Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

You earn a strong income, yet financial stress still creeps in. That’s because financial planning for professionals isn’t just about making more money-it’s about making your money work strategically for your career goals.

At Sager CPA, we’ve seen talented professionals leave thousands on the table through missed tax strategies, poor investment choices, and unclear financial direction. The good news is that clarity changes everything.

High earners often assume their income handles everything. A 2018 National Health Interview Survey of over 22,000 U.S. adults revealed that financial worries spike psychological distress regardless of income level, with each point increase in financial anxiety linked to a 0.315-point jump in psychological distress. This means earning $200,000 annually doesn’t shield you from the stress of misaligned finances. The real issue is that professionals conflate earning power with financial security, two entirely different things. Your paycheck covers expenses, but it doesn’t automatically create a strategy that protects your wealth, minimizes taxes, or positions you for the next career move. Without intentional planning, that six-figure salary becomes just another expense-driven lifestyle where money flows in and flows out without purpose.

Your schedule is packed. Client meetings, project deadlines, team management, and industry obligations consume your hours. Adding financial planning to an already maxed-out calendar feels impossible, so it doesn’t happen. The problem is that postponing planning costs you more than the time you’d spend addressing it now. A professional earning $150,000 annually who misses tax deductions loses money in taxes annually, depending on their bracket. Over a decade, that’s significant avoidable losses. Unemployed individuals show a 0.329 correlation between financial worries and distress compared to 0.236 for employed professionals, according to the 2018 survey data, but employed high earners who fail to plan experience their own version of that stress through opportunity cost and inefficiency. The solution isn’t finding more time; it’s recognizing that financial planning is part of career management, not separate from it. When you treat it as essential rather than optional, it moves from the never-ending to-do list into your quarterly priorities.

Financial guidance aimed at the general population doesn’t fit your situation. Standard retirement calculators assume average income trajectories and standard deductions. Your career path, income volatility, bonus structures, stock options, and professional expenses are different. Married professionals show a weaker link between financial worries and distress (−0.070 interaction effect) than unmarried counterparts, yet many married high earners still lack coordinated financial strategies because they’ve received only generic advice. Homeowners experience lower worry-related distress than renters, but without a plan addressing your specific mortgage, equity position, and investment strategy, homeownership alone doesn’t protect you. You need guidance that speaks to your actual situation: your compensation structure, the investment strategy that matches your risk tolerance and timeline, the insurance gaps that could derail your career, and the estate decisions that protect what you’ve built. Generic financial planning misses these specifics entirely, which is why professionals with complex income situations benefit from advisors who understand their unique circumstances.

Your compensation structure shapes everything that follows. Most professionals receive a salary, but many also have bonuses, stock options, deferred compensation, or variable income streams. Each component requires different planning. A $150,000 salary with a $50,000 annual bonus and stock grants differs fundamentally from a straight $200,000 salary, yet many professionals treat them identically for planning purposes. The bonus creates a spike in taxable income that demands strategic withholding and estimated tax payments. Stock grants introduce vesting schedules, potential concentrated positions, and capital gains timing decisions. Deferred compensation plans allow you to push income into future years, which can lower your current tax bracket and align income with retirement timing. Map your actual compensation first: base salary, bonus structure, vesting schedules, option exercise prices, and any deferred amounts. Once you see the full picture, you make intentional decisions instead of reacting to tax bills each year.

Tax efficiency at higher income levels isn’t about finding loopholes; it’s about using legal structures that Congress designed for your situation. Professionals in the top tax brackets pay 37% federal tax on ordinary income, plus state taxes that can exceed 10% in high-tax states. A married professional earning $250,000 in California faces a combined federal and state rate exceeding 50% on additional income. That means half of every additional dollar vanishes unless you use tax-advantaged accounts and strategies.

Contributing the maximum to a 401k reduces taxable income by $23,500 in 2024, saving over $8,700 in combined federal and state taxes for a high earner. An HSA paired with a high-deductible health plan provides triple tax benefits: deductible contributions, tax-free growth, and tax-free withdrawals for medical expenses. Roth conversions shift income into years when your tax bracket is lower, locking in current rates before retirement. Charitable giving through donor-advised funds lets you bunch donations into high-income years and take the deduction immediately while distributing to charities over time. Tax-loss harvesting in taxable investment accounts offsets gains throughout the year. These aren’t exotic strategies; they’re standard tools that professionals overlook because they lack someone translating tax code into action. Without intentional tax planning, you write larger checks to the IRS than necessary.

Building wealth requires separating what you earn from what you keep, then making the kept portion work for your future. A professional earning $200,000 annually who spends $180,000 and invests $20,000 accumulates far less wealth than someone earning $150,000, spending $100,000, and investing $50,000. The difference isn’t income; it’s intentional allocation.

