Financial clarity for individuals: A Personal Finance Roadmap

Achieve financial clarity for individuals with our personal finance roadmap. Master budgeting, savings, and debt management strategies.

Most people know they should have a handle on their finances, but few actually do. Without financial clarity for individuals, money decisions become stressful and reactive instead of intentional.

At Sager CPA, we’ve seen how a simple roadmap transforms the way people relate to their money. This guide walks you through the exact steps to build one.

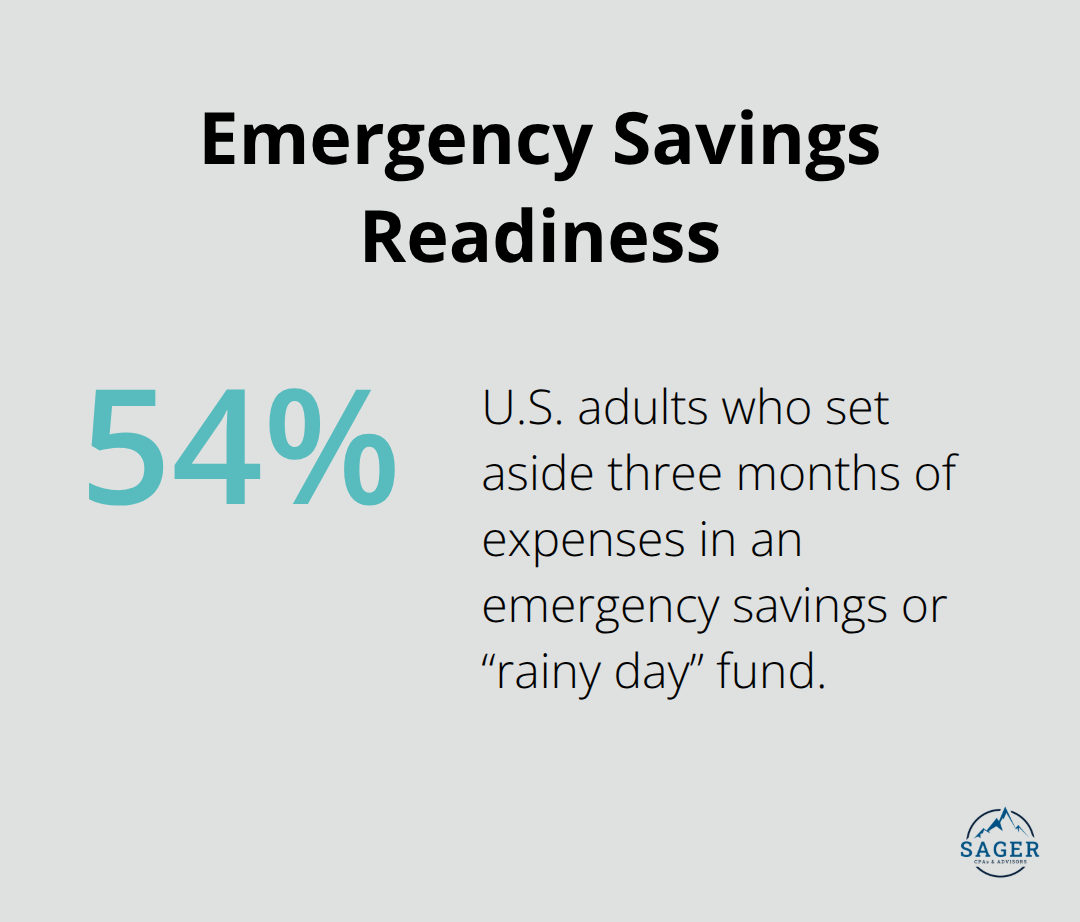

Most people operate without a clear picture of where their money actually goes. The Federal Reserve’s 2023 report on household finances found that 54 percent of adults had set aside money for three months of expenses in an emergency savings or “rainy day” fund. This isn’t because they lack income-it’s because they lack visibility.

Without tracking income and expenses separately, you can’t see the gap between what you earn and what you spend.

A spreadsheet or budgeting app takes 30 minutes to set up but reveals patterns you’ve likely ignored for years. You’ll find that subscriptions drain $200 monthly, dining out costs $450, and transportation eats another $300. These aren’t catastrophic numbers individually, but together they represent $950 per month or $11,400 per year that could fund an emergency fund, retirement savings, or debt payoff. The problem isn’t that you’re bad with money-it’s that you’ve never actually looked at the numbers.

