Owner Retirement Income Planning: Securing Your Golden Years

Plan your owner retirement income with strategies to maximize wealth, minimize taxes, and secure financial independence for your future.

Most startups fail because founders skip the financial planning phase. We at Sager CPA have seen countless founders jump straight to product development without understanding their cash position.

Early stage startup planning requires three critical steps: validating your concept, building a financial foundation, and achieving cash flow readiness. This guide walks you through each phase so you can move forward with confidence instead of guesswork.

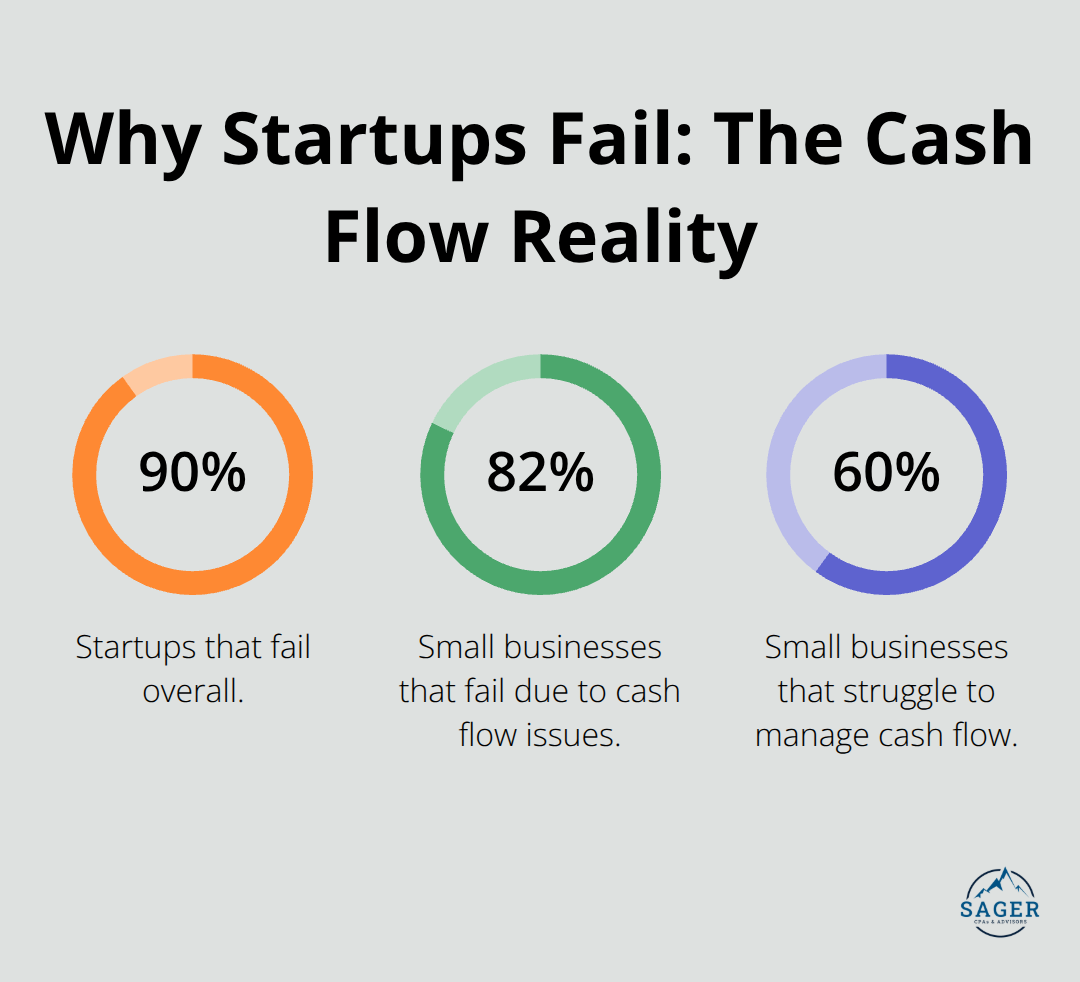

Skip customer conversations and your startup dies. Around 90% of startups fail, and a significant portion never validate that anyone actually wants what they are building.

