Custom Tax Planning: Tailored Solutions for Your Unique Situation

Discover tailored tax planning strategies designed for your unique financial situation. Learn how custom solutions can help you save more on taxes.

Most people leave thousands of dollars on the table every year simply because they don’t have a tax strategy tailored to their specific situation. Generic tax advice doesn’t work when your financial life is unique.

At Sager CPA, we’ve seen firsthand how custom tax planning transforms what clients actually owe. This guide walks you through how to build a strategy that fits your circumstances, avoid costly mistakes, and take advantage of opportunities most people miss.

Custom tax planning starts with understanding exactly what you earn, what you can deduct, and where tax law creates opportunities for your specific situation. We at Sager CPA map your complete financial picture during every engagement-income from all sources, existing deductions you’re using, deductions you’re missing, and major financial events on the horizon. This assessment reveals the gap between what you currently pay and what you should actually owe. Most clients discover they’ve overlooked deductions worth thousands annually.

Self-employed individuals frequently miss home office deductions, vehicle expenses, or professional development costs. Business owners often fail to structure S-corp elections that could lower their current tax burden significantly. High-income earners typically don’t optimize charitable giving vehicles like donor-advised funds, which provide an immediate deduction while allowing you to distribute funds to charities over time. The assessment phase also identifies which income streams trigger additional tax obligations. Capital gains, rental income, and business profits each have distinct planning levers that generic tax filing completely ignores.

