Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Most entrepreneurs focus on growing revenue but ignore the tax strategies that could save them thousands annually. At Sager CPA, we’ve seen business owners leave money on the table simply because they didn’t plan ahead.

The right tax moves-from choosing your business structure to maximizing deductions-can dramatically reduce what you owe. This guide covers the entrepreneur tax planning strategies that actually work for growing businesses.

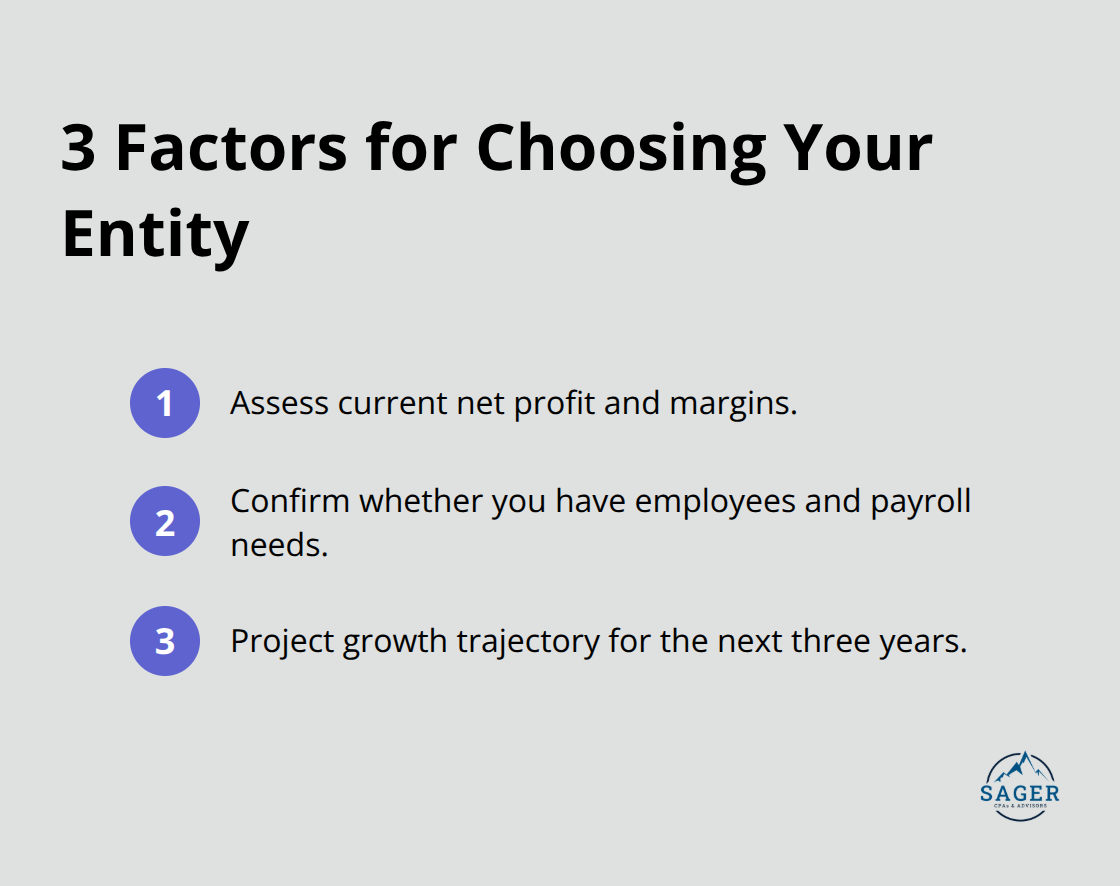

The structure you choose for your business determines how much you pay in taxes each year. Most entrepreneurs pick a structure based on liability protection alone and completely miss the tax angle. That’s a costly mistake. An S Corporation can save you tens of thousands annually compared to an LLC taxed as a sole proprietorship, but only if your income level justifies the added complexity. Evaluate your structure based on three concrete factors: your net profit, whether you have employees, and your growth trajectory over the next three years.

S-Corps split your profit into salary and distributions, which reduces self-employment tax on the distribution portion. Self-employment tax runs 15.3 percent on net earnings, so the savings add up fast. If you earn $120,000 in net profit and elect S-Corp status, you might pay yourself a reasonable salary of $60,000 and take $60,000 as a distribution. That distribution avoids the 15.3 percent self-employment tax, saving roughly $9,180 annually. However, S-Corps require payroll processing, quarterly filings, and a separate tax return, which costs $1,500 to $3,000 per year in accounting and compliance fees. The break-even point sits around $60,000 to $80,000 in net profit. Below that threshold, the compliance costs outweigh the tax savings. Above that threshold, the math works decisively in your favor. Many solopreneurs earning $50,000 stay as LLCs because S-Corp overhead destroys the benefit. Conversely, service businesses with $150,000-plus in profit almost always benefit from S-Corp status.

