Financial Risk Management Startup: Build Resilience Into Your Growth Plan

Build financial resilience into your startup's growth plan with proven risk management strategies that protect profits and accelerate scaling.

Your tax situation is unique, and a one-size-fits-all approach won’t cut it. At Sager CPA, we build tailored tax strategy plans designed specifically around your income, deductions, and life circumstances.

This guide walks you through how to assess your tax situation, implement smart planning strategies, and sidestep costly mistakes that drain thousands from your bottom line.

The first step toward a smarter tax strategy is understanding exactly what you’re working with. This means mapping every income stream, identifying which expenses actually reduce your taxes, and confirming your filing status matches your circumstances. Most people skip this foundation and jump straight to filing, which costs them thousands in missed opportunities.

Start by listing all income sources. This includes your W-2 wages, freelance earnings, investment gains, rental income, and any other money coming in. The IRS data shows taxpayers overpay by about $1 billion annually due to underutilized credits and deductions. That’s not random-it happens because people don’t fully account for what they earn or what they can deduct.

If you’re self-employed, your income picture becomes even more complex. You need to track business revenue separately from personal income, calculate your net profit after legitimate business expenses, and understand how self-employment tax applies. For rental properties, you must separate rental income from other income streams because it follows different deduction rules. Side hustles count too. If you earned money on the side in 2025, that income is taxable even if you received no 1099 form. Write down the exact amount-guessing leads to penalties.

