Pension Planning for Business Owners: Secure Your Later Years

Create a secure retirement as a business owner with effective pension planning strategies and tax-advantaged account options.

Investment taxes can reduce your portfolio returns by 20-30% annually if not managed properly. Most investors lose thousands of dollars each year to preventable tax inefficiencies.

We at Sager CPA see clients implement tax-efficient investment strategies that save them significant money. The right approach can add substantial value to your long-term wealth building.

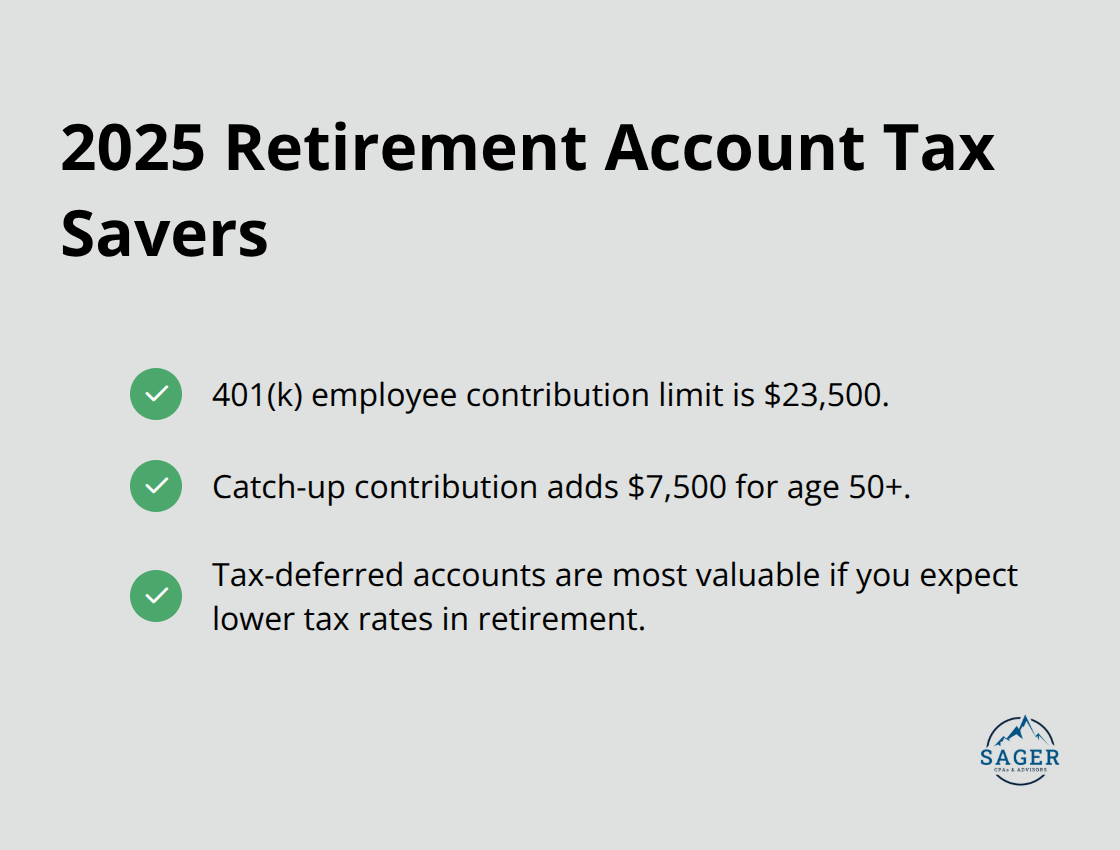

Tax-deferred accounts like 401(k)s and traditional IRAs reduce your current tax burden while investments grow without annual tax drag. The 2025 contribution limits allow $23,500 annually in 401(k)s, with catch-up contributions up to $7,500 for those 50 or older. These accounts work best when you expect lower tax rates in retirement.

Tax-free Roth accounts operate differently – you pay taxes upfront but enjoy tax-free growth and withdrawals. Roth IRAs benefit high earners who anticipate higher future tax rates, though income limits restrict direct contributions for individuals who earn over $153,000.

Asset location matters more than most investors realize. Municipal bonds belong in taxable accounts since their tax-free income provides no additional benefit in tax-sheltered accounts. Index funds and buy-and-hold stocks work efficiently in taxable accounts due to minimal distributions and favorable capital gains treatment.