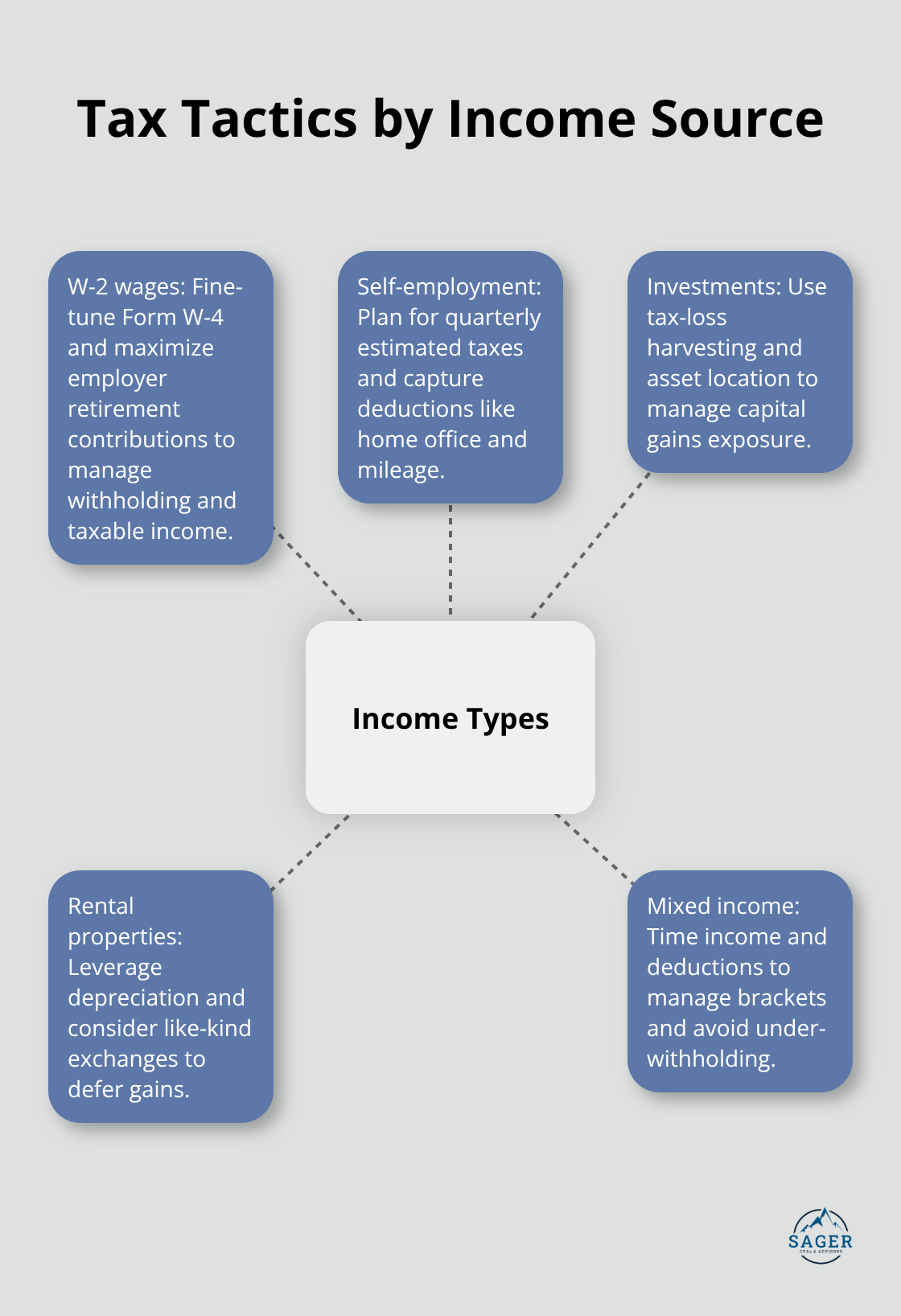

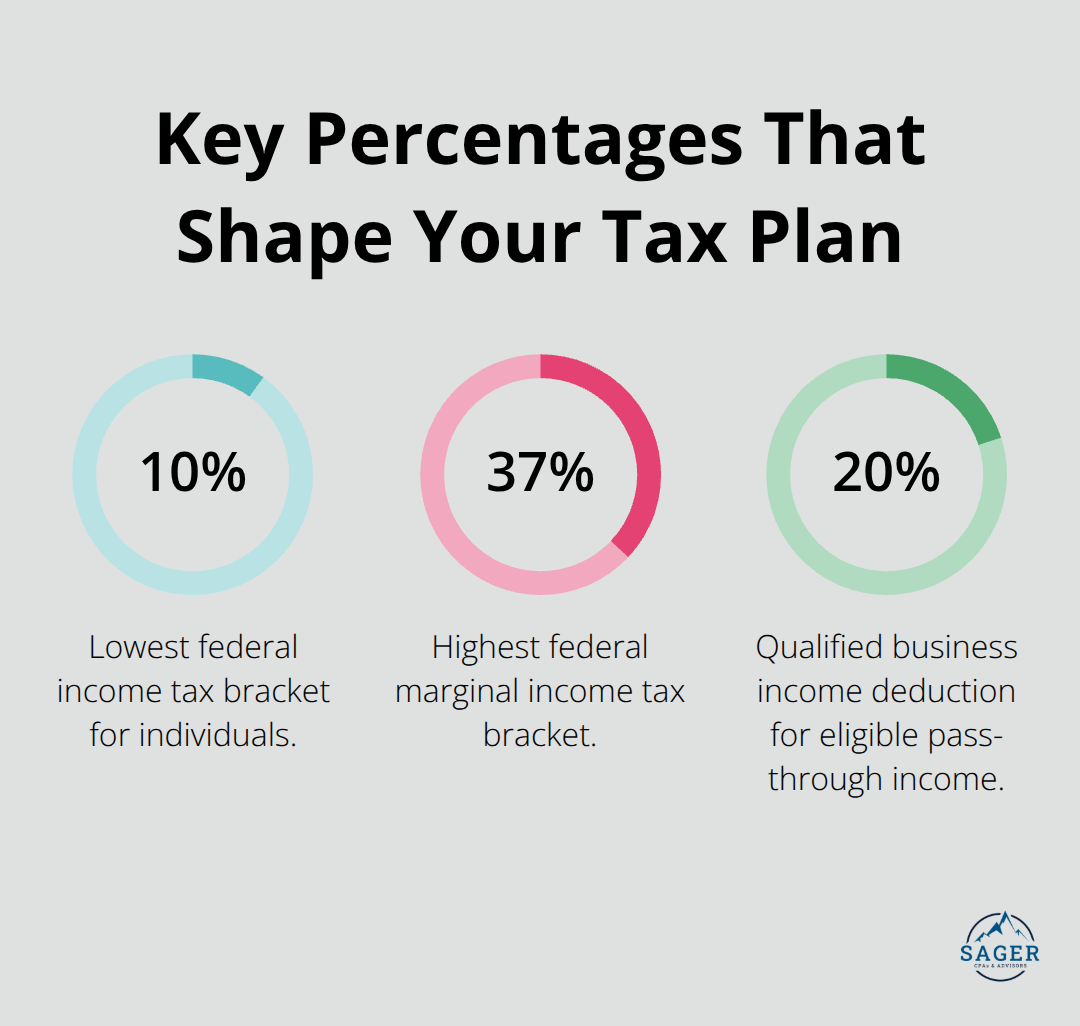

W-2 wages, self-employment income, investment returns, and rental properties don’t all respond to the same tax planning approach. Someone earning $150,000 in W-2 income faces entirely different opportunities than someone with the same income split between business profit and investment gains. The U.S. tax system uses seven federal income tax brackets ranging from 10% to 37%, and higher income pushes you into a higher marginal rate, making bracket management essential for your strategy.

If you’re self-employed or earn substantial non-wage income, you may need to make estimated tax payments throughout the year rather than waiting until April. We analyze whether your current withholding matches your actual tax liability or whether adjustments to your Form W-4 would prevent overpaying or underpaying. Real estate investors benefit from depreciation strategies and 1031 exchanges that reduce taxable income from rental operations. Business owners need to evaluate entity structure-whether an S-corp election makes financial sense given your profit levels and payroll expenses.

