Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Tax planning isn’t just about filing returns-it’s about strategically positioning your finances throughout the year. The benefits of tax planning extend far beyond April 15th, potentially saving thousands in unnecessary payments.

We at Sager CPA see clients miss significant opportunities simply because they wait too long to act. Smart tax planning requires year-round attention and the right strategies implemented at optimal times.

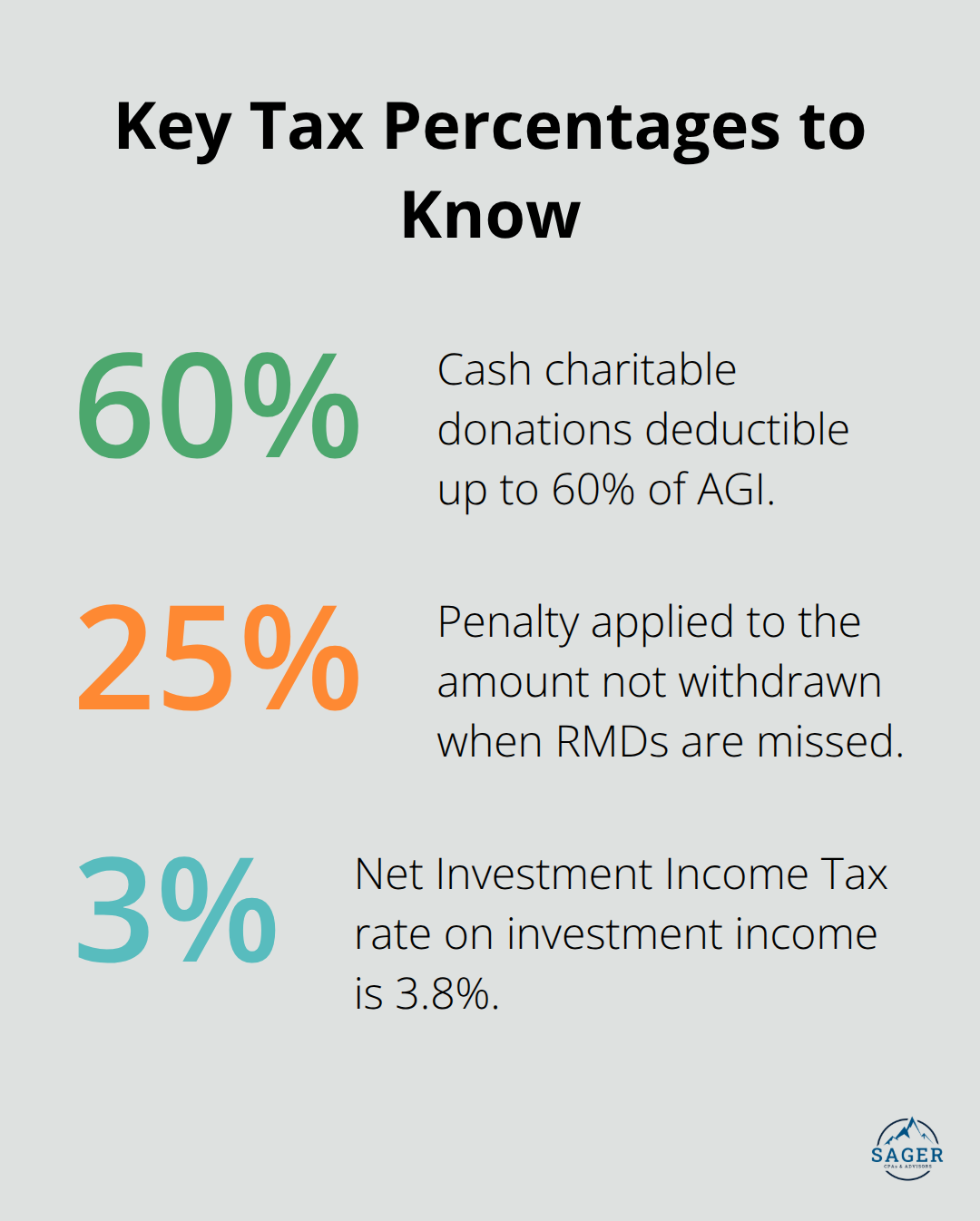

Tax planning succeeds when you apply three fundamental principles that separate successful taxpayers from those who overpay. The first principle maximizes deductions through strategic timing of deductions and expenses. The IRS allows taxpayers to deduct up to 60% of their adjusted gross income for cash charitable donations, yet most people donate randomly throughout the year instead of bunching donations to exceed the standard deduction of $15,750 for individuals in 2025.

