How to Create a Good Marketing Strategy for Small Business

Build a good marketing strategy for small business with actionable steps to boost growth, reach customers, and increase sales today.

Tax planning strategies can make a significant difference in your financial future. By implementing effective approaches, you can legally minimize your tax burden and maximize your wealth.

At Sager CPA, we’ve seen firsthand how proactive tax planning can lead to substantial savings for both individuals and businesses. This blog post will guide you through essential strategies and highlight the importance of professional expertise in navigating the complex world of taxes.

Tax planning is a strategic approach to manage finances with the aim to minimize tax liability within legal bounds. It doesn’t involve tax evasion but focuses on making intelligent decisions that lead to significant savings over time.

A proactive stance on tax planning yields substantial benefits. A Government Accountability Office study revealed that the applicable standard deduction for taxpayers who do not itemize deductions is $6,000. This highlights the potential impact of thoughtful tax planning.

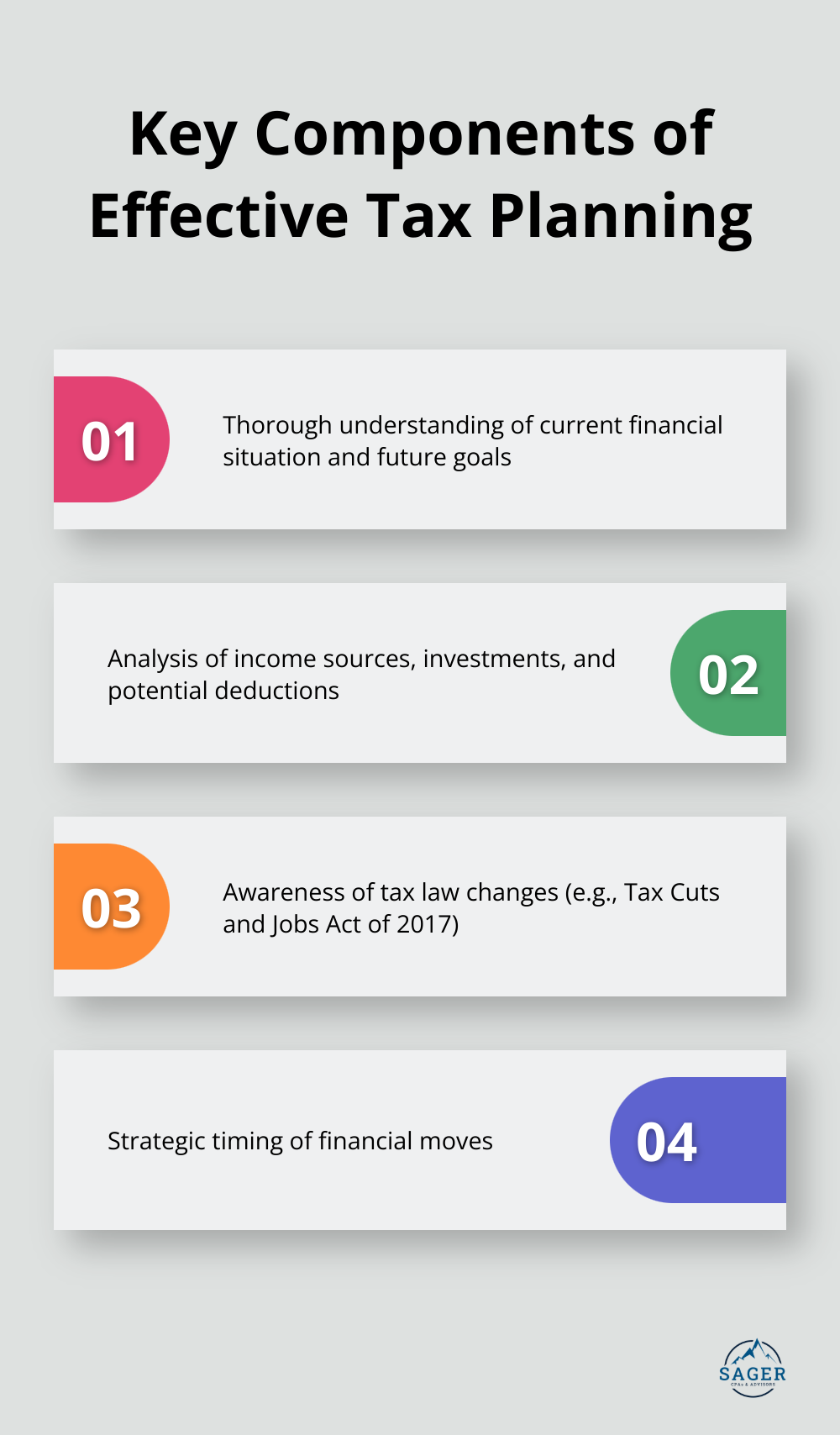

Effective tax planning involves several crucial elements:

Timing plays a critical role in tax planning. Strategic moves at the right time can maximize tax benefits. For instance, the acceleration of deductions into the current year or deferral of income to the next year can sometimes lower overall tax liability.

Every individual and business has unique financial circumstances, which renders a one-size-fits-all approach ineffective. A tax plan should be tailored to specific situations, considering factors such as income level, business structure, investment portfolio, and long-term financial objectives.

Small business owners might focus on strategies like maximizing business expense deductions or selecting the most tax-efficient business structure. Individuals nearing retirement might prioritize optimizing withdrawals from retirement accounts to minimize tax burden in their later years.

As we move forward, we’ll explore essential tax planning strategies for both individuals and businesses. These strategies will provide a foundation for creating a comprehensive tax plan that aligns with your financial goals and circumstances.

Tax planning creates a comprehensive strategy that aligns with your financial goals. It goes beyond reducing your current tax bill to optimize your overall financial position.

Income splitting distributes income among family members or over time to lower the overall tax burden. Business owners might employ their spouse or children, which shifts some income to lower tax brackets. The IRS reports that the average effective tax rate for all taxpayers was 13.3% in 2018, highlighting the potential impact of strategic income distribution.

Income deferral can also reduce tax liability. If you expect a year-end bonus, ask your employer to delay payment until January. This pushes the income into the next tax year, potentially keeping you in a lower tax bracket for the current year.

