Startup Financial Planning: Laying a Foundation for Growth

Build a solid financial foundation for your startup with our practical planning guide covering budgeting, forecasting, and growth strategies.

Most startups fail because of cash problems, not bad ideas. We at Sager CPA have seen firsthand how startup financial planning separates thriving businesses from those that run out of money.

This guide walks you through the core financial decisions you’ll face: managing cash flow, controlling costs, and choosing the right funding path. Get these foundations right, and you’ll have the clarity to grow with confidence.

Cash flow projections fail when founders treat them as wish lists instead of realistic forecasts. About one-third of startups admit to underestimating monthly expenses, which means your first instinct will likely be wrong. Start by listing every expense you actually pay: payroll, software subscriptions, rent, insurance, payment processing fees, hosting costs, and the supplies you forget about until the credit card bill arrives.

For revenue, use two approaches at once. Bottom-up means counting deals in your pipeline and applying realistic conversion rates from your actual sales data, not industry averages. Top-down means estimating your total addressable market and applying a conservative percentage you could realistically capture. When these two methods point in different directions, that gap reveals where your assumptions are weakest. A 12-month projection in a spreadsheet, month by month, matters because cash does not flow evenly. A SaaS company might collect payment upfront but pay hosting costs throughout the month, while a product business might need to purchase inventory before selling anything. Nearly 2 in 5 startups fail because they run out of cash, which happens because they ignored the timing difference between spending and receiving money.

It does. Burn rate is the amount of cash you spend each month minus the revenue you bring in, and it determines how many months you can survive on current funds. If you have $100,000 and burn $10,000 monthly, you have 10 months of runway. That number should terrify you into action if it falls under 12 months.

The mistake founders make is calculating gross burn (total monthly expenses) instead of net burn (expenses minus revenue). Gross burn looks worse and feels more urgent, but net burn is what actually matters for survival. Once you know your burn rate, stop updating it annually and start tracking it monthly because your business changes faster than you think. When you hit a hiring milestone or launch a new marketing campaign, your burn rate shifts immediately.

Establish a cash reserve specifically for unexpected expenses before crisis strikes, not after. Most startups face surprises: a key employee leaves and you need contract help, a supplier raises prices, or a major customer delays payment. These shocks force you to raise emergency funding or cut essential functions without a buffer in place.

Try to maintain three months of operating expenses in reserve. This reserve is not an investment account; it is insurance. Keep it in a separate high-yield savings account earning at least 4 or 5 percent annually, which adds meaningful returns on cash you hold anyway. With this foundation in place, you can move forward to the next critical decision: how you structure your expenses and control costs as you scale.

