Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Freelancers face a unique tax situation that most W-2 employees never encounter. You’re responsible for paying both the employer and employee portions of self-employment tax, tracking your own deductions, and making quarterly estimated payments to the IRS.

At Sager CPA, we’ve helped hundreds of freelancers cut their tax bills significantly through smart tax planning. The difference between a disorganized approach and a strategic one can easily amount to thousands of dollars each year.

Self-employment tax hits harder than most freelancers expect. You pay 15.3% on your net earnings-12.4% for Social Security and 2.9% for Medicare. Here’s the critical part: only 92.35% of your net self-employment income faces this tax, not the full amount. A freelancer earning $50,000 in net profit doesn’t pay self-employment tax on the entire $50,000. You can deduct half of your self-employment tax as an adjustment to income on Form 1040, which provides some relief but doesn’t eliminate the burden. The IRS calculates this on Schedule SE, and most freelancers file this form without fully understanding how to lower the taxable amount. Your income reporting directly impacts this calculation, so accuracy matters tremendously.

Documentation becomes your defense against underpayment penalties. The Census Bureau found that self-employed individuals report 40% more wages and self-employment income in surveys than in actual tax records, which suggests many freelancers either overestimate their income or underestimate their deductions. This gap points to a fundamental problem: poor recordkeeping and incomplete deduction tracking.

Quarterly estimated tax payments force you to confront your income reality four times per year rather than once at tax time. Most freelancers underestimate these payments because they fail to account for deductible business expenses when calculating what they owe. You should base your quarterly payments on your actual net profit, not gross revenue. If you earned $10,000 in gross income but spent $3,000 on legitimate business expenses, your self-employment tax applies to $7,000, not $10,000.

Many freelancers pay quarterly taxes on gross income and then claim deductions at year-end, which results in overpayment or creates cash flow problems. Set up a simple system where you track income when received and expenses when paid, which aligns with the cash basis most freelancers use.

Digital accounting tools like Wave or similar platforms eliminate manual spreadsheet errors and generate the Schedule C figures you need for quarterly payments. These systems track your income and expenses automatically, reducing the time you spend on administrative work. You gain real-time visibility into your profit margins, which helps you make informed decisions about quarterly tax payments.

Documentation requirements are straightforward: keep receipts for every business expense, maintain records of all income sources, and log business mileage immediately after trips. The IRS doesn’t require fancy systems, but it does require proof. A missed receipt or vague expense description can disqualify an entire deduction during an audit.

Your quarterly payments should reflect your actual profit margin, not a percentage of gross income. This is why accurate expense tracking from month one prevents costly mistakes later. With your income and expenses properly documented, you’re ready to explore which deductions actually apply to your freelance work.

