Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Retirement brings a new set of financial challenges, especially when it comes to taxes. At Sager CPA, we understand that optimizing tax strategies for retirees is crucial for maintaining financial stability during your golden years.

This blog post will guide you through effective ways to manage your retirement income, implement tax-efficient withdrawal strategies, and maximize deductions and credits available to retirees. By following these practical tips, you’ll be better equipped to minimize your tax burden and make the most of your hard-earned retirement savings.

Retirement income originates from various sources, each with unique tax implications. Effective tax planning in retirement requires a clear understanding of these income streams.

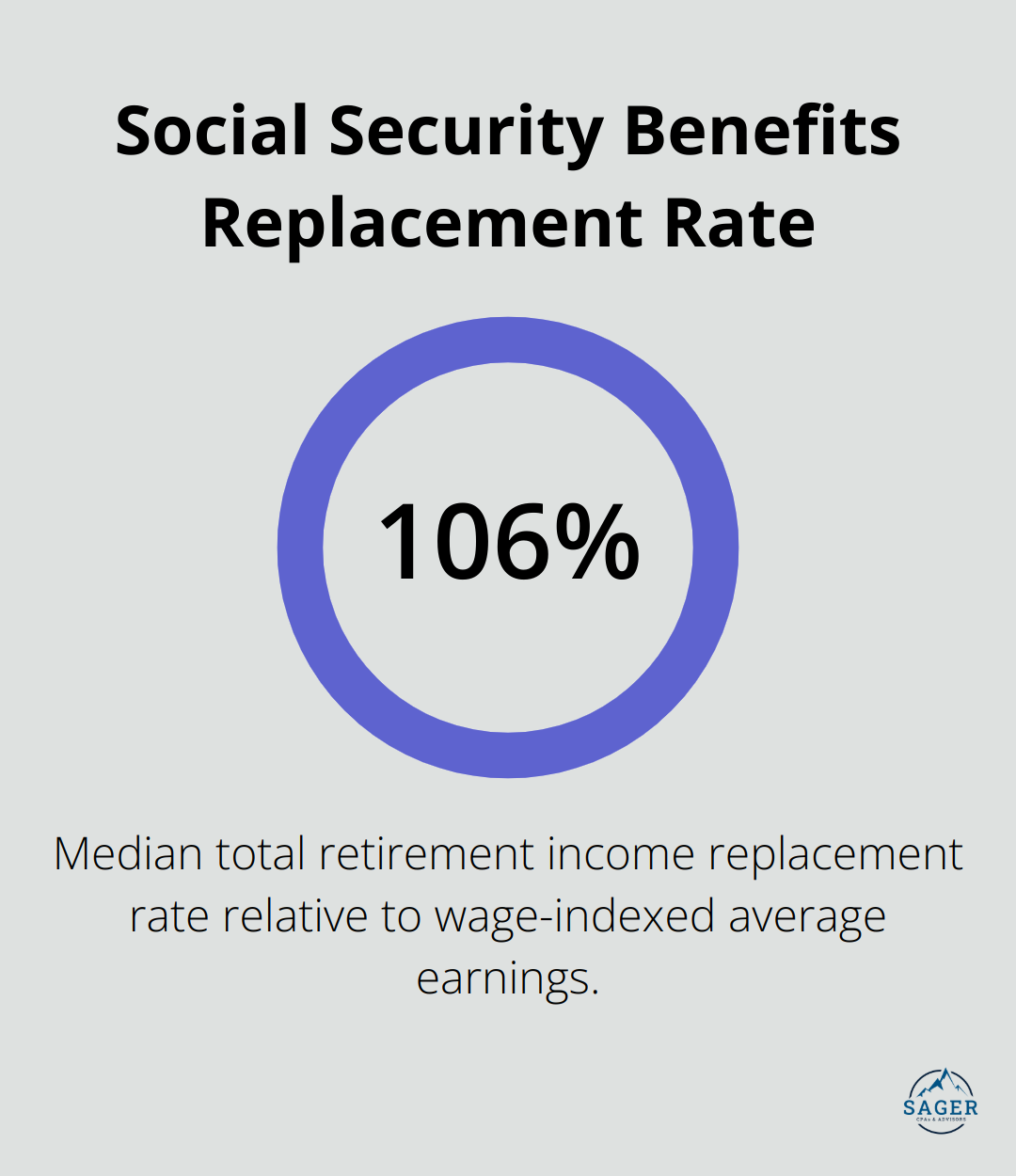

Social Security benefits constitute a substantial portion of retirement income for many Americans. The Social Security Administration reports that the median total retirement income replacement rate is 106 percent relative to wage-indexed average earnings. However, up to 85% of your Social Security benefits may face taxation, depending on your total income. To reduce taxes, you can explore strategies such as timing your benefit claims or balancing withdrawals from other income sources.