Switching from an LLC to an S-Corp mid-year or changing from a C-Corp to an S-Corp triggers tax reporting complications that many business owners underestimate. The IRS treats conversions differently depending on your prior structure. If you operated as a sole proprietor or partnership and elect S-Corp status, the transition is relatively clean. If you operated as a C-Corp and convert to S-Corp, you face potential double taxation on built-in gains for five years after the election. One manufacturing business converted from C-Corp to S-Corp without understanding this rule and faced a $45,000 unexpected tax bill when they sold inventory at a gain. The timing of a structure change matters enormously. An election filed in January positions you to capture the full year of savings. An election filed in October means you only benefit for three months and still incur the year-round compliance burden. If you’re considering a change, plan it for January and coordinate with your accountant to file the election properly by March 15 of the following year.

As your business scales, your tax situation becomes more complex. The structure that worked at $80,000 in profit may not work at $250,000. Higher income levels unlock additional tax planning opportunities through retirement contributions, qualified business income deductions, and strategic expense timing. Your accountant should review your structure annually and model the tax impact of staying put versus making a change. This forward-looking approach prevents you from overpaying taxes in years when a structure shift would have saved substantially.

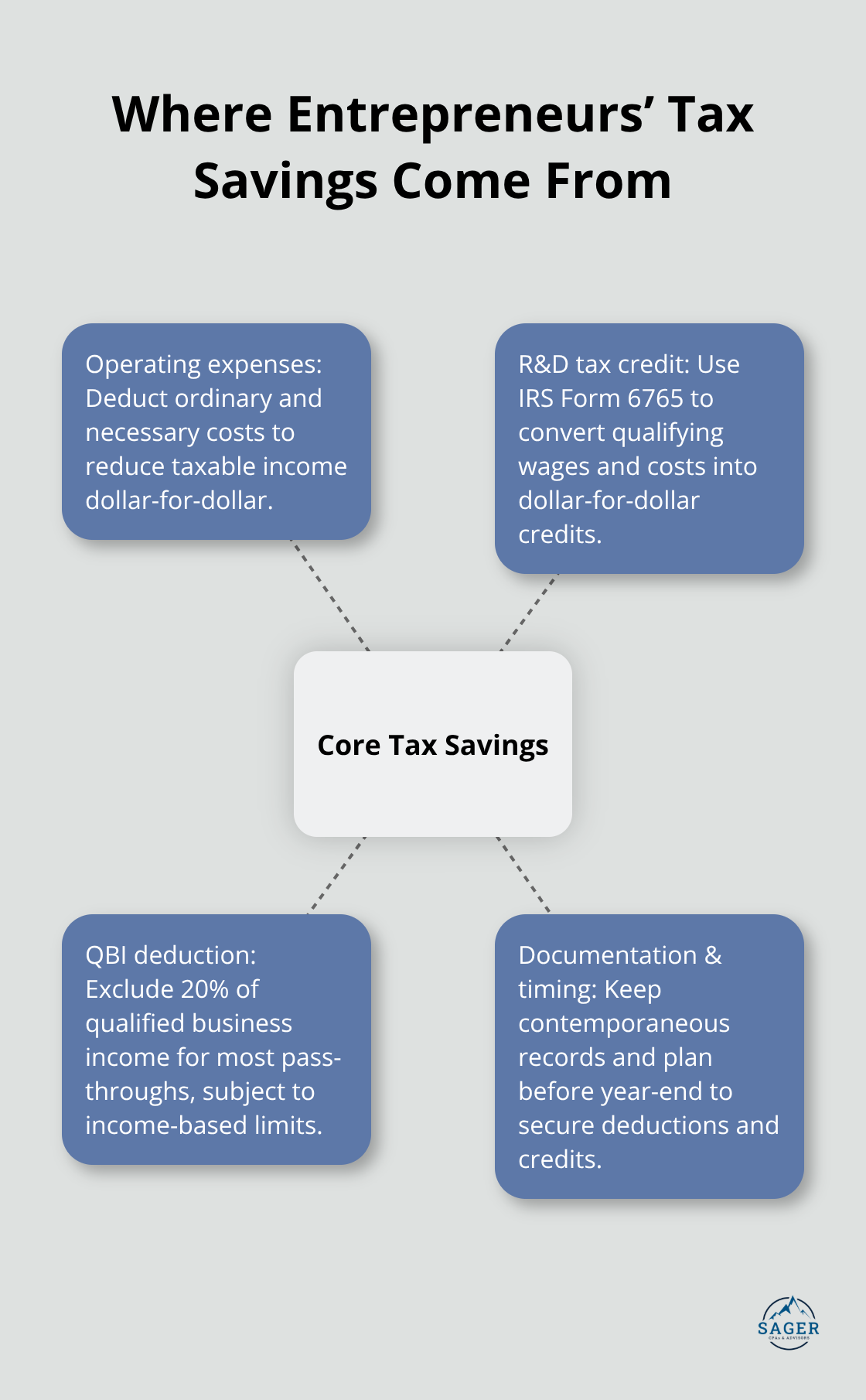

Most business owners treat taxes as an April problem. That mindset costs them thousands. The actual tax savings come from three places: operating expenses you already spend money on but fail to deduct, research and development work you already perform but never claim credits for, and the qualified business income deduction that most pass-through entities qualify for but don’t optimize. We see this pattern repeatedly. A service business owner deducts $15,000 in home office expenses when they could legitimately claim $28,000. A software company invests $80,000 in product development but never files for the R&D tax credit. A consulting LLC earns $200,000 and pays full self-employment tax on all of it despite qualifying for a 20% business income deduction that could save $6,000 annually.