Goals without numbers are wishes, not plans. When you say you want to save more or get ahead financially, you have no way to measure progress or know when you’ve succeeded. A realistic goal states exactly how much you need, by when, and for what purpose. Instead of vague aspirations, you need targets like saving $15,000 for an emergency fund within 18 months or paying off an $8,000 credit card balance in two years.

Without these specifics, your budget has no direction and your spending decisions lack a framework. You spend money on convenience purchases because nothing pulls against that impulse. Your daily choices disconnect from your bigger life plans, and months pass without meaningful progress toward what actually matters to you.

Quarterly reviews catch drift before it becomes a crisis. Without this discipline, inflation quietly erodes your purchasing power, interest on debt compounds against you, and retirement contributions lag behind what you need.

This is where many people find themselves stuck: they have income, they have expenses, but they lack the structure that connects the two to their actual goals. The next section shows you exactly how to build that structure.

Open a spreadsheet or use a free budgeting tool like YNAB or EveryDollar and spend one hour documenting your actual take-home income and all expenses from the past month. Pull bank statements, credit card bills, and subscription receipts instead of estimating. Categorize everything into housing, food, transportation, insurance, subscriptions, dining out, and miscellaneous. This single step reveals the truth that most people avoid: you’ll see exactly where your money flows and how much is discretionary versus fixed.

