Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Tax-efficient investing strategies can significantly boost your overall returns. At Sager CPA, we’ve seen how smart tax planning in investment decisions can lead to substantial wealth accumulation over time.

Minimizing your tax burden while maximizing your investment growth is a powerful combination. This post will guide you through key strategies to optimize your portfolio’s tax efficiency and help you keep more of your hard-earned money.

Tax-efficient investing is a strategy that maximizes your after-tax returns by minimizing the impact of taxes on your investment portfolio. This approach recognizes that your actual gains are not just about how much your investments earn, but how much you keep after taxes.

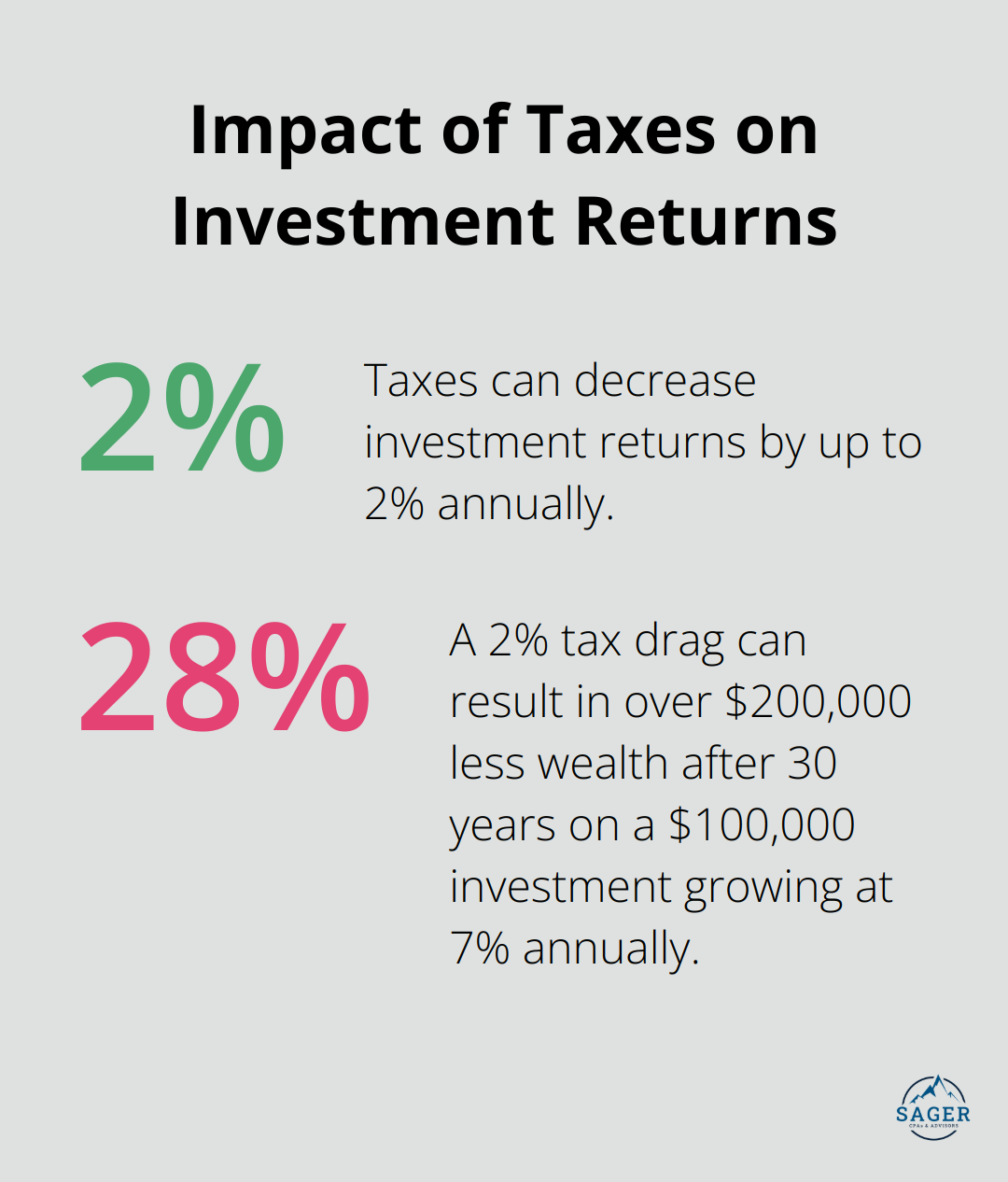

Taxes can significantly reduce your investment returns. A study by Vanguard found that taxes can decrease investment returns by up to 2% annually. This tax drag compounds over time, potentially resulting in substantial wealth loss. For instance, a $100,000 investment growing at 7% annually could result in over $200,000 less wealth after 30 years due to a 2% tax drag.

