Tax Optimization for Businesses: Proactive Planning for Profits

Reduce your tax burden with strategic planning. Learn tax optimization strategies for businesses to keep more profits and grow faster.

At Sager CPA, we often get asked about the tax implications of financial planning services. Many people wonder if financial planning advice is tax deductible.

The answer isn’t always straightforward, as it depends on various factors and specific IRS guidelines. In this post, we’ll break down the rules and help you understand when and how you might be able to deduct financial planning fees on your taxes.

Financial planning advice is a professional service that helps individuals and businesses manage their money effectively. It creates a roadmap for your financial future, covering topics from budgeting and saving to investing and retirement planning.

Financial planning services encompass various areas:

Financial planning advice can significantly impact your financial health. The human capital theory suggests that individuals should invest a significant amount of time in learning how to plan for their healthcare in retirement or hire professional help.

Financial advisors stay up-to-date with changing tax laws and investment opportunities. For example, they can help you navigate complex situations like the 2020 CARES Act, which allowed for penalty-free withdrawals from retirement accounts due to COVID-19.

Financial planning isn’t just about making money-it’s about achieving your life goals. Whether you’re saving for a home, planning for your children’s education, or preparing for retirement, a solid financial plan can help you get there.

As we move forward, it’s important to understand how these financial planning services relate to tax deductions. The next section will explore the tax implications of financial planning fees and when they might be deductible.

The Tax Cuts and Jobs Act (TCJA) of 2017, effective for tax years 2018 to 2025, eliminated the deductibility for “miscellaneous items,” such as fees for financial advisors. This change will remain in place until 2025. Prior to the TCJA, taxpayers could deduct these fees as miscellaneous itemized deductions if they exceeded 2% of their adjusted gross income (AGI).

The impact of this change has been substantial. The Bipartisan Policy Center reports that the percentage of taxpayers who itemize deductions plummeted from 32% in 2017 to a mere 11% in 2018. This stark decrease highlights the far-reaching effects of the TCJA on tax strategies related to financial planning.

While direct deductions for financial planning fees are off the table for individuals, alternative strategies can help offset these costs:

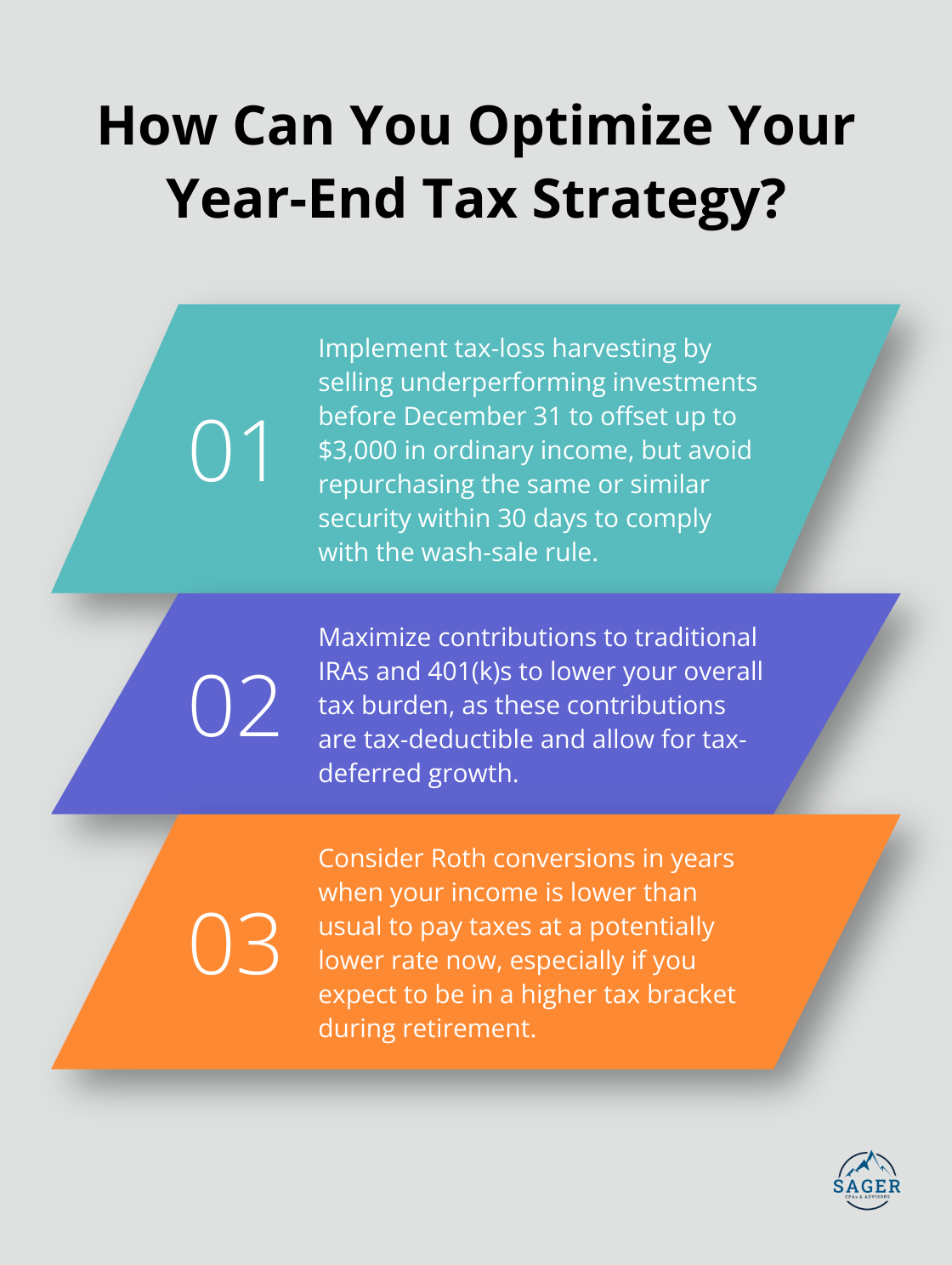

Financial advisors can still provide value through tax-efficient investment strategies. Tax-loss harvesting involves selling an investment that’s underperforming and losing money, then using that loss to reduce taxable capital gains and potentially offset up to $3,000 in ordinary income.

It’s important to note two key points:

While not directly related to advisor fees, contributions to certain retirement accounts can provide tax benefits. Contributions to traditional IRAs and 401(k)s are tax-deductible, which can lower your overall tax burden.

The tax landscape is not static. The TCJA provisions are set to expire in 2025, which could potentially restore the deductibility of financial planning fees. Until then, a focus on comprehensive financial planning that incorporates tax-efficient strategies can yield significant benefits.

Despite the current non-deductibility of fees, professional financial advice remains valuable. A skilled advisor can help navigate complex financial situations, optimize investment strategies, and provide insights that lead to long-term financial success.

As we move forward, it’s essential to consider how to maximize the tax benefits of financial planning within the current legal framework. The next section will explore strategies to optimize your financial planning efforts in light of these tax considerations.

One of the most effective ways to derive tax benefits from financial planning is through strategic investment management. Tax-loss harvesting is a popular investment strategy that seeks to obtain a tax benefit from the sale of securities that have declined in value. This strategy can significantly reduce your tax liability by offsetting capital gains taxes on your winning positions.

The IRS allows investors to offset up to $3,000 in ordinary income using realized losses through tax-loss harvesting. However, you must be aware of the wash-sale rule, which prohibits buying back the same or a substantially similar security within 30 days before or after a loss sale.

Another strategy focuses on long-term investments. The long-term capital gains tax rate is typically lower than the rate for short-term gains.

Retirement accounts offer another avenue for tax optimization. Contributions to traditional IRAs and 401(k)s are tax-deductible, providing immediate tax relief. Moreover, earnings in these accounts grow tax-deferred, allowing for increased compound growth without immediate tax implications.

For those who expect to be in a lower tax bracket in retirement, Roth conversions can be a powerful tool. You can benefit from a Roth conversion by paying taxes now at a lower rate if your tax rate is likely to be higher when you take distributions. This strategy can be particularly effective in years when your income is lower than usual.

While financial planning fees themselves may not be deductible, maintaining detailed records of all financial activities is important. This practice not only helps in accurately reporting income and deductions but also provides a clear picture of your financial health.

You should track all investment-related expenses, including transaction fees and research costs. While these may not be directly deductible, you can use them to adjust your cost basis, potentially reducing capital gains taxes when you sell investments.

For business owners or self-employed individuals, some financial planning costs may be deductible as business expenses if they relate directly to your business operations. Accurate records are essential for justifying these deductions if questioned by the IRS.

A comprehensive approach to financial planning goes beyond simple tax considerations. While maximizing tax benefits is important, it’s equally necessary to ensure that your financial strategies align with your overall goals and risk tolerance. You can work towards long-term financial success while optimizing your tax situation within the current legal framework by combining strategic tax planning with sound financial management.

Financial planning advice is not tax-deductible under current legislation, but its value extends beyond potential tax benefits. The Tax Cuts and Jobs Act of 2017 eliminated the deductibility of financial advisor fees for individuals until 2025. However, this doesn’t diminish the importance of professional financial guidance.

A holistic approach to financial planning considers your overall financial health, goals, and risk tolerance. Professional advice can help you navigate complex financial situations, optimize investment strategies, and provide insights that lead to long-term financial success. Tax considerations should not be the sole driver of your financial decisions.

Given the complexities of tax law and financial planning, consulting with a tax professional is important. At Sager CPA, we offer expert financial management and tax planning services tailored for individuals and businesses. Our approach ensures that you plan proactively for your financial future (not just react to current tax laws).

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.