Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Tax laws are shifting in 2025, and waiting until April won’t cut it. The sooner you understand what’s changing, the better you can position yourself financially.

At Sager CPA, we’ve seen firsthand how personalized tax solutions make the difference between a reactive scramble and a strategic advantage. This guide walks you through the changes ahead and the moves you can make right now.

The One Big Beautiful Bill, signed into law on July 4, 2025, restructures how federal taxes work across nearly every category. This isn’t a minor tweak-it’s a fundamental shift that affects your filing status, what you can deduct, and how much you owe. The SALT deduction cap increases to $40,000 through 2029, after which point it reverts to $10,000, which means millions of taxpayers in high-tax states now benefit from itemizing instead of taking the standard deduction. For 2025, the standard deduction sits at $31,500 for married filing jointly and $15,750 for individuals. If you live in a state with meaningful income or property taxes, you likely cross that threshold now. There’s also a new $6,000 senior deduction for taxpayers 65 and older, available whether you itemize or not, though it phases out above $75,000 for singles and $150,000 for married couples. A brand-new vehicle interest deduction of up to $10,000 applies to loans for U.S.-assembled cars purchased between 2025 and 2028, with phase-outs starting at $100,000 MAGI for singles and $200,000 for married filers. The federal gift and estate tax exemption rises to $15 million per individual and $30 million for married couples in 2026, with inflation adjustments thereafter-a significant window if you plan wealth transfers.

Your 401(k) contribution limit for 2026 reaches $72,000, and IRAs max out at $7,000, with catch-up contributions adding $7,500 and $1,000 respectively for those 50 and older. HSA limits increased to $4,300 for individuals and $8,550 for families, offering triple tax benefits: contributions reduce taxable income, growth stays tax-free, and withdrawals for qualified medical expenses never face taxation. Starting in 2026, bronze and catastrophic health plans become HSA-compatible, expanding access significantly. The Child Tax Credit remains at $2,200 per qualifying child under 17, while the Earned Income Tax Credit maxes out at $649 for those with no qualifying children. A new Trump Account for children under 18 allows $5,000 in annual contributions, with a one-time government seed of $1,000 for births between 2025 and 2028. Roth IRA conversions remain available, though converting raises your adjusted gross income and can affect other deductions-coordinate this move carefully with your tax strategy.

