Owner Retirement Income Planning: Securing Your Golden Years

Plan your owner retirement income with strategies to maximize wealth, minimize taxes, and secure financial independence for your future.

Most business owners spend decades building wealth but never create a concrete plan for accessing it in retirement. Owner retirement income planning isn’t something you can improvise-it requires strategy, timing, and a clear understanding of your financial picture.

At Sager CPA, we’ve seen too many entrepreneurs leave money on the table because they didn’t plan ahead. This guide walks you through the essential steps to turn your business success into lasting retirement income.

Most business owners have never calculated their actual retirement expenses. They assume they’ll spend less than they do now, then face a painful reality check within months of retiring. The truth is blunt: experts estimate you need to replace 70 to 90 percent of your pre-retirement income to maintain your standard of living. That’s not a suggestion-it’s a baseline.

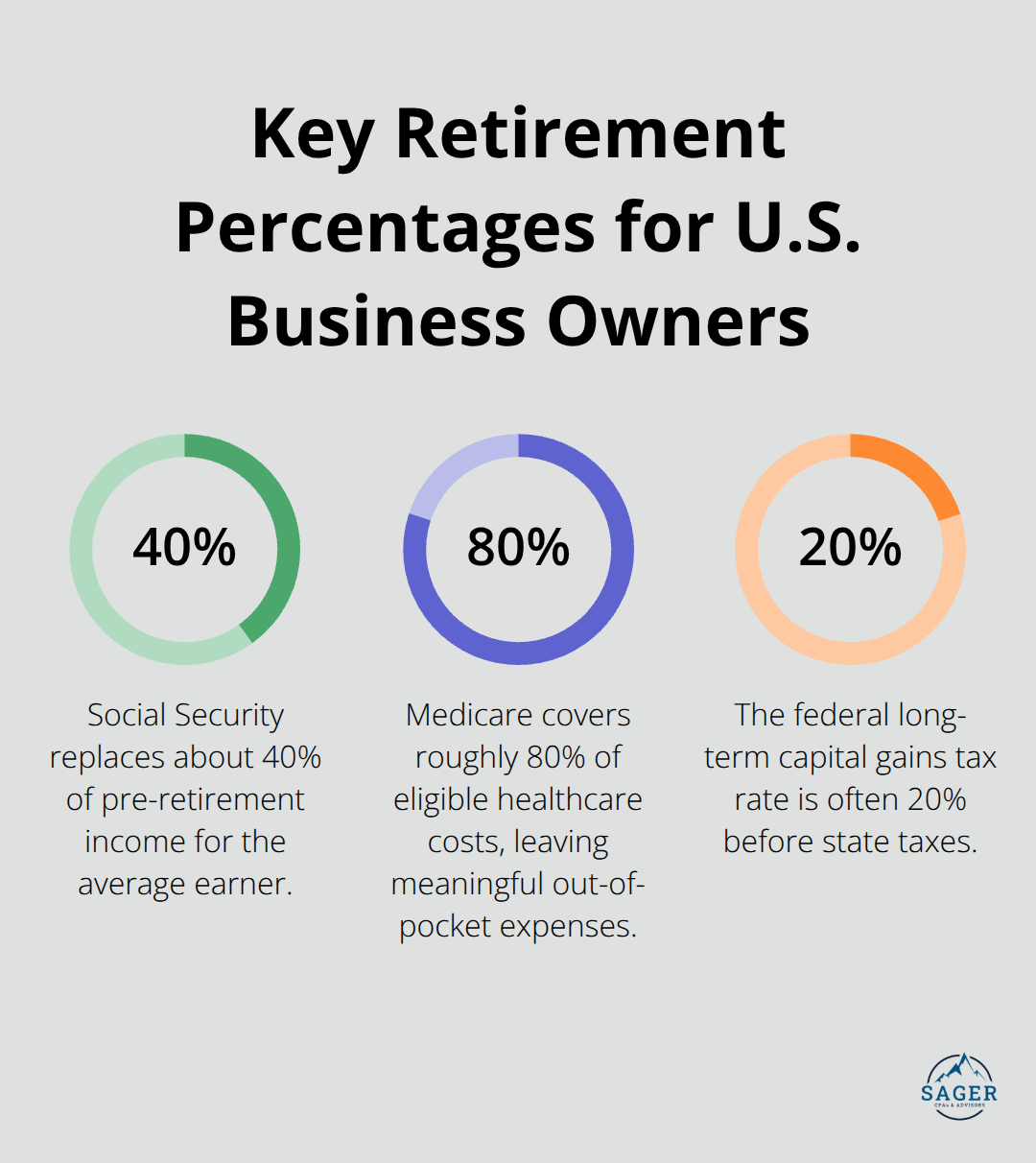

Start by listing every expense you currently have: housing, utilities, insurance, healthcare, travel, dining, hobbies, and gifts. Then project which expenses disappear in retirement (commuting costs, work clothes, business meals) and which increase (healthcare, travel, leisure activities). Most business owners underestimate healthcare costs significantly. Medicare covers roughly 80 percent of eligible costs, leaving substantial out-of-pocket expenses, and long-term care can drain retirement savings faster than any other factor. Add a 3 to 4 percent annual inflation buffer to your projections because expenses won’t stay static over a 20-year retirement-the average American spends roughly two decades retired.