These aren’t theoretical gaps-they represent concrete money left on the table.

Your operating expenses reduce your taxable income dollar-for-dollar. That $5,000 software subscription, the $2,400 annual equipment maintenance, the $1,200 professional development course, the $800 in office supplies-all count. The IRS requires deductions to be ordinary and necessary for your business, but that bar is low if you genuinely use the expense. Most entrepreneurs make mistakes with timing and documentation. For cash-basis businesses, you can accelerate expenses into December to lower this year’s taxable income. One creative agency prepaid $6,000 in annual software subscriptions in late December instead of spreading them across the year. That single move dropped their tax bill by roughly $1,500. You must actually have the expense in December-you cannot manufacture fake deductions. But if you were going to spend the money anyway, moving the payment date forward captures the deduction sooner.

Home office deductions work the same way but require stricter rules. You can deduct a portion of your rent, utilities, internet, and depreciation if you use a dedicated space exclusively for business. The IRS allows two methods: the simplified method at $5 per square foot (up to 300 square feet for a maximum $1,500 deduction) or the actual expense method where you calculate the percentage of your home used for business and deduct that percentage of all household expenses. A freelancer with a 200-square-foot dedicated office claims $1,000 annually under the simplified method with zero documentation beyond your lease and a measurement. The actual expense method works better for larger spaces or high-cost areas. A consultant in San Francisco with a 400-square-foot home office could legitimately deduct $800 monthly in rent plus utilities and internet, totaling $12,000 annually. The difference between claiming nothing and claiming $12,000 is $3,000 to $4,000 in annual taxes. Most home-based entrepreneurs claim nothing because they fear IRS scrutiny. That fear is overblown. The deduction is legal and common. Document your square footage, your total home expenses, and the percentage used for business, and you’re covered.