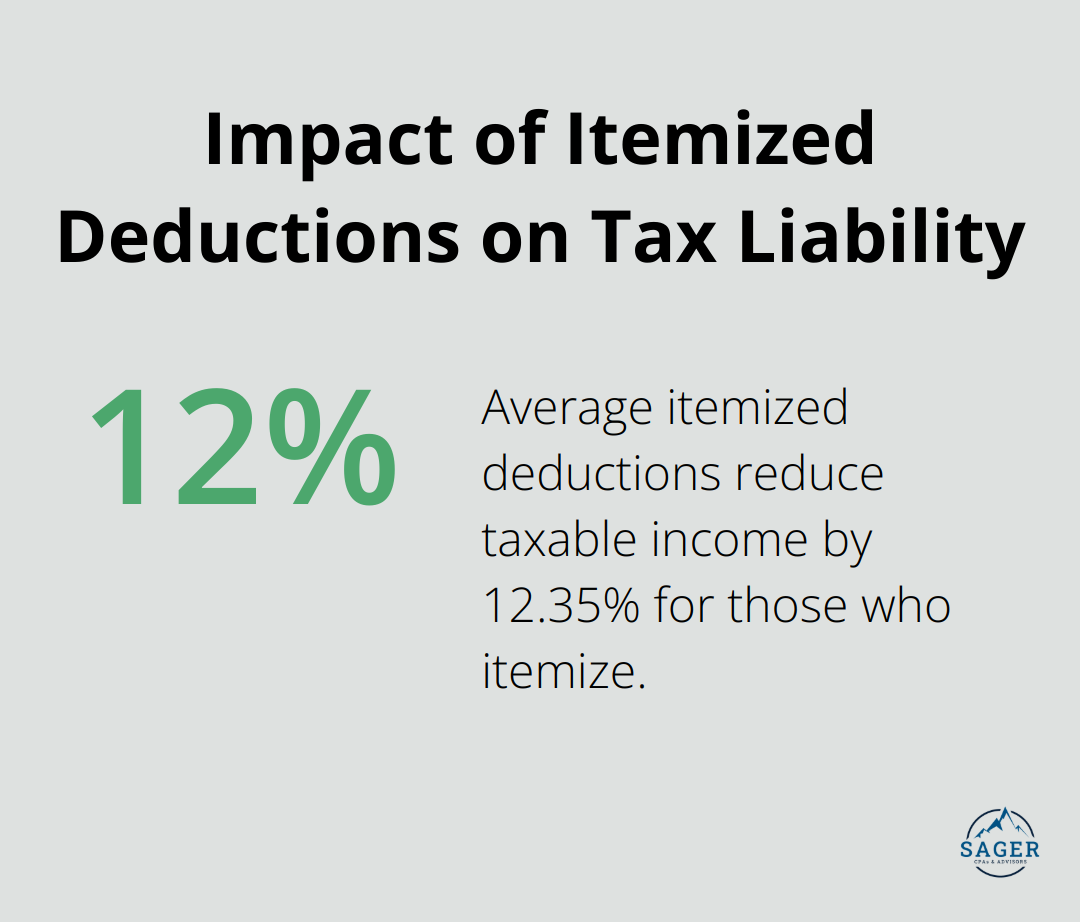

Understanding and leveraging available deductions and credits reduces your tax burden. In 2018, taxpayers claimed an average of $12,352 in itemized deductions (according to IRS data). This underscores the importance of tracking expenses and understanding which deductions apply to your situation.

For businesses, Section 179 of the Internal Revenue Code allows business taxpayers to deduct the cost of certain property as an expense when the property is first placed in service.

Retirement accounts offer excellent tax advantages. Traditional 401(k) contributions reduce your taxable income for the year, while Roth IRA contributions grow tax-free. The IRS limits for 2021 allow you to contribute up to $19,500 to a 401(k), or $26,000 if you’re 50 or older.

Self-employed individuals can use a SEP IRA, which allows contributions of up to 25% of net earnings from self-employment (up to $58,000 for 2021). This results in substantial tax savings while building your retirement nest egg.

The right business structure significantly impacts your tax liability. The Tax Cuts and Jobs Act of 2017 reduced the corporate tax rate to a flat 21%, making C corporations more attractive for some businesses. However, pass-through entities like S corporations and LLCs may still benefit others, especially with the qualified business income deduction allowing up to a 20% deduction on pass-through income.

Implementing these strategies requires careful planning and expertise. A qualified tax professional ensures compliance and maximizes your tax savings. The next section will explore how working with a professional tax advisor can enhance your tax planning efforts and lead to better financial outcomes.

