Tax Planning Freelancers: Maximizing Deductions and Savings

Maximize deductions and cut taxes as a freelancer. Learn tax planning strategies that actually save money and reduce your filing burden.

Freelancers often leave thousands of dollars on the table each year by missing deductions and overlooking tax planning opportunities. The difference between a disorganized approach and a strategic one can mean thousands in savings.

At Sager CPA, we’ve helped countless self-employed professionals reclaim money they didn’t know they could deduct. This guide walks you through the deductions you’re likely missing, the tax strategies that actually work, and how to structure your business for maximum efficiency.

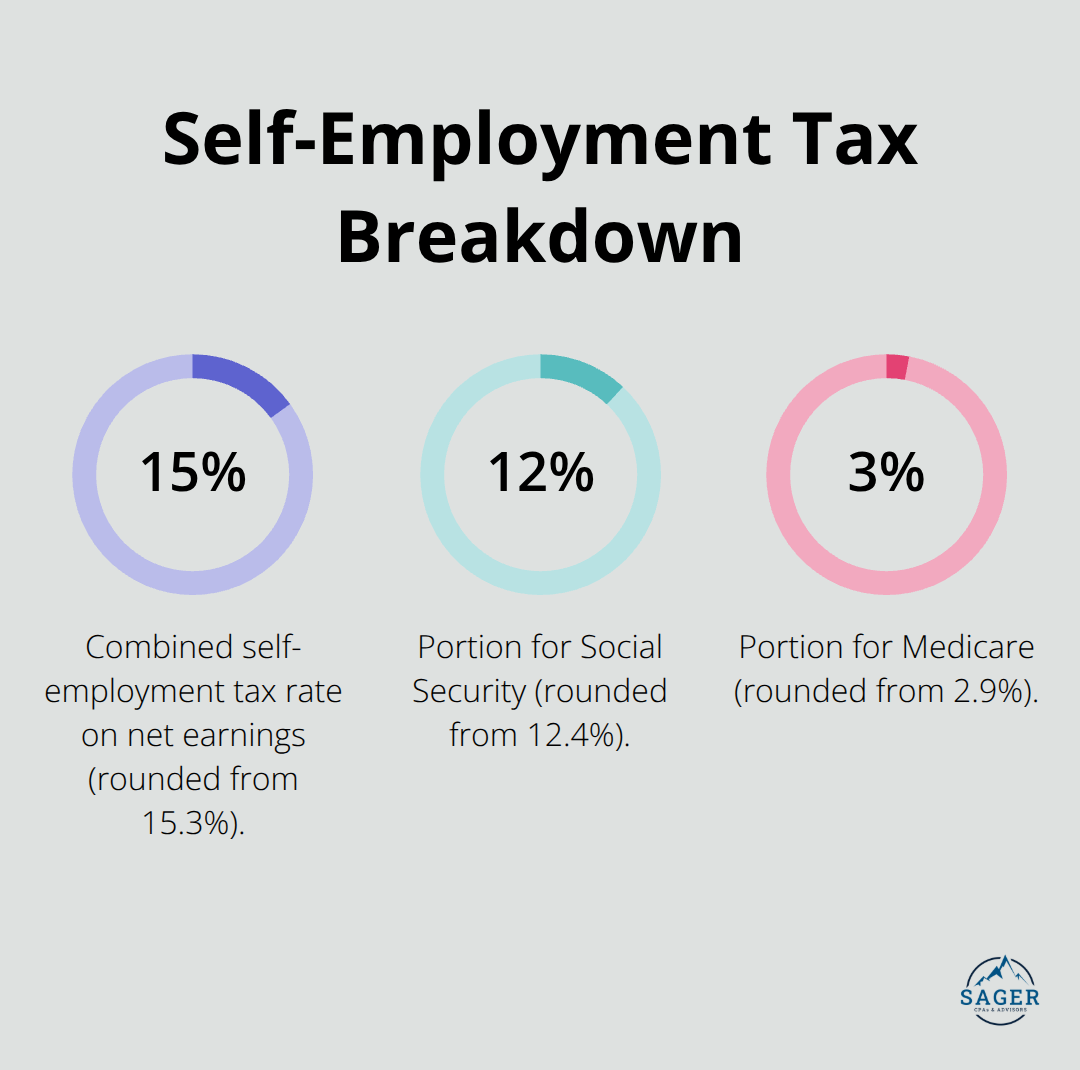

Self-employment tax hits differently than regular income tax, and most freelancers underestimate what they actually owe. The IRS requires you to pay self-employment tax of 15.3% in combined Social Security and Medicare taxes on your net earnings-12.4% for Social Security and 2.9% for Medicare. A freelancer earning $60,000 in net profit owes roughly $8,478 in self-employment tax alone, before calculating federal income tax. Most freelancers miss that you’re responsible for both the employer and employee portion, unlike W-2 employees who split this burden with their employer. You can deduct 50% of your self-employment tax on Schedule 1, which reduces your adjusted gross income, but the other half remains a direct tax obligation.

The IRS requires you to file a return if your net earnings from self-employment reach $400 or more, and you’ll report this on Schedule SE and Schedule C.

If you expect to owe more than $1,000 in taxes for the year, the IRS demands quarterly estimated tax payments using Form 1040-ES. The deadlines are April 15, June 17, September 16, and January 15 of the following year. Most freelancers miscalculate these payments-they overestimate income or fail to account for deductions they’ll claim at year-end, resulting in either overpayment or underpayment penalties. Calculate your estimated tax based on your actual net profit through the previous quarter, then adjust forward quarters accordingly. If your income varies significantly month-to-month, pay conservatively in early quarters and increase