The U.S. Chamber of Commerce reports that cash flow issues can result from a lack of funding, poor budgeting, or inventory management issues, but the root cause often traces back earlier-to launching without proof of demand.

Start by talking to at least 20 people in your target market who face the problem you want to solve. These conversations must happen before you write a single line of code. Ask about their current tools, what frustrates them, and how much they currently spend on solutions. Don’t ask leading questions like “Would you use this?” Instead, ask about their actual workflow and pain points.

When Material Security’s founders tested their security idea, they created marketing vignettes that resembled sales pages to gauge enterprise buyer interest without building anything. This approach forced them to clarify messaging and revealed what buyers actually cared about-integration timelines, not product features alone.

Your friends will praise your idea. Strangers will tell you the truth. Sprig’s founders specifically recruited cold contacts at YC-backed companies for feedback rather than relying on their network. This reduced bias and surfaced real objections. When you hear skepticism about market size, customer willingness to pay, or execution difficulty, that’s valuable intelligence.

Seek out founder networks and industry insiders-lawyers, investors, and operators in your space can point out feasibility gaps you missed. Linear’s founders validated their startup idea by interviewing coworkers about performance bottlenecks before they quit their jobs. This grounded their assumptions in specific, measurable problems.

Research your competitors using platforms like CB Insights, PitchBook, and Crunchbase to understand what they charge, who they serve, and where they struggle. If a competitor has a 2-star rating on G2 for customer support, that’s your opening.

Identify the smallest atomic unit of value you can test-not the entire product, just the core feature that solves the primary pain. Test that one risky assumption with real customers willing to pay, even if it’s a pilot or limited launch. If customers won’t pay enough to cover your development costs, iterate or pivot before you burn through your runway. This validation work directly informs the financial foundation you’ll build next.

Validation proved your market wants what you are building. Now comes the part most founders avoid: building a financial model that tracks actual money flowing in and out. This is not optional busywork. The U.S. Chamber of Commerce reports that 82% of small businesses fail due to cash flow issues, and about 60% of small businesses struggle with managing cash flow according to PYMNTS. These failures happen because founders treat financial planning as something to do after launch, not before.

Open a spreadsheet and input three things: your current cash on hand, how much money comes in each month, and how much goes out. That is your foundation. Use monthly periods for the first 18 months so investors see you understand near-term reality, then simplify forecasts for years two and three. Do not create separate models for different audiences. One spreadsheet becomes both your operational dashboard and your investor pitch. Label every column with actual month and year, separate known inputs from assumptions, and show all calculations so someone can follow your logic.

The most common mistake founders make is projecting revenue without grounding it in unit economics. If your customer acquisition cost is $500 and the average customer pays you $600, you need enough cash to acquire at least 50 customers before you break even. That is your real runway constraint, not some arbitrary monthly burn rate.

Your model must explain why cash moves the way it does. If you project revenue growth of 20% month-over-month, what drives that? More customers? Higher prices? More product usage? Tie each revenue line to a concrete driver like user signups, conversion rate, or average deal size.

For expenses, break spending into people costs versus non-people costs because that reveals where your money actually goes and where you can find savings.

