Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Most business owners and high-income earners leave thousands of dollars on the table each year simply because they lack a structured approach to tax planning. A one-size-fits-all strategy won’t work when your financial situation is unique.

At Sager CPA, we’ve seen firsthand how tailored tax strategy plans transform the way our clients manage their tax burden. In this guide, we’ll show you exactly how to build a personalized roadmap that works for your specific circumstances.

Most business owners conduct a financial review only when filing their tax return. This reactive approach locks you into the year’s decisions by the time you sit down with a tax professional. Proactive tax planning that happens throughout the year, not in March, reveals specific inefficiencies that a year-end scramble never catches. A comprehensive financial review early in the year uncovers opportunities you’d otherwise miss. You might find that your business structure costs you thousands in unnecessary self-employment tax, or that your timing of income and deductions works against you. For instance, if you’re a cash-basis business with strong profits, you can defer some revenue to the following year while prepaying certain business costs to shift your tax liability and improve cash flow. The IRS allows this strategy, but only if you identify the opportunity before December.

High-income earners often overlook the fact that their deduction strategy leaves money on the table. A proper review examines whether you maximize deductions on equipment and real estate, whether you capture all eligible business expenses, and whether your entity structure aligns with current tax law changes. Structuring your income and deductions requires specificity about your situation, not generic advice. If you own real estate, cost segregation studies accelerate depreciation dramatically. Gas stations qualify for 100% year-one depreciation of the building shell under certain IRS rules, car washes treat building components as 15-year property enabling substantial first-year deductions, and self-storage facilities reclassify internal components as 5-year personal property. These aren’t theoretical benefits; they represent concrete tax reductions available right now under the Omnibus Business and Budget Act.

The R&D Tax Credit matters when your company engages in innovative activities. You can deduct or credit qualifying research and development expenses, but you must document what qualifies before year-end, not scramble to justify it during an audit. Equipment purchases placed in service after January 19, 2025 qualify for 100% bonus depreciation, a change from the 60% available in 2024. If you plan capital equipment purchases, the timing decision directly impacts your tax bill. Charitable contributions also face changing deduction floors starting in 2026: corporations may deduct gifts only above 1% of taxable income, while individuals who itemize face a 0.5% floor.

The number 100% seems to be not appropriate for this chart. Please use a different chart type. Completing gifts in 2025 captures larger deductions before these floors tighten. These timing windows close fast, and missing them costs real money.

The opportunities to reduce your tax burden exist throughout the year, but only if you take action before deadlines pass. The next section examines the planning mistakes that prevent most business owners from capturing these savings.