payments as your year-end profit becomes clearer. Underpayment penalties compound quickly, so setting aside 30% of each client payment into a dedicated tax account prevents the scramble come April. The Form 1040-ES worksheet walks you through the calculation, though many freelancers benefit from using tax software or consulting with a professional to get the math right the first time.

Your federal income tax bracket depends on your total taxable income after deductions, not just your freelance earnings. A freelancer in the 22% federal bracket paying 15.3% in self-employment tax faces a combined marginal rate of roughly 37.3%, making strategic deductions exponentially more valuable. High-income freelancers face the 3.8% net investment income tax on top of regular taxes if their modified adjusted gross income exceeds $200,000 as a single filer. This creates a powerful incentive to time deductions and income strategically. Maximizing retirement contributions like a SEP IRA contribution limits-which allows you to contribute up to 25% of your net self-employment income or $69,000 in 2024-directly reduces both your income tax and self-employment tax burden. Large equipment purchases or professional development investments made before year-end can drop you into a lower bracket. The alternative minimum tax, calculated on Form 6251, can also affect high-income freelancers, so understanding your specific tax situation beats generic planning advice.

The 37.3% combined rate means every dollar you deduct saves you roughly 37 cents in taxes. Home office expenses, vehicle mileage, professional development, and health insurance premiums all reduce your net profit before self-employment tax applies. This is where most freelancers leave money on the table-they claim obvious deductions but miss the smaller ones that add up throughout the year. Tracking business supplies, software subscriptions, and client entertainment expenses requires discipline, but the tax savings justify the effort. The next section covers the specific deductions you’re likely missing and how to calculate them properly.

Most freelancers claim the obvious deductions-maybe home office or mileage-then stop. The real money sits in the smaller, overlooked categories that compound throughout the year.