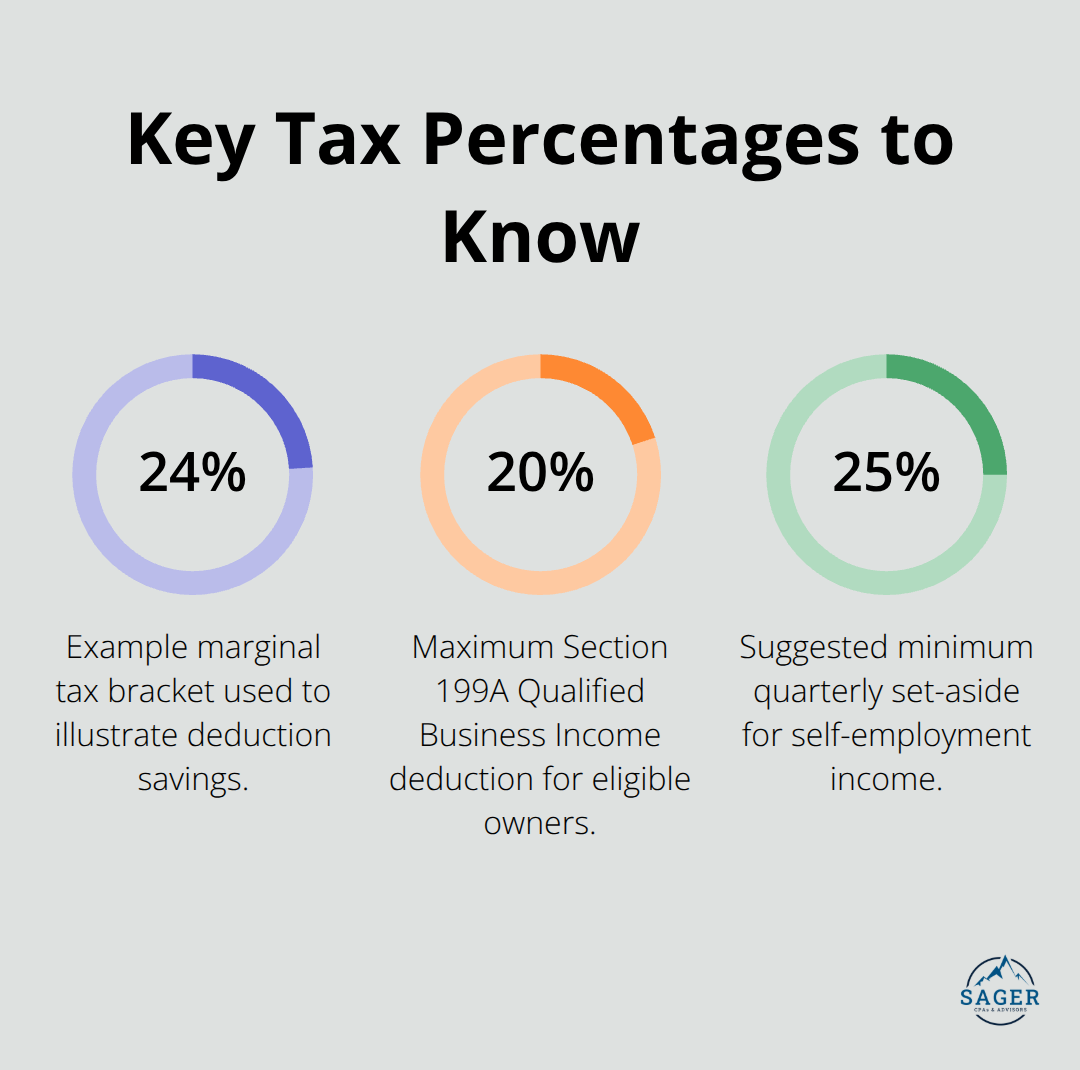

Deductions and credits are not the same thing, and this distinction matters. A deduction reduces your taxable income, while a credit directly reduces the tax you owe. A $1,000 deduction might save you $240 in taxes if you’re in the 24% bracket. A $1,000 credit saves you $1,000 in taxes.

Most people miss deductions because they don’t track them throughout the year. If you’re self-employed, home office expenses, equipment, software subscriptions, and vehicle mileage all count. Track mileage daily-the IRS allows 67 cents per mile in 2025 for business driving. If you have a qualifying home office, you can deduct a portion of rent or mortgage interest, utilities, and internet based on square footage.