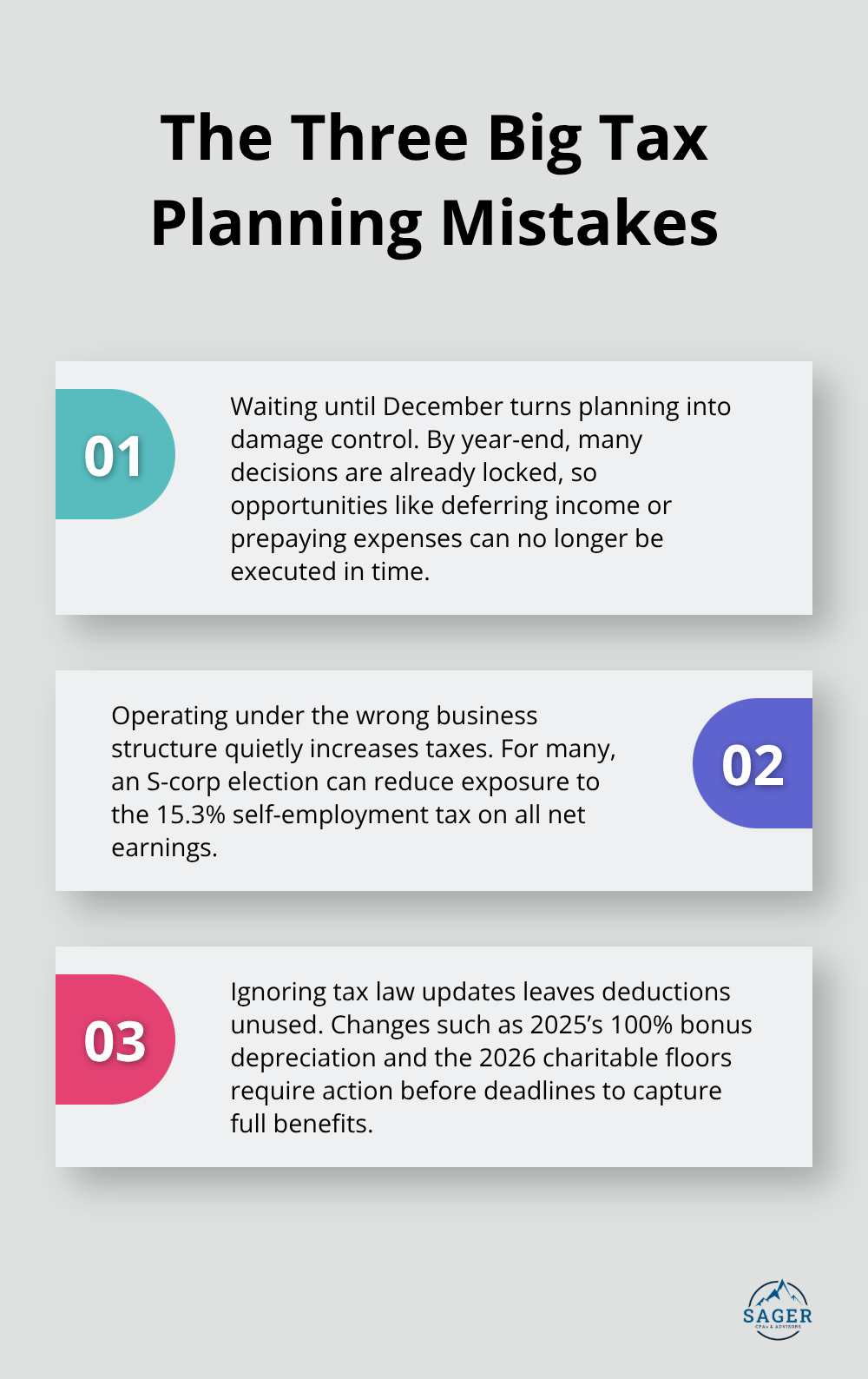

The gap between what you pay in taxes and what you could legitimately owe often comes down to three critical mistakes that business owners make repeatedly.

The first and most expensive mistake is treating tax planning as a December activity instead of an ongoing process. When you wait until year-end to review your finances, you’ve already locked in decisions that cost you money. A business owner who defers revenue to reduce this year’s income needs to make that decision before the transaction closes, not after.

Similarly, prepaying business expenses to shift tax liability only works if you identify the opportunity with time to execute it. The IRS allows these strategies, but the window closes on December 31st.

Clients tell us every January that they wish they’d planned earlier because they missed a $15,000 equipment purchase that would have qualified for 100% bonus depreciation, or they failed to complete charitable contributions before the 2026 deduction floor changes took effect. Once March arrives, that opportunity is gone forever.

The second mistake is running your business in a structure that doesn’t match your actual tax situation. Many business owners operate as sole proprietorships or standard partnerships when an S-corporation election could save them thousands annually in self-employment tax. If you earn $150,000 in net business income and operate as a sole proprietor, you pay self-employment tax on the full amount. Restructuring as an S-corp allows you to take a reasonable salary and distribute the remaining profit as dividends, which avoids self-employment tax on that portion.

The math is straightforward: self-employment tax runs 15.3% on net earnings, so saving even $20,000 from this tax means $3,060 in your pocket. Yet business owners often stick with their original structure out of inertia rather than strategy.

