Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Most small business owners can tell you their revenue. Few can explain where their cash actually goes.

At Sager CPA, we’ve seen this gap destroy otherwise healthy businesses. Financial clarity for SMBs isn’t optional-it’s the difference between thriving and struggling. This guide walks you through the cash flow and cost management strategies that actually work.

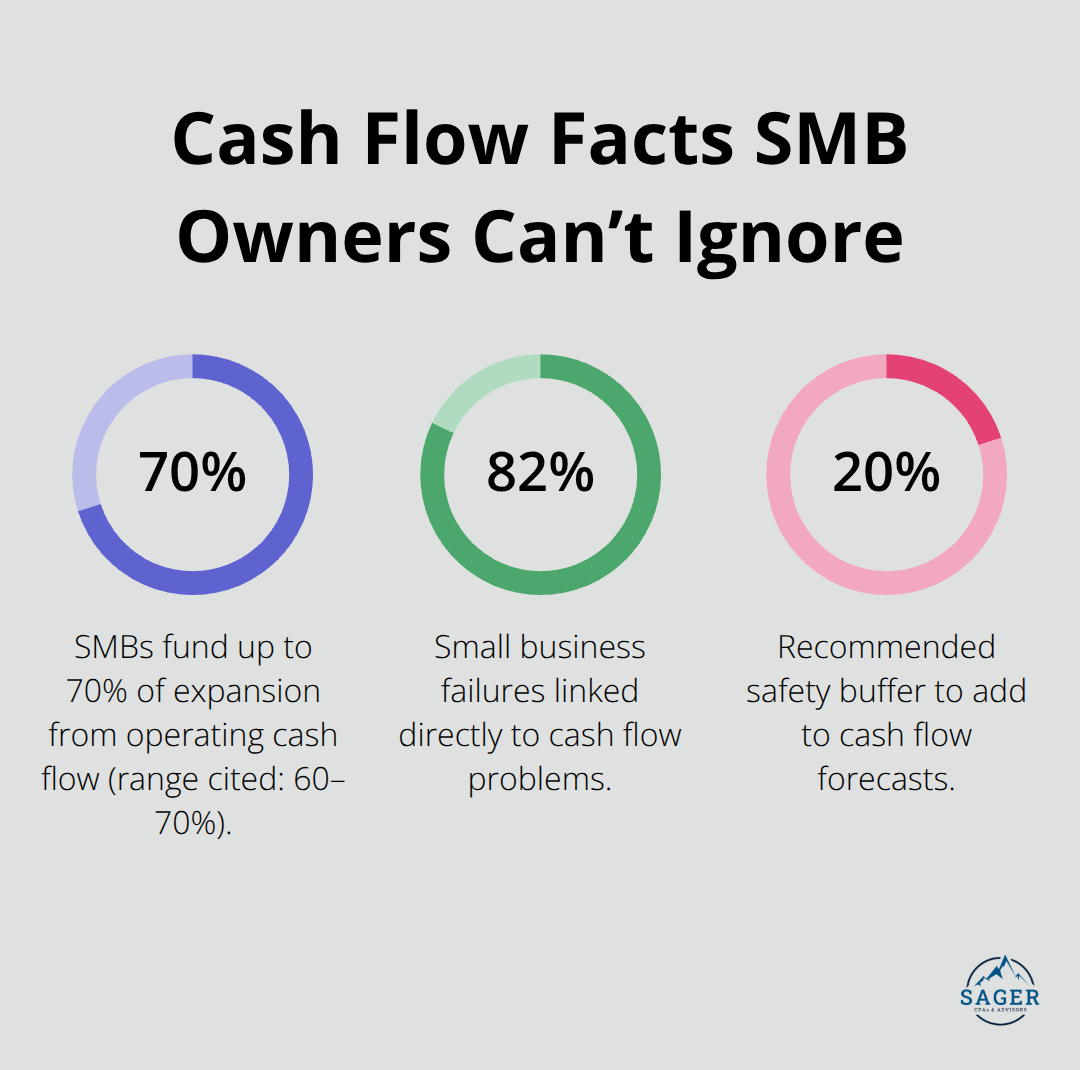

Cash flow is the movement of money in and out of your business, and it determines whether you survive. Operating cash flow-the cash generated from your core business operations-funds payroll, covers rent, and pays suppliers. Most SMBs fund about 60 to 70% of their expansion through operating cash flow, which means weak operating cash flow stops growth regardless of what your profit statement shows. A striking 82% of small business failures link directly to cash flow problems, not poor products or services. This statistic should shift how you view your financial statements. You need to know your operating cash flow before you know anything else about your business.

