Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Your business is likely your biggest financial asset, yet most business owners plan their retirement the same way employees do. That approach leaves money on the table and misses critical tax opportunities.

At Sager CPA, we’ve seen business owner retirement planning go wrong too many times-owners exit without a strategy and watch thousands slip away in taxes. The good news is that with proper planning, you can structure your exit to keep more of what you’ve built.

Most business owners have between 80 and 90 percent of their personal net worth tied directly into their company, according to wealth management research on business owner finances. That concentration of wealth creates a fundamentally different retirement scenario than what standard 401k and IRA planning addresses. When you retire as an employee, your company stays intact and your retirement accounts remain yours. When you own the business, the business itself becomes the retirement account, and selling it or transferring it becomes the defining financial event of your life. Generic retirement planning ignores this reality entirely. It assumes your wealth is already diversified across stocks, bonds, and savings accounts. It fails to account for the timing of a business sale, the tax hit from that sale, or the need to convert a single large asset into sustainable retirement income.

Standard financial advisors build retirement plans around diversified portfolios and steady income streams. They work with 401ks, IRAs, and investment accounts that follow predictable tax rules. Your business operates under completely different rules. A business sale triggers capital gains taxes, potentially at both federal and state levels. The timing of that sale affects your tax bracket for the year. The structure of the sale (asset versus stock, installment versus lump sum) determines how much tax you actually owe.

Most financial advisors lack the framework to handle these variables because they’ve never worked with business valuations, entity structures, or the specialized strategies that apply to business exits.

A business sale without deliberate tax planning can erode significant proceeds in federal and state taxes. An owner selling a business for $2 million without optimization might lose substantial amounts to taxes, leaving considerably less for retirement. The same sale with proper structuring-considering installment sales, charitable strategies, or 1042 exchanges for eligible transactions-can preserve significantly more. The difference between a reactive exit and a planned one often amounts to hundreds of thousands of dollars.

Your standard retirement planner cannot navigate these options because they require specialized knowledge of business valuation, entity structure, capital gains treatment, and timing strategies that most financial advisors simply don’t possess. This gap between employee retirement planning and business owner retirement planning becomes critical when your exit approaches. You need someone who understands both the operational side of your business and the tax implications of moving that business into a post-sale financial strategy. The strategies available to you depend on your entity type, the buyer’s identity, and your personal tax situation-variables that demand expertise in business taxation and exit planning.

These tax and structural decisions shape not just your immediate proceeds, but your entire retirement income stream. Getting them right requires planning that starts years before you actually sell.