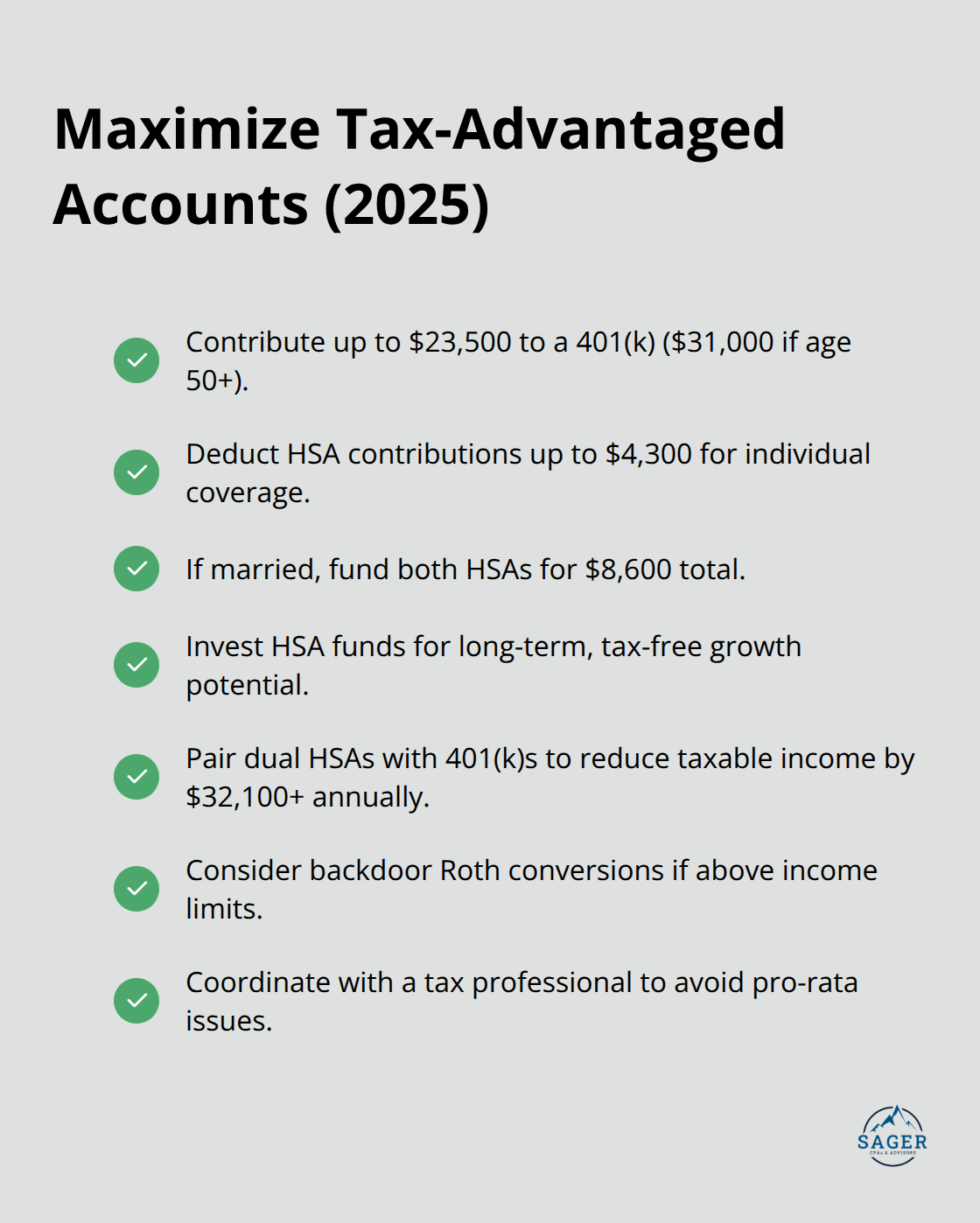

For employees, educator expenses up to $300 are deductible if you paid them out of pocket. Student loan interest deductions reach $2,500 annually if you qualify. Health Savings Accounts offer triple tax advantages-you deduct contributions, growth is tax-free, and qualified medical withdrawals are tax-free. If you have an HSA-eligible health plan, contributing the maximum ($4,300 for individual coverage in 2025) is one of the smartest moves available.

Your filing status determines your tax bracket and which credits you qualify for. Married filing jointly typically offers the lowest tax rate, but not always. Some couples benefit from filing separately if one spouse has significant deductions or credits the other doesn’t. Single filers face steeper rates than married couples on the same income.

Head of household status applies if you’re unmarried, pay more than half household expenses, and have a qualifying dependent-this status offers better rates than single filing. Many people don’t realize their filing status can change year to year based on life events. Getting married, divorced, or having a child shifts your entire tax picture.

Your tax bracket isn’t just about income-it’s about taxable income after deductions. Someone earning $80,000 with $15,000 in deductions sits in a different bracket than someone earning $80,000 with no deductions. This complete financial picture forms the foundation for everything that comes next. Once you understand what you earn, what you can deduct, and how your filing status affects your taxes, you’re ready to implement strategic planning approaches that actually reduce what you owe.

Strategic tax planning means making deliberate choices about when you recognize income and where you place your money. Control when you recognize income by deferring bonuses, self-employment billings, or capital gains until the end of the year to avoid paying taxes in the near term. If you’re self-employed or have variable income, you control timing more than most people realize.

Deferring a bonus from December to January shifts it into the next tax year, potentially keeping you in a lower bracket. If you expect a spike in income this year, accelerate deductible business expenses into the current year to reduce your taxable base. For rental properties, time major repairs or equipment purchases before year-end to capture deductions when you need them most.

The IRS allows 2025 contributions to 401(k) accounts up to $23,500 (or $31,000 if you’re 50 or older), and these contributions directly reduce your taxable income dollar-for-dollar. Maximize retirement and health savings accounts to reduce your taxable income. Contributions are tax-deductible, the money grows tax-free, and withdrawals for qualified medical expenses carry zero tax.

The 2025 limit sits at $4,300 for individual coverage, and you can invest HSA funds rather than letting them sit idle in a savings account. If you’re married, max out both spouses’ HSAs ($8,600 total) alongside a 401(k) strategy to reduce taxable income by $32,100 or more annually. For high-income earners, backdoor Roth conversions allow you to contribute to a Roth IRA even when your income exceeds the standard limits.

This requires careful execution and coordination with your tax professional to avoid pro-rata complications, but the long-term benefit of tax-free growth justifies the complexity.

Business structure matters more than most owners acknowledge. A sole proprietor pays self-employment tax on all net profit at 15.3%, which includes both the employee and employer portions of Social Security and Medicare tax. An S-corporation election allows you to pay yourself a reasonable salary and take the remainder as a distribution, avoiding self-employment tax on the distribution portion.

