Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Most young adults graduate college with little to no experience managing their own finances. The average 22-year-old carries $37,000 in student debt while earning just $35,000 annually.

We at Sager CPA see countless young professionals struggle with budgeting for young adults because they never learned the fundamentals. This guide breaks down the exact steps to build a budget that actually works for your lifestyle and income level.

Most young adults make a critical error when they budget: they use their gross salary instead of their actual take-home pay. Your true monthly income is what hits your bank account after taxes, health insurance, 401k contributions, and other deductions.

A $50,000 annual salary typically becomes $3,200 monthly after deductions, not the $4,167 you might expect. Examine your most recent pay stub and multiply your net pay by the number of paychecks per month.

Add all income sources like side gigs, freelance work, or part-time jobs, but only count money you actually receive. Many young adults forget about irregular income streams that can boost their monthly totals.

Skip the guesswork and track your actual spending for exactly two weeks. Download your bank statements and credit card transactions, then categorize every expense.

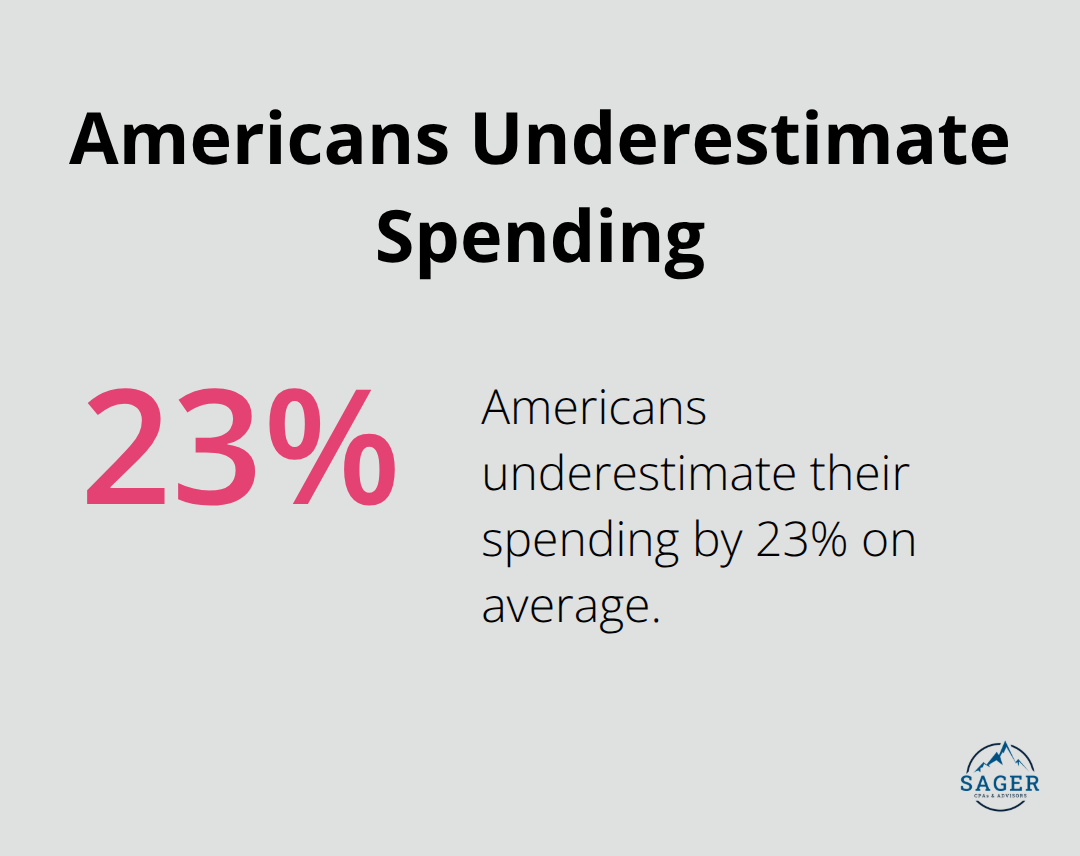

The Federal Reserve reports that Americans underestimate their spending by 23% on average. Use a simple spreadsheet or apps like Mint to record everything from your $5 coffee to your $1,200 rent payment.