Your profit statement tells you whether you made money on paper. Your cash flow statement tells you whether you have money in the bank. These are not the same thing. A business can show a healthy profit while running out of cash because revenue recognition happens when you invoice a customer, not when they pay you. If your customers take 60 days to pay and your suppliers demand payment in 30 days, you face a cash problem even if you’re profitable. The cash conversion cycle measures exactly how quickly your business turns operations into real cash in the bank, and this separates businesses that thrive from those that collapse. When profits and operating cash flow drift apart, investigate your accounts receivable aging to see how long customers actually take to pay, check whether inventory piles up, and verify that revenue recognition matches reality. The Indirect Method, which most firms use to calculate cash from operations, starts with net income and then adjusts for non-cash expenses like depreciation and changes in working capital. This adjustment process reveals why a company posting strong earnings might actually burn cash.

Positive operating cash flow pays for equipment investments, debt repayment, and shareholder distributions. When you have consistent positive operating cash flow, you control your own destiny. When operating cash flow turns negative while net income stays positive, you have a red flag that demands immediate action. This situation typically signals slow collections or excess inventory consuming working capital. Address accounts receivable management by offering early-payment discounts to reduce days sales outstanding, and review inventory control to prevent capital from sitting idle on shelves. Conversely, if you see consistently positive financing cash flow-meaning you’re borrowing money or raising equity just to cover day-to-day expenses-your underlying operations need fixing. This warning sign indicates that your business model isn’t producing enough cash from its core activities to sustain itself.

The difference between thriving and struggling often comes down to how well you manage the timing of money moving in versus money moving out. Most businesses don’t fail because they lack customers or products; they fail because cash runs out before revenue arrives. This timing gap creates real pressure on your operations, and understanding it helps you take action before the problem becomes critical. The next section walks you through how to identify and categorize the costs that create this timing pressure in the first place.

Fixed costs hit your account every month regardless of sales volume, while variable costs fluctuate with production or service delivery. Rent, insurance, and salaries are fixed; materials, packaging, and hourly labor are variable. Most SMB owners underestimate fixed costs when projecting profitability, and this mistake compounds quickly. A service business might have low variable costs but crushing fixed overhead that makes each new client less profitable than the math suggests.

To find your break-even point, divide your total fixed costs by the difference between your sales price per unit and variable cost per unit. If you operate with high fixed costs and thin margins, you need significantly higher volume to survive a slow month. Seasonal businesses often struggle because their fixed costs don’t pause when revenue drops. Calculate your fixed and variable costs separately for each revenue stream or product line-many SMBs discover that one product line carries the entire company while another drains cash despite looking profitable on paper.

Hidden costs wreak havoc on cash flow forecasts because they’re invisible until they become catastrophic. Unused software licenses accumulate quickly, and the average SMB wastes thousands annually on subscriptions nobody uses. Aging hardware forces expensive emergency repairs and downtime; unexpected outages create significant operational losses.

Cybersecurity breaches cost an average of $4.88 million, yet most SMBs treat security as optional. Poor accounts receivable management creates a hidden cost that compounds monthly-if your customers take 60 days to pay instead of 30, you’re financing their operations. Inventory sitting on shelves ties up working capital that could cover payroll. Inaccurate bookkeeping creates the worst hidden cost of all because you can’t fix what you can’t see.

