Tax Optimization for Businesses: Proactive Planning for Profits

Reduce your tax burden with strategic planning. Learn tax optimization strategies for businesses to keep more profits and grow faster.

Investment planning is complicated by tax concerns, making it a challenging task for many investors. At Sager CPA, we understand the intricate relationship between taxes and investment strategies.

This blog post explores how tax considerations shape investment decisions and offers insights into tax-efficient planning. We’ll cover key topics like tax-advantaged accounts, capital gains, and the impact of tax brackets on your investment choices.

Understanding capital gains taxation is essential for effective investment planning. Long-term capital gains (from assets held over a year) receive preferential tax treatment compared to short-term gains. In 2024, individuals in the 10% and 12% tax brackets pay 0% on long-term capital gains, while higher brackets face 15% or 20% rates (still lower than ordinary income tax rates).

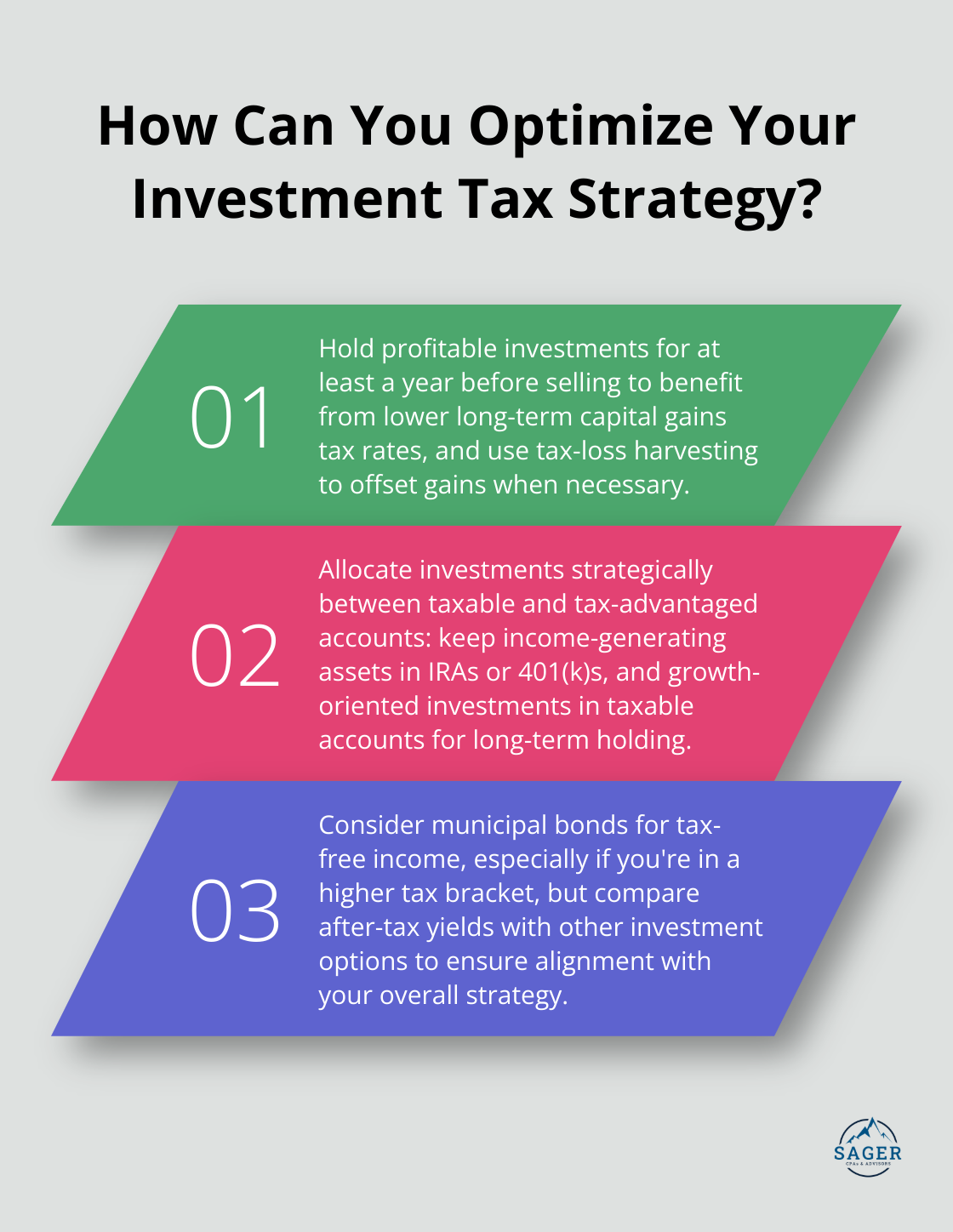

To capitalize on this, investors should consider holding profitable investments for at least a year before selling. If earlier sales are necessary, look for opportunities to offset gains with losses from other investments through tax-loss harvesting.

