Financial Risk Management Startup: Build Resilience Into Your Growth Plan

Build financial resilience into your startup's growth plan with proven risk management strategies that protect profits and accelerate scaling.

Most business owners focus on revenue targets but ignore the financial roadmap needed to reach them. Business financial planning bridges that gap by turning strategy into concrete numbers and actions.

At Sager CPA, we’ve seen firsthand how companies that plan financially outperform those that don’t. The difference comes down to clarity, control, and confidence in your numbers.

Financial planning forces you to answer hard questions that most business owners avoid. What will your cash position look like in six months if a major client leaves? How much operating expense can you actually afford without crushing profitability? When should you invest in growth versus protecting reserves? These aren’t theoretical exercises-they directly determine whether your business survives downturns and capitalizes on opportunities. A 3–5 year planning horizon with cash flow as your primary liquidity metric helps you secure funding and guides long-term growth decisions. Without this framework, you’re essentially flying blind, reacting to problems instead of preventing them.

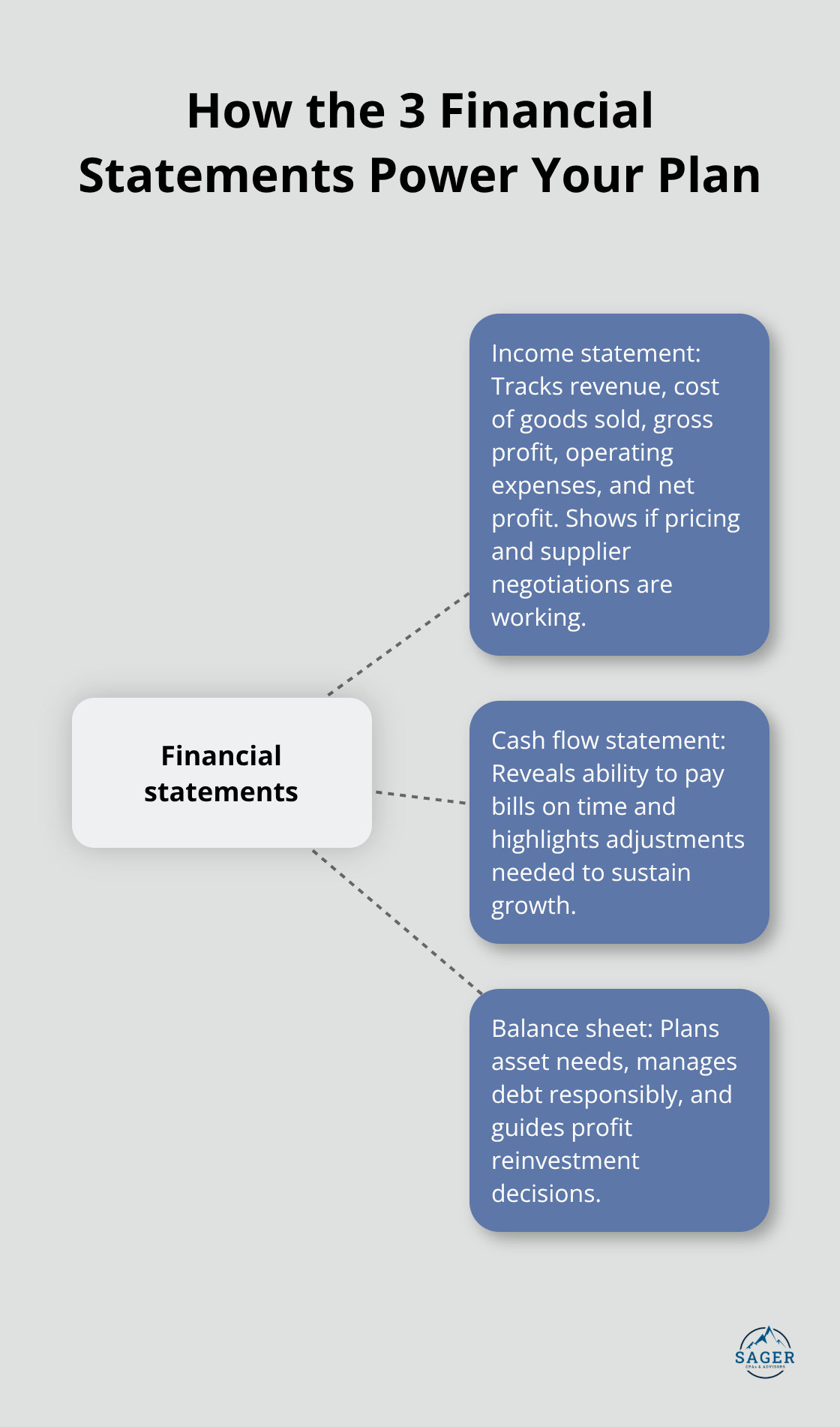

Business strategy and financial planning must move together or your strategy fails. You might decide to enter a new market or launch a product line, but without projecting the cash requirements, timeline to profitability, and impact on your existing cash flow, you’re just guessing. Financial planning translates your strategic ambitions into concrete revenue targets, expense budgets, and cash milestones. The income statement tracks your revenue, cost of goods sold, gross profit, operating expenses, and net