Traditional IRA and 401(k) distributions incur taxation as ordinary income. Required Minimum Distributions (RMDs) for those reaching age 73 in 2024 must be taken by April 1, 2025, with the second RMD due by December 31, 2025. Failure to take RMDs results in a substantial 25% penalty on the amount not withdrawn. Conversely, qualified distributions from Roth IRAs offer tax-free withdrawals, providing valuable flexibility in managing your taxable income during retirement.

If you receive a pension, most pension income is subject to taxation. The specific tax treatment depends on the distribution method and timing. Lump-sum distributions might elevate you to a higher tax bracket, while periodic payments distribute the tax burden over time. Some pension plans offer a choice between these options, necessitating careful consideration of the tax implications.

Investment income (including dividends, interest, and capital gains) can significantly impact your retirement tax situation. Long-term capital gains benefit from preferential tax rates, while short-term gains face taxation as ordinary income. In 2024, married couples filing jointly with taxable income up to $89,250 can take advantage of a 0% long-term capital gains rate. Strategic harvesting of capital gains and losses can help you manage your tax liability effectively.

To optimize your retirement income strategy, you should consider the tax implications of each income source. Balancing withdrawals from taxable and tax-advantaged accounts can help you maintain a lower overall tax rate. Additionally, you might explore options such as Roth conversions or charitable giving strategies to further reduce your tax burden.

As we move forward, we’ll examine specific tax-efficient withdrawal strategies to help you make the most of your retirement savings while minimizing your tax obligations.

