Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Most businesses we work with at Sager CPA have financial records that don’t tell the full story. Inconsistent bookkeeping, misclassified expenses, and missing documentation create blind spots that affect decision-making and stakeholder confidence.

Financial clarity audits fix these problems by identifying errors, strengthening your controls, and creating transparent reporting that actually reflects your business performance.

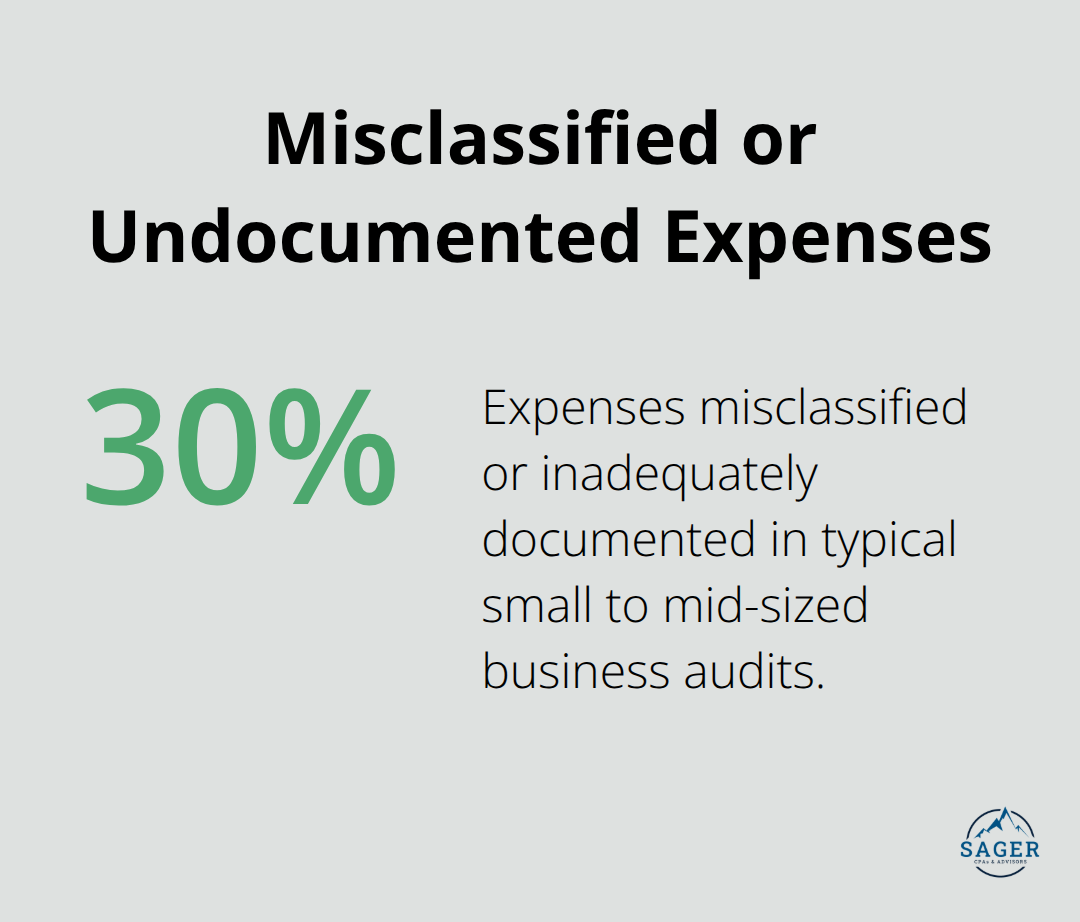

A financial clarity audit exposes problems that spreadsheets and standard bookkeeping miss. Most businesses operate with scattered records across departments, inconsistent account classifications, and transactions that lack proper documentation. An audit systematically examines these gaps and uncovers the real state of your finances. Companies typically find that approximately 30% of their expenses are misclassified or inadequately documented.

This matters because misclassified expenses distort your profitability picture, making it impossible to identify which departments or products actually generate profit. An audit catches these errors before they compound into larger compliance and decision-making problems.

A thorough audit evaluates your internal controls-the systems and procedures that prevent errors and fraud. Weak controls allow mistakes to slip through repeatedly. An auditor tests your approval processes, segregation of duties, and reconciliation practices to identify where controls fail. For example, if one person can approve payments and process them without oversight, that’s a control gap that creates risk. The audit report provides specific recommendations to fix these gaps. Implementing stronger controls reduces the likelihood of costly errors and makes your team more accountable. The cost of fixing controls now is far less than the cost of discovering fraud or major errors later.