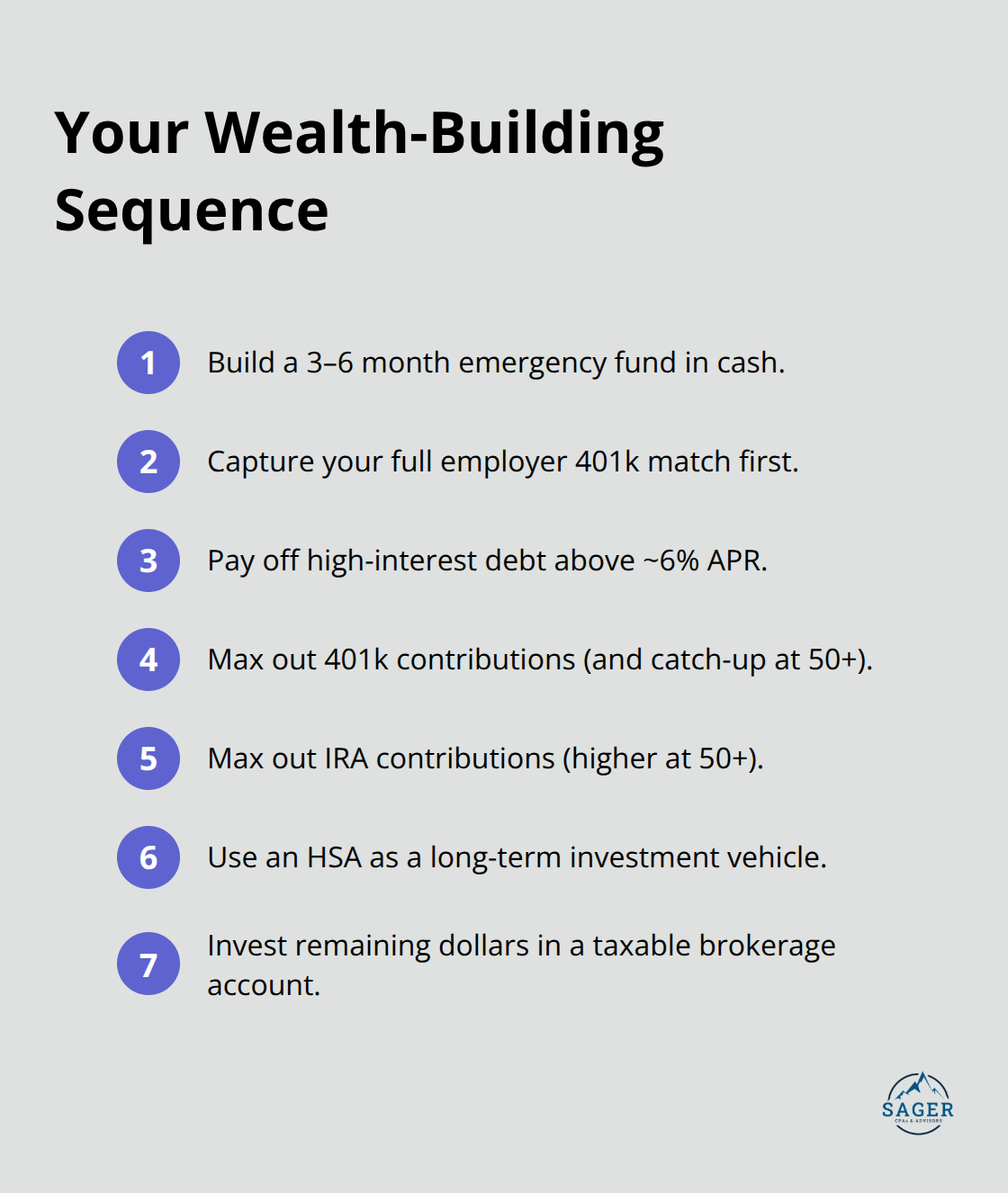

Start with an emergency fund of three to six months of essential expenses, not discretionary spending. This typically means $30,000 to $60,000 for high-earning professionals, and it should sit in a high-yield savings account earning 4–5% annually, not tied up in investments.

Next, capture your full employer 401k match because it’s an immediate guaranteed return. Then address high-interest debt above 6% APR before aggressive investing beyond the match.

Once debt is managed and the match is captured, max out your 401k contributions at $23,500 annually in 2024, and from age 50 onward, add another $7,500 in catch-up contributions. Max out an IRA contribution at $7,000 annually, or $8,000 at age 50 plus. If you have access to an HSA, treat it as a retirement account by investing the balance beyond immediate medical needs. Only after these tax-advantaged accounts are maximized should you invest in taxable brokerage accounts. This hierarchy matters because it forces discipline and ensures your wealth-building strategy follows tax-efficient sequences rather than scattered decisions. Professionals who follow this approach consistently reach significant wealth accumulation by their 40s and 50s because compounding works on a deliberate foundation, not random choices.