One effective tax-efficient strategy involves holding investments for longer periods. The IRS offers lower capital gains tax rates for long-term investors. As of 2025, long-term capital gains (on investments held for more than a year) are taxed at 0%, 15%, or 20%, depending on your income bracket. In contrast, short-term gains face taxation as ordinary income, which can reach rates as high as 37%.

Strategic asset location is another key aspect of tax-efficient investing. This strategy involves sorting your investments into different accounts, which has the potential to help lower your overall tax bill.

Tax-loss harvesting is a powerful tool for tax-efficient investors. This strategy involves selling investments that have decreased in value to offset capital gains from other investments. The IRS allows investors to deduct up to $3,000 of capital losses against ordinary income each year, with any excess carried forward to future years. However, it’s important to navigate this strategy carefully to avoid violating IRS wash sale rules, which prohibit repurchasing a substantially identical security within 30 days of the sale.

These tax-efficient investing strategies can help you keep more of your investment returns and accelerate your wealth accumulation over time. The next section will explore how to implement these strategies in your own portfolio, taking into account your unique financial situation and goals.

Strategic asset location enhances portfolio tax efficiency. Place investments in accounts that offer the most favorable tax treatment for each asset type. High-yield bonds and REITs (which generate regular taxable income) often perform best in tax-advantaged accounts like IRAs or 401(k)s. Growth stocks or index funds (with lower turnover and fewer taxable events) suit taxable accounts better.

Morningstar, an investment research company offering mutual fund, ETF, and stock analysis, ratings, and data, and portfolio tools, provides valuable insights into asset location strategies.