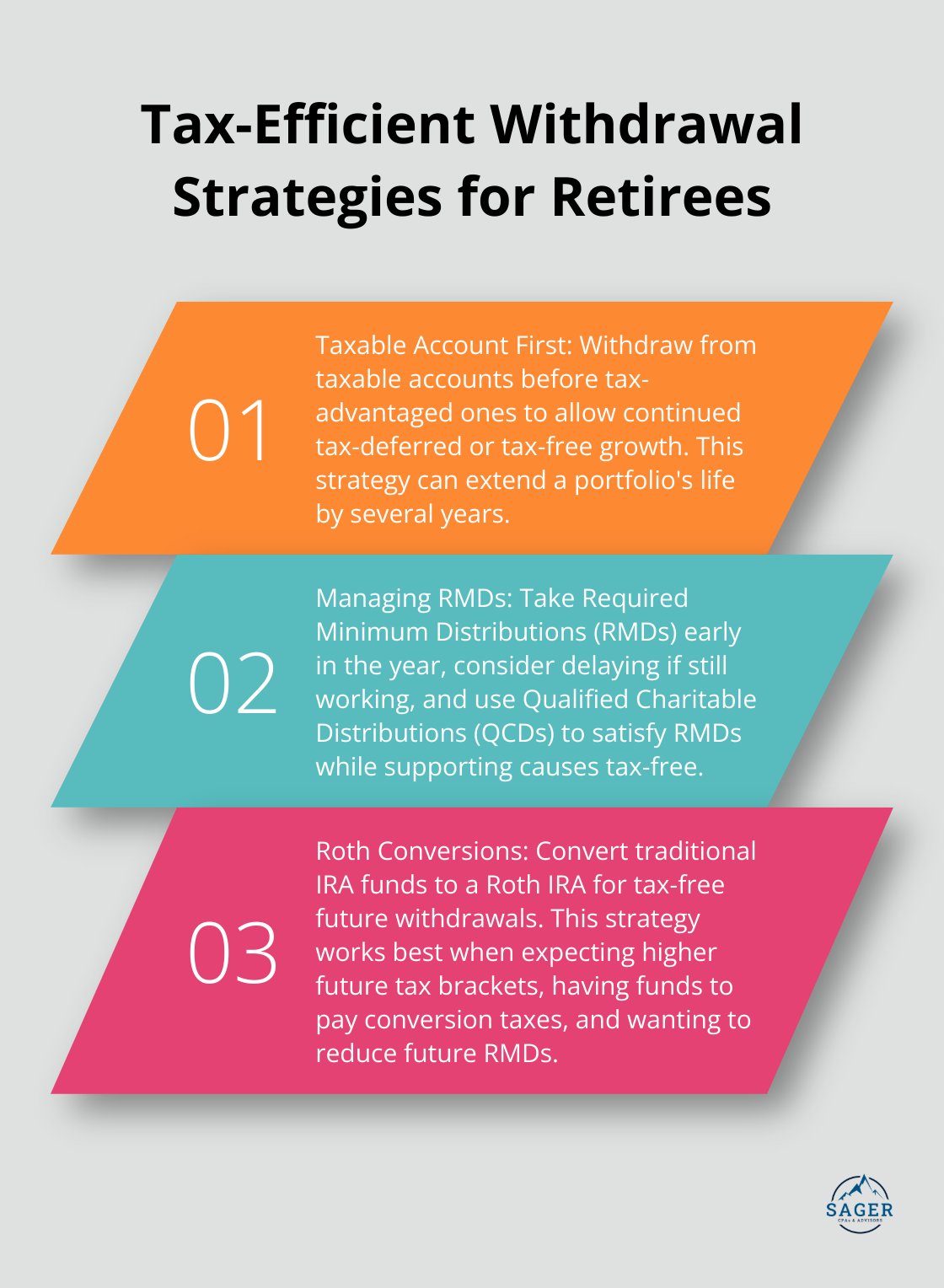

Most retirees benefit from withdrawing from taxable accounts first. This strategy allows tax-advantaged accounts to grow tax-deferred or tax-free. A T. Rowe Price study indicates this approach can extend a portfolio’s life by several years compared to prioritizing tax-deferred account withdrawals.

However, this strategy isn’t universal. Retirees with significant unrealized gains in taxable accounts should consider a blended approach to avoid higher tax brackets.

Individuals 73 and older must take Required Minimum Distributions (RMDs) from certain retirement plans, including traditional IRAs, SEP IRAs, SIMPLE IRAs and 401(k) plans. The IRS calculates these based on account balance and life expectancy. Failure to take RMDs results in a 25% penalty on the amount not withdrawn.

To manage RMDs effectively:

Roth conversions can serve as a powerful tax strategy tool. Converting traditional IRA funds to a Roth IRA incurs taxes now but provides tax-free withdrawals in the future, potentially allowing you to better manage your tax brackets.

This strategy works best when:

Minimizing taxes often involves careful income management to stay within lower tax brackets. This might include:

For example, in 2024, married couples filing jointly can have up to $89,450 in taxable income and remain within the 12% bracket (a fact worth noting for strategic planning).

Tax laws change frequently and can be complex. While these strategies provide a starting point, personalized advice proves invaluable. The next section will explore how retirees can maximize deductions and credits to further reduce their tax burden.