When your financial statements are audited and verified, lenders take notice. Banks and credit providers view audited statements as significantly more credible than unaudited statements. This credibility translates into better loan terms and lower interest rates. Investors also prefer audited statements because they reduce perceived risk. If you’re seeking capital investment or planning to sell your business, an independent audit removes doubt about your numbers. Transparent, verified reporting also improves relationships with suppliers and vendors who may offer better payment terms to businesses they trust. Beyond external relationships, audited financials give your leadership team confidence in the data used for strategic decisions. When executives know their numbers are accurate and complete, they make better choices about resource allocation, expansion, and cost management.

The real value of a financial clarity audit emerges when you act on its findings. Your next step involves assessing your current financial systems and determining which recommendations address your biggest vulnerabilities.

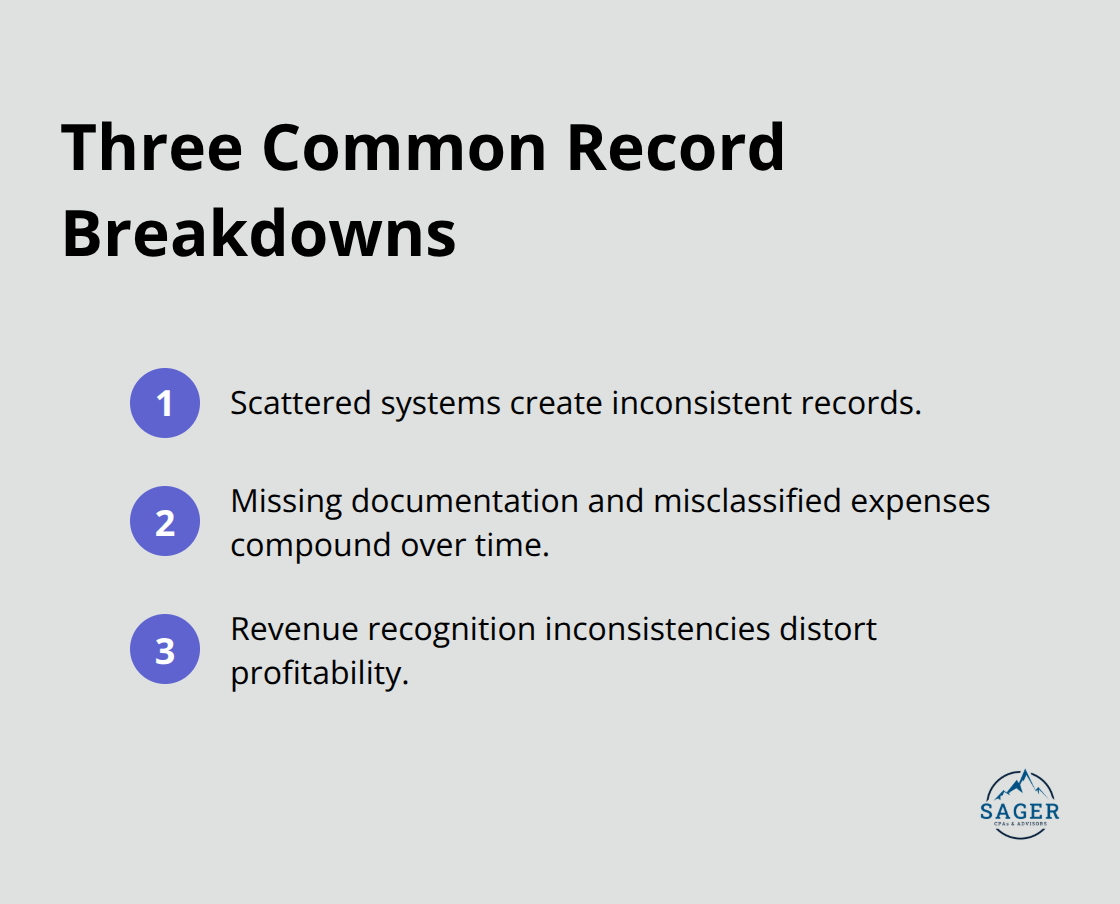

Most businesses operate with financial records scattered across multiple systems, email inboxes, and departmental spreadsheets. One department tracks expenses in QuickBooks, another uses spreadsheets, and a third relies on credit card statements that never get properly coded. This fragmentation creates the first major problem: inconsistent record-keeping that makes it impossible to get a complete financial picture.