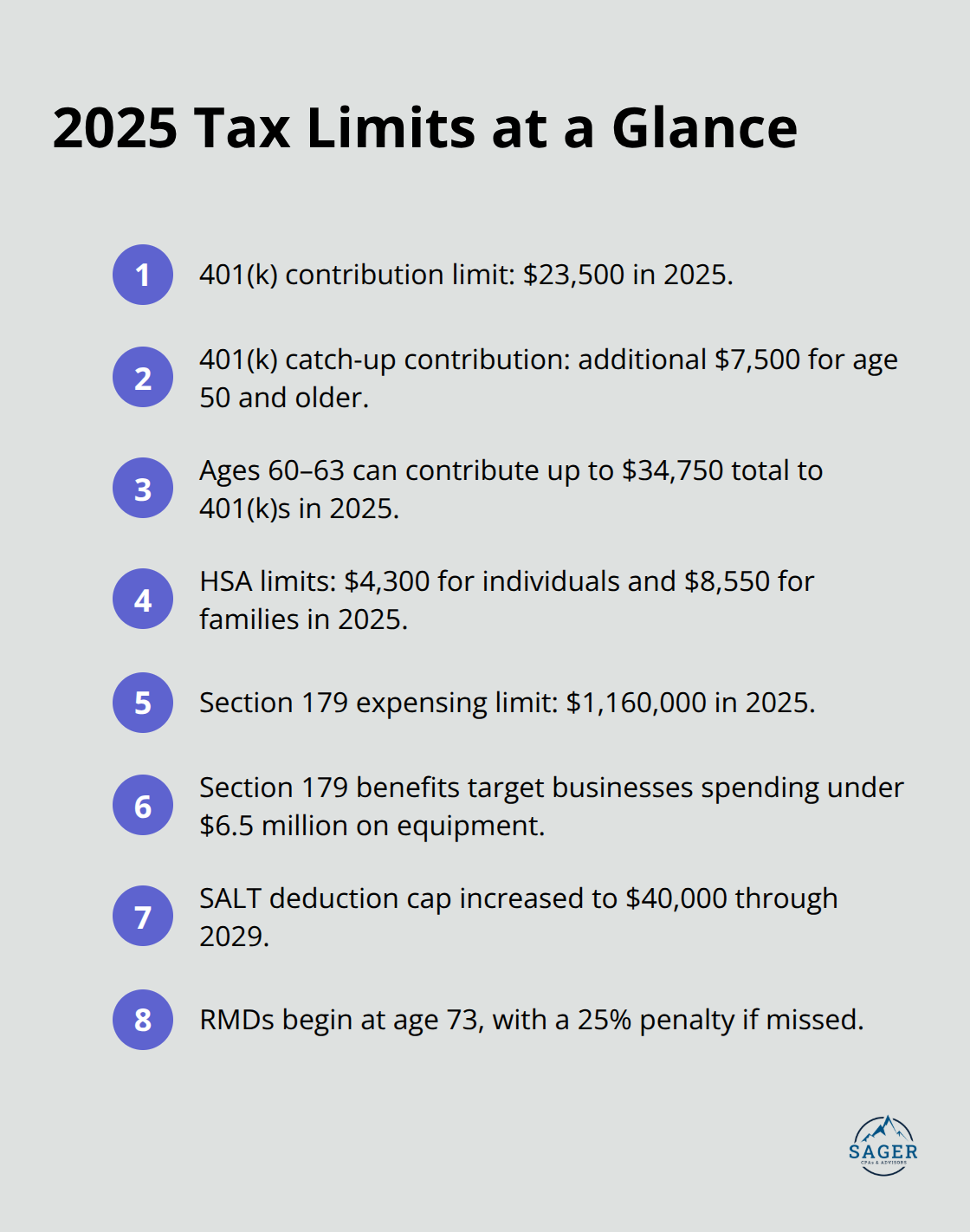

The second principle involves leveraging tax-advantaged accounts to their maximum potential. For 2025, you can contribute $23,500 to your 401k plus an additional $7,500 if you’re 50 or older, while individuals aged 60-63 can contribute up to $34,750 total through supersized catch-up contributions.

The third principle focuses on strategic income and expense timing. Tax-loss harvesting allows you to offset capital gains with investment losses, which reduces your overall tax burden while you maintain your investment portfolio. High earners should consider Roth conversions during lower-income years, as each conversion follows a separate five-year rule for withdrawals.

Health Savings Accounts provide triple tax benefits with contribution limits of $4,300 for individuals and $8,550 for families in 2025. The most effective tax planning happens in the final quarter of the year when you can still make adjustments. Required minimum distributions must begin at age 73, and missing these distributions triggers a 25% penalty on the amount not withdrawn (making compliance essential for retirement account holders).

These foundational principles create the framework for more sophisticated strategies that can dramatically reduce your tax burden.

The most aggressive tax reduction comes from maximum retirement contributions with strategic timing. Individuals aged 50 and older can contribute catch-up contributions of up to $7,500 to their 401k, which represents a significant tax deduction opportunity that most people miss. The backdoor Roth strategy works for high income earners who exceed Roth IRA income limits through after-tax dollar contributions to a traditional IRA with immediate conversion to avoid pro rata rule complications.