profit-these numbers tell you whether your pricing strategy actually works and whether your supplier negotiations are paying off. The cash flow statement reveals whether you can pay bills on time and what adjustments need to happen to sustain growth. The balance sheet helps you plan asset needs, manage debt levels responsibly, and decide how much profit to reinvest. Together, these three statements answer whether your strategy is financially viable before you commit significant resources.

Risk management in business happens through data, not intuition. Expense forecasting that covers fixed, variable, one-time, semi-variable, and hidden costs lets you spot cost overruns before they damage cash flow. Benchmarking your rent as a percentage of revenue against industry norms immediately shows whether your real estate costs are competitive. Break-even analysis translates your strategy into a concrete sales target and helps you stress-test whether your pricing and cost structure actually work. Monthly cash flow projections for at least 12 months (capturing starting balance, inflows, outflows, and ending cash) reveal seasonal swings and supplier payment term opportunities you’d otherwise miss. Identifying high-impact threats and building contingency plans and emergency funds separates businesses that survive disruptions from those that collapse when conditions shift.

The next section explores how to build a financial plan that actually works for your business.

Start with an honest assessment of where your business stands right now. Pull together your last 12 months of bank statements, tax returns, and accounting records to understand your actual revenue, expenses, and cash position. This isn’t about creating a polished narrative for investors-it’s about seeing the real numbers so you can build projections that matter.