When we examine a company’s books during a financial clarity audit, we frequently find that departments classify the same type of expense differently. One team codes software subscriptions as office expenses, while another puts them under technology costs. Revenue recognition varies too-some sales are recorded when invoiced, others when payment arrives, and some slip through the cracks entirely. These inconsistencies aren’t always intentional; they happen because no centralized system enforces consistent practices.

The result is financial statements that don’t accurately reflect what actually happened in the business. Decision-makers then rely on incomplete or misleading data when they allocate budgets or assess department performance.

The second breakdown involves expenses that are misclassified or undocumented. A business owner pays a contractor from a personal account and forgets to record it. A vendor invoice gets filed but never matched to the payment. Meals and entertainment expenses lack receipts or business purpose documentation. These gaps compound over time and create serious problems during tax season and audits.

Missing documentation for major transactions forces auditors to spend extra hours reconstructing what happened, which increases audit costs. More importantly, undocumented transactions create compliance risk-the IRS may disallow deductions or challenge the legitimacy of expenses. This forces a choice: either reconstruct the documentation retroactively (expensive and time-consuming) or accept that those expenses can’t be substantiated.

The expense misclassification problem extends to revenue recognition too. Some businesses record revenue when they invoice, others when they collect payment, and some when they deliver the service. Without consistent policies, your financial statements show inflated or deflated revenue depending on timing. This distorts your actual profitability and makes year-to-year comparisons meaningless.

A financial clarity audit identifies these exact problems and establishes the documentation standards and classification rules that prevent them from recurring. Once you understand where your records break down, the next step involves taking action to fix these gaps systematically.

Start a financial clarity audit by conducting an honest assessment of your current financial systems before you bring in external auditors. Pull together your chart of accounts, review how expenses are classified across departments, and identify which transactions lack proper documentation. This self-assessment takes a week or two but saves auditors significant time and reduces your overall audit costs.

Look specifically at your three highest expense categories and trace 10-15 transactions in each to spot classification patterns and documentation gaps. If you use accounting software like QuickBooks or Xero, export your last two quarters of transactions and review them for inconsistencies. This groundwork isn’t about fixing everything yourself; it’s about understanding the scope of problems so auditors can focus on the areas that matter most.

Once you have this baseline, you’re ready to engage external auditors who can provide the objectivity and expertise your internal team cannot. When selecting an auditor, ask specifically about their experience with businesses in your industry and their approach to identifying control weaknesses. The auditor should explain their testing methodology upfront and clarify what documentation you need to gather before they arrive.

Most audits for small to mid-sized businesses take four to six weeks from start to finish, with the bulk of fieldwork completed in two to three weeks. Plan for this timeline and designate someone internally to coordinate document retrieval and answer auditor questions. A CPA can benefit your small business by bringing specialized expertise to this process and helping you navigate findings effectively.

The real work begins after the audit report lands on your desk. You’ll receive findings organized by severity, and you need to prioritize them based on impact and feasibility. High-priority findings typically address control gaps that create fraud risk or compliance exposure-these demand immediate action. Medium-priority findings improve accuracy and efficiency but aren’t urgent.

Create a specific action plan with assigned owners, completion dates, and success metrics for each finding. For example, if the auditor identifies that vendor invoices aren’t matched to purchase orders before payment, your action plan should specify that the accounts payable manager will implement a three-way matching process by a specific date, and you’ll measure success by tracking the percentage of invoices matched before payment.

Some findings require software changes or new procedures that take two to three months to implement fully. Others need only training or process clarification and can be completed within weeks. Schedule a post-audit meeting with your leadership team and the auditors to discuss findings and ensure everyone understands the recommended improvements. This collaborative approach creates accountability and prevents audit recommendations from sitting on a shelf unimplemented.

A financial clarity audit transforms how your business operates and makes decisions. When you identify hidden discrepancies, strengthen your controls, and establish consistent reporting practices, your leadership team stops guessing and starts deciding based on verified data. Your lenders and investors see a business they can trust, and your team understands what good financial discipline looks like.

The businesses that benefit most from financial clarity audits act on the findings rather than letting reports sit unread. Within three to six months of implementing audit recommendations, most businesses report better visibility into their operations, fewer surprises during tax season, and more confidence in their financial statements. Clear reporting also changes resource allocation decisions-when you know your actual profitability by department or product line, you invest capital where it matters most.

The path forward starts with an honest assessment of where your records break down and continues through a thorough audit process. Sager CPA works with businesses to turn audit findings into lasting improvements in financial management and decision-making. Contact us to discuss your specific financial challenges and create a personalized strategy for achieving the clarity your business needs.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.