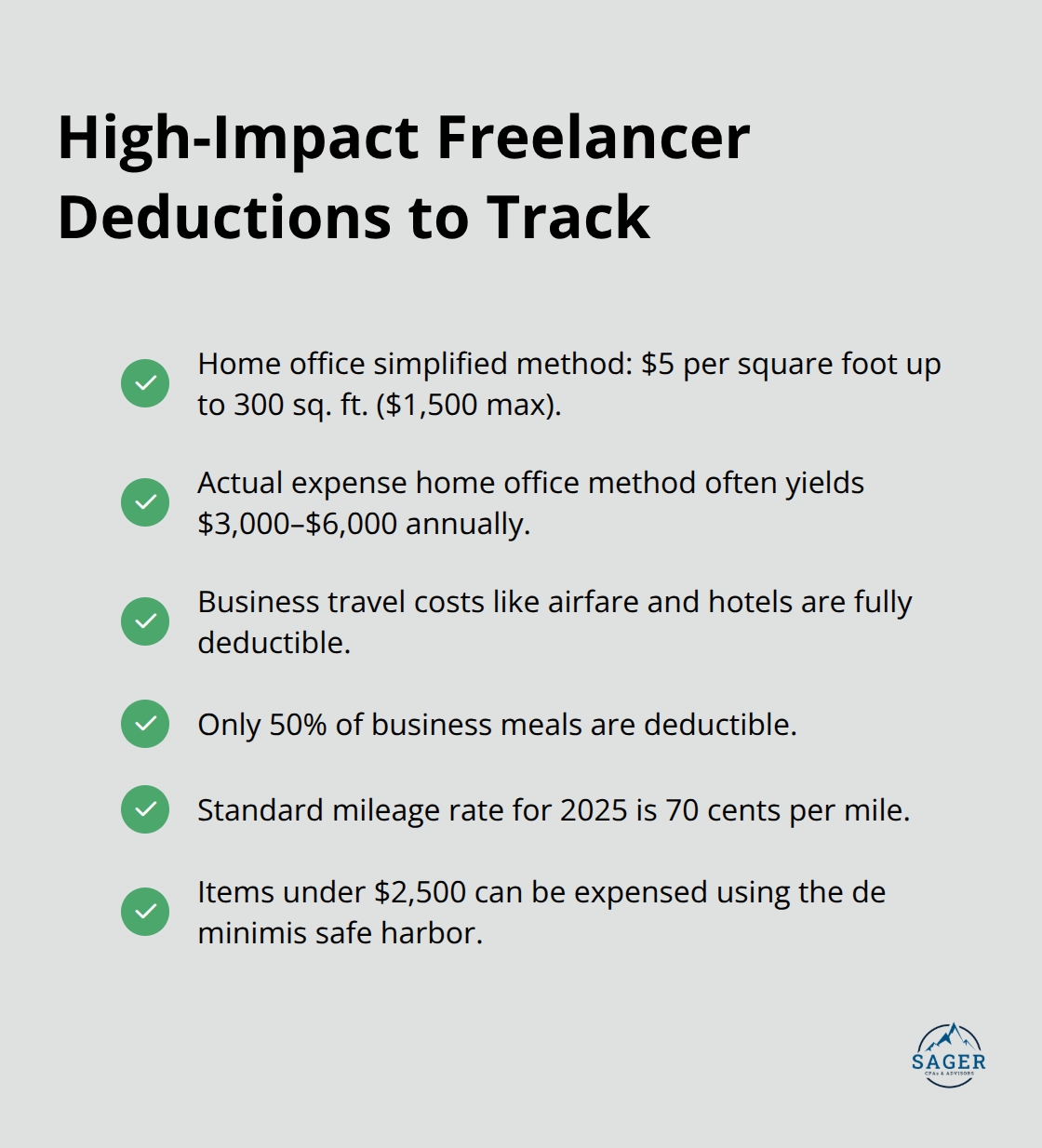

The home office deduction represents the largest missed opportunity for most freelancers. If you work regularly and exclusively from a dedicated space in your home, you qualify. The IRS offers two methods: the simplified approach at $5 per square foot up to 300 square feet (maximum $1,500 annually) or the actual expense method using Form 8829, which captures rent or mortgage interest, utilities, insurance, and repairs prorated to your workspace. The actual expense method almost always wins for freelancers. A freelancer renting a 1,200-square-foot apartment and using 200 square feet exclusively for work can deduct roughly one-sixth of rent, utilities, and internet costs-often $3,000 to $6,000 annually depending on location and local costs.

Document this with photos, floor plans, and measurements showing the exclusive business use. Many freelancers abandon this deduction because they fear it triggers audits, but the IRS expects home office deductions from self-employed workers. The real risk comes from claiming a home office when you don’t use it exclusively for business or when you can’t prove your measurements.

Business travel and meals generate substantial deductions if you track them correctly. Airfare, hotels, rental cars, and taxis are fully deductible when you travel for business purposes. Meals present a stricter rule: only 50% of meal costs are deductible, and the meal must be directly related to business or occur during a business trip. A freelancer attending a conference in Denver can deduct 50% of restaurant meals during that trip. The GSA publishes per diem rates by city, which simplifies calculations if you travel regularly.

Professional development expenses like courses, certifications, and training materials directly related to your freelance work are deductible on Schedule C. A web developer purchasing courses on advanced coding languages or a copywriter buying marketing certification programs can deduct these costs immediately. The key distinction: education that maintains or improves skills for your current work is deductible, but education that qualifies you for a new profession is not.

Vehicle expenses for business purposes deserve attention because the standard mileage rate for 2025 is 70 cents per mile. Track every business trip using apps like MileIQ or a simple spreadsheet, recording the date, destination, miles driven, and business purpose. A freelancer making client visits, attending networking events, or traveling to purchase supplies can accumulate 5,000 to 15,000 business miles annually. At 70 cents per mile, that translates to $3,500 to $10,500 in deductions. The alternative actual expense method works better only if your vehicle has high maintenance costs or you financed it recently, but most freelancers benefit more from the standard mileage rate because it requires less documentation.