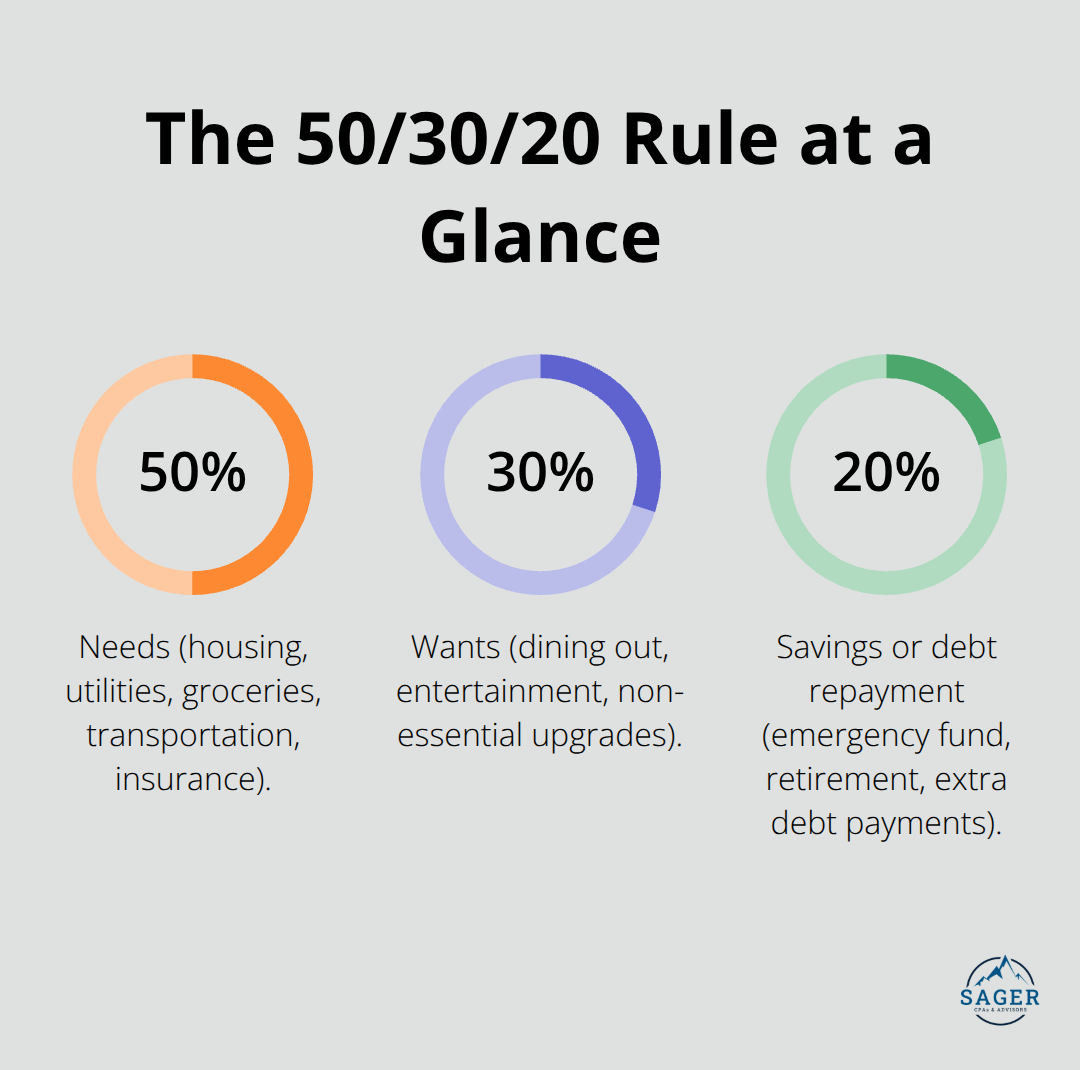

Once you have this baseline, you stop guessing about your finances. The 50/30/20 rule suggests allocating 50% of income to needs, 30% to wants, and 20% to savings or debt repayment, but your actual numbers might look different-and that’s fine. What matters is that you know them.

Spend the next week reviewing this data weekly rather than monthly; weekly reviews catch mistakes and make patterns obvious faster. Then set three specific financial goals with exact dollar amounts and target dates. Don’t say you want an emergency fund-say you want to build an emergency fund within two years. Don’t say you want to pay off debt-say you want to eliminate a $9,500 credit card balance in 24 months.

These concrete targets let you calculate how much you need to save monthly: divide your goal amount by the number of months available. Now your budget has purpose and direction.