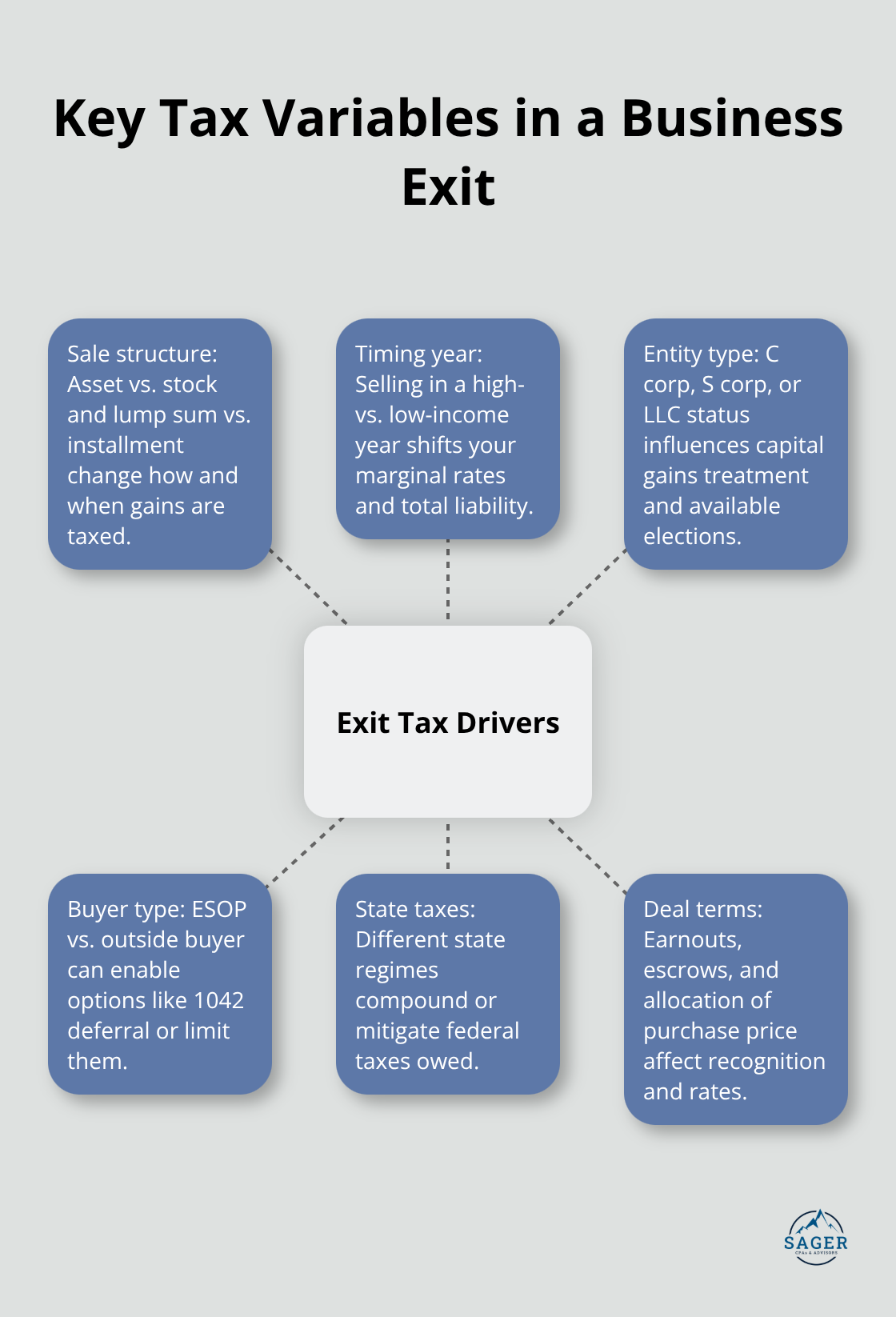

The way you structure your business sale determines how much tax you actually owe, and that decision should never be made casually. An asset sale versus a stock sale creates fundamentally different tax outcomes for you as the seller. In an asset sale, you sell the individual components of your business-inventory, equipment, customer lists, goodwill-and each asset gets taxed at potentially different rates. In a stock sale, you’re selling ownership shares, which generally receives capital gains treatment. The choice between these structures depends on what the buyer prefers, your entity type, and your personal tax situation.

If you structure the deal as an installment sale rather than a lump-sum payment, you can spread the capital gains across multiple years, which keeps you in a lower tax bracket each year and reduces the total tax hit. This approach also improves cash flow because you receive payments over time instead of facing a massive tax bill in year one. For C corporations with eligible stock sales, a 1042 exchange allows you to defer capital gains entirely if you reinvest the proceeds in qualified replacement property-though this requires the buyer to be an employee stock ownership plan and advance planning before the letter of intent is signed.

The timing of your exit matters just as much as the structure. Selling during a year when your other income is lower reduces your overall tax bracket and can save tens of thousands in federal taxes alone. State taxes compound this effect significantly; selling in a high-income year in a high-tax state versus a lower-income year in a lower-tax state can swing your after-tax proceeds by six figures or more. Consider your age and required minimum distribution obligations if you’re over 70½-selling in a year before your RMDs begin, or coordinating the sale with charitable giving strategies, can offset substantial tax liability.