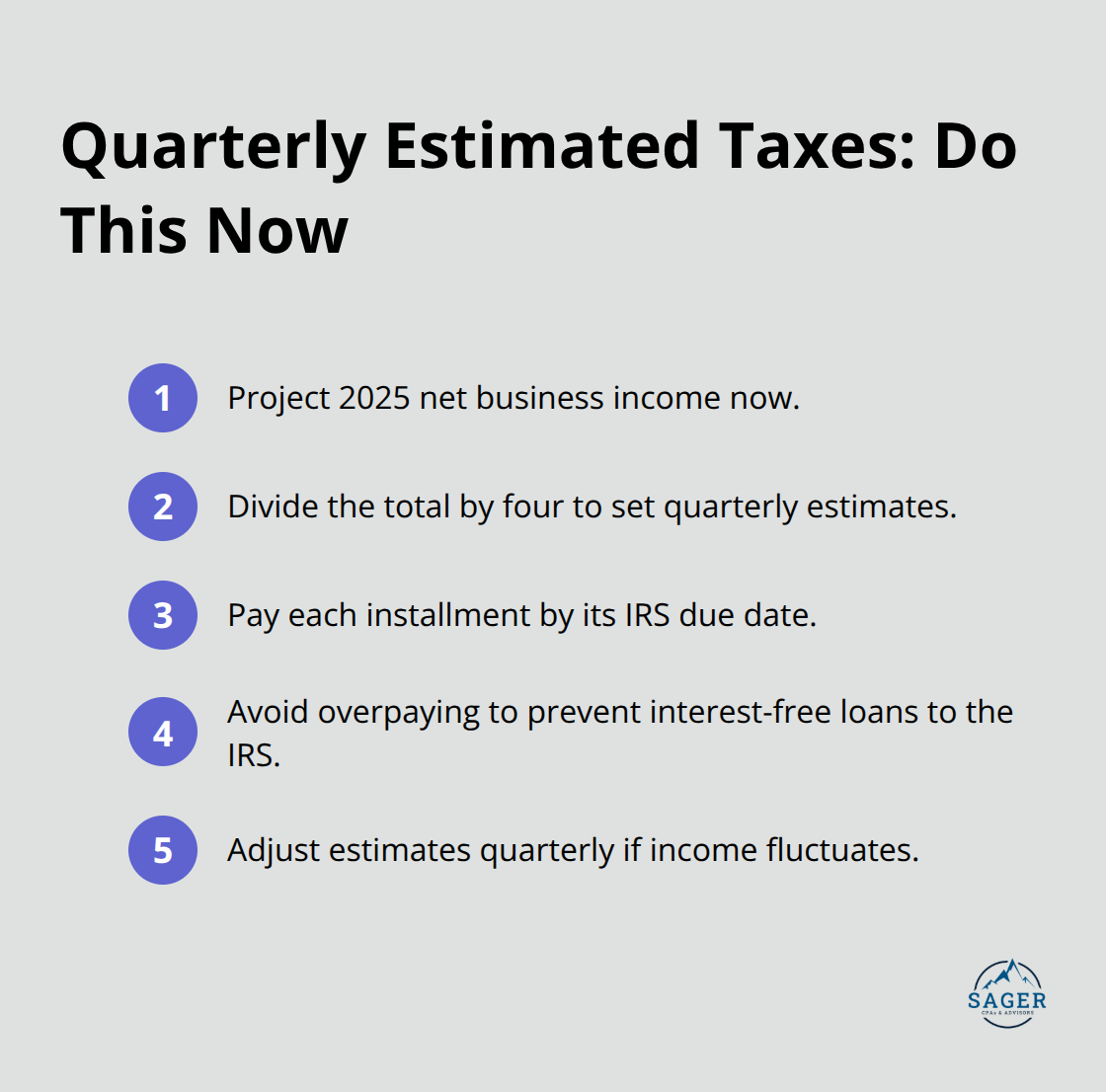

Self-employed individuals and business owners face stricter reporting obligations. If you process more than $20,000 in payments across over 200 transactions through payment apps or online marketplaces in 2025, you’ll receive Form 1099-K in January 2026, and the IRS will have a copy too. Backup withholding thresholds for third-party networks increased to apply only when total payments exceed $20,000 and more than 200 transactions occur in a calendar year, reducing withholding burden for smaller sellers. Quarterly estimated tax payments remain mandatory if you have substantial non-wage income-self-employment, investments, taxable Social Security, or pensions. The year splits into four periods, with the final payment due in mid-January. Missed quarterly payments trigger penalties that compound, making this one of the easiest mistakes to prevent if you plan ahead.

A new 1% excise tax on remittance transfers begins January 1, 2026, requiring providers to collect and remit semimonthly, with first deposits due January 29, 2026. Clean vehicle credits expire for acquisitions after September 30, 2025, and home energy credits end for property placed in service after December 31, 2025. If you’re considering either purchase or upgrade, timing matters significantly. These deadlines create urgency-waiting until late 2025 to evaluate whether these credits apply to your situation leaves little room for action. The window to capture these benefits closes fast, and once it does, you lose the opportunity entirely. Understanding which credits apply to your circumstances now positions you to make informed decisions about timing and investment.

The 2025 tax changes create a unique opportunity to stop reacting and start planning. Most taxpayers wait for their documents to arrive in January, then scramble through April. That approach costs you thousands. We recommend starting your strategy now, while you control the timing of income, deductions, and account contributions.

Your filing status, state of residence, and business structure determine whether you benefit from the new SALT cap increase, the senior deduction, or the vehicle interest write-off. If you’re married and live in a high-tax state like California or New York, the $40,000 SALT cap through 2029 likely shifts you from the standard deduction to itemizing. Calculate this now. Add your state income taxes plus property taxes. If that sum exceeds $31,500, you itemize and capture the full benefit.

If you’re self-employed, the equation changes entirely. Your quarterly estimated tax obligations don’t disappear-they demand precision. The IRS expects four payments throughout 2025, with the final payment due January 15, 2026.

Missing even one triggers penalties that compound. Conversely, overpaying those estimates means you give the IRS an interest-free loan. The solution is straightforward: implement proactive tax planning by projecting your 2025 net business income now, dividing by four, and scheduling payments before each deadline.

For retirement accounts, 2026 limits reach $24,500 for 401(k)s and $7,500 for traditional or Roth IRAs, with catch-up contributions of $8,000 and $1,000 respectively for those 50 and older. The contribution deadline for 2025 IRAs is April 15, 2026, but HSA contributions close on the same date. If you’re eligible for an HSA under your health plan, maxing it out at $4,300 for individuals or $8,550 for families delivers immediate tax savings plus tax-free growth for medical expenses. Starting in 2026, bronze and catastrophic plans qualify for HSA contributions, expanding eligibility significantly.