The third mistake is ignoring how tax law changes affect your specific situation. The Omnibus Business and Budget Act raised equipment bonus depreciation from 60% to 100% in 2025, created new R&D deduction rules, and changed charitable contribution floors starting in 2026. If you own rental properties or equipment-heavy operations, these changes directly impact your tax bill, but only if you know they exist and plan accordingly. Businesses that don’t track these changes continue using outdated strategies that leave deductions on the table.

These three mistakes share a common thread: they all stem from a lack of intentional planning. The next section shows you how to build a personalized tax roadmap that prevents these costly errors and positions your finances for real savings.

The gap between knowing you need a tax plan and having one that moves your finances forward comes down to execution. A real tax roadmap requires three concrete steps: understanding exactly where your money sits, deciding what outcomes matter most, and then taking measurable action before tax deadlines arrive. A comprehensive financial review examines your complete situation-not just last year’s tax return, but your business structure, equipment purchases, revenue patterns, charitable contributions, and retirement plan setup. This review identifies specific inefficiencies that generic tax software misses entirely. For example, a business owner earning $200,000 annually might discover that restructuring as an S-corp saves $8,000 to $12,000 annually in self-employment taxes, or that a cost segregation study on a $2 million commercial property accelerates $300,000 in depreciation into year one. These aren’t theoretical numbers; they’re concrete opportunities that exist in your situation right now.

Once you understand what’s possible, goal-setting becomes straightforward. The main goal is short-term reduction of tax liability. You reduce your effective tax rate by a specific percentage, improve cash flow by a target amount, or position yourself for a business sale through entity structure optimization. Try defining measurable objectives tied to actual dollar amounts rather than vague aspirations like “pay less in taxes.” A goal of reducing your federal tax bill by $15,000 annually is actionable; a goal of “tax efficiency” is not. Specific targets force you to prioritize which strategies matter most and allocate resources accordingly.