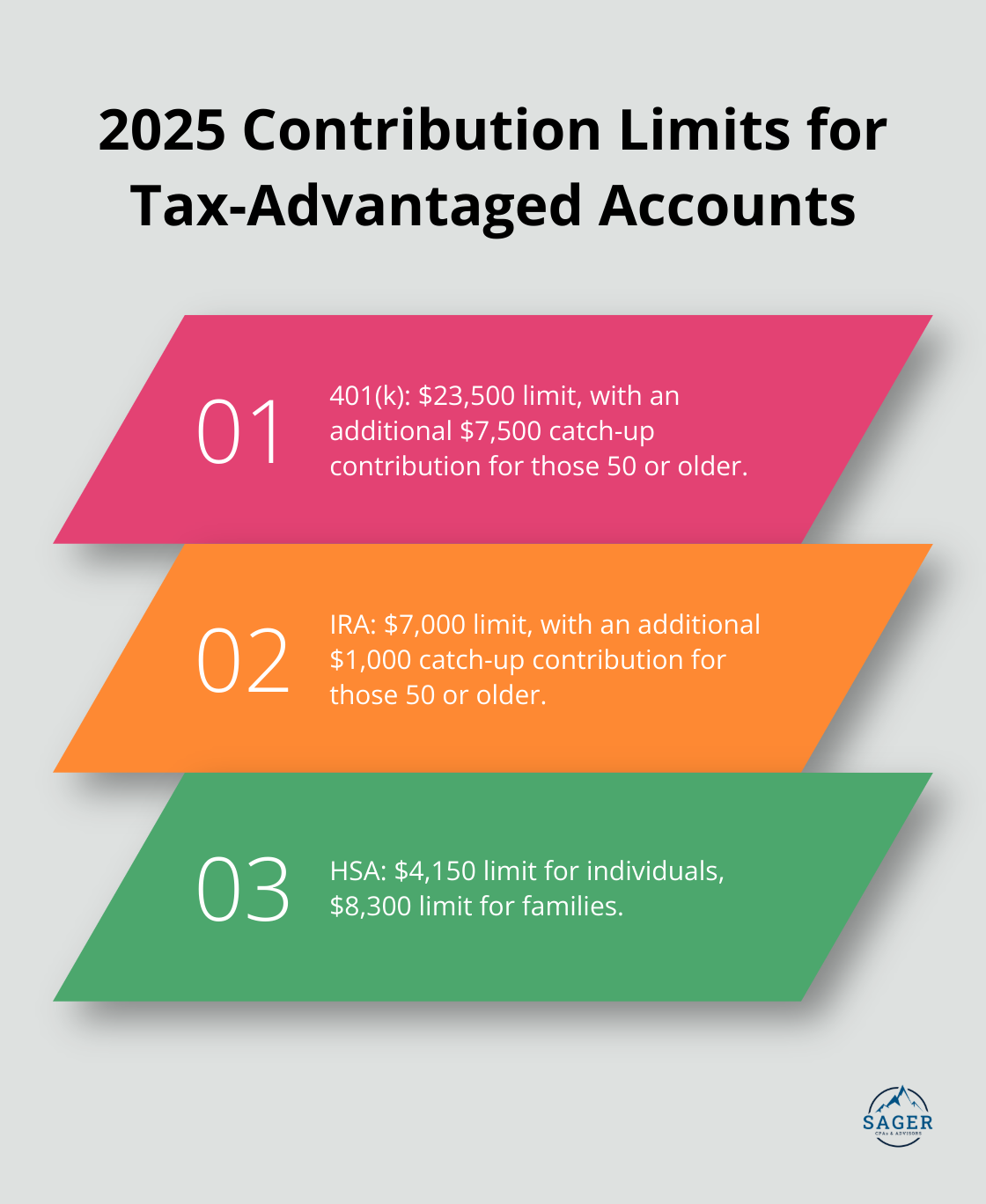

Tax-advantaged accounts form a cornerstone of tax-efficient investing. In 2025, you can contribute up to $23,500 to a 401(k), with an additional $7,500 catch-up contribution for those 50 or older. IRA limits stand at $7,000, with a $1,000 catch-up contribution.

Health Savings Accounts (HSAs) offer a unique triple tax advantage: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. In 2025, individuals can contribute up to $4,150, and families up to $8,300 to an HSA.

Municipal bonds excel as tax-efficient investments for higher tax bracket investors. These bonds typically exempt interest from federal taxes (and often state and local taxes for in-state residents). While municipal bonds generally offer lower yields than taxable bonds, their tax-exempt status can result in higher after-tax returns for investors in higher tax brackets.

For example, a municipal bond yielding 3% would equate to a taxable bond yielding about 4.62% for an investor in the 35% federal tax bracket (3% / (1 – 0.35)). This tax advantage significantly boosts overall returns, especially in high-interest rate environments.

Tax-loss harvesting reduces tax liability while maintaining overall investment strategy. This technique involves selling investments at a loss to offset capital gains. For instance, you could sell a depreciated stock to realize the loss and immediately reinvest in a similar (but not identical) security to maintain market exposure.

These tax-efficient investing strategies potentially keep more investment returns in your pocket and accelerate wealth accumulation. However, tax laws change constantly and require expert navigation. The next section will explore how to implement these strategies in your own portfolio, considering your unique financial situation and goals.

The first step to implement tax-efficient investing involves a thorough assessment of your current tax situation. Review your income sources, tax bracket, and existing investment portfolio. Your tax bracket determines the rates at which your investment income and capital gains are taxed. For example, in 2025, single filers with taxable income between $44,726 and $182,100 fall into the 22% federal tax bracket for ordinary income, but pay only 15% on long-term capital gains.

Scrutinize your portfolio for tax-inefficient investments. These often include actively managed mutual funds with high turnover rates, which can generate significant short-term capital gains. The average turnover rate for actively managed U.S. stock funds was 63% in 2024 (according to Morningstar), potentially resulting in higher tax bills for investors in taxable accounts.

Based on your tax situation and portfolio analysis, create a comprehensive tax-efficient investment plan. This plan should outline strategies such as:

When you rebalance your portfolio, consider the tax implications of your actions. Instead of selling appreciated assets in taxable accounts (which triggers capital gains taxes), try to rebalance within tax-advantaged accounts where possible. Alternatively, use new contributions to under-weighted asset classes to avoid realizing gains.

The implementation of a tax-efficient investing strategy can be complex. Collaboration with financial professionals provides valuable insights and ensures your strategy aligns with your overall financial goals. A financial advisor can potentially add 100 to 200 bps in net return through behavioral coaching, with tax-efficient investing and asset location being key contributors to this value.

Tax-efficient investing strategies maximize investment returns and accelerate wealth accumulation over time. These strategies minimize the impact of taxes on your portfolio, allowing more of your money to work for you. Your personal financial situation, goals, and risk tolerance determine the most effective strategies for you.

The long-term impact of tax-efficient investing can be substantial. Over decades, the compounding effect of tax savings can result in significantly higher wealth accumulation. This can mean the difference between a comfortable retirement and a truly prosperous one (or between achieving your financial goals and falling short).

Professional advice proves valuable when implementing tax-efficient investing strategies. At Sager CPA, we specialize in helping individuals and businesses optimize their financial strategies. Our team provides personalized guidance, ensuring your investment approach aligns with your overall financial plan and tax situation.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.