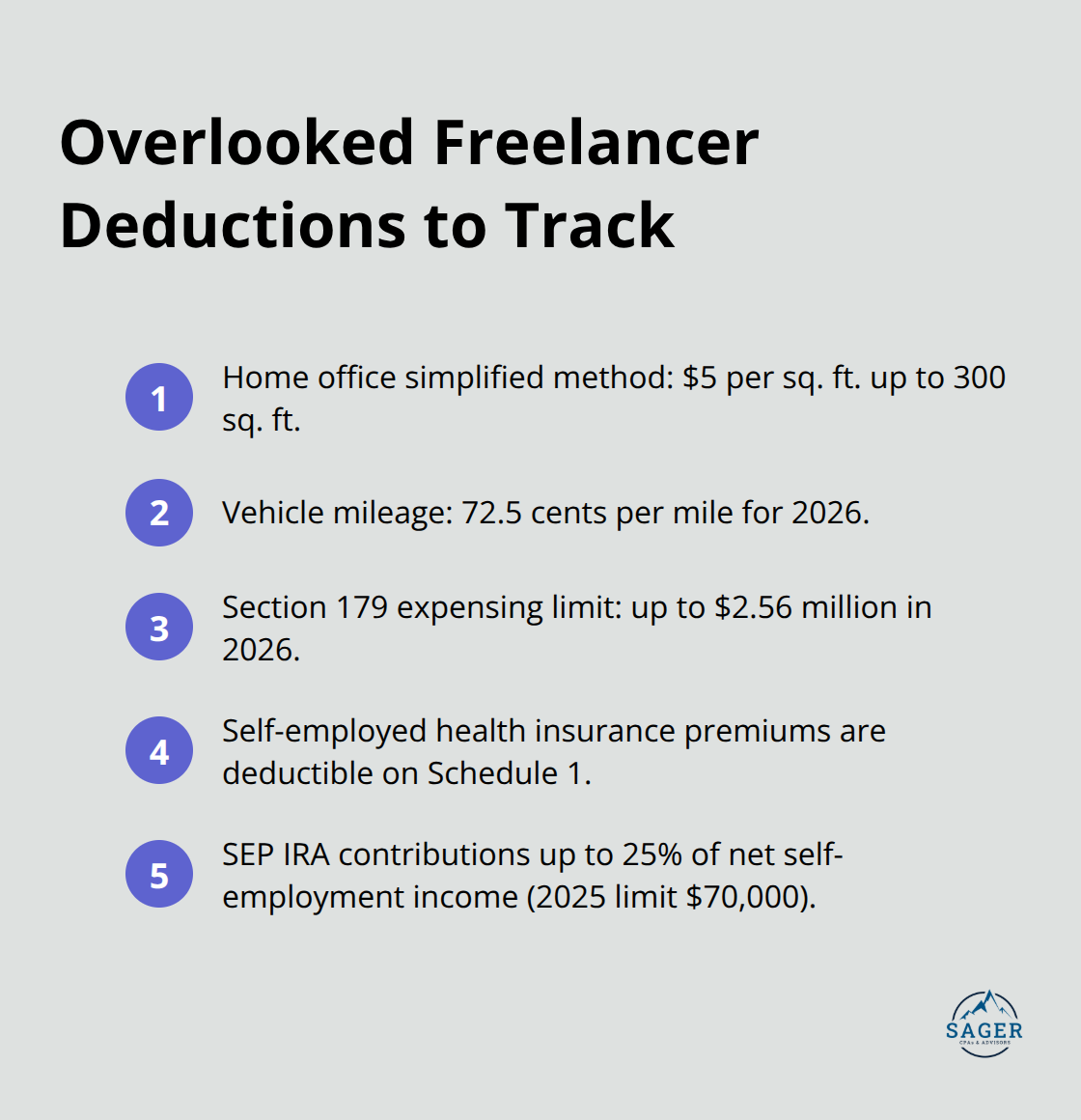

Your home office deduction alone can save you hundreds annually if you calculate it correctly. The IRS offers two methods: the simplified approach at $5 per square foot (up to 300 square feet maximum) or actual expenses using Form 8829.

The simplified method works well for freelancers with modest home offices. A 150-square-foot dedicated workspace costs $750 to deduct annually with zero paperwork beyond documenting your space. The actual expense method requires you to track utilities, internet, and insurance proportional to your office square footage, but it yields larger deductions if you have a substantial dedicated space.

Most freelancers underestimate their vehicle expenses because they only count gas. The IRS standard mileage rate for 2026 is 72.5 cents per mile for business use. A freelancer driving 15,000 business miles annually saves roughly $10,875 in deductions using the standard rate.

Track every business trip meticulously-client meetings, supply runs, travel to coworking spaces, even driving to the bank to deposit checks. Apps like MileIQ automate this tracking and sync with your tax software, eliminating the guesswork. The actual expense method (fuel, maintenance, insurance, depreciation) works better only if your vehicle expenses genuinely exceed the standard rate, which rarely happens for typical freelancers.

Professional development costs and equipment purchases represent another major blind spot. Tuition for courses, certification programs, software subscriptions, and industry conferences are fully deductible on Schedule C if they maintain or improve your job skills. A freelancer taking a $2,000 course to sharpen their craft saves roughly $740 in taxes at a 37% combined rate.