Actively managed funds that generate frequent taxable events should occupy tax-deferred spaces. High-growth stocks and REITs perform best in Roth accounts where unlimited appreciation remains tax-free forever.

Long-term capital gains face lower rates compared to ordinary income rates. Federal income tax has seven tax rates in 2025: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. This difference makes hold periods critical for tax efficiency, as long-term capital gains receive preferential treatment versus short-term gains taxed as ordinary income.

Tax-loss harvest allows you to offset gains with losses plus deduct $3,000 annually against ordinary income. The wash-sale rule prevents you from claim losses on substantially identical securities purchased within 30 days (make careful time essential for effective tax management).

Health Savings Accounts (HSAs) provide triple tax benefits – deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. These accounts beat even Roth IRAs for tax efficiency when used properly.

529 education plans offer tax-free growth for qualified education expenses, and many states provide additional tax deductions for contributions. These strategies form the foundation for the specific investment techniques we’ll explore next.

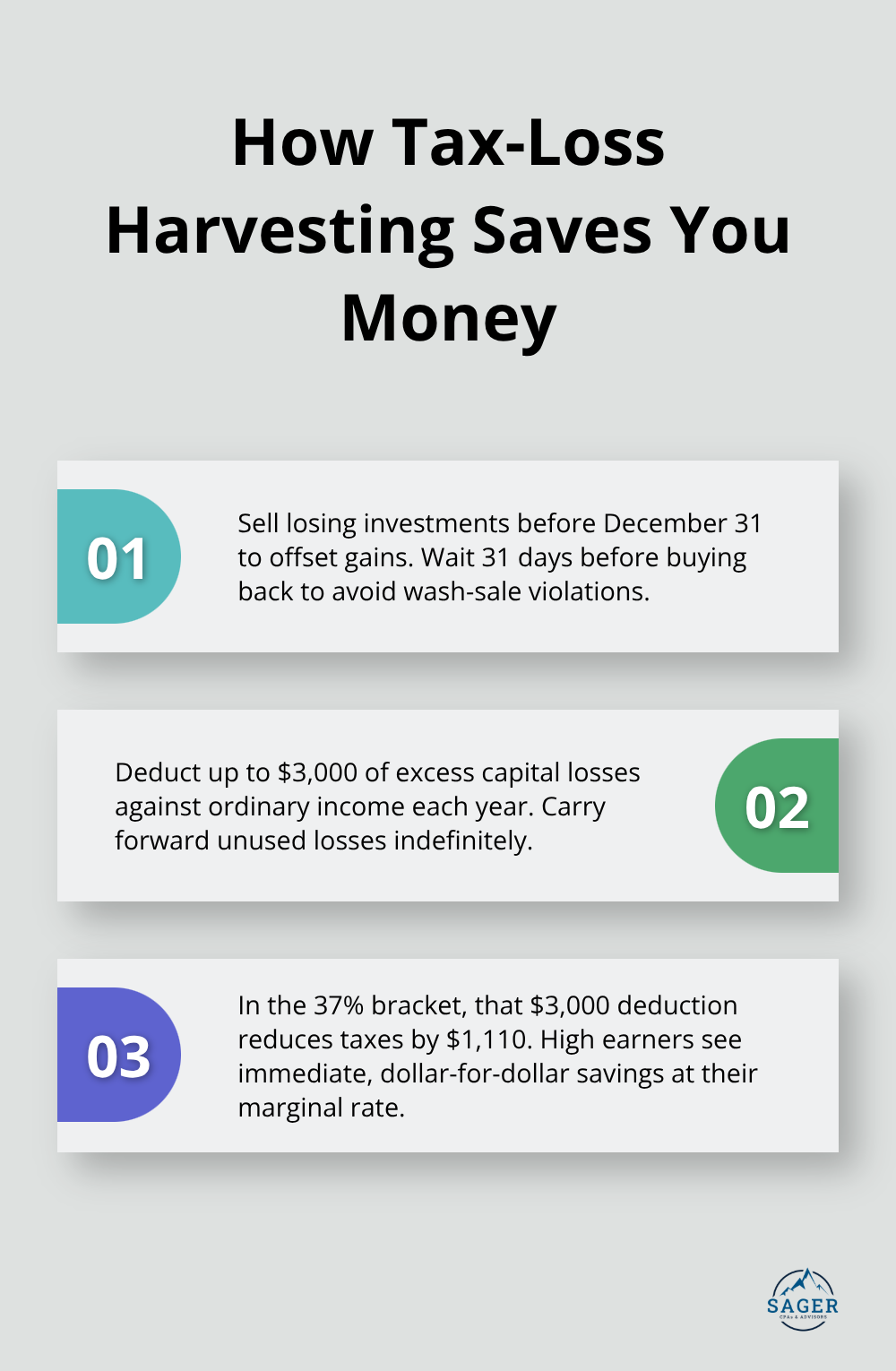

Tax-loss harvesting delivers immediate tax savings when you execute it correctly. Sell losing investments before December 31 to offset realized gains, then wait 31 days before repurchasing to avoid wash-sale violations. The IRS allows you to deduct up to $3,000 annually in excess losses against ordinary income, with unlimited carryforward for future years.

High-income investors in the 37% bracket can save $1,110 annually just from this $3,000 deduction.

Municipal bonds provide tax-free income that becomes increasingly valuable as your tax bracket rises. A 5% municipal bond yield equals 7.94% taxable equivalent yield for someone in the 37% bracket, which makes them superior to corporate bonds for high earners. Focus on bonds from your home state to avoid both federal and state taxes on interest income.

Max out employer 401k matches first since this provides instant 100% returns on your contribution. The 2025 limits of $23,500 plus $7,500 catch-up for those 50 and older create substantial tax savings. Someone in the 32% bracket saves $7,520 annually in current taxes with maximum contributions.