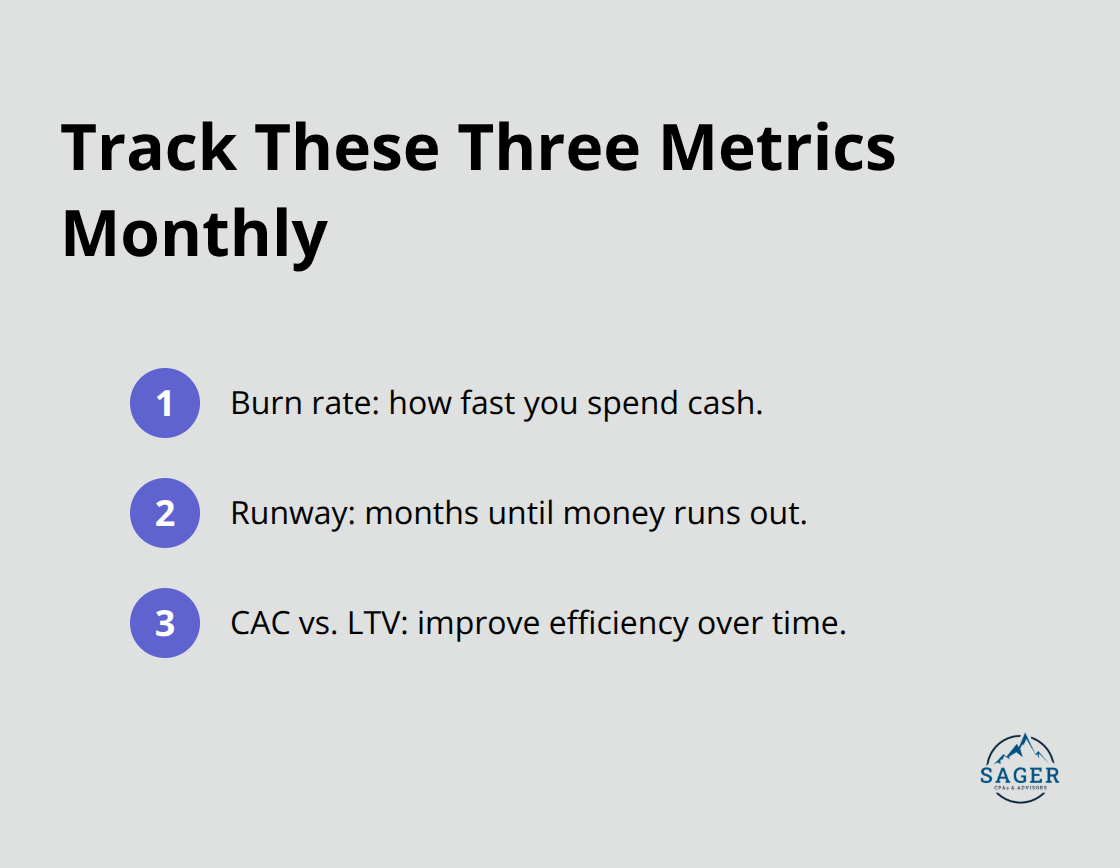

If payroll is 70% of your budget, you have a hiring problem. If office rent is killing your runway, negotiate or relocate before you run out of cash. Track three critical metrics monthly: burn rate (how fast you spend cash), runway (months until money runs out), and customer acquisition cost relative to customer lifetime value. Your efficiency target is to improve this ratio over time.

If your DSO (Days Sales Outstanding) is 90 days but you only have 60 days of runway, offer a 10% discount for upfront payment. That simple move accelerates cash and extends your viability. Monthly reconciliation is non-negotiable: compare your spreadsheet ending balance to your actual bank statement. If they do not match, investigate immediately. This discipline catches errors before they become catastrophic.

Conservative assumptions for the next 12 to 18 months preserve credibility with investors who will ask three specific questions: will you run out of cash, what measurable progress happens with this raise, and can you raise the next round? Your model must answer all three clearly. With your financial foundation in place, you now shift focus to the longer view-mapping out exactly when you need funding and how seasonal patterns or unexpected costs will test your cash reserves.

Your 12-month cash flow forecast tells you exactly when money runs dry. Most founders guess. You need to know the precise month when your bank account hits zero if no revenue comes in. Start with your current cash, subtract monthly burn (total expenses minus any incoming revenue), and calculate how many months you can operate. This number is your runway. If you have $50,000 and burn $8,000 per month, you have 6.25 months before the lights go out. That becomes your hard deadline for either generating revenue, raising capital, or both.