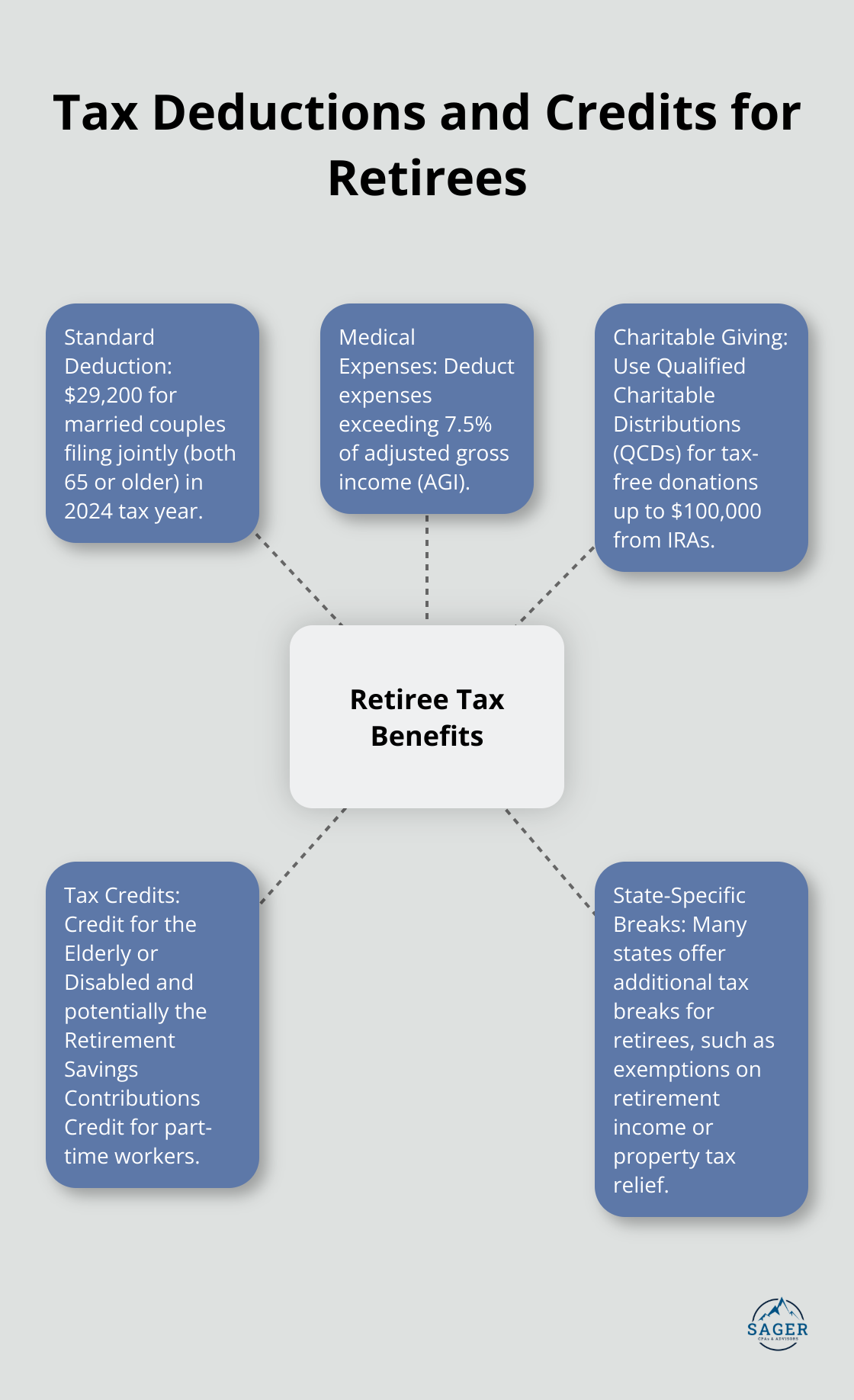

For the 2024 tax year, married couples filing jointly (both 65 or older) receive a standard deduction of $29,200. This increased amount often eliminates the need for itemization. However, if your itemized deductions exceed this threshold, you should explore this option.

Itemized deductions include state and local taxes (capped at $10,000), mortgage interest, and charitable contributions. Maintain detailed records of these expenses throughout the year to make an informed decision when filing your taxes.

Medical expenses can significantly burden retirees. You can deduct medical expenses that exceed 7.5% of your adjusted gross income (AGI). This includes costs for prescription medications, medical equipment, and long-term care insurance premiums.

To optimize this deduction, consider concentrating medical expenses into a single year when possible. For example, schedule elective procedures in the same tax year to push you over the 7.5% threshold, allowing for a larger deduction.

Charitable donations provide both personal satisfaction and tax benefits. For those 70½ or older, Qualified Charitable Distributions (QCDs) offer a particularly advantageous option. You can donate up to $100,000 directly from your IRA to qualified charities without including the distribution in your taxable income.

Another effective strategy involves donating appreciated securities. This approach allows you to avoid capital gains tax on the appreciation while still claiming the full market value as a charitable deduction.

For non-itemizers, consider concentrating multiple years of charitable giving into a single year to surpass the standard deduction threshold. Donor-advised funds serve as an excellent tool for this strategy, allowing you to claim the deduction in the year of contribution while distributing the funds to charities over time.

Retirees should not overlook available tax credits. The Credit for the Elderly or Disabled can reduce your tax bill if you meet specific age or disability requirements. This credit is available for taxpayers aged 65 or older, or those retired on permanent and total disability who received taxable disability income for the tax year.

Additionally, the Retirement Savings Contributions Credit (Saver’s Credit) rewards low- to moderate-income taxpayers for contributing to retirement accounts. While many retirees may not qualify due to income limits, those still working part-time should consider this option.

Many states offer additional tax breaks for retirees. These can include exemptions on retirement income, property tax relief, or special deductions for seniors. Research your state’s specific offerings or consult with a local tax professional to take full advantage of these opportunities.

Effective tax strategies for retirees play a vital role in preserving financial stability during retirement. Your unique financial situation requires a personalized approach to tax planning, as strategies that work for others may not be optimal for you. A proactive stance on tax optimization can lead to substantial savings over time and provide greater financial security in your retirement years.

Regular reviews and adjustments of your tax strategies become necessary as tax laws evolve and your financial circumstances change. We at Sager CPA offer expert financial management and tax planning services tailored to your specific needs. Our team can help you navigate complex tax laws, identify opportunities for tax savings, and develop a comprehensive plan to minimize your tax liabilities throughout retirement.

Professional guidance proves invaluable when optimizing your retirement tax strategy. We can ensure you take advantage of all available deductions, credits, and strategies (which can change frequently). With careful planning and expert support, you can enjoy a more financially stable and rewarding retirement.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.