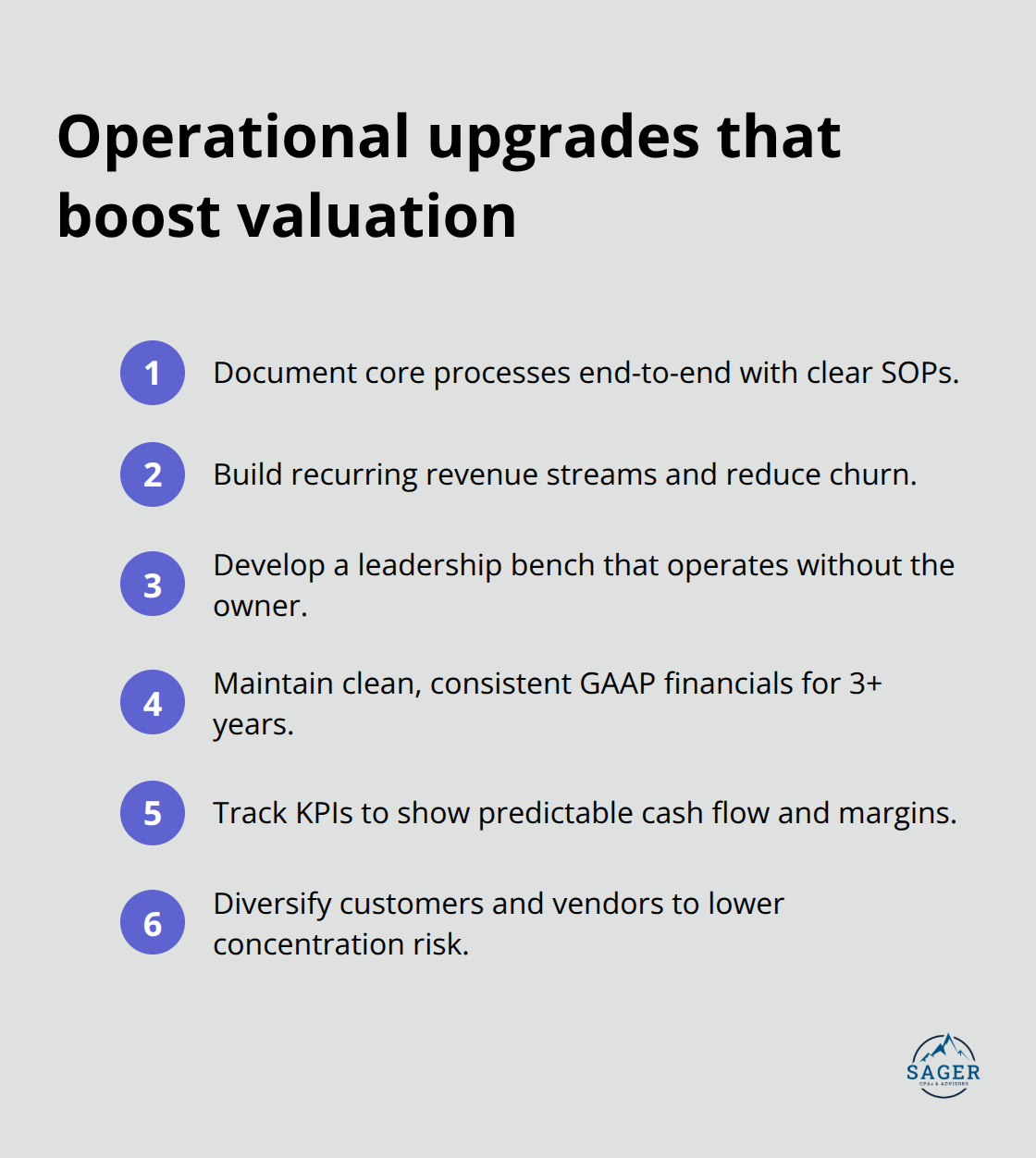

Beyond tax structure and timing, the operational strength of your business directly affects what a buyer will pay. Buyers conduct thorough due diligence and pay premiums for businesses with documented systems, recurring revenue, and leadership depth beyond the owner.

Recurring revenue models offer predictable income, which is highly appealing to buyers. Document your processes, build a management team that can function without you, and show consistent financial records for at least three years. A business with strong systems, a capable team, and predictable cash flow attracts multiple buyers and commands higher offers, which gives you negotiating leverage and reduces the pressure to accept the first offer that comes along.

