Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Corporate tax planning strategies can make or break a company’s financial health. At Sager CPA, we’ve seen firsthand how effective tax planning can significantly impact a business’s bottom line.

In this post, we’ll explore key strategies for successful corporate tax planning, common pitfalls to avoid, and the long-term benefits of implementing a solid tax strategy. Whether you’re a small business owner or a large corporation, these insights will help you navigate the complex world of corporate taxation.

Corporate tax planning is a strategic approach to manage a company’s financial affairs. It aims to minimize tax liabilities while ensuring compliance with tax laws. This process aligns short-term tax savings with long-term business goals.

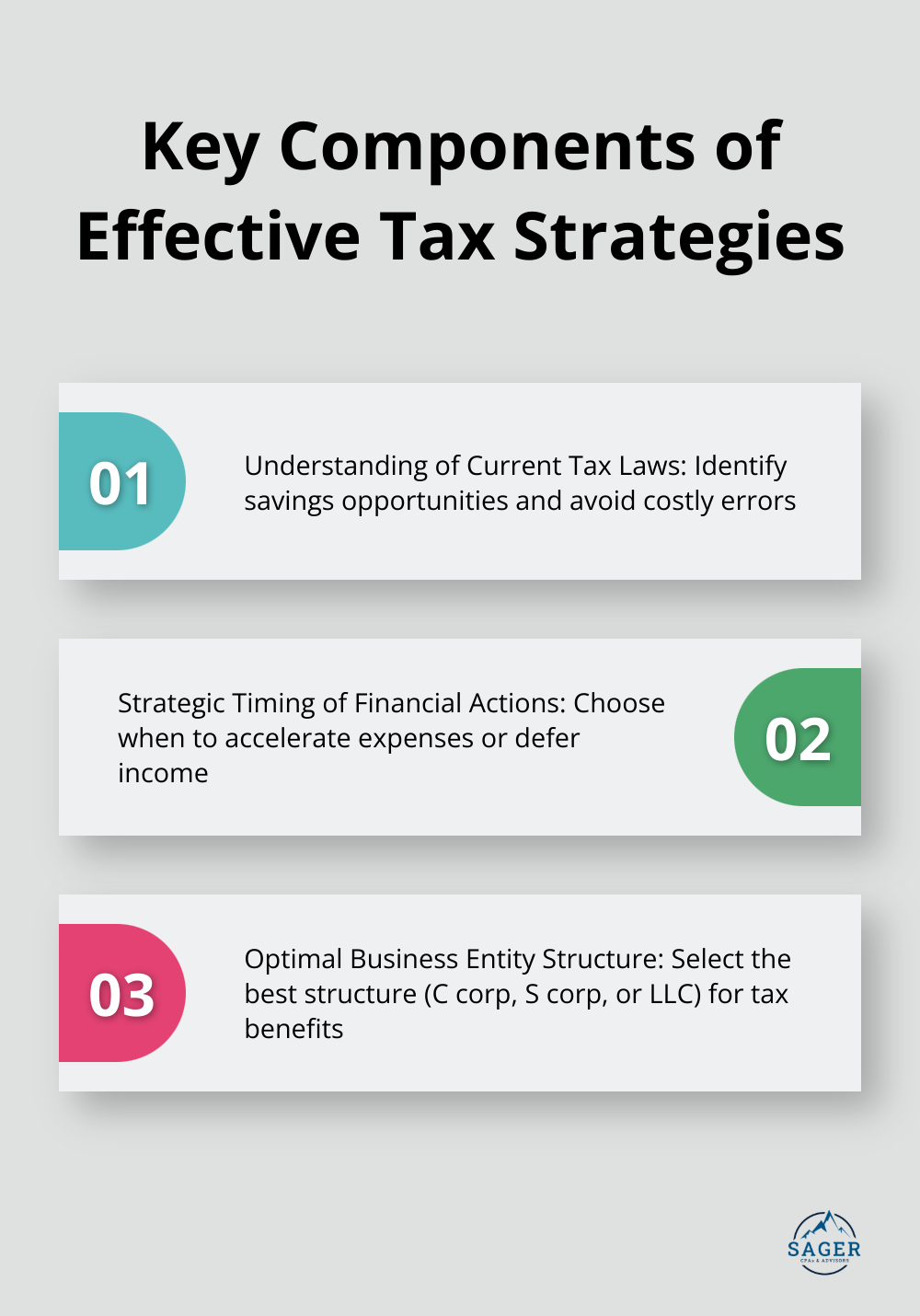

Successful corporate tax planning relies on several essential elements:

Proactive tax planning offers numerous advantages for businesses:

The tax landscape constantly evolves. The Tax Cuts and Jobs Act of 2017 brought significant changes to corporate taxation, and more changes are likely in the future. Companies that take a proactive approach to tax planning are better positioned to adapt to these changes and capitalize on new opportunities.