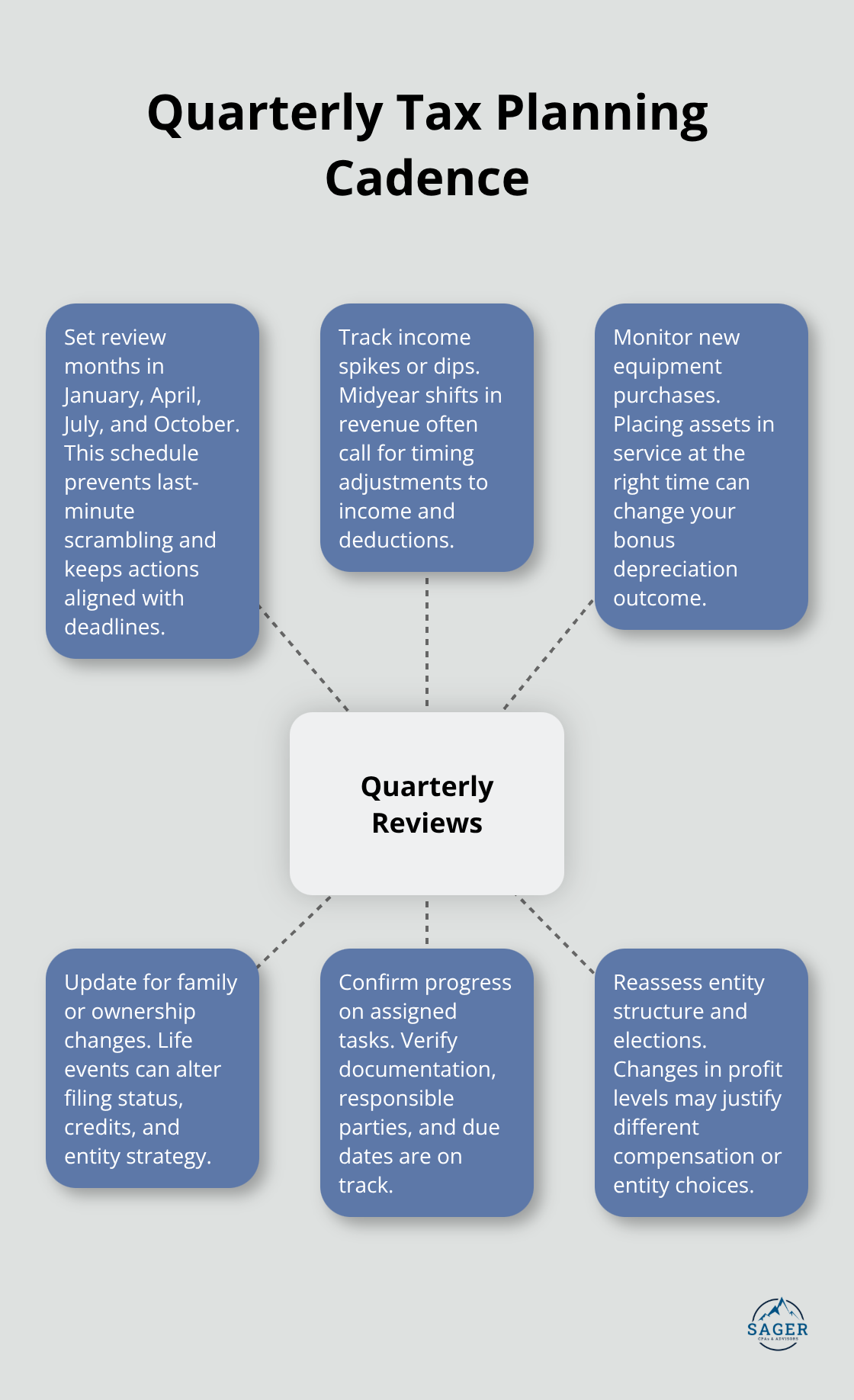

Creating an action plan means identifying which strategies apply to your circumstances and assigning deadlines to each one. If you own equipment-heavy operations, the 100% bonus depreciation available in 2025 requires documenting qualifying purchases before year-end. If you’re planning charitable giving, completing gifts in 2025 captures deductions before the 1% corporate floor and 0.5% individual floor take effect in 2026. If you operate a rental property, determining whether you meet the material participation test (500-plus hours annually required under IRS rules) directly affects whether depreciation losses offset your other income. The action plan should list specific tasks, responsible parties, and hard deadlines.

Quarterly reviews keep the plan on track and catch changes early. A new equipment purchase in October, a significant income spike in Q3, or a change in family circumstances all warrant strategy adjustments before year-end. Scheduling these reviews in January, April, July, and October prevents last-minute scrambling and ensures you make intentional decisions rather than reactive ones.

Many business owners find that this cadence transforms tax planning from an annual burden into an integrated part of financial management. The cost of professional guidance pays for itself when a single strategy saves five, ten, or twenty times the fee you paid for the plan.

Customized tax strategies work because they address your specific situation rather than applying generic rules to unique circumstances. A tailored tax strategy plan that ignores the differences between an equipment-heavy operation, a professional service provider, and a real estate investor leaves money on the table. Tax efficiency comes from intentional planning that happens throughout the year, not from hoping your year-end tax return captures every available deduction.

The math on professional tax planning is compelling. A single strategy-whether restructuring as an S-corp, accelerating depreciation through cost segregation, or timing charitable contributions before deduction floors tighten-often saves multiples of what you pay for expert guidance (business owners who invest in proper planning typically recover their advisory fees within the first year through concrete tax reductions). More importantly, they avoid the costly mistakes that reactive planning creates: missed deadlines, suboptimal business structures, and overlooked law changes that directly impact your bottom line.

Schedule a consultation to review your current situation and identify where a personalized strategy creates real savings. Sager CPA and Advisors specializes in building customized action plans that reduce your tax liability while keeping your finances on solid ground. The conversation itself often reveals opportunities you didn’t know existed.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.