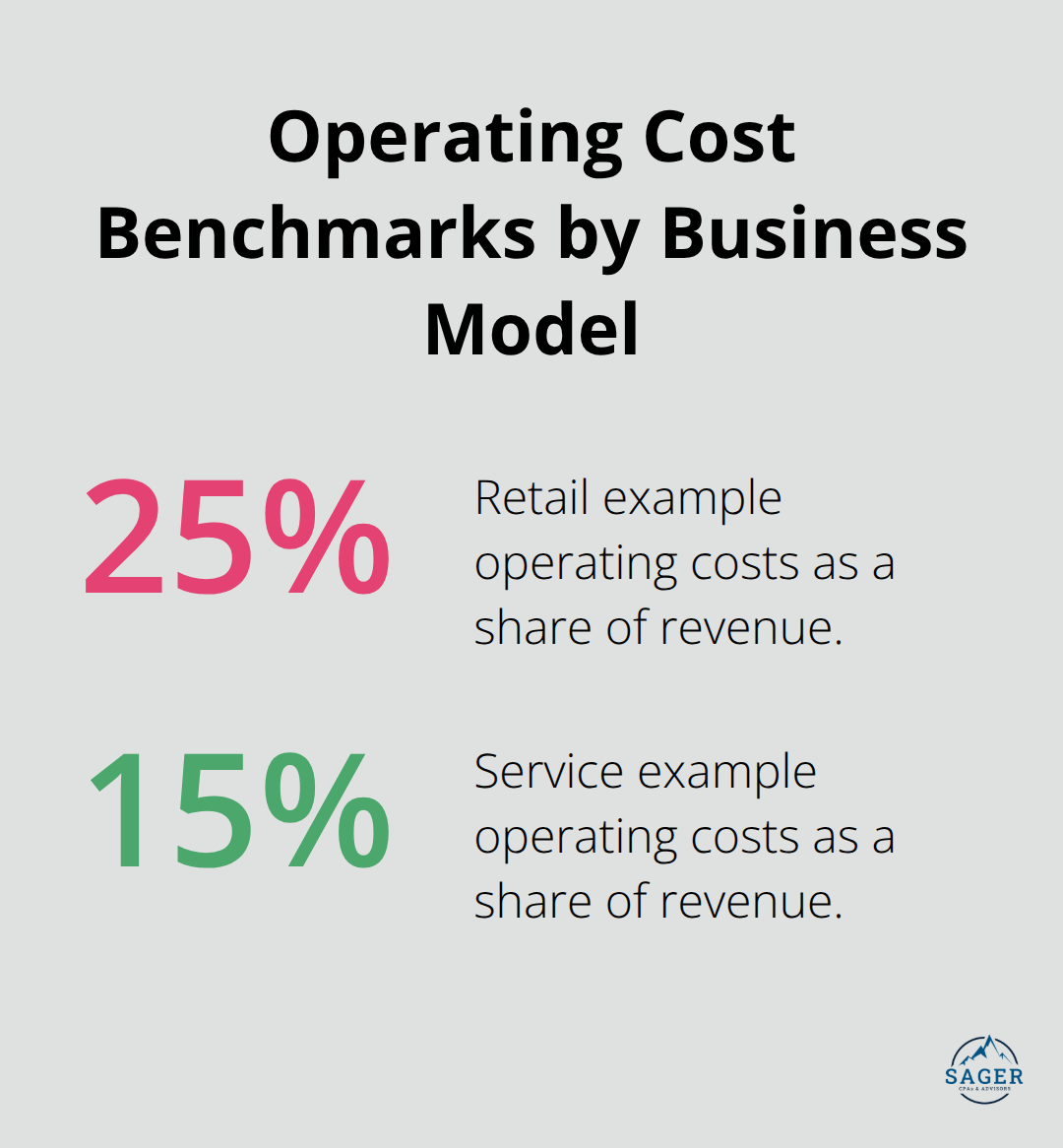

Look at your gross profit margin by comparing revenue to your cost of goods sold. Check your operating expense ratio by dividing total operating expenses by revenue. A retail business running at 25% of revenue in operating costs faces very different constraints than a service business at 15%.

Examine your accounts receivable aging to see how long clients actually take to pay you, not how long you think they should. If your terms say net 30 but customers pay in 45 days on average, that 15-day gap directly impacts your cash position.

Calculate your current cash conversion cycle by tracking how many days pass between paying suppliers and collecting from customers. A manufacturing business might have a 90-day cycle while a SaaS company might have negative days because they collect upfront. These baseline metrics become your reference point for realistic projections.

Bottom-up forecasting starts with your sales pipeline and unit economics. If you have 10 sales reps each carrying a pipeline worth 8 times their annual quota, and your historical close rate is 25%, multiply that out to see what revenue actually materializes. For product businesses, count your current customers, apply your historical churn rate, project new customer additions based on your marketing spend and conversion rates, then multiply by average customer value.

Top-down forecasting uses market sizing to validate whether your growth assumptions are realistic. If your industry grows 5% annually but you’re projecting 20% growth, you’re betting on taking market share from competitors-that’s a conscious choice you should make with eyes open. Build three scenarios: a most-likely case based on your historical performance adjusted for known changes, an upside case assuming faster customer acquisition or higher retention, and a downside case assuming a major customer leaves or conversion rates drop 20%.

Effective cash flow forecasting is the lifeblood of a business, enabling daily liquidity and resilience to unforeseen shocks. Monthly revenue projections for 12 months should account for seasonality. If 40% of your annual revenue comes in Q4, don’t pretend revenue distributes evenly across months.

List every fixed cost (rent, insurance, software subscriptions, base salaries) that stays the same regardless of revenue. List variable costs that scale with production or sales volume. Identify one-time expenses you know are coming-equipment replacement, facility upgrades, hiring pushes. Build in a contingency line for unexpected costs, typically 5–10% of your operating expense total depending on how stable your business is.

Use industry benchmarks to reality-check yourself. If your industry standard for rent is 8% of revenue and you’re at 12%, you have a conversation to have with your landlord or a decision to make about relocation. Cover fixed, variable, one-time, semi-variable, and hidden costs so you spot cost overruns before they damage cash flow.