Next, inventory what you actually have. Social Security replaces about 40 percent of pre-retirement income based on your earnings history, according to the Social Security Administration. Use their retirement estimator tool to see your projected benefits and test different claiming ages. Many business owners delay claiming until 70 to maximize payments, but others need income earlier and claim at 62-the decision depends entirely on your health, other assets, and cash flow needs.

Then assess your business value. If you plan to sell your company, that’s your largest asset, but most owners haven’t had a formal valuation. A CPA can help determine realistic sale value, earnout structures, and tax implications. Beyond the business, account for retirement accounts (401(k), SEP IRA, Solo 401(k), traditional and Roth IRAs), real estate equity, investment portfolios, and any pensions. Document the exact balances and growth rates-vague estimates lead to vague plans that fail when you retire.

Subtract your projected income sources from your projected expenses. That gap is the number that should drive every financial decision you make over the next few years. If your gap is $50,000 annually and you have $1 million in liquid assets, you’re on track. If your gap is $100,000 and you have $500,000 in assets, you have serious work to do.

This gap forces honest conversations about whether your business sale will fund retirement, whether you need to work longer, or whether you need to reduce expenses. Some owners realize they need to accelerate business growth before selling. Others recognize they should diversify income streams now rather than depend entirely on one lump sum. The gap is uncomfortable but essential-it’s the difference between retiring with confidence and retiring with regret. Understanding this number positions you to make strategic moves that actually work, which brings us to the specific strategies that transform your business into reliable retirement income.

