, maintain detailed cost allocations, and create a filing system that survives a tax authority request. This isn’t bureaucracy-it’s the difference between a defensible position and financial devastation when auditors arrive.

Documentation that proves your transfer prices reflect real market conditions (supported by comparable independent transactions) protects you far more effectively than any aggressive structure built on paper alone.

International tax planning examples show that businesses succeed when they combine three core elements: understanding the rules, documenting everything, and adapting when regulations shift. Coca-Cola’s transfer pricing disputes, Zambia’s revenue gains from dedicated transfer pricing units, and Jamaica’s decade-long capacity-building all prove that tax authorities worldwide now possess the expertise to challenge weak justifications. Your competitive advantage comes from treating international tax planning as an ongoing discipline rather than a one-time project.

Working with tax experts matters because the cost of mistakes far exceeds the investment in professional guidance. A single transfer pricing adjustment can trigger penalties exceeding 40% of the disputed amount, plus accounting fees to reconstruct documentation after the fact. Tax rules shift constantly across jurisdictions-Pillar Two’s 15% global minimum tax now applies across more than 135 countries, Germany’s Zinsschranke and Italy’s anti-hybrid guidance reshaped 2025 planning, and BEPS continues evolving.

Map your current cross-border operations, identify where income gets taxed, and assess whether your transfer pricing, entity structure, and timing decisions align with current rules. We at Sager CPA help businesses implement customized tax planning strategies that reduce liabilities while maintaining full compliance. Schedule a consultation to review your international tax position and create a personalized strategy tailored to your specific operations across jurisdictions.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.