Equipment like computers, monitors, and furniture can be expensed immediately under Section 179 (up to $2.56 million in 2026) or depreciated over several years. Choosing Section 179 accelerates your deductions and maximizes year-end tax planning.

Health insurance premiums for self-employed individuals deserve special attention because they reduce both income tax and self-employment tax. Self-employed health insurance deductions (including long-term care and Medicare premiums) go on Schedule 1 and cover you, your spouse, and dependents. A freelancer paying $8,000 annually in health insurance saves roughly $2,960 in combined taxes.

Retirement contributions offer even larger deductions. A SEP IRA allows SEP IRA contribution limits up to 25% of your net self-employment income, with a 2025 limit of $70,000. A freelancer earning $100,000 in net profit can contribute $25,000 to a SEP IRA, eliminating $25,000 from taxable income and saving approximately $9,250 in taxes. Solo 401(k)s provide similar benefits with flexibility to contribute as both employee and employer.

Tracking these deductions requires organized records-receipts, invoices, mileage logs, and documentation of business purpose. The tax savings justify the discipline. Your record-keeping system directly determines whether the IRS accepts your deductions during an audit. With these deductions identified and tracked, the next step involves structuring your business entity and timing your income strategically to amplify these savings even further.

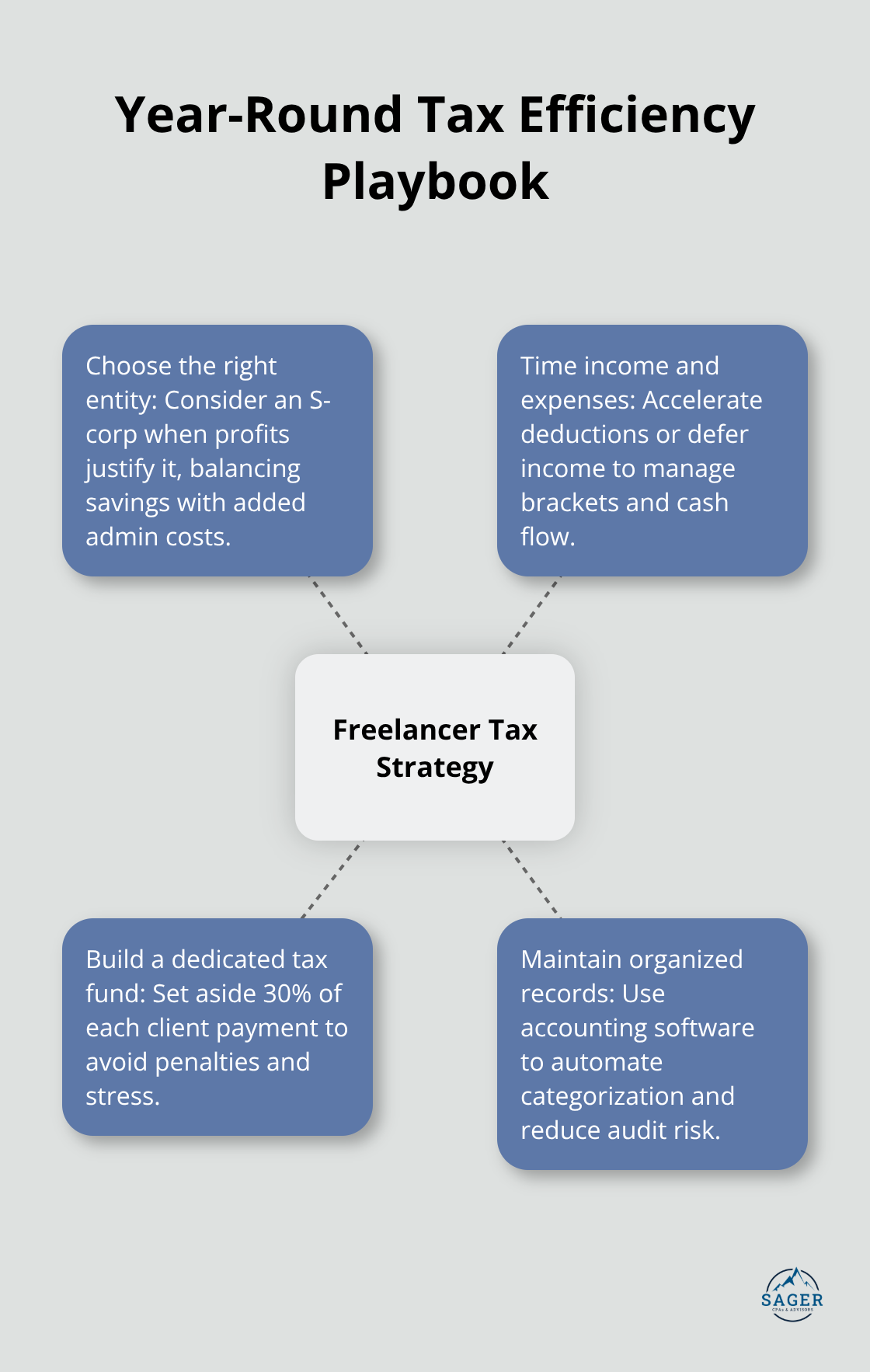

Most freelancers operate as sole proprietors without questioning whether that structure makes sense for their income level and tax situation. A sole proprietorship works fine initially, but once you hit $60,000 to $80,000 in net profit annually, an S-corporation election can reduce your self-employment tax burden significantly. With an S-corp, you split income between W-2 wages (subject to self-employment tax at 15.3%) and distributions (not subject to self-employment tax). A freelancer earning $100,000 in net profit who takes a $50,000 W-2 salary and $50,000 in distributions saves roughly $4,590 in self-employment taxes compared to a sole proprietorship. The tradeoff involves additional accounting costs and payroll processing, typically $2,000 to $3,000 annually, but the math favors an S-corp election when your profit exceeds $80,000. Form 2553 elects S-corp status with the IRS, though you must file it within specific timeframes to be effective for the current year. If you’re married and both work in the business, a qualified joint venture election allows you to file separately as sole proprietors rather than as a partnership, simplifying your tax filing while maintaining liability protections if you’ve formed an LLC.