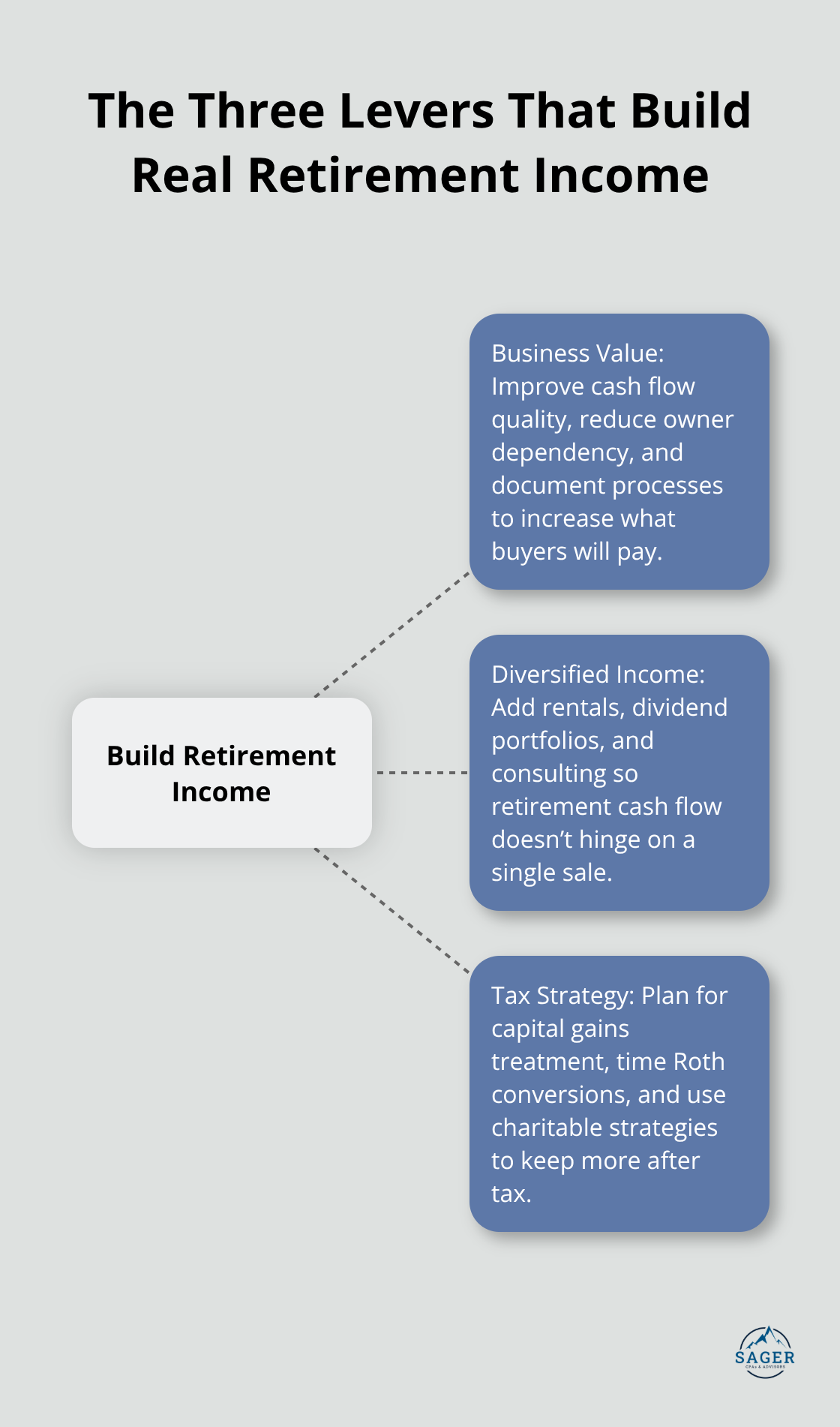

The gap you identified in the previous section won’t close itself. You need deliberate moves now to transform your business into actual retirement cash. Most owners wait too long, then scramble in their final working years. That approach costs money-sometimes hundreds of thousands of dollars. Three areas move the needle: your business value, your income diversification, and your tax strategy. Each one demands action, not wishful thinking.

Your business is likely your largest asset, but its value isn’t fixed-it depends on what a buyer will actually pay for it. Buyers evaluate cash flow, customer concentration, employee retention, and recurring revenue. If your business depends on you personally, its value drops significantly because a buyer inherits the risk that customers leave when you do.

Start now by documenting your processes, cross-training key employees, and building customer relationships beyond yourself. A business that runs without you is worth 30 to 50 percent more than one that doesn’t. If you have three years before retirement, spend them reducing your operational dependency. A formal business valuation from a CPA will show you exactly where your business stands and what specific improvements drive value. Don’t guess-get the number.

Beyond maximizing sale value, consider whether a full exit makes sense or whether you should stay partially involved through an earnout agreement, where the buyer pays you over time based on business performance. Earnouts let you reduce your retirement income gap while staying engaged in work you built. They also spread your tax liability across multiple years instead of one massive year, which matters significantly for your overall tax bill.

Diversification is your second lever, and most owners ignore it until it’s too late. Relying entirely on a business sale creates massive risk-the deal might not happen, the price might disappoint, or the timeline might shift. Instead, build secondary income streams now.

Real estate investments generate ongoing rental income that doesn’t depend on business performance. A 20-unit apartment building generating $8,000 monthly cash flow provides $96,000 annually in retirement income, independent of whether your business sells. Dividend-paying investment portfolios work similarly-a $500,000 portfolio generating 4 percent annually produces $20,000 in retirement income. Consulting arrangements with your successor or industry peers generate income while you transition out of full-time work.

These aren’t theoretical ideas-they’re concrete income sources you control. Start building them now by allocating a portion of current business profits to real estate investments, investment accounts, or developing consulting relationships. The sooner you start, the more time these income streams have to mature before retirement arrives.