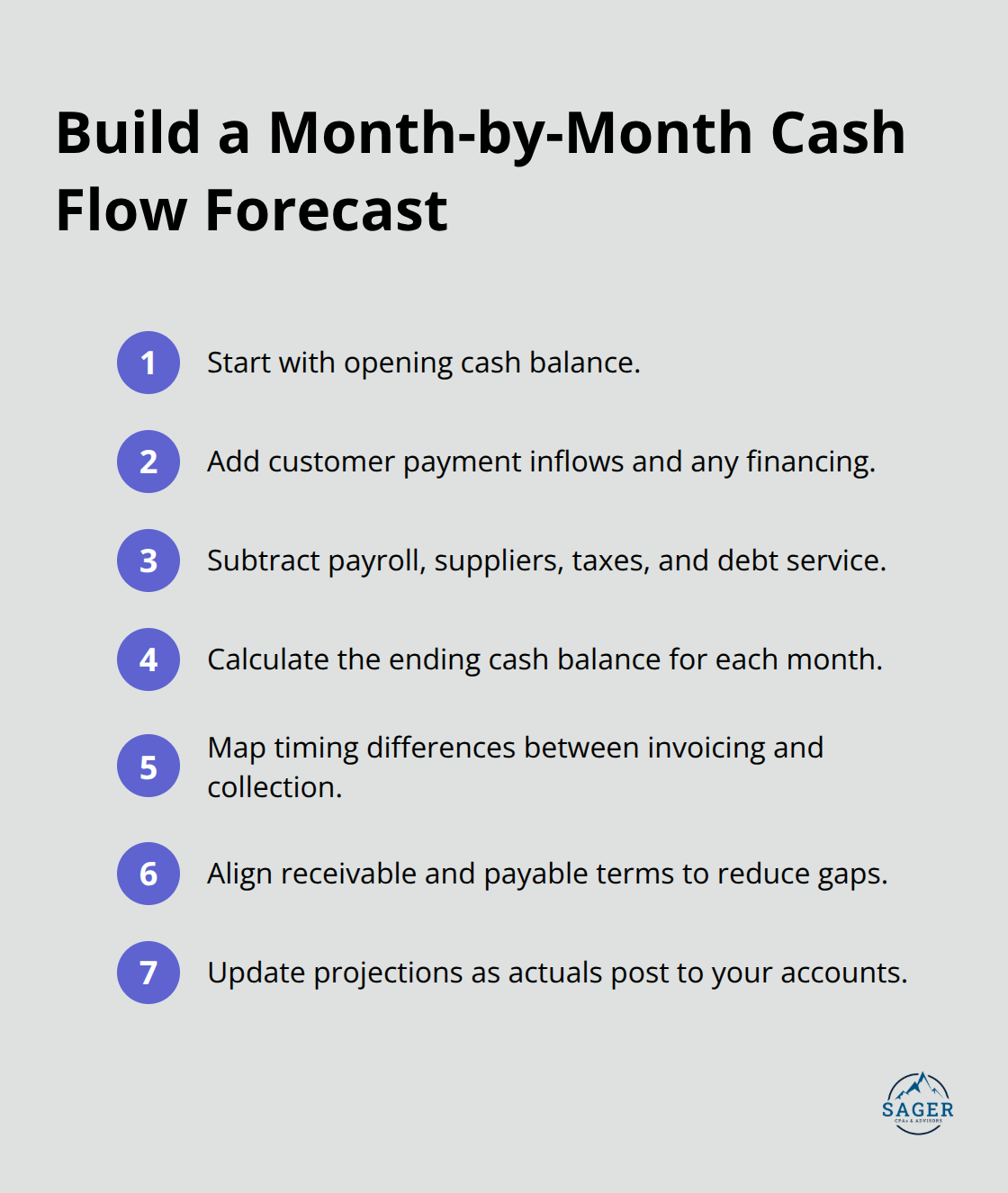

Profitable companies fail because they run out of cash. Your profit and loss statement shows whether you made money, but your cash flow statement shows whether you have money in the bank to pay your team on Friday. Build a month-by-month cash flow projection starting with your opening cash balance, adding cash inflows from customer payments and any financing, subtracting cash outflows for payroll, suppliers, taxes, and debt service, then calculating your ending balance.

The timing matters more than the total. You might invoice $100,000 in month one but not collect it until month two. You might incur $50,000 in payroll expense in month one that doesn’t get paid until the 15th of month two. Map these timing differences explicitly.