For a business netting $100,000, this structure can save $3,000 to $5,000 annually depending on how you split salary versus distributions. However, the IRS scrutinizes S-corporation owners who claim unreasonably low salaries, so you must document that your W-2 wage reflects fair market value for your role. If you own rental properties, cost-segregation studies accelerate depreciation deductions by breaking down property components into shorter useful lives. A $500,000 rental property might generate $15,000 to $25,000 in additional first-year deductions through this strategy alone.

The Section 199A Qualified Business Income deduction allows eligible business owners to deduct up to 20% of qualified business income, but calculating this correctly requires understanding your specific entity type and income level. Many business owners leave this deduction on the table because they don’t track it during the year or fail to understand their eligibility. These planning strategies work best when they align with your actual business structure and goals rather than forcing you into a generic approach. The next section covers the costly mistakes that derail even well-intentioned tax plans and how to sidestep them.

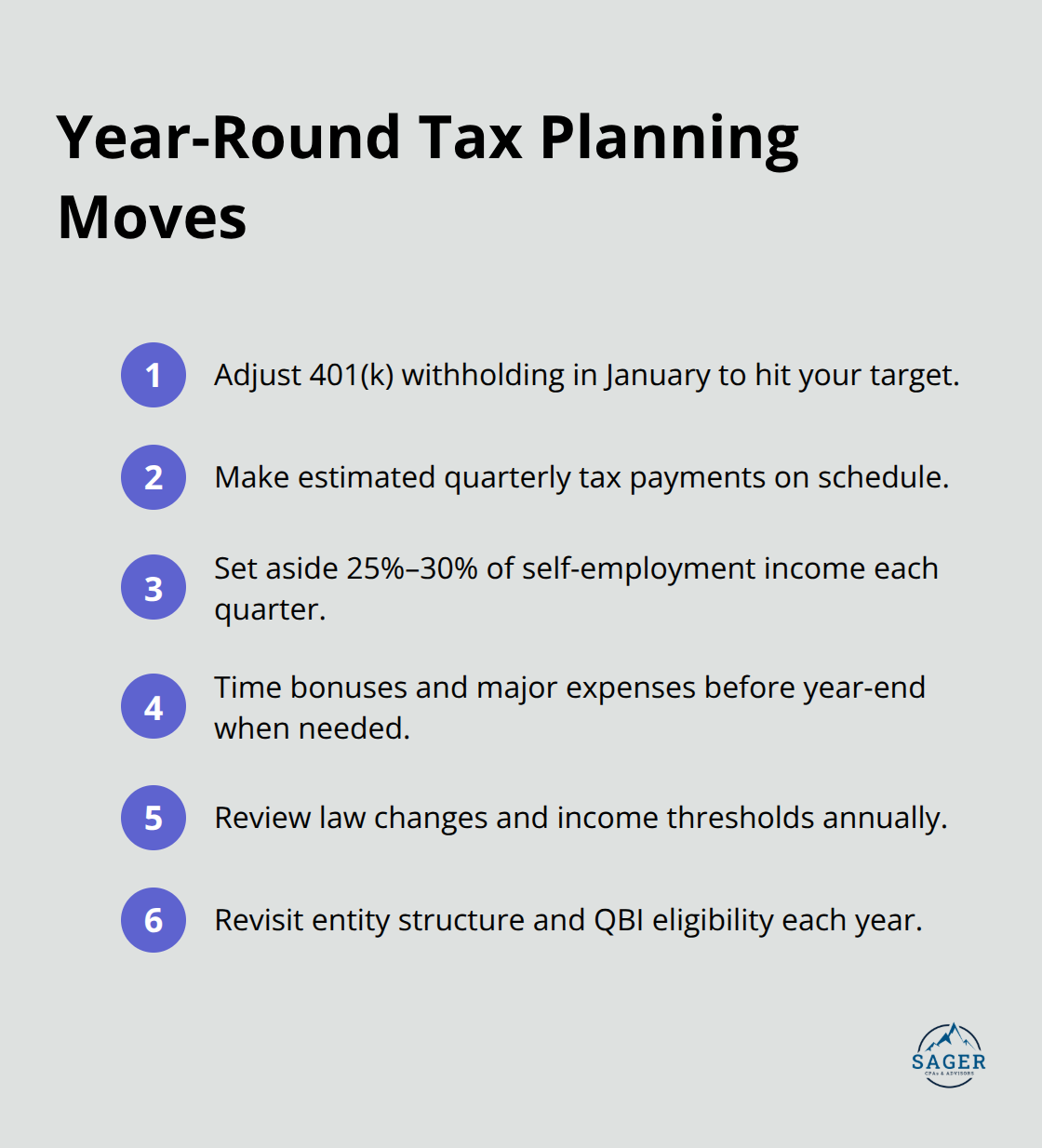

Most people treat tax planning like an annual chore instead of an ongoing discipline, and this mistake alone costs them thousands. You file your taxes in March or April, receive a refund or owe money, and then forget about taxes until next year rolls around. This approach leaves money on the table every single month. Tax planning works only when you make decisions throughout the year, not after the fact.

If you defer a bonus in December hoping to lower your bracket, that decision needs to happen in October when you still control the timing. If you want to max out your 401(k) to reduce taxable income, you need to adjust your payroll withholding in January, not realize in November that you’re short. The IRS allows you to make estimated quarterly tax payments if you’re self-employed or have variable income, which means you can spread your tax burden across four payments instead of one lump sum in April.

Most self-employed workers skip quarterly payments and face penalties for underpayment. Setting aside 25% to 30% of self-employment income each quarter prevents surprises and gives you cash flow visibility. Tax law changes happen constantly, and recent years brought shifts in depreciation rules, retirement contribution limits, and business deduction thresholds. If you’re still using last year’s tax strategy without reviewing current rules, you’re operating with outdated information.

The Section 199A deduction for business owners phases out at higher income levels, and the phase-out thresholds change annually. A strategy that worked perfectly in one year might be partially unavailable in the next if your income crossed a threshold.