For business owners considering structure changes, the timing matters significantly. If you operate as a sole proprietor, converting to an S-corporation or LLC can reduce self-employment taxes on distributions, though setup costs and ongoing compliance requirements apply. This decision requires comparing your net business income against the administrative burden. A business generating $100,000 in net income typically benefits from an S-corp election; one generating $30,000 may not.

The vehicle interest deduction of up to $10,000 for U.S.-assembled cars purchased through 2028 applies only to new vehicles financed with loans, not leases. If you’re planning a vehicle purchase, verify the VIN on the NHTSA website to confirm assembly location before finalizing the purchase. Estate planning windows are opening wider. The $15 million individual exemption and $30 million couple exemption in 2026 mean substantial gifts or trust structures established now capture current values before they appreciate. Donor-advised funds offer immediate tax deductions in 2025 while allowing you to distribute funds to charities over years, splitting the tax benefit across your current bracket.

None of these moves happen automatically. Your tax outcome depends on decisions you make in the next 60 days-and the guidance you receive shapes whether those decisions work in your favor or against it.

Quarterly estimated tax payments trip up most self-employed workers and business owners because the IRS expects four separate payments throughout the year, each due on specific dates regardless of whether you’ve received income yet. The final payment for 2025 is due January 15, 2026. Miss even one deadline and penalties accumulate at 0.5% of the unpaid tax per month, compounding your liability beyond the original shortfall. The math is brutal: if you owe $10,000 in quarterly taxes and skip all four payments, penalties alone can exceed $500 by April.

Project your 2025 net business income now, divide it into four equal installments, and schedule payments before each deadline rather than waiting to see how the year actually unfolds. Many business owners assume they can catch up with a single large payment in April, but the IRS penalizes every missed quarter independently. If your income fluctuates significantly, adjust your estimates quarterly rather than locking in fixed amounts. The penalty relief available for the first three quarters of 2026 does not extend backward, so correcting 2025 shortfalls costs you real money.

Documentation failures create a second category of costly errors that audits expose immediately. The IRS allows deductions only when you can prove them with contemporaneous records, and most business owners keep receipts scattered across email, credit card statements, and desk drawers rather than organized by category. A 2025 Thomson Reuters Institute survey found that 75% of tax professionals report clients strongly desire more comprehensive tax guidance, yet many still approach record-keeping casually. Deductions claimed without supporting documentation get disallowed entirely, and if the IRS questions your return, reconstructing three years of receipts becomes exponentially harder than maintaining organized files from the start.

Property improvements, vehicle expenses, professional development costs, and home office allocations require specific documentation standards. Home office deductions demand either actual expense records (utilities, insurance, repairs proportional to square footage) or the simplified method of $5 per square foot up to 300 square feet. Choose one method for the year and stick with it. Vehicle deductions require contemporaneous mileage logs showing date, destination, business purpose, and miles driven; credit card receipts alone won’t suffice if you face audit scrutiny.

File extensions and amendments represent a third mistake category that compounds when you file late without understanding the consequences. An extension delays your filing deadline to October 15 but does not extend your payment deadline, which remains April 15. File an extension without paying estimated tax due and you trigger failure-to-pay penalties on the balance owed, even though you technically filed on time. Amendments filed after the statute of limitations closes permanently forfeit any refund claims, so delaying an amendment that’s in your favor costs you the entire refund amount.

The statute of limitations runs three years from the original filing date for most situations, but six years if you underreport income by 25% or more, and indefinitely if fraud is involved. Amend proactively within that window to protect refunds you’re entitled to, while waiting beyond three years locks you out permanently.

The 2025 tax landscape demands action now, not in April. Every decision you delay costs you money-whether that’s missing the deadline for a retirement contribution, failing to time a business structure change, or overlooking a deduction window that closes permanently. The One Big Beautiful Bill created genuine opportunities for taxpayers willing to plan strategically, but those opportunities evaporate if you wait until tax season arrives.

Working with a tax professional transforms how you approach these decisions. A qualified advisor identifies which changes apply to your specific situation, calculates whether itemizing beats the standard deduction for you, and structures your business to minimize what you owe. Most people need help translating tax law changes into actionable moves that actually reduce their liability while keeping them compliant with IRS requirements.

Personalized tax solutions for 2025 start with understanding your filing status, income sources, state of residence, and business structure. We at Sager CPA help individuals and businesses navigate exactly this kind of complexity by combining precise accounting with strategic advisory services designed to reduce your tax liability. Contact Sager CPA today to discuss how we position you for a stronger financial future.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.