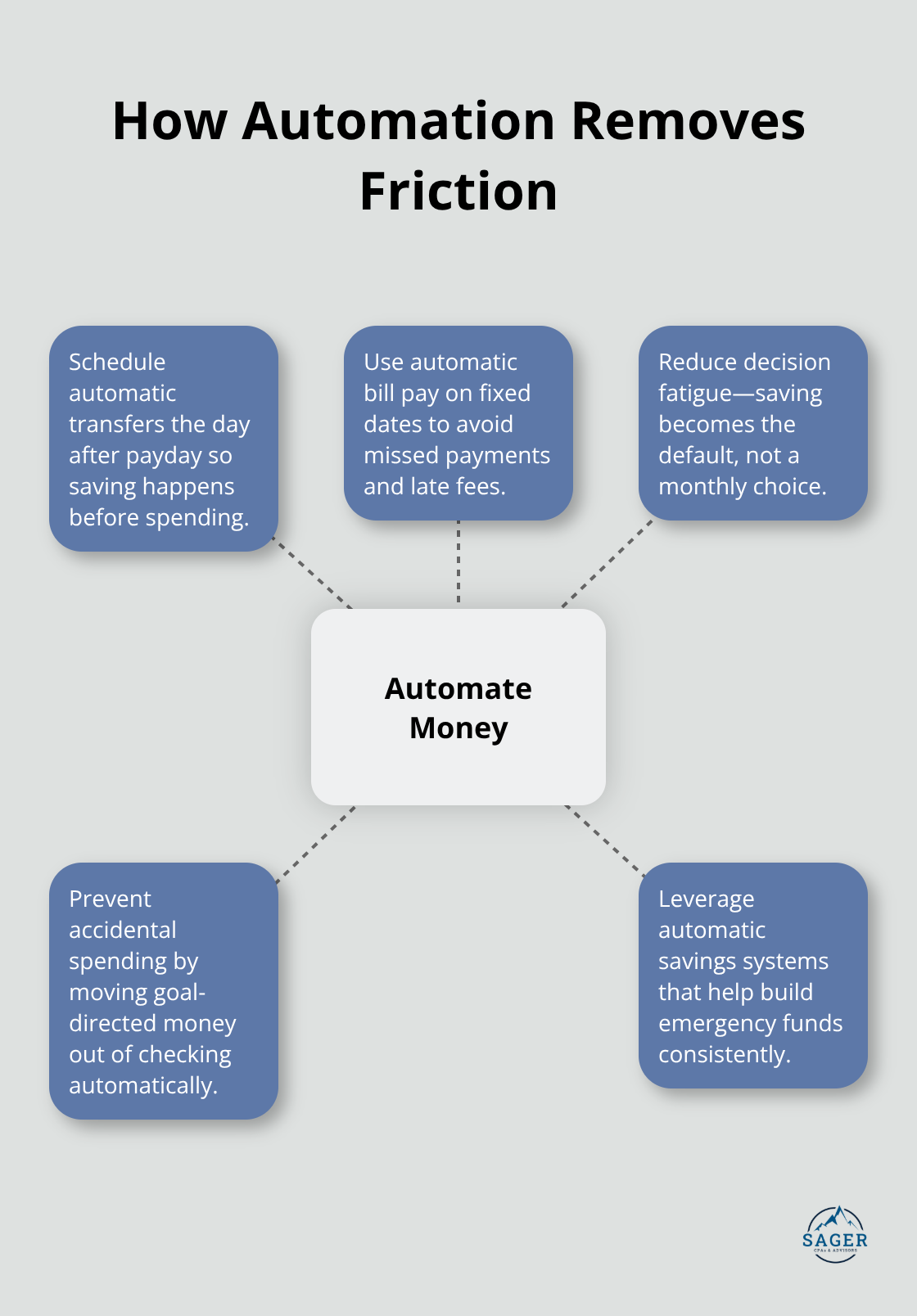

Set up automatic transfers from your checking account the day after you’re paid-before you spend the money. Automation removes willpower from the equation and prevents you from accidentally spending money earmarked for goals. This approach works because the money leaves your account before temptation strikes.

Conduct a quarterly review in January, April, July, and October. Spend 45 minutes comparing your actual spending against your budget categories, checking progress toward your three goals, and adjusting for life changes like a salary increase or unexpected expense. If you spent $600 on dining out when you budgeted $400, that’s data worth examining. Did your social life shift, or did you lose discipline?

If a car repair derailed your emergency fund contributions, adjust your timeline rather than abandoning the goal. This rhythm keeps your roadmap aligned with reality instead of letting it gather dust. As your financial picture becomes clearer, you’ll face decisions about where to direct your savings-and that’s where the next section helps you prioritize what comes first.

Your roadmap only matters if you actually follow it, and that means removing friction from the process. Set up automatic transfers from your checking account to a dedicated savings account on the day after you’re paid, before you touch the money for anything else. Do the same with bill payments-schedule them to come out automatically on fixed dates so you never miss a deadline and never have to think about whether you paid the electric bill. This approach works because it eliminates decision fatigue. You don’t choose to save each month; saving happens by default. Automatic savings systems help build emergency funds by automating the savings process. Automation also prevents the common mistake of spending money you intended to save.

If the money sits in your checking account waiting for you to transfer it, something will come up and derail your plan. When it leaves automatically, that temptation never materializes.

Review your spending categories from the previous month and identify where you spent more than you budgeted. If dining out exceeded your target, that’s the category to address first because it’s usually the easiest to control. Cut subscriptions you don’t use-most people have streaming services, apps, or memberships they forgot about. These often represent $100 to $300 monthly that vanishes without providing value. After you handle the obvious waste, look at your fixed costs like housing, insurance, and transportation. These are harder to cut but often worth the effort. Refinancing a car loan or shopping for cheaper insurance can save $50 to $150 monthly without changing your lifestyle.

The standard recommendation is 3 to 6 months of expenses, but if your income fluctuates or you’re self-employed, try 9 to 12 months instead. Keep this money in a high-yield savings account earning up to 4.15% APY, not in stocks or investments. An emergency fund’s job is stability, not growth. Once you have $1,000 set aside for genuine emergencies, you can pause contributions temporarily to attack high-interest debt like credit cards charging 18 to 25 percent annually.

After your emergency fund reaches your target and debt is under control, your roadmap becomes clearer. At that point, working with a financial professional makes sense. A consultation can clarify whether you’re on track for retirement, identify tax opportunities you’re missing, and build a plan tailored to your actual situation rather than generic advice. Sager CPA and Advisors offers expert financial management and tax planning services designed to reduce liabilities and create informed decision-making through regular communication and supportive partnerships. Schedule a consultation to create a personalized financial strategy that goes beyond budgeting to include tax planning, investment alignment, and long-term wealth building.

Financial clarity for individuals transforms how you make decisions about money. When you know exactly where your income goes and what your goals are, spending becomes intentional rather than reactive. You stop wondering if you can afford something and start knowing whether it aligns with your priorities.

Your roadmap adapts as life changes. Income increases, expenses shift, and priorities evolve-quarterly reviews catch these shifts and keep your plan relevant. If you receive a raise, you decide whether to increase savings, reduce debt faster, or adjust your lifestyle. If an unexpected expense hits, you adjust timelines instead of abandoning goals.

As your financial clarity grows and your situation becomes more complex-retirement planning, tax optimization, investment alignment-working with a professional makes sense. Sager CPA and Advisors offers expert financial management and tax planning services designed to reduce liabilities and create informed decision-making through regular communication and supportive partnerships. A consultation can clarify whether you’re on track, identify opportunities you’re missing, and build a strategy tailored to your actual situation.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.