IRAs and 401(k)s serve as powerful instruments for tax-efficient investing. Traditional IRAs and 401(k)s offer immediate tax deductions on contributions and tax-deferred growth. For 2024, contribution limits are set at $7,000 for IRAs and $23,500 for 401(k)s (with additional catch-up contributions available for those 50 and older).

Roth versions of these accounts don’t provide upfront tax breaks but allow tax-free withdrawals in retirement. This option can benefit those who anticipate being in a higher tax bracket in the future.

Strategic allocation of investments between taxable and tax-advantaged accounts can optimize tax efficiency. Hold investments generating regular taxable income (e.g., bonds, dividend-paying stocks) in tax-advantaged accounts. Keep growth-oriented investments planned for long-term holding in taxable accounts to leverage lower capital gains rates.

Municipal bonds offer an excellent choice for tax-conscious investors, particularly those in higher tax brackets. Many investors turn to municipal bonds to add diversification to their portfolio, provide a source of income, and minimize state and federal tax liability.

For example, a municipal bond yielding 3% would equate to a taxable bond yielding about 4.6% before taxes for an investor in the 35% federal tax bracket. However, it’s crucial to compare after-tax yields of municipal bonds with other investment options to ensure they align with your overall strategy.

While municipal bonds can provide tax advantages, they may offer lower yields compared to corporate bonds. Always consider your comprehensive investment strategy and risk tolerance when incorporating them into your portfolio.

Tax efficiency represents just one aspect of investment planning. A holistic approach that aligns with your overall financial goals while optimizing your tax situation is key. The next section will explore how your tax bracket can influence your investment decisions, helping you make more informed choices for your financial future.

Your tax bracket significantly influences your investment strategy. With new tax brackets in 2024, some taxpayers may find that their tax bill is lower than expected. If you currently occupy a higher bracket but anticipate a lower one in retirement, you should consider maximizing contributions to traditional IRAs or 401(k)s. This approach allows you to deduct contributions now and pay taxes on withdrawals later at potentially lower rates.

Alternatively, if you expect to be in a higher tax bracket in the future, Roth accounts become more attractive. While you won’t receive an immediate tax break, your withdrawals in retirement will be tax-free. This can prove particularly beneficial if tax rates increase or your income grows substantially.

Your tax bracket should guide when you realize investment gains or losses. If you’re near the top of your current bracket, consider deferring income to the next tax year to avoid moving into a higher bracket. This might involve postponing the sale of appreciated assets or delaying year-end bonuses (if possible).

Conversely, if you find yourself in a lower bracket than usual, it might be an opportune time to realize capital gains. The 0% long-term capital gains rate applies to individuals in the 10% and 12% tax brackets, presenting a unique opportunity for tax-free profit taking.

For deductions, tax-loss harvesting might be a strategy to consider for 2024. You might be able to offset taxable income by selling investments that have lost value.

Your tax bracket should inform how you balance growth and income investments. Higher-bracket investors might prefer growth-oriented stocks and municipal bonds to minimize taxable income. Growth stocks that don’t pay dividends can be particularly tax-efficient as you control when to realize gains.

For those in lower tax brackets, dividend-paying stocks might appeal more. Qualified dividends are taxed at preferential rates, potentially as low as 0% for those in the lowest brackets. However, keep in mind that dividends from REITs are typically taxed as ordinary income, which could push you into a higher bracket if not managed carefully.

ETFs often offer tax advantages over mutual funds due to their structure, which typically results in fewer capital gains distributions. This can benefit high-bracket investors looking to minimize taxable events.

Tax laws change frequently, and these changes can have a significant impact on your investment strategy. Try to stay informed about potential tax law changes and adjust your investment approach accordingly. For example, if tax rates are expected to increase in the future, you might consider accelerating income into the current year or deferring deductions to future years when they might be more valuable.

As we move forward, it’s essential to consider how different investment vehicles can impact your tax situation. Let’s explore the tax implications of various investment options to help you make more informed decisions about your portfolio composition.

Stocks and mutual funds can offer tax efficiency, but they require careful management. When you sell stocks at a profit, you’ll owe capital gains tax. The rate depends on your holding period. For 2024, if you’re in the 22% tax bracket or below, you’ll pay 0% on long-term capital gains. Higher earners face 15% or 20% rates.

Mutual funds can be less tax-efficient due to capital gains distributions. Even if you don’t sell your shares, you might receive taxable distributions when the fund manager sells securities within the fund. In 2023, U.S. equity funds paid out an estimated $208 billion in capital gains distributions (according to Morningstar).

To minimize tax impact, consider holding individual stocks long-term and choose tax-efficient mutual funds with low turnover rates.