Roth conversions during low-income years beat the wait until retirement when RMDs force higher tax brackets. Each conversion follows its own five-year rule, so smaller amounts converted over multiple years provide more withdrawal flexibility than large single conversions. Traditional IRA contributions of $7,000 plus $1,000 catch-up for those 50 and older still provide immediate tax deductions.

S-Corp elections slash self-employment taxes for profitable businesses through income conversion from wages to distributions. The Tax Foundation reports that proper business structure selection can reduce overall tax burden by 15-25% annually for small business owners. Limited Liability Companies provide operational flexibility but lack the payroll tax savings of S-Corp status above $60,000 in annual profit.

Partnership structures work best for multi-owner businesses that seek pass-through taxation with basis step-up advantages. Section 179 deductions allow immediate expense recognition of $1,160,000 in equipment purchases for 2025, benefiting small and mid-size businesses that spend less than $6.5 million per year for equipment. Cash-basis accounting lets businesses defer income to December and accelerate deductible expenses.

Tax-loss harvesting offsets realized capital gains with investment losses to reduce your overall tax burden while you maintain your investment portfolio. The wash sale rule prevents loss claims if you buy substantially identical securities within 30 days before or after the sale. Investors can offset up to $3,000 in ordinary income annually with excess losses beyond capital gains.

Municipal bonds provide tax-free income that helps high earners avoid the Net Investment Income Tax of 3.8% on investment income. Appreciated securities donated to charity provide larger tax benefits than cash donations since the entire fair-market value qualifies for deduction (avoiding capital gains tax entirely). These advanced tax strategies require careful coordination to avoid common mistakes that can derail your entire tax plan.