The second major mistake is overlooking deductions and credits that directly apply to your situation. Taxpayers overpay by about $1 billion annually due to underutilized credits and deductions according to IRS data. That’s not a guess, and it’s not rare. It happens to people across all income levels because they don’t track potential deductions throughout the year or don’t understand which ones apply to them.

Education credits like the American Opportunity Tax Credit provide up to $2,500 per student annually, but only if you paid qualified education expenses in the tax year. If you paid tuition in December 2024 but filed your 2024 return without claiming it, you missed that credit entirely. Catch-up contributions for retirement accounts represent another commonly overlooked opportunity. If you’re 50 or older, you can contribute an additional $7,500 to your 401(k) and $1,000 to your IRA beyond the standard limits. Many people hit the standard limit and stop, unaware they can contribute more.

For rental property owners, depreciation recapture creates tax liability when you sell, but accelerating depreciation through cost-segregation studies in the years you own the property reduces your current tax burden and is perfectly legal. The mistake isn’t claiming too many deductions-it’s claiming too few.

Ignoring tax law changes is expensive. Tax rate reductions and changes to the standard deduction, child credit, and personal exemptions represent provisions that require ongoing attention. If Congress doesn’t extend expiring provisions, tax brackets and deductions will shift significantly. Planning now for potential changes means adjusting your strategy proactively instead of scrambling when your taxes spike.

A tax professional who monitors legislative changes and communicates them to you prevents these costly oversights. Working with someone who stays informed about evolving tax rules protects your bottom line and keeps your strategy aligned with current law.

A generic tax return filed once a year leaves thousands on the table. Tailored tax strategy plans work only when they fit your specific income, business structure, deductions, and life circumstances-not when you force yourself into a template designed for someone else. The real value emerges from the year-round discipline these plans create, allowing you to make intentional decisions throughout the year about income timing, account funding, and business structure rather than scrambling in March to find missed deductions.

We at Sager CPA build customized solutions by starting with your complete financial picture. We assess your income sources, identify deductions and credits that apply specifically to you, and align your tax strategy with your actual goals (not generic best practices). We monitor tax law changes so you don’t have to, adjust your plan as your circumstances shift, and communicate regularly so you understand exactly how your strategy reduces what you owe.

The difference between filing taxes and planning taxes is substantial-one costs you money, the other saves it. Schedule a consultation with Sager CPA to discuss your specific situation and build a personalized financial strategy that works for your circumstances.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.