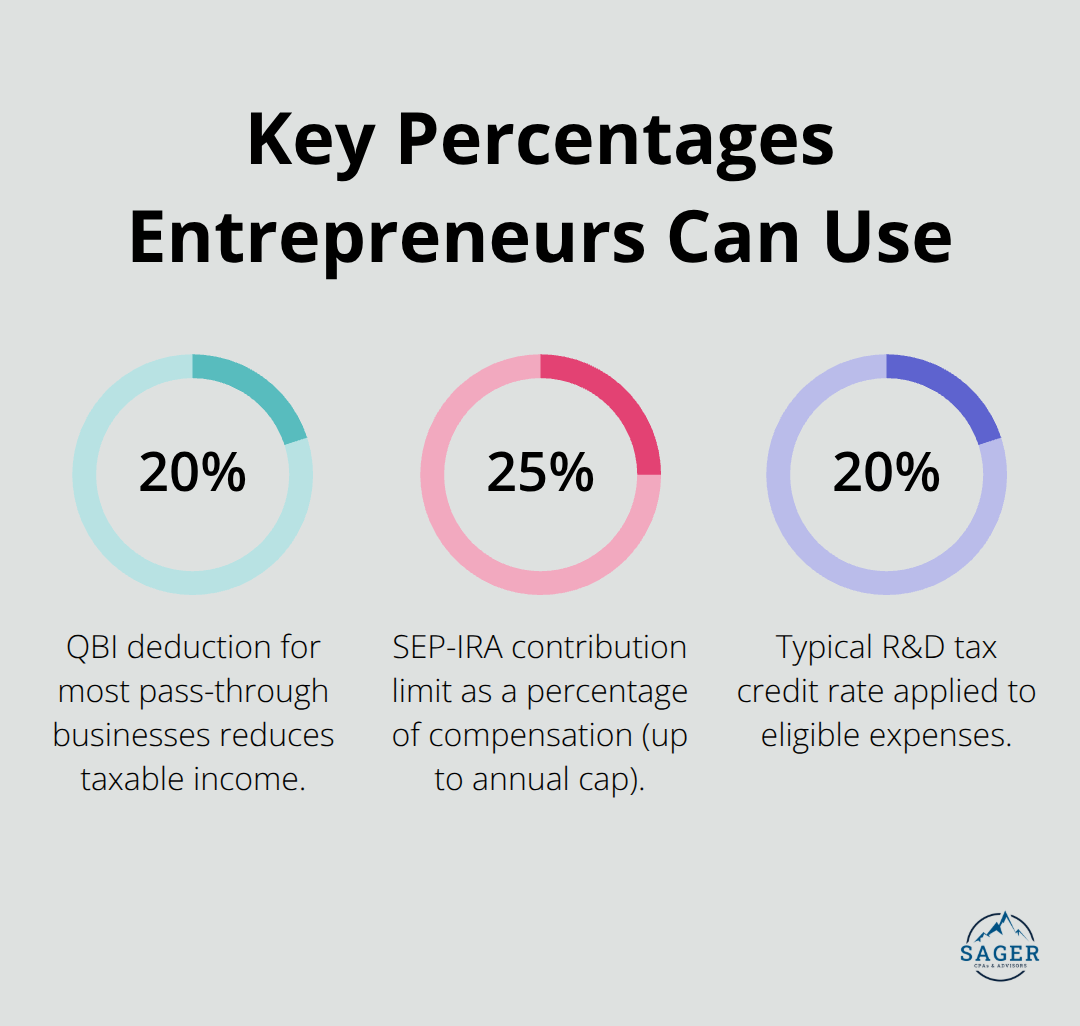

If your business involves creating software, designing products, improving processes, or solving technical problems, you likely qualify for the R&D tax credit. This credit is not a deduction-it directly reduces your tax bill dollar-for-dollar. Businesses can claim the R&D tax credit by filing IRS Form 6765, which requires determining which expenses qualify and maintaining adequate documentation. A software development company with four engineers earning $80,000 each spends $320,000 on wages alone. If 70% of their work involves developing new features or improving the platform, that’s $224,000 in potentially eligible wages. At a 20% credit rate, that translates to $44,800 in tax savings. Most small tech companies never claim this credit because they assume it only applies to pharmaceutical companies or aerospace firms. That assumption is wrong. Any business engaged in developing or improving a product or process qualifies. A digital marketing agency that built custom software for client reporting claimed $18,000 in R&D credit. A manufacturing business that redesigned their production process to reduce waste claimed $12,000. The barrier to claiming the credit is documentation. You need contemporaneous records showing what work was performed, how much time employees spent on qualifying activities, and which costs were directly tied to the research. Many businesses fail IRS scrutiny because they lack this documentation. Start tracking now if you want to claim the credit. Have employees log time spent on research activities separately from client work. Keep records of supplies purchased for research. Document the technical challenges you faced and how you overcame them. If you’ve been running a qualifying business for multiple years without claiming the credit, you can file an amended return back to 2022 for small businesses, potentially recovering tens of thousands in overpaid taxes.