If you offer customers 45-day payment terms and you pay suppliers in 30 days, you need enough cash reserves to cover that 15-day gap multiplied by your monthly expense run rate.

Seasonal businesses need extended forecasting of 18 months or more because the peak season determines how much cash you need to build during slow months. A landscaping business generating 70% of annual revenue between April and October needs cash reserves built during winter to survive the lean months and fund spring operations.

Automate your cash flow forecast using accounting software with real-time bank feeds so you’re not working from month-old data. Your forecast updates automatically as actual deposits and expenses hit your accounts. Set calendar reminders to review your forecast monthly against actual results and adjust forward projections based on what you’re actually seeing. When reality diverges from forecast-customers pay slower than expected or you spent more on contractor labor-update your projections immediately rather than hoping the trend reverses.

The next section shows you how to identify the specific financial metrics and KPIs that will tell you whether your plan is actually working.

Most businesses create a financial plan once and then ignore it for 12 months until the next planning cycle. This approach wastes the entire value of planning because business conditions shift constantly. Your best customer might leave in month three, forcing you to cut expenses or accelerate new customer acquisition. A supplier might raise prices 15% in month six, shrinking margins across your product line. A new competitor might enter your market in month eight, pressuring your pricing strategy. When you lock your plan in a drawer and pretend it still reflects reality, you’re not managing your business-you’re managing fiction.

Monthly reviews against actual results take 30 minutes but catch problems while you still have time to fix them. Compare your actual revenue, expenses, and cash balance to what you projected. When reality diverges from forecast, update your forward projections immediately rather than hoping next month corrects the variance. This disciplined monthly habit transforms planning from a static document into an active management tool that actually guides your decisions.

Cash flow mismanagement kills more profitable companies than unprofitability does. You can have a solid gross margin and positive net income on your P&L while your bank account sits empty because of timing gaps between when you pay expenses and when you collect revenue. If you pay your team every two weeks but customers pay you in 60 days, you’re funding their cash flow with yours.

The gap between outflows and inflows determines whether you survive. A business that collects upfront (like a SaaS company with annual subscriptions) faces very different cash constraints than a business that invoices and waits 45 days for payment. Map these timing differences explicitly in your cash flow forecast. Your profit and loss statement shows whether you made money, but your cash flow statement shows whether you have money in the bank to pay your team on Friday.

Many business owners underestimate operating expenses by 20–40% because they overlook semi-variable costs that creep upward as the business grows, hidden costs like professional services and software subscriptions that accumulate over time, and one-time expenses that happen more frequently than expected.

Build your expense forecast by going line-by-line through your actual spending from the past 12 months, not by guessing. If you spent $8,000 monthly on contractor labor last year, don’t project $6,000 because you hope to hire permanent staff. Project $8,000 and then plan the transition carefully. Include a 5–10% contingency reserve in your operating expense budget depending on how volatile your costs are. When you underestimate expenses, your cash flow projections become worthless and you end up short on cash when you thought you’d be fine.

Financial planning transforms strategy from ambition into executable reality. When you connect your business goals to concrete revenue projections, expense budgets, and cash flow timelines, strategy stops being wishful thinking and becomes a roadmap you can actually follow. The companies that outperform their competitors aren’t smarter or luckier-they simply know their numbers and adjust when reality diverges from forecast.

Your first step is straightforward: pull together your last 12 months of financial data and build a baseline understanding of where you stand. Calculate your gross margin, operating expense ratio, and cash conversion cycle. Project your revenue using both bottom-up pipeline analysis and top-down market sizing, then forecast your expenses by reviewing actual spending from the past year rather than making assumptions. Build a month-by-month cash flow projection that accounts for timing gaps between when you pay suppliers and when customers pay you, then commit to reviewing these numbers monthly against actual results and updating your forward projections when conditions shift.

This disciplined approach to business financial planning prevents the cash traps that kill profitable companies, catches problems early enough to fix them, and gives you the confidence to make growth investments without gambling with your business’s survival. We at Sager CPA help you build a personalized financial strategy through expert accounting and tax planning services tailored to your specific situation. Schedule a consultation with Sager CPA to create a customized financial plan that connects your strategy to your cash position and positions your business for sustainable growth.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.