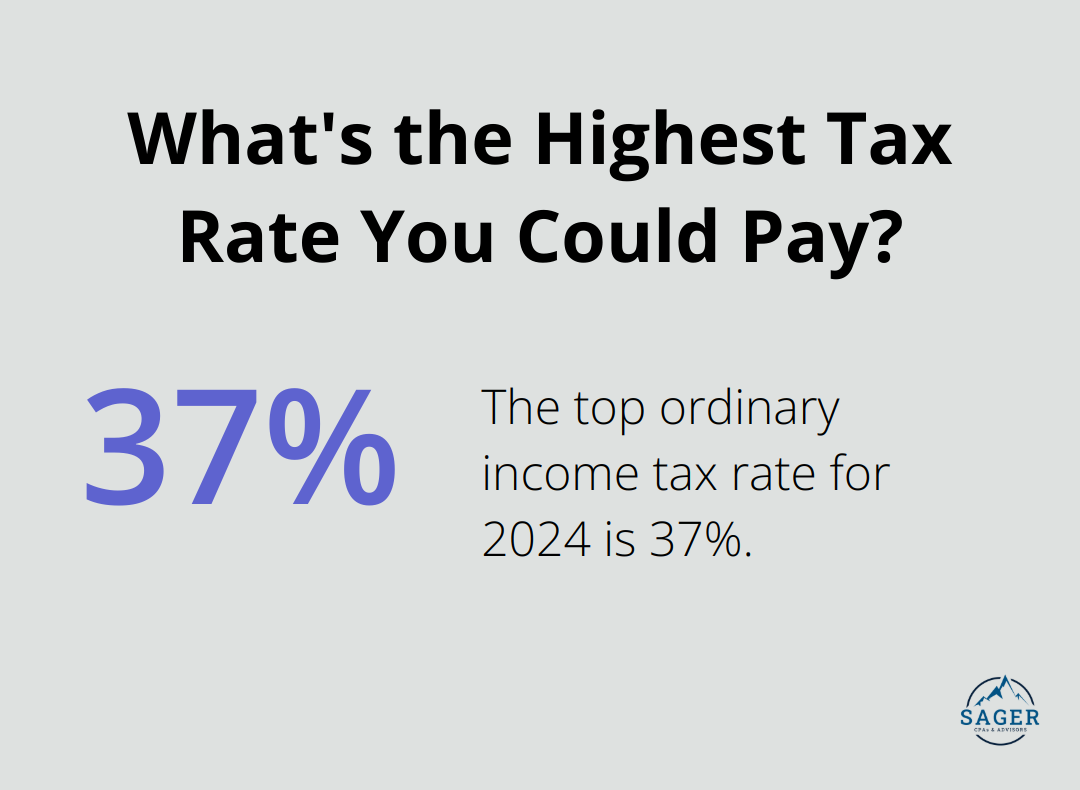

Real Estate Investment Trusts (REITs) offer attractive income potential but come with unique tax considerations. REITs typically don’t pay corporate income taxes because their earnings have been passed along to investors as dividend payments. Most REIT dividends are taxed as ordinary income, which can push you into a higher tax bracket. For 2024, the top ordinary income tax rate is 37%.

However, a portion of REIT dividends may qualify for the 20% pass-through deduction introduced by the Tax Cuts and Jobs Act. This can effectively lower your tax rate on these dividends.

For optimal tax efficiency, consider holding REITs in tax-advantaged accounts like IRAs or 401(k)s. This strategy allows you to defer taxes on the high income they generate.

Exchange-Traded Funds (ETFs) often offer superior tax efficiency compared to mutual funds. This year, more ETFs are paying out capital gains than in 2022 and 2023. Nonetheless, ETFs remain more tax-efficient than mutual funds.

ETFs also allow for tax-loss harvesting, where you sell an underperforming ETF to realize a loss and offset gains elsewhere in your portfolio. This strategy can be particularly effective in volatile markets.

When you select ETFs, look for those with low turnover rates and consider broad market index ETFs, which tend to be the most tax-efficient.

While tax considerations play a significant role, they shouldn’t be the sole factor in your investment decisions. Your overall financial goals, risk tolerance, and investment timeline should guide your choices. A professional tax advisor can help you navigate these complex decisions and create a tax-efficient investment strategy tailored to your unique situation.

Investment planning is complicated by tax concerns, but a tax-aware approach can significantly enhance overall returns. Understanding the tax implications of different investment vehicles and strategies allows for informed decisions that align with financial goals while minimizing tax burden. A long-term perspective remains essential in investment planning, as it helps investors stay the course and make decisions that support sustainable growth.

Tax laws and market conditions change over time, so investors must regularly review and adjust their strategies. Working with a financial advisor provides invaluable benefits in navigating the complex interplay between investments and taxes. At Sager CPA, we offer expert financial management and tax planning services tailored for individuals and businesses.

Our team can help develop a comprehensive investment strategy that considers your unique financial situation, risk tolerance, and tax implications. A proactive approach to tax-aware investing and professional guidance optimizes investment returns while minimizing tax liabilities. This balanced strategy builds wealth more efficiently and provides greater financial stability as you work towards your long-term financial goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.