Backdoor Roth conversions work for high earners who exceed Roth IRA income limits. You contribute to traditional IRAs then convert immediately. This strategy requires no existing traditional IRA balances to avoid pro-rata tax complications. Convert traditional accounts to Roth during low-income years (like job transitions or early retirement) to pay taxes at reduced rates.

Index funds and ETFs generate fewer taxable distributions than actively managed funds due to lower turnover rates. Vanguard reports their index funds average 3% annual turnover versus 35% for actively managed funds, which creates significant tax differences. Place tax-inefficient assets like REITs and high-dividend stocks in tax-sheltered accounts where distributions avoid current taxation.

Target-date funds belong in 401k accounts rather than taxable accounts since their rebalancing creates unnecessary tax events when held outside retirement plans. These fund selection principles work hand-in-hand with proper timing strategies, but many investors make critical errors that can cost them thousands in unnecessary taxes.

December sales create the worst tax mistakes investors make. You trigger immediate capital gains taxes when you sell winners in December, while January sales defer tax liability by an entire year. The IRS requires payment on gains realized by December 31, which forces you to pay taxes months earlier than necessary. Smart investors sell losers before year-end for tax deductions and hold winners until January to delay tax payments. This difference can save thousands annually for high-income investors who face the 20% long-term capital gains rate plus the 3.8% net investment income tax.

You waste municipal bonds’ tax-free benefits completely when you place them in tax-deferred accounts. These bonds generate no additional value inside 401k accounts since the tax shelter provides no benefit for already tax-free income. High-dividend stocks and REITs belong in tax-sheltered accounts where their frequent distributions avoid annual taxation. Index funds work best in taxable accounts due to their tax-efficient structure and low turnover rates. Vanguard data shows actively managed funds distribute capital gains 6 times more frequently than index funds, which makes account placement decisions worth tens of thousands over decades. The step-up basis rule makes taxable accounts ideal for assets you plan to leave as inheritance, since heirs receive a reset cost basis that eliminates all capital gains taxes.