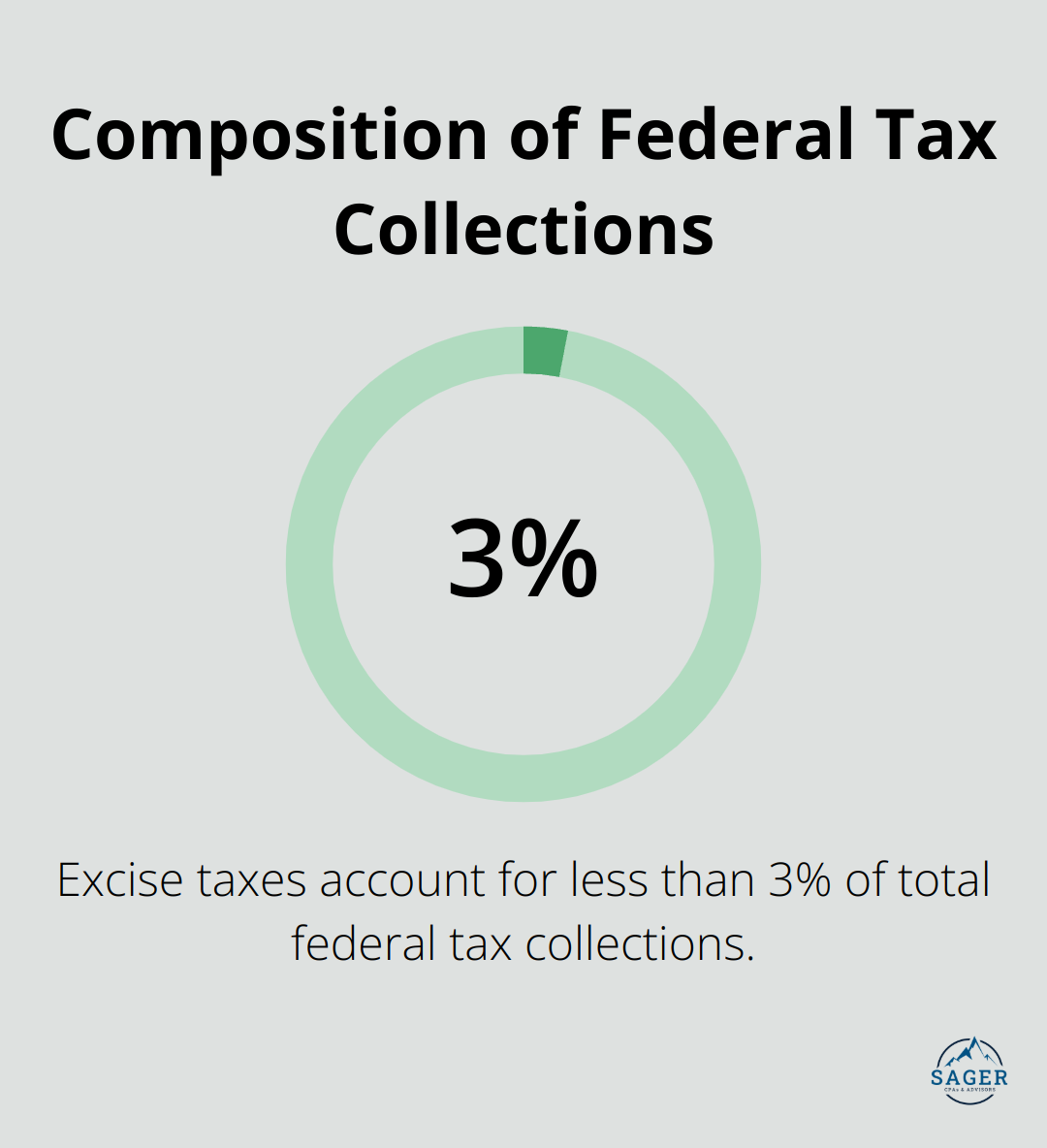

CPAs maintain up-to-date knowledge of the latest tax laws and regulations. Excise taxes account for less than 3 percent of total federal tax collections. A CPA navigates this complexity to ensure you don’t miss potential savings or unintentionally violate tax laws.

Every financial situation requires a unique approach. A CPA analyzes your specific circumstances to develop tailored strategies. For small business owners, a CPA might recommend a SEP IRA, which allows contributions limited by the lesser of 25% of your business net income or the nominal max amount ($61,000 for 2022).

CPAs don’t just react to your current financial situation; they plan for the future. This includes forecasting potential tax liabilities and developing strategies to mitigate risks. The Government Accountability Office found that 77% of taxpayers could benefit from year-round tax planning, yet only a small percentage engage in this practice.

Tax planning requires regular adjustments as your financial situation evolves and tax laws change. A CPA provides continuous support to keep your tax strategy optimized. This attention can lead to substantial savings over time.

A CPA starts with a comprehensive analysis of your financial situation, including income sources, investments, and potential deductions. Based on this analysis, they develop a customized tax strategy that aligns with your short-term and long-term financial goals.

The process includes regular check-ins to review and adjust your tax plan. CPAs monitor changes in tax laws and your financial situation, making real-time adjustments to maximize your tax savings. For example, when the Tax Cuts and Jobs Act was implemented in 2017, CPAs immediately analyzed its impact on clients and adjusted strategies accordingly.

CPAs also provide year-round support, answering questions and offering guidance as financial decisions arise. This ongoing partnership ensures that tax considerations factor into all your major financial decisions (from business investments to retirement planning).

Tax planning strategies play a vital role in optimizing financial positions for individuals and businesses. These strategies include income splitting, maximizing deductions, and strategic use of retirement accounts. The dynamic nature of tax laws necessitates regular reviews and adjustments to ensure the most beneficial approaches are utilized.

Professional expertise becomes invaluable when navigating the complexities of tax planning. Sager CPA specializes in developing tailored tax planning strategies for diverse clients. Our team stays current with the latest tax laws and regulations to provide effective solutions.

We encourage you to take the next step in optimizing your financial future. Schedule a consultation with Sager CPA today to create a personalized tax planning strategy (aligned with your goals). Our proactive approach and customized solutions will help you make informed financial decisions and achieve long-term stability and growth.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.