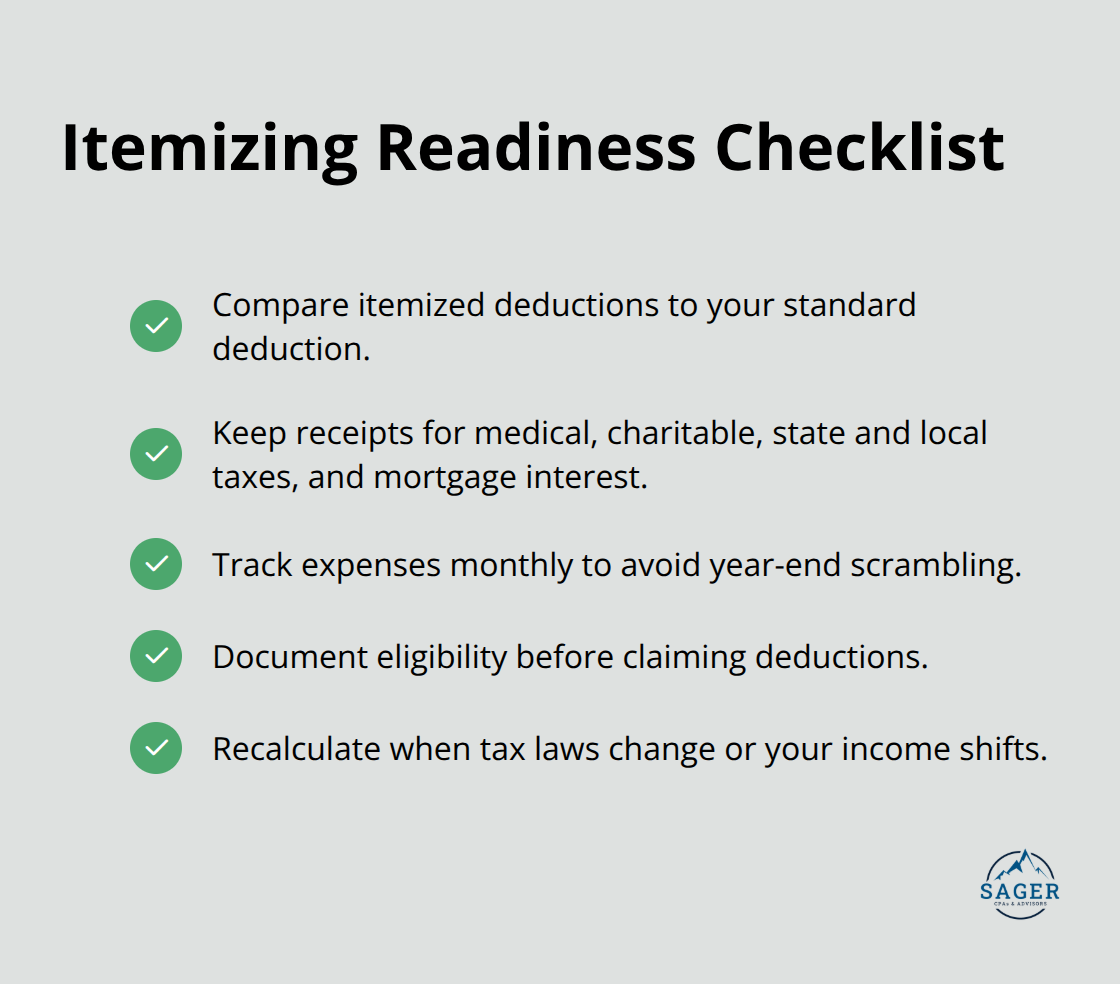

Your deduction analysis goes far beyond the standard deduction. Itemizing makes sense only when eligible deductions exceed the standard deduction for your filing status, but many people skip this calculation entirely and leave deductions unused.

Once we’ve assessed your situation thoroughly, we develop a written strategy that outlines specific actions and their expected impact on your tax liability. This isn’t theoretical-it’s actionable. The strategy might include adjusting your withholding, timing income recognition, accelerating or deferring deductions, restructuring business operations, or repositioning investments. We establish benchmarks so you can measure whether the plan delivers results.

Implementation happens throughout the year, not during tax season. Proactive planning embeds tax savings into your cash flow by anticipating liabilities before they arrive, which means you’re not scrambling to find money in April. We monitor changes in tax law that affect your situation and adjust your strategy accordingly, capturing new credits or deductions as they become available. This year-round approach prevents the common mistake of failing to plan throughout the year, which costs most people more than any single overlooked deduction.

The real power of custom tax planning emerges when you move from strategy to execution-and that’s where understanding the specific mistakes that derail most taxpayers becomes your competitive advantage.

Most taxpayers make the same critical error: they treat tax planning as something that happens in March or April when they gather receipts and file returns. This reactive approach leaves money on the table every single year. The IRS withholding estimator shows that consistently large refunds signal over-withholding throughout the year, meaning you’ve given the government an interest-free loan instead of keeping that cash in your business or investments. Waiting until tax season also means you miss timing opportunities that require action before December 31st.

If you’re self-employed or earn substantial non-wage income like dividends or rental income, estimated tax payments are due on specific quarterly deadlines, and missing even one creates penalties and underpayment interest. The cost of reactive filing versus proactive planning isn’t marginal-it’s often the difference between paying thousands more in taxes than necessary and optimizing your liability throughout the year. Year-round tax monitoring catches income spikes, major purchases, or business changes that affect your strategy while you still have time to adjust withholding, defer income, or accelerate deductions.

The second mistake happens because most people don’t systematically track what they’re actually eligible to claim. Self-employed individuals commonly miss home office deductions worth hundreds annually because they assume the standard deduction covers everything. Real estate investors overlook depreciation strategies that reduce taxable rental income substantially. High-income earners skip the calculation comparing itemized deductions against the standard deduction and miss thousands in tax savings when itemizing makes sense.

Medical expenses above 7.5% of your adjusted gross income, charitable donations, state and local taxes, and mortgage interest all create deduction opportunities that vanish if you don’t document them. These opportunities disappear even faster when tax laws shift and you fail to update your strategy accordingly.

The Tax Cuts and Jobs Act changed depreciation rules, expanded certain credits, and modified how business income flows through to individual returns-yet many people still use outdated strategies from years past. Taxpayers who haven’t adjusted their filing approach in five years miss credits introduced in 2022 or 2023 entirely. Staying informed about changes requires either subscribing to IRS updates yourself or working with a tax professional who monitors regulatory changes and alerts you when new opportunities apply to your situation.