Your third area is tax efficiency, which directly impacts how much retirement income you actually keep. When you sell your business, the proceeds trigger capital gains taxes, often 20 percent federal plus state taxes depending on where you live. A $2 million sale nets roughly $1.4 to $1.6 million after taxes-a substantial difference from the headline number.

Tax-efficient withdrawal strategies in retirement matter equally. Roth conversions before age 72 let you move money from traditional retirement accounts to Roth accounts at a lower tax rate now, then withdraw tax-free in retirement. This strategy works especially well in years between business sale and when required minimum distributions begin. Charitable giving strategies, if you care about philanthropy, can reduce your taxable income while funding causes you believe in.

A CPA experienced in business owner transitions can structure your sale and retirement withdrawals to minimize what you owe in taxes. The difference between a generic accountant and a strategic one often exceeds $50,000 over your retirement years.

These three areas aren’t independent-they work together. A higher business sale price reduces how much you need from other income sources. Diversified income streams reduce pressure to maximize business value at any cost. Tax-efficient strategies applied at the right time multiply what you keep from both business sales and investments.

The owners who retire with confidence aren’t the ones who stumble into retirement-they’re the ones who orchestrate it. Your next step is identifying which of these three areas offers the fastest payoff for your specific situation, which means understanding the mistakes that derail most business owners before they even get close to the finish line.

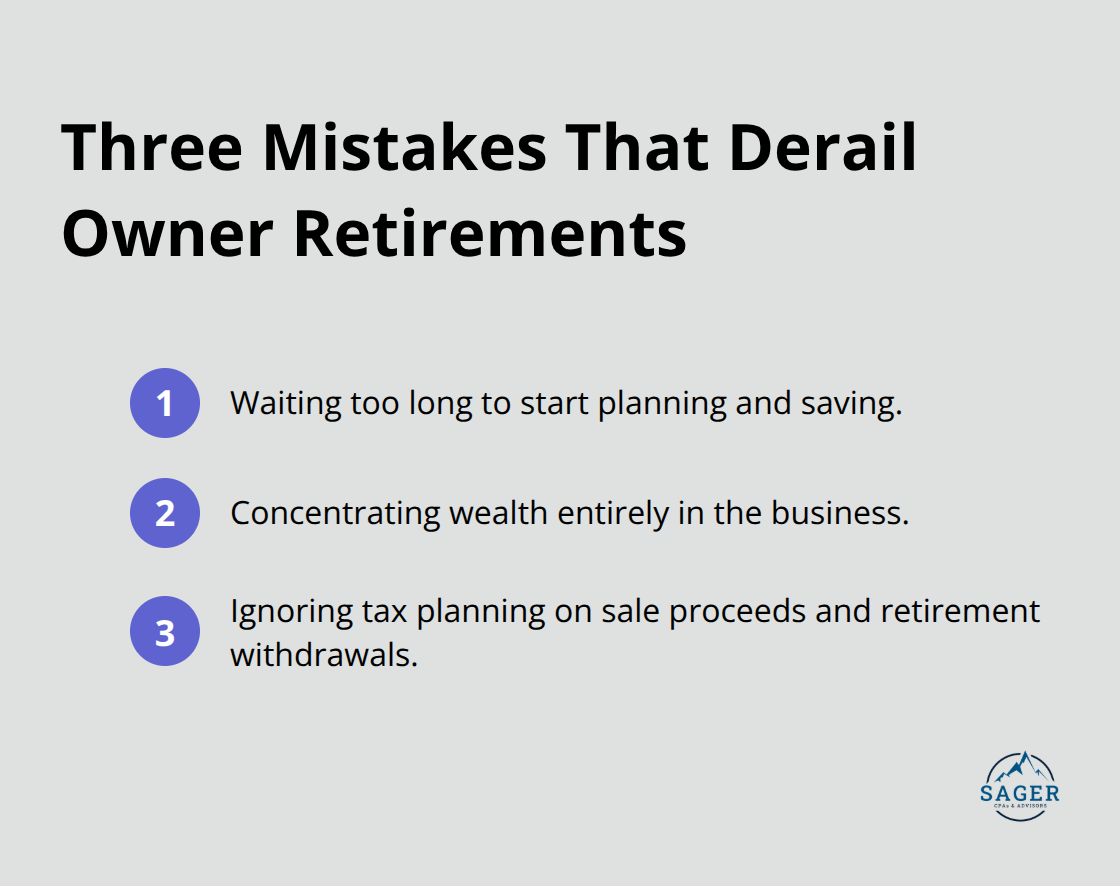

Most business owners make their biggest retirement planning mistakes between ages 45 and 55, when they still have time to fix them but convince themselves they don’t. The first mistake is waiting too long to start.