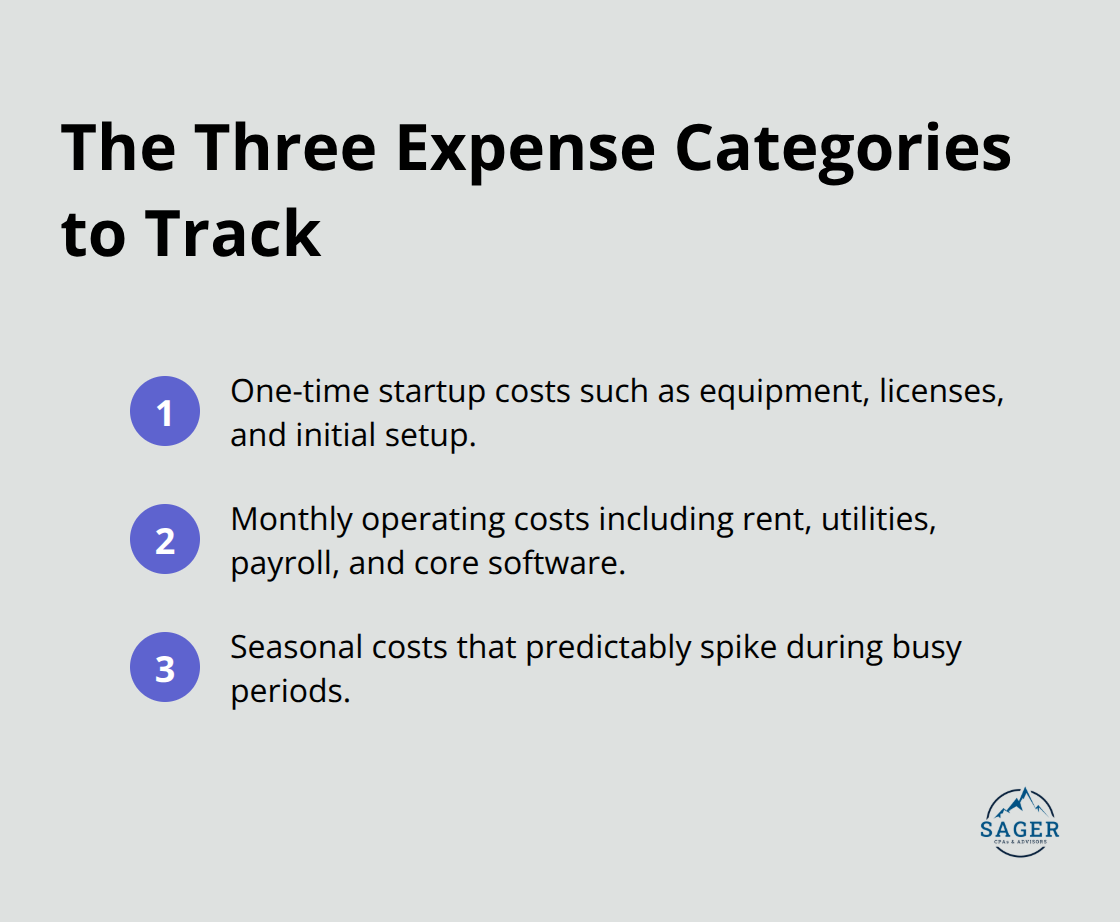

Start tracking expenses in three categories: one-time startup costs, monthly operating costs, and seasonal costs that spike during predictable periods. Review your expense list monthly and ask which items directly generate revenue.

Anything that doesn’t should be scrutinized for elimination or reduction. Software consolidation alone typically saves SMBs thousands yearly-standardizing on fewer platforms reduces support tickets, simplifies security governance, and cuts licensing waste.

This expense clarity sets the foundation for the next step: building a realistic forecast that accounts for when money actually moves in and out of your business.

The gap between forecasting cash flow and actually executing it destroys more SMB growth plans than bad markets ever will. Most owners guess at their monthly cash needs instead of calculating them, then panic when reality doesn’t match their assumptions. Start with a foundation: list every fixed cost that hits your account monthly, then add variable costs based on realistic revenue projections for the next 12 months. This forces you to confront timing issues immediately.

If you invoice customers net-30 but pay suppliers net-15, you need working capital to bridge that gap. Calculate your cash conversion cycle by tracking how long it takes from paying for inventory to collecting cash from customers, then add a 20% safety buffer to your forecast. Seasonal businesses need separate forecasts for peak and off-peak months rather than averaging the year, because averages hide the months when cash actually runs dry.

Update your forecast monthly as real numbers arrive, comparing actual cash movement to what you predicted. This comparison reveals whether your assumptions about customer payment timing or inventory turnover match reality. Most SMBs discover their customers actually take 45 days to pay instead of 30, or that seasonal dips last six weeks longer than expected.

These discoveries should trigger immediate action: tighten accounts receivable collection, reduce inventory ordering during slow periods, or negotiate extended payment terms with suppliers. The sooner you identify gaps between forecast and reality, the sooner you can adjust operations to protect cash.