The financial structure of your sale shapes immediate proceeds, but what you do with those proceeds determines whether your retirement actually works. That’s where post-sale strategy becomes equally important to the exit itself.

Selling your business solves the immediate liquidity problem, but it creates a new one: converting that lump sum into sustainable retirement income while preserving wealth for the people and causes that matter to you. The proceeds from your business sale represent years of work compressed into a single financial event. How you deploy that capital in the months after closing determines whether your retirement thrives or merely survives.

If you plan to keep the business operating under new leadership rather than sell it outright, you need a formal succession plan years before you step back. The PwC 2023 U.S. Family Business Survey found that only one-third of family businesses had a written succession plan, which explains why so many transitions collapse into conflict and value destruction. A documented plan identifies who takes over, what skills they need, and how you’ll phase out your involvement.

For family businesses, have explicit conversations about whether your children or other relatives actually want to run the company, what compensation they’ll receive, and how the ownership structure will change. For employee succession, identify your highest-performing managers at least five years before you want to exit, then create a deliberate development path that includes mentoring, expanded responsibilities, and exposure to board-level decisions. Without this advance preparation, you face pressure to accept poor terms or hand the business to someone unprepared for the role.

Once you receive proceeds from the sale, most business owners make a critical mistake: they park the money in a standard brokerage account and hope it grows. That approach wastes substantial tax advantages available to you in the years immediately following a sale. Consider a diversified portfolio that accounts for inflation, which historically runs 2-3 percent annually and erodes purchasing power significantly over a 30-year retirement.