As we move forward, let’s explore specific strategies that can help businesses maximize their tax efficiency and achieve long-term financial success.

Corporate tax planning extends beyond minimizing tax liabilities; it involves creating a comprehensive strategy that aligns with business goals. Here are key approaches to optimize your tax strategy:

Businesses can reduce their tax burden by fully utilizing available tax credits and deductions. Discover 25+ small business tax deductions to maximize savings in 2025. Find tips, strategies, and best practices to reduce your tax bill. The Research and Development (R&D) Tax Credit offers substantial savings for companies that invest in innovation. Energy-efficient upgrades also lead to significant tax savings through various government incentives. Companies should conduct a thorough review of all potential deductions, from equipment depreciation to employee benefit programs, to minimize their tax burden.

Your business structure significantly impacts your tax obligations. S corporations help owners avoid double taxation on corporate income. C corporations might benefit businesses expecting high growth, as they’re subject to a flat 21% tax rate. Limited Liability Companies (LLCs) offer flexibility in taxation, allowing members to choose their preferred tax treatment. Regular reviews of your business structure ensure it continues to align with your financial goals.

The timing of income recognition and expense incurrence can significantly impact your tax liability. If you expect to be in a lower tax bracket next year, it might benefit you to defer income to that year. Conversely, if you’re experiencing a high-income year, accelerating deductible expenses into the current year can help offset your tax burden.

Tax-advantaged accounts serve as powerful tools for reducing overall tax liability. Setting up a 401(k) plan for your employees not only provides them with valuable benefits but also offers tax advantages for your business. Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs) can provide tax benefits while helping manage healthcare costs.

Tax laws constantly evolve, and staying informed about these changes is essential for effective tax planning. The Tax Cuts and Jobs Act of 2017 brought significant changes to corporate taxation, and more changes are likely in the future. Companies that take a proactive approach to tax planning (by staying informed and adapting quickly) position themselves to capitalize on new opportunities and avoid potential pitfalls.

As we move forward, let’s explore common challenges businesses face in corporate tax planning and how to overcome them effectively.