Timing your income and expenses throughout the year matters far more than most freelancers realize. If you anticipate finishing the year in the 24% federal tax bracket, accelerate deductions into December by purchasing equipment, paying professional development costs, or making retirement contributions before year-end. This strategy drops your taxable income and potentially moves you into the 22% bracket, saving thousands. Conversely, if you’re on track for a strong year, defer invoicing until January to shift income into the next tax year, spreading your tax burden across two years rather than concentrating it into one.

Strategic timing of income and expenses requires coordination, but the tax savings justify the effort.

A dedicated tax fund separate from your operating account prevents the scramble when estimated payments or annual taxes come due. Set aside 30% of every client payment into this account automatically, then adjust downward if your year-end accounting reveals you’ve overcontributed. This discipline eliminates the stress of liquidating business assets or taking on debt to cover tax liability.

Strong record-keeping systems powered by accounting software (such as QuickBooks or FreshBooks) sync your bank transactions automatically, categorizing expenses and tracking mileage without manual data entry. The software generates your Schedule C data directly, reducing errors and audit risk while cutting your tax preparation time in half. Maintaining organized records year-round means your tax professional spends less time hunting for receipts and more time optimizing your deductions.

The gap between what freelancers actually owe and what they pay comes down to execution. You now understand self-employment tax mechanics, identified deductions you’ve been missing, and learned how business structure and timing amplify your savings. A freelancer earning $80,000 who implements these tax planning strategies saves between $8,000 and $12,000 annually compared to one who doesn’t.

Tax planning for freelancers isn’t complicated, but it does require discipline. Tracking mileage, organizing receipts, timing equipment purchases, and maintaining a dedicated tax fund separate from operating accounts transforms your tax situation from reactive scrambling to proactive optimization. Working with a tax professional changes the equation entirely by helping you identify blind spots in your deduction strategy, structure your business entity for maximum efficiency, and build tax planning systems that work year-round rather than just at filing time.

We at Sager CPA help freelancers capture deductions as they happen instead of discovering missed opportunities after the year ends. Schedule a consultation with Sager CPA to review your current tax situation and identify where you’re leaving money on the table. The investment in professional guidance pays for itself many times over through deductions and strategies you wouldn’t find on your own.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.