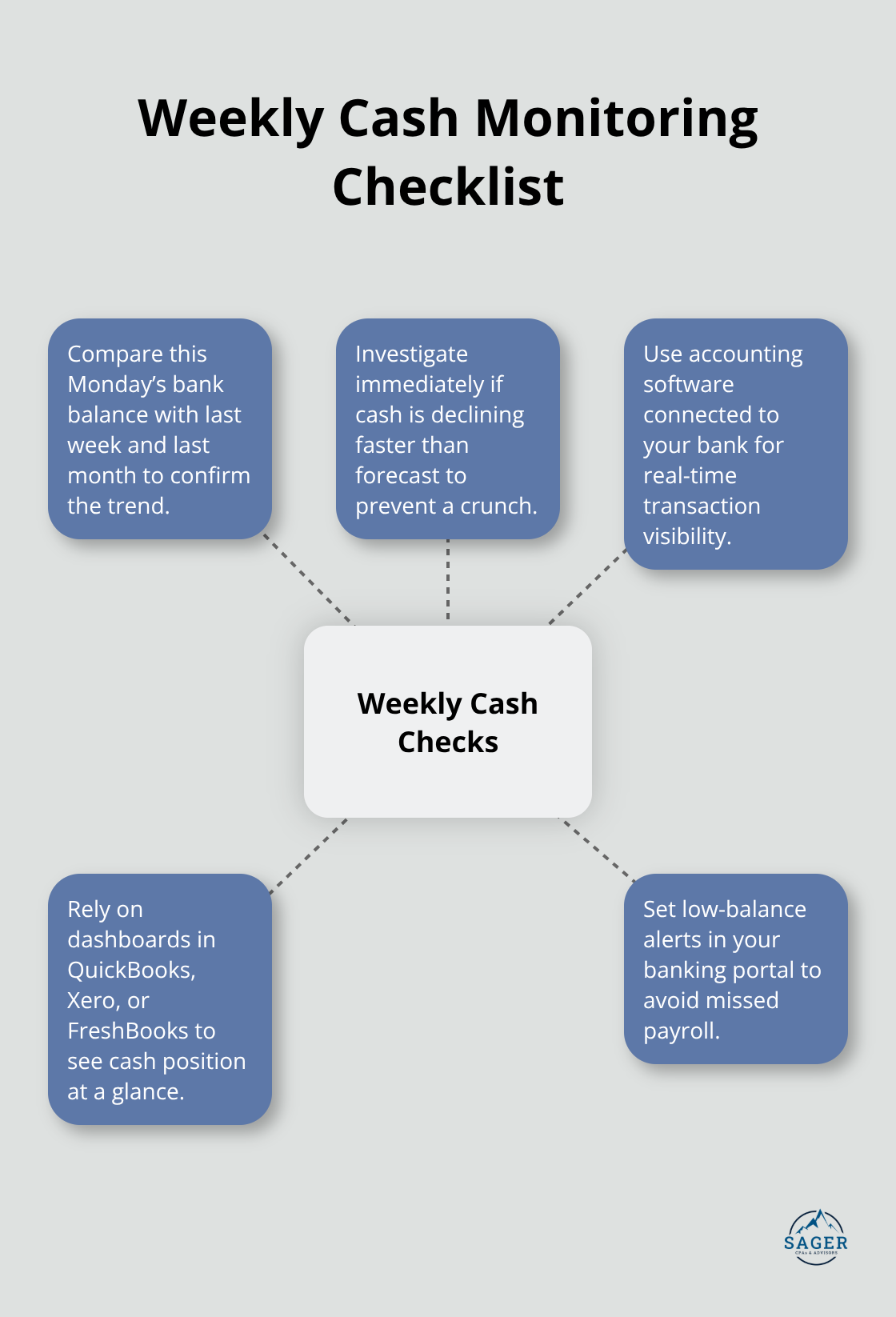

Monitoring cash flow weekly rather than monthly separates businesses that catch problems early from those that discover them too late. Pull your bank balance every Monday morning and compare it to the same day last week and last month, then ask whether that trajectory aligns with your forecast. If cash is declining faster than expected, investigate immediately instead of waiting for a monthly close.

Weekly cash checks take 15 minutes but reveal collection problems, unexpected expenses, or timing mismatches before they become crises. Use accounting software that connects directly to your bank account so you see transactions in real time rather than waiting for manual entry. QuickBooks, Xero, or FreshBooks all provide dashboard views that show cash position at a glance. Set up alerts in your banking portal for low balance thresholds so you never accidentally miss payroll.

The reality is that most SMBs operate with thin margins, meaning a single slow customer or unexpected expense can flip the cash position from comfortable to critical within weeks. Weekly monitoring converts cash flow from a mystery into a controllable variable. Seasonal businesses should monitor even more frequently during their peak season, when inventory investments and payroll surges create the biggest cash demands.

Financial clarity for SMBs comes down to one simple truth: you cannot manage what you do not measure. Cash flow and cost management are not accounting exercises-they’re survival tools. The businesses that thrive know their operating cash flow, understand the timing gap between when money leaves and when it arrives, and track expenses with ruthless honesty.

The gap between profit and cash flow has destroyed more promising businesses than market downturns ever will. A company posting strong earnings while cash dwindles heads toward a wall. Weekly cash monitoring, accurate expense categorization, and realistic forecasting transform cash flow from a source of anxiety into a controllable variable. When you know your break-even point, understand your fixed versus variable costs, and catch hidden expenses before they compound, you gain the ability to make decisions from strength rather than desperation.

Start this week by pulling your last three months of bank statements and categorizing every expense as fixed or variable. Calculate your cash conversion cycle and compare your actual customer payment timing to what you assumed. If you’re ready to move beyond guesswork and build a financial strategy tailored to your business, we at Sager CPA can help-schedule a consultation with us to create a personalized financial strategy that gives you the clarity and confidence to grow without constant worry about cash.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.