This exercise reveals spending patterns you never noticed. After 14 days, multiply your totals by 2.17 to estimate monthly expenses.

Fixed costs like rent, insurance, and loan payments stay the same each month, while variable expenses like groceries, entertainment, and gas fluctuate. Separate these categories because they require different strategies.

Fixed expenses should consume no more than 60% of your net income to maintain financial flexibility. This foundation sets you up to apply proven methods that transform chaotic spending into organized financial control.

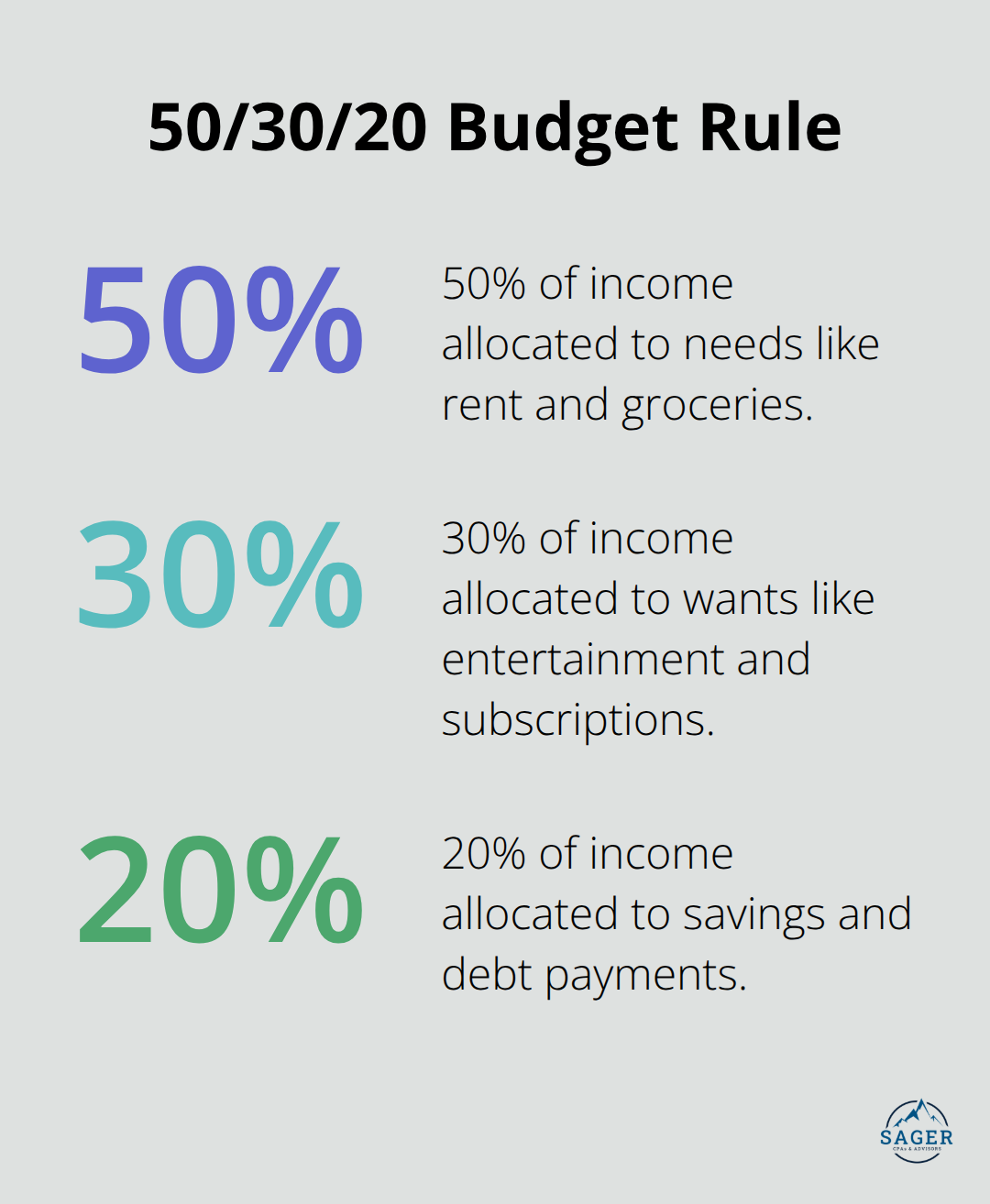

The 50/30/20 rule provides the most practical foundation for young adults who want immediate budget success. Allocate 50% of your net income to needs like rent and groceries, 30% to wants like entertainment and subscriptions, and 20% to savings and debt payments. This framework works because it acknowledges that young adults need flexibility while they build financial discipline.