The margin between what you actually owe and what you pay often comes down to whether someone actively tracks changes in tax law and adjusts your plan accordingly. This ongoing attention to regulatory shifts separates those who optimize their tax position from those who simply file and hope they haven’t missed anything. The mistakes outlined here-waiting to plan, failing to track deductions, and ignoring tax law changes-compound over time, which makes understanding how different life situations demand different tax strategies your next critical step.

Business owners face a fundamentally different tax challenge than W-2 employees because business income flows through at ordinary rates unless you structure it strategically. S-corp elections for business income splitting makes financial sense when your net business profit exceeds roughly $60,000 to $80,000 annually, because you can split income between W-2 wages and distributions, reducing self-employment tax on the distribution portion. The math is straightforward: self-employment tax runs 15.3% on net earnings, so reducing taxable self-employment income by $50,000 saves you approximately $7,650 in taxes annually. However, S-corp elections create additional compliance requirements and payroll processing costs, typically $1,500 to $3,000 yearly, which means the election only makes sense above those income thresholds.

Real estate investors operating rental properties should evaluate cost segregation studies for real estate depreciation, which accelerate depreciation deductions in early years of property ownership. A cost segregation study might identify additional depreciation deductions on a property purchase, deferring taxes substantially while you retain cash flow. Business owners also need to assess whether the qualified business income deduction under current tax law applies to your situation, as this 20% deduction on pass-through business income can reduce your effective tax rate significantly if your total taxable income falls within eligible ranges.

High-income earners operate in a different tax landscape because marginal rates climb to 37% at the federal level, and many states layer additional income taxes on top. For this group, the focus shifts from basic deductions to strategic income timing and advanced vehicles like donor-advised funds, which provide immediate tax deductions while allowing you to distribute funds to charities over time. High-income earners also benefit from tax-loss harvesting strategies that offset capital gains throughout the year rather than waiting until December, capturing losses when market downturns occur.

If you anticipate a major life transition like selling a business, receiving a large inheritance, or experiencing significant income fluctuation, the year before the event becomes critical for tax planning. Someone selling a business in 2027 should start planning in 2026 to evaluate whether spreading the sale proceeds across multiple years reduces your tax bracket exposure, or whether structuring the sale to qualify for installment treatment improves your after-tax outcome.

Major life events including marriage, divorce, retirement, or significant property purchases each trigger distinct tax opportunities and obligations. Married couples filing jointly access lower tax brackets than single filers on identical income, but divorce changes your filing status and potentially eliminates certain deductions you previously claimed. Someone retiring before age 59½ needs to plan for early withdrawal penalties on retirement accounts unless they structure withdrawals through rule 72(t) distributions, which allow penalty-free access if the withdrawals follow IRS-specified calculations. These situations demand proactive planning months in advance, not reactive filing after the event occurs.

Custom tax planning transforms what you actually owe by adapting as your income, business structure, and life circumstances shift throughout the year. The gap between what most people pay and what they should owe comes down to whether you act proactively or wait until April to react. Business owners who implement S-corp elections save thousands annually, real estate investors who use depreciation strategies keep more rental income, and high-income earners who optimize charitable giving reduce their effective tax rate substantially-these are concrete reductions in what you owe because your strategy matches your actual situation.

A tax professional who understands your complete financial picture monitors tax law changes throughout the year, catches income spikes or major purchases that affect your strategy, and adjusts your plan before December 31st when you still have time to act. This ongoing attention prevents the costly mistakes that derail most taxpayers: waiting to plan, overlooking deductions, and ignoring regulatory shifts. We at Sager CPA build personalized financial strategies that reduce your tax liability while supporting your long-term growth through precise accounting combined with strategic planning tailored to your unique circumstances.

Schedule a consultation with Sager CPA to map your financial situation against real tax-saving opportunities. The conversation typically reveals deductions you’ve missed and strategies that fit your goals. Your custom tax plan starts with understanding exactly where you stand and where you want to go.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.