Your compensation structure and tax-efficient allocation form the foundation, but they only work when you coordinate them with your broader financial picture. The next step involves aligning these income and investment decisions with protection strategies that safeguard what you’ve built.

Most professionals stumble into financial mistakes not from recklessness but from gaps in execution. You’ve structured your compensation thoughtfully and allocated funds strategically, yet transitions, tax oversights, and allocation drift still derail your progress. A professional earning $200,000 who misses $15,000 in deductible business expenses loses $5,550 in federal taxes alone at a 37% bracket, plus state taxes that could exceed $1,500 combined. Over five years, that totals over $36,000 in avoidable losses. The mistakes aren’t conceptual; they’re operational blind spots that emerge during life changes, seasonal income spikes, or when your financial situation outgrows your previous approach.

Divorce, remarriage, job changes, home purchases, and inheritance events shift your tax position and asset structure overnight, yet most professionals continue executing the same financial playbook from last year. A married professional who goes through divorce faces sudden changes to filing status, child support obligations, alimony treatment, and asset division timing. These transitions demand immediate tax planning adjustments because the IRS doesn’t care about your personal circumstances; it cares about your tax filing status and income recognition. Similarly, a bonus or stock grant vesting creates concentrated income in a single year that demands different withholding and estimated tax calculations than your regular salary. Professionals who don’t adjust their tax strategy for these events either overpay significantly or underpay and face penalties plus interest. Treat major transitions as financial planning triggers, not just life events. When you change jobs, marry, divorce, inherit assets, or experience significant income shifts, that’s when you need to review your tax position, beneficiary designations, and insurance coverage.

High earners in professional services, real estate, consulting, and specialized trades often have deductible business expenses that go uncaptured because they lack systems to track them. Vehicle and mileage expenses, home office deductions, professional development, equipment purchases, meals with clients, and subscriptions to industry publications are deductible, yet professionals frequently either don’t track them or don’t claim them because they lack documentation. The IRS allows home office deductions of either $5 per square foot up to 300 square feet or your actual expenses including utilities, insurance, and depreciation, yet most remote professionals claim nothing. A consultant with a 200-square-foot home office working 50% of the time could deduct $500 annually under the simplified method alone, but that requires intentional tracking and filing. Without documentation systems, these deductions vanish, and you pay taxes on income you could have legitimately reduced.

Your portfolio doesn’t match your stated goals or risk tolerance when allocation drift occurs. A professional who invested 80% equities at age 35 correctly may still hold 80% equities at age 55 without reassessing. Market performance creates unintended allocation shifts; an equity-heavy portfolio that gains 15% while bonds gain 3% gradually becomes more aggressive than intended. At age 55, that aggressive allocation increases sequence-of-returns risk heading into retirement, meaning a market downturn in your early retirement years damages your long-term outcomes disproportionately. Professionals should review asset allocation annually and rebalance when allocations drift more than 5% from targets. This requires discipline because rebalancing means selling winners and buying losers, which feels counterintuitive during bull markets.

The cure for all three mistakes involves establishing systems that catch these gaps before they cost you money. A calendar reminder for transition reviews ensures you address tax and beneficiary changes when life events occur. A folder system for deduction documentation captures expenses throughout the year so you don’t scramble during tax season. An annual allocation audit confirms your portfolio still matches your risk tolerance and timeline. These operational habits prevent the costly gaps that income and strategy alone can’t fix. Without systems, even well-intentioned professionals miss opportunities and overpay taxes year after year.

Financial clarity separates those who accumulate wealth from those who simply earn it. Your income alone doesn’t determine your financial security-your compensation structure, tax strategy, allocation discipline, and operational systems do. A professional earning $200,000 who misses tax deductions, fails to rebalance, and lacks transition planning ends up with far less wealth than someone earning $150,000 who executes intentionally across all four areas.

Research shows that financial worries affect professionals at every income level, and those worries translate directly into stress that impacts your career performance and personal wellbeing. The solution isn’t earning more; it’s gaining clarity about where your money goes, how it’s taxed, and whether it’s positioned to support your actual goals rather than your lifestyle. Professional guidance accelerates this clarity significantly because you’ve built your career by surrounding yourself with specialists in your field.

Your financial life deserves the same approach. Schedule a consultation with Sager CPA to create a personalized financial planning for professionals strategy that reflects your actual situation, not generic assumptions. Financial planning for professionals isn’t about complexity for its own sake-it’s about clarity that powers your career growth and protects what you’ve built.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.