NerdWallet advocates the 50/30/20 budget with this formula for take-home pay allocation. Calculate these percentages with your true monthly income from the previous step. If your net pay is $3,200, you have $1,600 for needs, $960 for wants, and $640 for savings and debt.

Manual budgets fail because they rely on willpower alone. Set up automatic transfers for your savings the day after each paycheck arrives. Most banks allow you to create recurring transfers between accounts for free (check with your specific bank for details).

Automate at least 10% of your income into a high-yield savings account like Marcus by Goldman Sachs or Ally Bank, which currently offer rates above 4%. The Federal Reserve notes that having savings helps families cope with income fluctuations and unexpected expenses.

Skip complex spreadsheets and use proven apps that sync with your bank accounts. YNAB costs $14 monthly but forces you to assign every dollar a job before you spend it. Mint offers free expense tracking with automatic categorization, while PocketGuard shows exactly how much you can spend after you cover bills and savings goals.

These apps eliminate the math and provide instant alerts when you approach category limits. The key is consistency rather than perfection in your first few months.

Your first budget won’t be perfect, and that’s normal. Track your actual spending against your planned categories for 30 days, then adjust the percentages based on reality. If you consistently overspend on groceries but underspend on entertainment, shift money between categories.

Most young adults need 2-3 months to find their ideal allocation. The important step is to start with the 50/30/20 framework and modify it based on your actual patterns. Even experienced budgeters face challenges when their spending habits don’t match their initial plans, which leads us to the most common mistakes that derail new budgets.

The biggest budget killers aren’t the obvious expenses like rent or car payments. Small daily purchases destroy more budgets than any single large expense. A $4 daily coffee costs $1,460 annually, while a $12 lunch habit consumes $3,120 per year.

The Bureau of Labor Statistics shows that Americans aged 25-34 spend $3,526 annually on food away from home, yet most budgets allocate only $1,800 for this category. Track every purchase under $20 for one week and multiply by 52 to see your real annual impact. These micro-expenses add up faster than most young adults realize.

Young adults set themselves up for failure when they create budgets that require monk-like discipline. You allocate $200 monthly for entertainment when you currently spend $500, which guarantees failure within two weeks.

The American Psychological Association research shows that extreme restriction triggers binge behavior in 78% of people who attempt lifestyle changes. Start when you cut your current expenses by 15% rather than 50%. If you spend $800 monthly on entertainment, try $680 first. Success builds momentum better than perfection builds frustration.

Most financial advice tells young adults to pay off debt before they save, but this creates dangerous financial vulnerability. Without an emergency fund, one car repair or medical bill forces you back into debt.

Prioritize $1,000 in emergency savings before aggressive debt payments, even if your credit cards charge 22% interest. The Federal Reserve found that 40% of Americans cannot cover a $400 emergency expense (which explains why 43% of young adults return to credit card debt within six months of payment). Build your safety net first, then attack high-interest debt with clarity in financial management.

Budgeting for young adults becomes manageable when you follow these proven steps: calculate your true net income, track expenses for two weeks, and apply the 50/30/20 framework with automated savings transfers. Most young adults who stick to these fundamentals see financial improvements within 60 days. The process requires consistency rather than perfection in your first few months.

Consistent financial habits create compound benefits beyond immediate budget control. You build emergency funds that prevent debt cycles, establish credit habits that save thousands on future loans, and develop money management skills that last decades. The Bureau of Labor Statistics shows that adults who budget in their twenties accumulate 40% more wealth by age 40 compared to non-budgeters (a significant long-term advantage).

Your next step involves choosing digital tools that sync with your accounts and setting up automatic transfers this week. Start with the basics today and adjust your approach as your income and goals evolve. If your financial situation becomes complex or you need strategic tax planning guidance, Sager CPA offers personalized financial strategies to help you build long-term financial stability.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.