If your business is structured as an S-Corp, LLC, partnership, or sole proprietorship, you likely qualify for the qualified business income deduction. This deduction allows you to exclude 20% of your qualified business income from federal tax. A consulting LLC earning $150,000 in profit can deduct $30,000, reducing taxable income to $120,000. At a 32% combined federal and state tax rate, that saves $9,600 annually. The deduction is permanent under current tax law and applies automatically to most service businesses, though some service businesses face restrictions based on income level. The real opportunity lies in entity structure and income splitting. If you operate as a sole proprietor earning $200,000, you pay tax on all $200,000 and claim a $40,000 deduction. If you restructure as an S-Corp, pay yourself a $120,000 salary, and take $80,000 as distributions, you pay self-employment tax only on the $120,000 salary (saving roughly $9,000), and you still claim the $40,000 QBI deduction on the $200,000 profit. That combination saves $18,000 to $20,000 annually. The interaction between S-Corp structure and QBI deduction is where tax planning happens. Most accountants calculate each benefit in isolation and miss the combined impact. The key is not to chase the QBI deduction in isolation but to pair it with the right business structure for your income level. These three tax savings-operating expenses, R&D credits, and the QBI deduction-form the foundation of smart tax planning. But they only work if you structure your retirement contributions strategically as well.

Retirement contributions represent the most underutilized tax strategy for entrepreneurs. A Solo 401(k) allows you to contribute up to $66,000 in 2025 if you’re under 50, or $73,500 if you’re 50 or older. This is not a deduction that requires extensive documentation or IRS scrutiny. You fund the account, reduce your taxable income dollar-for-dollar, and the money grows tax-deferred. A solopreneur earning $120,000 in net profit who contributes $30,000 to a Solo 401(k) drops their taxable income to $90,000, saving roughly $7,200 in federal and state taxes at a 24% combined rate. That $30,000 contribution happens once per year, takes a few hours to set up, and delivers permanent tax relief.

A SEP-IRA works similarly but has lower contribution limits. You can contribute up to 25% of compensation, capped at $69,000 in 2025. The SEP-IRA requires less paperwork than a Solo 401(k), making it attractive for solopreneurs who want simplicity. However, the Solo 401(k) wins for most entrepreneurs because the contribution limit is higher and you can borrow against the balance if cash flow tightens. The critical timing issue is that most retirement plans must be established before December 31 to claim deductions on that year’s return. A business owner who waits until March to open a Solo 401(k) can still fund it for 2025, but only if they file their tax return late or amend it after filing. That creates unnecessary complexity. Open your plan in November or December, fund it before year-end, and lock in the deduction cleanly on your 2025 return.

The second-order benefit of retirement contributions is that they reduce your self-employment tax and your qualified business income deduction base simultaneously. If you earn $150,000 and contribute $40,000 to a Solo 401(k), your taxable income drops to $110,000. Your self-employment tax is calculated on the reduced amount, saving roughly $4,590 in self-employment taxes. Your QBI deduction of 20% now applies to $110,000 instead of $150,000, a difference of $8,000 in deductible income. Combined, that contribution saves you approximately $11,790 in taxes. Most entrepreneurs see the $9,600 QBI benefit or the $4,590 self-employment tax savings in isolation and miss that both effects stack together.

The math becomes even more powerful when you pair retirement contributions with S-Corp status. An S-Corp earning $200,000 in profit could pay a $120,000 salary and take $80,000 as distributions. That $120,000 salary is subject to self-employment tax, but the $80,000 distribution avoids it entirely, saving roughly $12,240 in self-employment taxes. If you then contribute $40,000 to a Solo 401(k) funded from the business profits, your taxable income drops to $160,000, and your self-employment tax base drops to $80,000. The combination of S-Corp structure and retirement contributions can save $15,000 to $20,000 annually for a business earning $200,000 or more. This is where tax planning stops being theoretical and becomes concrete. The mechanics require coordination between your business structure, retirement plan selection, and contribution timing, which is why working with a qualified advisor during your year-end planning window produces measurable results.

The tax strategies in this guide all share one reality: they demand action before December 31. April filing means you’ve already forfeited thousands in potential savings. The S-Corp election, retirement plan contributions, R&D credit documentation, and expense acceleration all carry hard deadlines that reset annually. Entrepreneur tax planning works because it aligns three decisions at once: your business structure, your retirement contributions, and your deduction strategy.

A business earning $200,000 that pairs S-Corp status with a $40,000 Solo 401(k) contribution and aggressive operating expense deductions saves $18,000 to $22,000 annually compared to a sole proprietor who claims minimal deductions. That difference compounds over five years into six figures of tax savings that fund growth, hiring, or owner distributions. The businesses that win on taxes plan in October and November, not the ones that scramble in March.

Schedule a conversation with a qualified tax advisor who understands your business model and growth trajectory. We at Sager CPA help entrepreneurs build customized tax strategies that reduce what you owe while supporting your long-term financial goals. A year-end planning session typically identifies $5,000 to $20,000 in immediate tax savings and positions your business for sustainable growth.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.