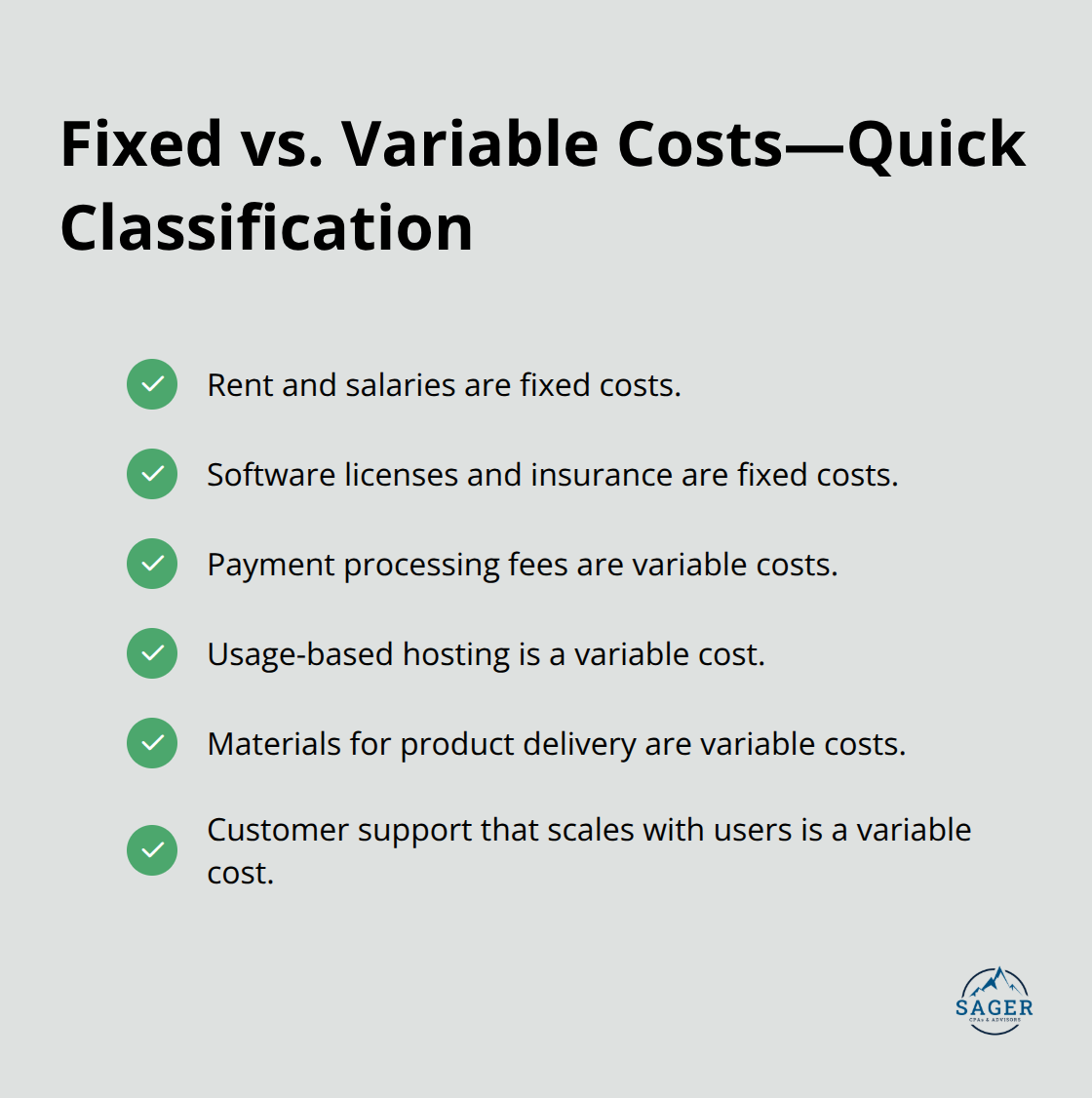

The gap between revenue and expenses determines whether your startup survives or suffocates. Most founders group all expenses together and call it done, which guarantees terrible cost decisions later. Separate your expenses into two categories immediately: fixed costs that stay the same regardless of sales volume, and variable costs that scale with revenue.

Fixed costs include rent, salaries, software licenses, and insurance. Variable costs include payment processing fees, hosting that scales with usage, materials for product delivery, and customer support labor that grows as your customer base expands. Once you see this split clearly, you understand which expenses to cut first when revenue disappoints.

If you have $50,000 in fixed costs monthly and revenue drops from $80,000 to $40,000, you cannot cut your way out of the problem by eliminating variable costs alone. This forces an honest conversation about headcount, office space, or subscriptions you’re paying for but not using. Track this split in your accounting system now, not when you’re in crisis mode.

Zero-based budgeting means you justify every dollar from scratch each quarter instead of assuming last quarter’s spending was correct. Start with zero and ask: what does this business actually need to accomplish its goals this quarter? Do you need all five software subscriptions or can two do the job? Are you paying for office space you barely use?

This method sounds tedious but catches waste that incremental adjustments miss. Most startups carry forward subscriptions, vendor contracts, or tools that made sense six months ago but no longer do. The process takes two hours with a spreadsheet: list every expense, assign it to a business outcome, and decide if that outcome still matters this quarter.