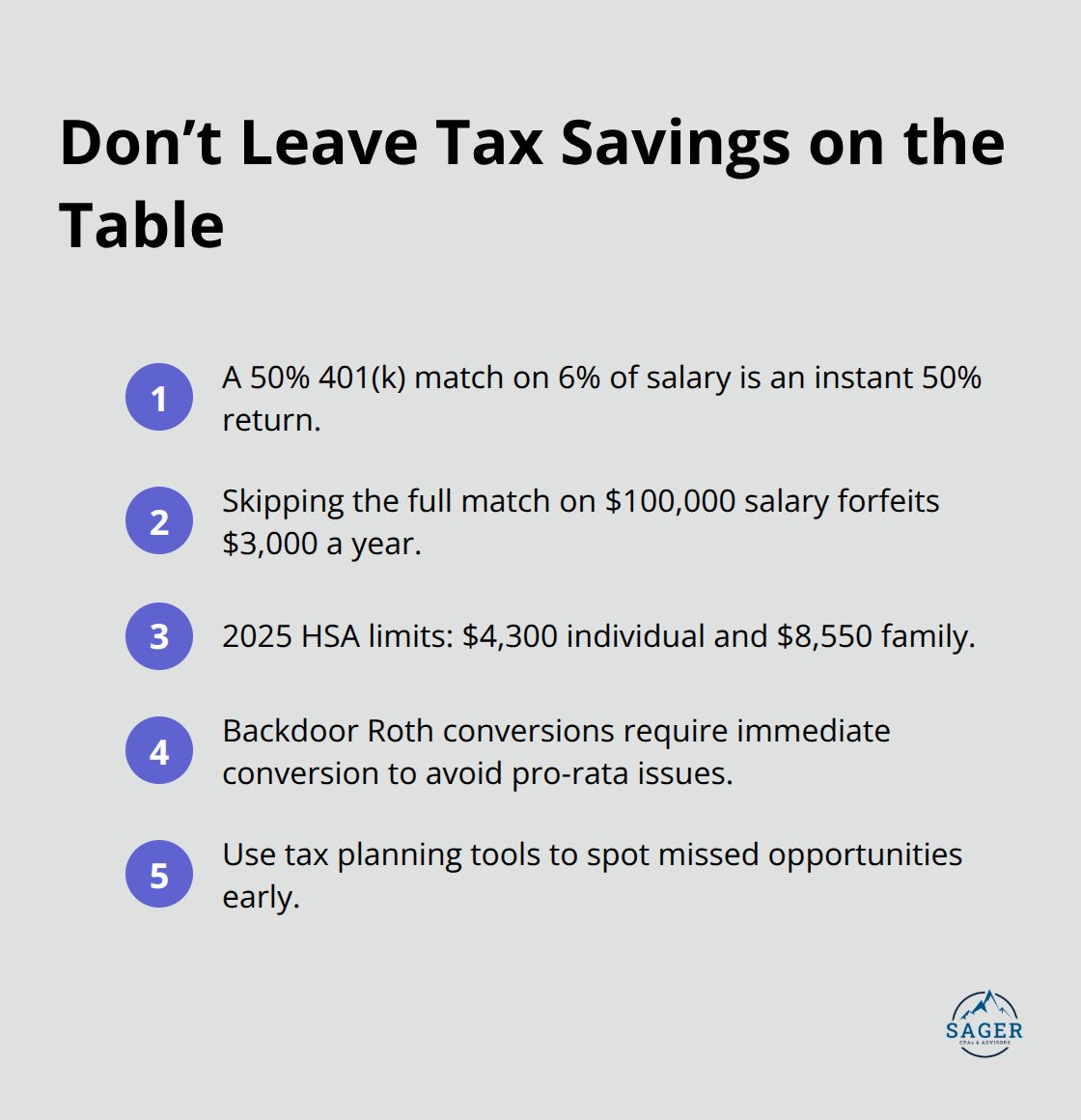

You make the costliest retirement error when you miss employer 401k matches. A typical 50% match on 6% of salary provides instant 50% returns that no investment strategy can replicate. Workers who earn $100,000 and skip the full match lose $3,000 in free money annually.

The 2025 HSA contribution limits of $4,300 for individuals and $8,550 for families create triple tax advantages that exceed even Roth IRA benefits. High earners who exceed Roth IRA income limits often miss backdoor Roth conversion opportunities that require immediate action after traditional IRA contributions to avoid pro-rata tax complications. Effective tax planning tools help identify these missed opportunities before they become costly oversights.

Tax-efficient investment strategies save you 20-30% annually on investment taxes when you implement them correctly. The most effective approaches combine maximum contributions to tax-advantaged accounts, strategic asset placement, and proper investment timing. Tax-loss harvesting provides immediate savings when you offset gains with losses, while municipal bonds deliver tax-free income for high earners in the 37% bracket.

Professional tax advice becomes essential as your investment portfolio grows and tax situations become more complex. We at Sager CPA help clients implement comprehensive strategies that reduce tax liabilities while they build long-term wealth. Our team creates customized action plans tailored to your specific financial situation.

Start optimization of your investment tax strategy today when you review your current account allocation and contribution limits. Consider whether your asset placement aligns with tax efficiency principles, and evaluate opportunities for tax-loss harvesting before year-end. Schedule a consultation with Sager CPA to develop a personalized strategy that maximizes your after-tax investment returns and supports your long-term financial goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.