The timeline for securing funding matters more than the amount. If you need Series A in month eight but investors typically take four months to decide, you must start fundraising in month four. That means your financial model needs to project forward with brutal honesty about what milestones you need to hit to attract investors. Series A rounds typically span 18 to 24 months from first conversation to cash in the bank, so plan accordingly. Don’t wait until month seven to start pitching. Most founders raise when they’re desperate, which puts them in a weak negotiating position. Raise when you have six to nine months of runway left, when you have momentum and choices.

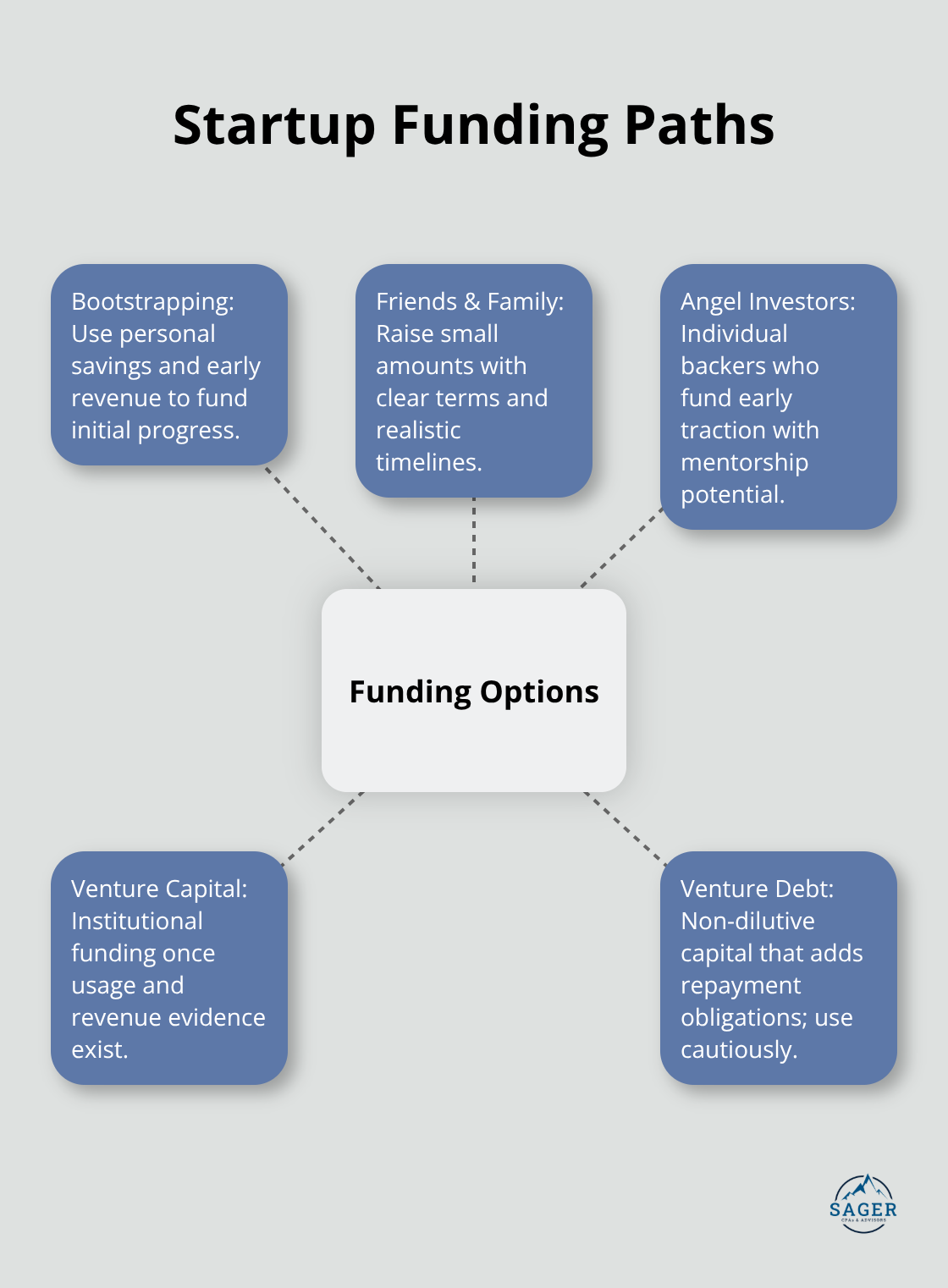

Venture capital is only one path, and it’s not always the right one. Early-stage startups typically bootstrap with personal funds, then move to friends and family rounds once they have initial traction. Friends and family rounds are delicate because these conversations require clear terms, realistic projections, and honest timelines.

Don’t ask your uncle for $50,000 without showing him your financial model and explaining exactly how you’ll use it. That conversation is harder but it builds trust and prevents relationship damage later.

Angel investors and venture firms enter the picture once you have a product customers actually use and revenue starting to flow. They’ll ask specific questions your financial model must answer: what’s your customer acquisition cost, what’s your retention rate, and how many months until you break even or reach profitability. If you can’t answer these with real data, you’re not ready for institutional capital. Some founders also consider venture debt as a bridge between equity rounds, but this adds interest payments and repayment obligations on top of your burn. Consult a financial advisor before taking on debt because it constrains your flexibility if fundraising takes longer than expected.

Seasonal patterns destroy cash flow forecasts that ignore them. If you sell to schools, revenue drops in summer. If you sell to retailers, December is massive but January is quiet. Map out your actual revenue patterns by month, not just annual totals. This changes your funding timeline. You might need a bridge loan or line of credit to survive the slow months, even if the year looks profitable overall.