Companies that skip quarterly reviews bleed cash slowly until they cannot afford to hire talent or invest in marketing when it matters. Review your budget quarterly, not annually, because your business changes faster than traditional budgeting cycles allow. After each quarter, compare what you actually spent to what you projected, understand the variance, and adjust your next quarter’s assumptions.

This discipline keeps you grounded in reality instead of chasing a fantasy spreadsheet that bears no relationship to your actual business. With your expenses organized and controlled, you now face the biggest decision of all: where your growth capital comes from and whether you should raise it at all.

Bootstrapping means you fund growth from revenue you already earned, while seeking investment means you trade ownership for cash upfront. Neither path is objectively correct, but the choice determines everything about how you operate. Bootstrapped founders keep full control and avoid diluting equity, but they grow slower because every dollar spent comes from customers who already paid. Funded founders move faster but answer to investors whose exit timeline might not match yours. The real decision is whether your market window allows slow growth or demands speed to capture share before competitors arrive.

If you operate in a market where the first mover wins significantly more customers than the second, bootstrap and you lose. If you compete in a category where steady execution matters more than speed, bootstrap and you keep the upside. Most founders romanticize bootstrapping until they realize their unfunded competitor just hired a sales team and started winning deals. Map your specific competitive landscape first, then choose your funding path based on that reality rather than ideology.

Debt financing through bank loans or lines of credit requires you to repay principal plus interest regardless of business performance, which means you owe money even in bad months. This creates pressure but preserves ownership. Equity financing through angel investors or venture capital gives you cash without repayment obligation, but investors own a piece of your company and often want board seats or strategic influence.

Early-stage founders typically start with personal savings or friends and family rounds, then move to angel investors for amounts between fifty thousand and five hundred thousand dollars. Beyond traditional routes, alternative financing options like revenue-based financing and crowdfunding platforms offer new avenues for capital. Venture capital enters at Series A with millions of dollars but expects explosive growth and a clear path to acquisition or public markets within five to seven years.

The funding path you choose should align with your unit economics and growth speed requirements. A SaaS company with strong gross margins and predictable recurring revenue can often attract venture capital because the business model scales efficiently. A services business with low margins and high labor costs struggles to attract VC because growth requires proportionally more expense. If your gross margin sits below forty percent, venture capital is unlikely to fund you because the math does not work at scale. If your gross margin exceeds seventy percent, VCs want to meet you. This is not ideology; this is how capital allocation works.

Sustainable growth means your revenue growth rate exceeds your burn rate increase, which means each month you need less runway than the month before. Most startups do the opposite: they grow revenue ten percent monthly but increase spending twenty percent monthly, which accelerates the path to zero cash. Instead, set a specific rule for your business: if you bootstrap, growth must exceed expense increases. If you raise funding, define the exact milestones that justify spending increases and stick to them ruthlessly.

A practical approach is allocating a fixed percentage of revenue to marketing and hiring, then stopping when that budget is consumed, regardless of opportunity. This forces discipline and prevents the common founder mistake of spending investment capital as if it were infinite.

Startup financial planning works when you treat it as a living document, not a one-time exercise. Your cash flow projections will be wrong-accept this now-but what matters is that you update them monthly, compare actual spending to projections, and adjust your next quarter based on what you learned. This discipline separates founders who panic when cash runs low from those who saw it coming three months earlier and took action.

The funding path you choose shapes everything that follows. Bootstrapping teaches you to be ruthless about spending because every dollar comes from customers, while raising capital teaches you to move fast and capture market share before competitors do. Neither approach is wrong, but choosing the wrong one for your specific market is fatal-map your competitive landscape honestly, understand your unit economics, and let that reality guide your decision.

Professional financial guidance becomes invaluable as your startup grows beyond the initial stage. We at Sager CPA work with founders to build financial systems that scale, create tax strategies that preserve cash, and prepare clean financials that investors actually trust. Schedule a consultation with Sager CPA to create a personalized financial strategy tailored to your business stage and growth goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.