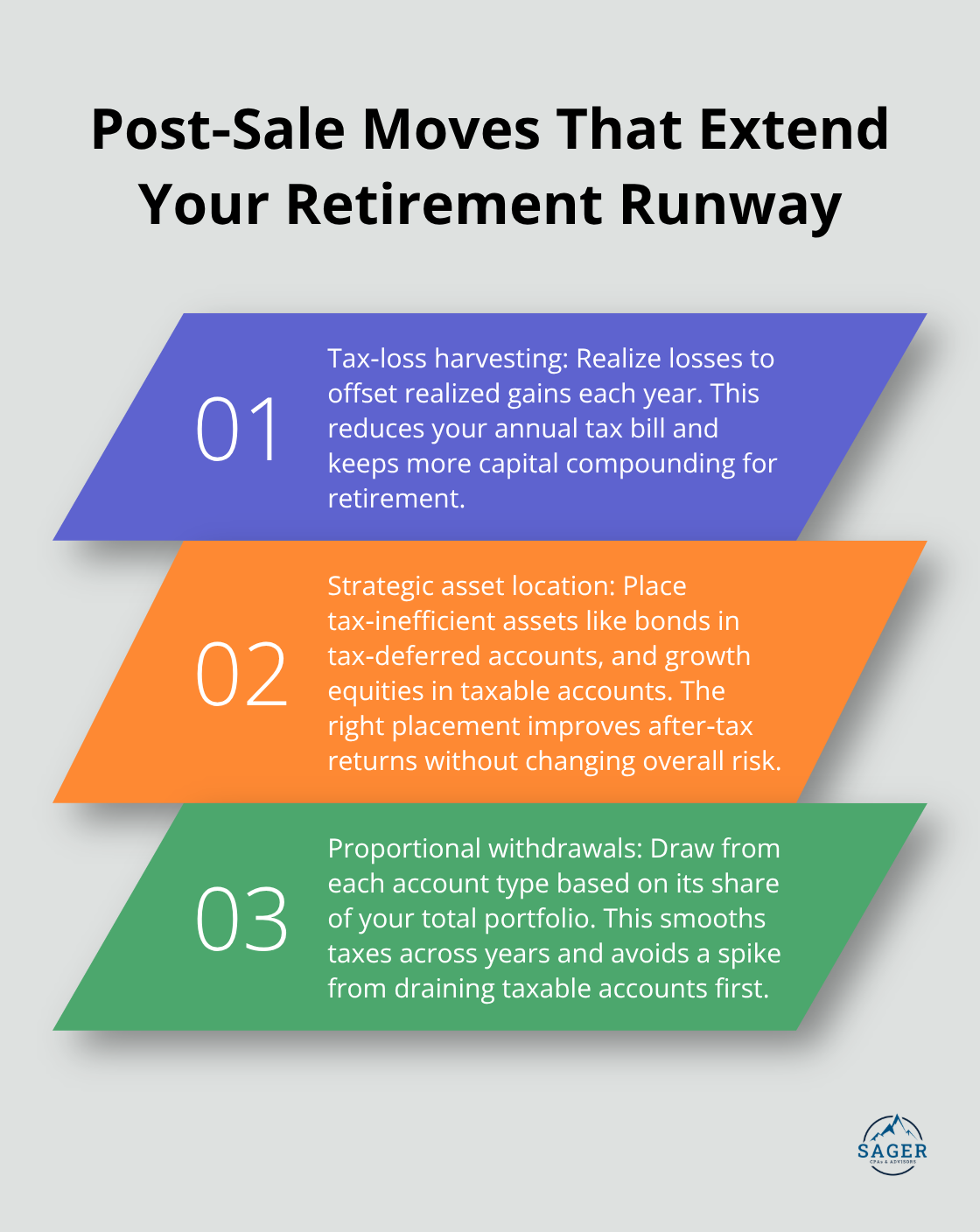

Tax-loss harvesting in your investment accounts offsets capital gains and reduces your annual tax bill. Strategic asset location, where you hold tax-inefficient investments like bonds in tax-deferred accounts and growth stocks in taxable accounts, improves your after-tax returns. A proportional withdrawal strategy that takes money from each account type in line with your overall balances creates a predictable tax burden each year, rather than the spike you’d face from draining taxable accounts first. These aren’t theoretical optimizations; they directly impact how long your money lasts. A business owner receiving $3 million in sale proceeds who manages withdrawals and asset location effectively can extend their retirement runway by years compared to someone using a reactive approach.

If philanthropy matters to you, structure your giving strategy around your sale timing, not as an afterthought. Donor-advised funds let you make a large tax deduction in the year of the sale when your income is highest, then distribute the money to charities over the following years at whatever pace you choose. This approach captures the full deduction upfront without forcing you to commit specific amounts to specific charities immediately.

If you hold appreciated assets like business equity, donate those assets directly to charity and avoid capital gains tax entirely while generating a charitable deduction based on the full fair market value. For owners over 70½, qualified charitable distributions from IRAs satisfy your required minimum distributions without counting as taxable income, which is especially valuable if you don’t need the RMD for living expenses. These strategies work together: you can structure a charitable remainder trust before the sale to transfer business interests and manage capital gains, then use donor-advised funds after the sale to distribute the remainder of your proceeds to causes you care about. The result is substantial tax savings combined with meaningful philanthropic impact.

Business owner retirement planning demands a fundamentally different approach than standard employee strategies because your business represents the majority of your net worth. The decisions you make about sale timing, asset versus stock structure, and post-sale deployment of proceeds directly impact the money available to you for the next 30 years. Start by assessing your current situation honestly and determine whether you want to sell outright, transfer the business to family or employees, or gradually wind down operations.

Engage professionals who understand business exits, not just general financial planning, and have your accountant, attorney, and wealth advisor work together on tax structure, entity decisions, and post-sale investment strategy. The gap between reactive and planned exits often amounts to hundreds of thousands of dollars in preserved wealth, and strategies like installment sales, charitable giving, and tax-loss harvesting form core components of a serious exit plan. If you’re considering a family or employee transition, start succession planning now even if your exit is years away, and if you’re selling to an outside buyer, document your systems and gather three years of clean financial records to command the highest valuation.

We at Sager CPA help business owners navigate these decisions with customized tax planning and strategic advisory services tailored to your situation. Schedule a consultation with us to create a personalized exit strategy that aligns with your financial goals and legacy vision.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.