Unexpected costs are guaranteed to appear. Equipment breaks. A key hire needs to be replaced quickly. A vendor raises prices. Budget 10 to 15 percent of your monthly expenses as a contingency reserve so one surprise doesn’t force you into panic mode. If you invoice in January but don’t get paid until March, your cash forecast looks terrible in February even though the money is coming. Model this explicitly by showing when revenue is recognized versus when cash arrives.

Your financial model isn’t a one-time document. Update it monthly with actual results, compare forecast to reality, and adjust forward projections based on what you’re learning. If customer acquisition costs more than you projected, that changes your runway calculation immediately. If retention is better than expected, you might need less capital than planned. This discipline keeps you grounded in reality instead of hoping your original assumptions were correct. When you update monthly, you catch problems early enough to fix them instead of discovering a cash crisis two weeks before it happens.

You’ve mapped the path from concept to cash flow readiness through three non-negotiable steps: validating that real customers want your solution, building a financial model grounded in actual numbers, and forecasting exactly when you’ll need funding. Early stage startup planning fails when founders skip validation and jump straight to spreadsheets, or worse, when they build a financial model disconnected from real customer behavior and market data. The most common mistake we see is treating the financial model as a one-time exercise for investors rather than a living operational tool that answers your own questions weekly.

Underestimating runway constraints destroys more startups than bad assumptions do. If you have six months of cash and Series A fundraising takes four months, you start conversations in month two, not month five-founders who wait until desperation sets in lose negotiating power and often accept unfavorable terms. Seasonal patterns and unexpected costs derail forecasts regularly, so model slow months explicitly and budget 10 to 15 percent of monthly expenses as contingency since surprises are guaranteed.

The path forward requires discipline: update your model monthly, reconcile it to your actual bank balance, and adjust projections based on what’s really happening. We at Sager CPA help founders and early-stage businesses build financial strategies that connect validation to sustainable growth. Schedule a consultation with us to create a personalized financial strategy that keeps your startup on track from concept through scaling.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.