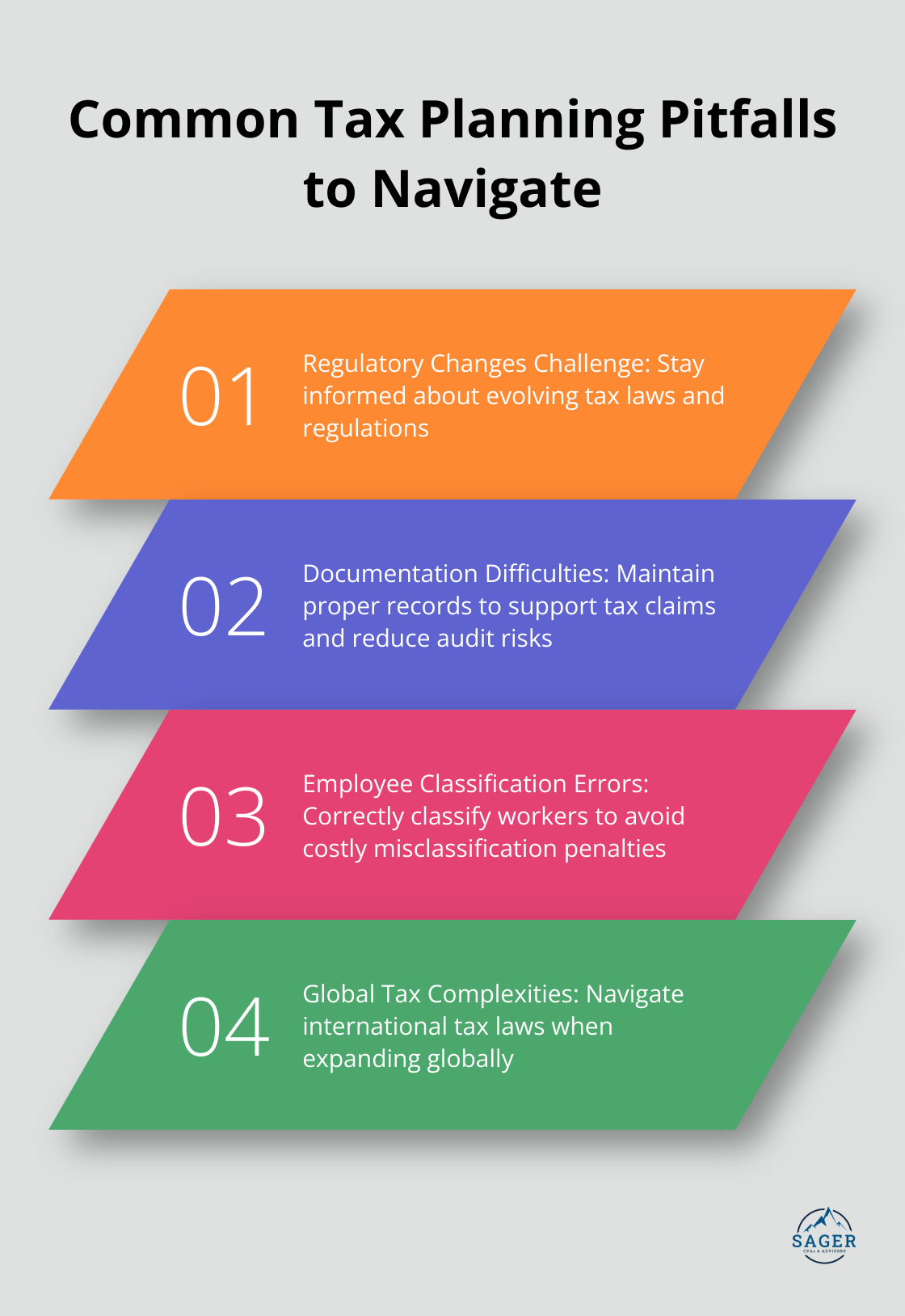

Corporate tax planning requires attention to detail and understanding of tax laws. The constant flux of regulations presents a significant challenge. The Tax Cuts and Jobs Act of 2017 introduced sweeping changes to corporate taxation, and many businesses still adapt to its implications. Non-compliance with new rules can result in missed deductions or tax overpayments.

To address this challenge, businesses should create a system to monitor tax law updates. This system might include tax law bulletin subscriptions, industry conference attendance, or partnerships with tax professionals who provide timely updates. Quarterly tax planning meetings help ensure strategy alignment with current regulations.

Proper documentation forms the foundation of effective tax planning and compliance. Many businesses fail to maintain adequate records throughout the year. This oversight can cause problems during tax preparation and increase audit risks. The IRS demands thorough documentation to support claimed deductions, credits, and income reporting.

To overcome this challenge, businesses should implement a robust record-keeping system. Accounting software can categorize expenses automatically and store digital copies of receipts. Clear protocols for employee expense reports and logs for business use of vehicles or home offices should be established. In the event of an audit, the taxpayer bears the burden of proof.

Misclassification of workers as independent contractors instead of employees is a common and expensive mistake. This error can result in significant tax liabilities (including back taxes, penalties, and interest). The IRS uses specific criteria to determine worker status, and misclassification consequences can be severe.

To avoid this pitfall, businesses should review the IRS guidelines on worker classification carefully. Factors to consider include the degree of control over the worker, the permanency of the relationship, and the worker’s financial investment in their tools or equipment. When in doubt, businesses should seek professional guidance. Regular workforce audits can help identify and correct misclassifications before they become problematic.

As businesses expand internationally, they often underestimate global taxation complexities. Each country has unique tax laws, and navigation can be challenging. Issues such as transfer pricing, permanent establishment rules, and double taxation agreements require specialized knowledge.

To address international tax considerations, businesses should research the tax implications of operating in specific countries thoroughly. Engagement of local tax experts in each jurisdiction of operation can be beneficial. Development of a comprehensive global tax strategy that accounts for the interplay between different tax systems can help maximize international profit potential while ensuring compliance with local regulations.

Corporate tax planning strategies are essential for businesses to optimize their financial performance and ensure long-term success. Companies can significantly reduce their tax burden while remaining compliant with ever-changing regulations through strategic approaches. However, navigating the complex landscape of corporate taxation requires expertise and vigilance to avoid costly mistakes and missed opportunities.

At Sager CPA, we offer expert financial management and tax planning services tailored for individuals and businesses. Our team provides precise accounting, strategic advisory services, and comprehensive tax planning to reduce liabilities and enhance financial clarity. We work closely with our clients to develop proactive strategies and customized action plans that align with their specific business goals and objectives.

Effective corporate tax planning strategies yield substantial long-term benefits beyond immediate tax savings. They improve cash flow management, support broader business objectives, and position companies to adapt quickly to regulatory changes. A well-executed tax strategy can free up resources for innovation, expansion, and investment in growth opportunities (which is crucial for long-term success).

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.