Gallup research shows that retirement plans participation rates among U.S. income brackets reveals significant disparities: households earning over $100,000 have retirement plans at an 83 percent rate, while households earning under $50,000 sit at just 28 percent. The gap in retirement confidence follows this same pattern.

Starting at 45 instead of 35 doesn’t just cost you compound growth-it costs you the psychological anchor of a concrete plan. When you lack one, you operate in denial and tell yourself you’ll figure it out later. Later arrives and you’re scrambling. A business valuation at 45 followed by three years of intentional value-building creates a fundamentally different outcome than waiting until 58 to get serious. The math is brutal: saving $6,500 annually at 7 percent returns grows to roughly $47,000 over five years, $138,000 over fifteen years, and $1.1 million over thirty-five years. Start at 45 instead of 35, and you lose hundreds of thousands in growth that you can never recover.

The second mistake is concentrating everything in your business. You’ve spent two decades building it, so naturally it feels safe. It isn’t. If your entire net worth sits in one company and the buyer backs out, the economy tanks, or a competitor emerges, your retirement evaporates. Many owners delay building real estate investments, investment portfolios, or consulting relationships because they assumed the business sale would fund everything. Then the sale falls through or takes two years longer than expected, and they’re forced to work past their target retirement date.

A $2 million business sounds like security until you realize that selling it generates one taxable event and then you need that money to last twenty to thirty years. Real estate producing $8,000 monthly generates $96,000 in annual retirement income that exists independent of business performance. A $500,000 investment portfolio generating 4 percent annually produces $20,000 in stable income. These secondary streams take years to build, which is exactly why you can’t wait until you’re fifty-eight to start. The owners who retire confidently are the ones who have multiple income sources working in parallel, not the ones betting everything on a single transaction.

The third mistake is underestimating taxes on the sale and retirement withdrawals. A $2 million business sale triggers capital gains taxes that often run 20 to 25 percent federally plus state taxes, netting you $1.4 to $1.6 million instead of the headline number. Many owners never calculate this. They see $2 million and plan around it, then get blindsided by the tax bill.

Equally damaging is ignoring tax-efficient withdrawal strategies in retirement. Roth conversions between business sale and age 72 let you move traditional retirement account balances to Roth accounts at lower tax rates now, then withdraw tax-free later. Charitable giving strategies, if philanthropy matters to you, reduce taxable income while funding causes you believe in. A strategic CPA can structure your sale and withdrawals to minimize what flows to the government instead of your bank account. The difference between thoughtful tax planning and generic preparation often exceeds $50,000 over retirement.

These three mistakes-starting too late, concentrating wealth, and ignoring taxes-aren’t inevitable. They result from inaction and wishful thinking instead of deliberate strategy. The owners who avoid these traps take action in their mid-forties, build multiple income streams, and work with a tax professional who thinks strategically about their specific situation.

Owner retirement income planning requires three concrete actions: calculate what you actually need, build multiple income sources before you retire, and structure your exit to minimize taxes. The owners who retire with confidence take a business valuation in their mid-forties, start building real estate or investment income streams immediately, and work with a CPA who thinks strategically about their specific situation. They understand that a $2 million business sale nets significantly less after taxes, so they plan accordingly, and they recognize that concentration risk in a single asset threatens their financial security.

Your next step demands honesty about where you stand right now. Identify whether you have a current business valuation, whether you have calculated your actual retirement expenses, whether you know what Social Security will provide, and whether you have secondary income streams beyond your business. If you answered no to any of these questions, you have work to do-and the sooner you start, the more options you will have when retirement arrives.

We at Sager CPA work with business owners to create personalized retirement strategies that account for your business value, your tax situation, and your specific goals. Schedule a consultation with our team to build a concrete plan that turns your business success into lasting retirement income. The difference between a generic approach and a strategic one often exceeds what you will spend on professional guidance.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.