Equipment purchases over a certain threshold require depreciation or Section 179 expensing rather than immediate write-offs, but items under $2,500 qualify for the de minimis safe harbor and can be deducted in the year purchased. A freelancer buying a monitor, keyboard, desk chair, or software license under $2,500 each deducts them immediately on Schedule C. These deductions form the foundation of your tax strategy, but they only work when you combine them with the right business structure and retirement planning decisions that further reduce your overall tax burden.

Timing decisions throughout your tax year create tangible savings that most freelancers ignore until December. The cash basis accounting system you use as a freelancer gives you real control: income counts when you receive it, and expenses count when you pay them. This means deferring client invoices into January reduces your current-year taxable income, while prepaying business expenses on a credit card in December lets you deduct the full amount even if you don’t pay the bill until the following year. A freelancer earning $80,000 could defer $10,000 in billings and prepay $5,000 in software subscriptions, office supplies, or professional services, lowering taxable income by $15,000. At a combined federal and self-employment tax rate of roughly 35%, that move saves approximately $5,250. The constraint here is genuine business logic: you cannot artificially manipulate cash flow in ways that damage client relationships or violate constructive receipt rules. Simply not cashing a check does not count as income deferral under IRS rules, but legitimately delaying when you send invoices absolutely does.

Your business structure choice determines whether you pay self-employment taxes on every dollar of profit or only on a reasonable salary. Most freelancers operate as sole proprietors, which means the full net profit from Schedule C faces the 15.3% self-employment tax. Converting to S corporation taxation through an LLC or corporation changes this dramatically. An S corp requires you to pay yourself a reasonable salary subject to payroll taxes, then take remaining profits as distributions that escape self-employment tax entirely. A freelancer with $100,000 in net profit might pay themselves a $60,000 salary and take $40,000 in distributions. The salary triggers payroll taxes of roughly $9,180, but the $40,000 distribution avoids the self-employment tax entirely, saving approximately $6,120 annually compared to sole proprietor status. The tradeoff involves filing Form 2553 with the IRS, handling quarterly payroll taxes, and maintaining corporate formalities, but the math favors this approach once your net profit consistently exceeds $60,000. Consult a tax professional to confirm salary reasonableness for your specific industry and situation, as the IRS scrutinizes S corp salaries that appear artificially low.

Retirement account choices directly reduce your taxable income while building wealth. A Solo 401(k) allows the highest contributions for most freelancers: you can defer up to $23,500 of your own compensation in 2025, then contribute an additional 25% of your net self-employment income as an employer contribution, with a total cap of $70,000 annually (or $77,500 if you’re age 50 or older). A freelancer earning $100,000 in net profit could contribute roughly $33,000 to a Solo 401(k), dropping taxable income to $67,000. A SEP IRA offers simpler administration with contributions up to 25% of net self-employment income, maxing at $70,000 in 2025, though it lacks the employee deferral component of a Solo 401(k). A Traditional IRA provides a lower ceiling at $7,000 annually but requires no self-employment income calculation. The timing matters: you must establish the account by December 31 to claim contributions for that tax year, though you can fund it until your tax filing deadline. Starting early compounds these advantages significantly. A 35-year-old freelancer funding a Solo 401(k) with $30,000 annually will accumulate roughly $1.8 million by age 65 assuming 7% annual growth, while someone starting at age 45 accumulates only $630,000 with the same contributions.

Tax planning for freelancers transforms from an annual burden into a strategic advantage when you act with intention. Most freelancers leave thousands of dollars on the table annually by treating taxes as an afterthought rather than a core business function. The combination of maximizing deductions, timing income and expenses strategically, choosing the right business structure, and funding retirement accounts creates a compounding effect that reshapes your bottom line.

Start with what you can implement immediately: document your home office, track mileage religiously, and establish a digital accounting system (these three actions alone typically save freelancers $2,000 to $5,000 annually). Next, evaluate whether converting to S corporation taxation makes sense for your income level and industry. Finally, commit to funding a retirement account before year-end, whether that’s a Solo 401(k), SEP IRA, or Traditional IRA.

The real advantage comes from working with a tax professional who understands freelance operations. At Sager CPA, we help freelancers implement customized tax strategies tailored to their specific situation. Schedule a consultation to review your current tax situation and identify which strategies apply to your freelance business.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.