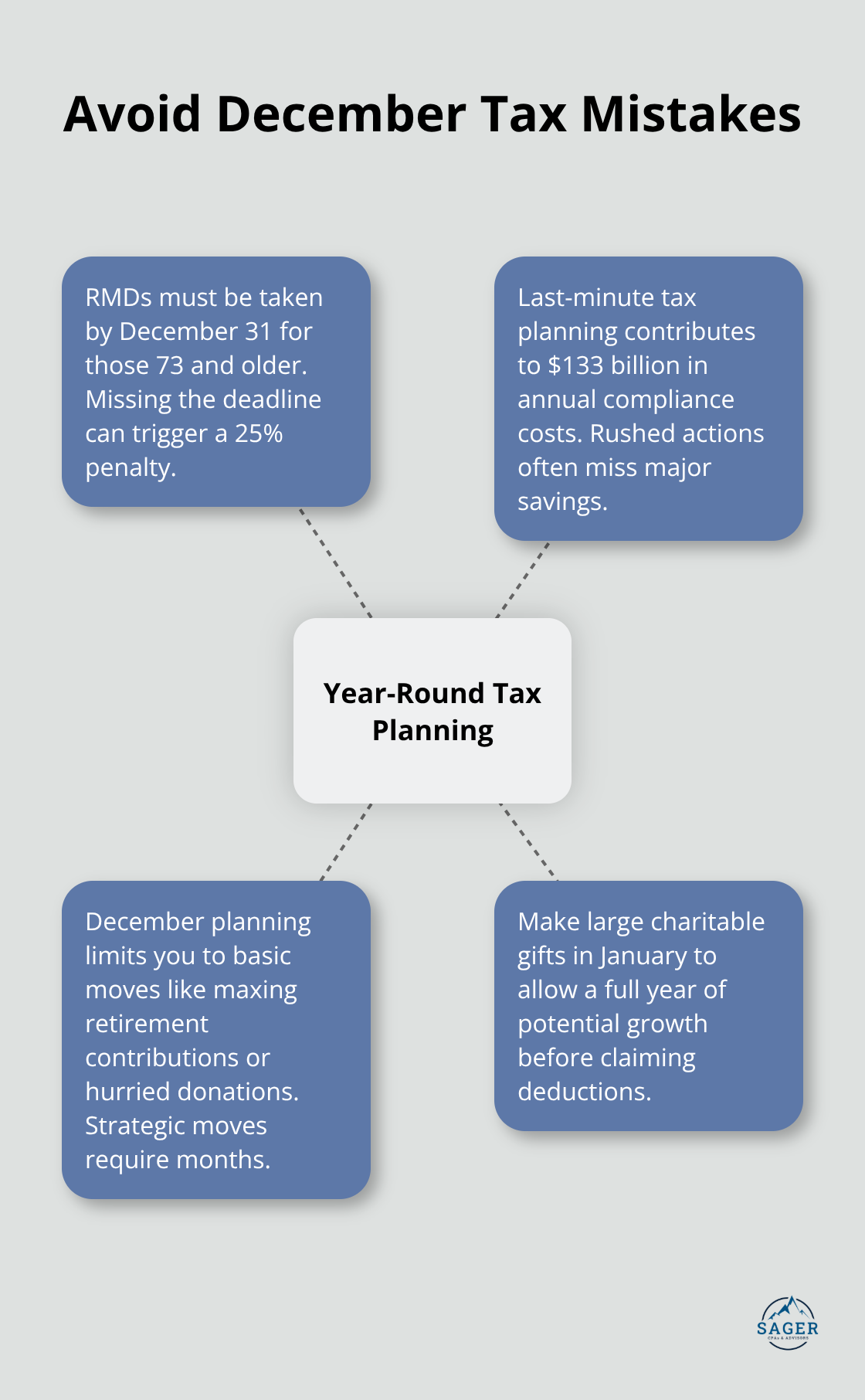

Most taxpayers lose thousands because they treat tax planning like a December fire drill instead of a year-round strategy. The Tax Foundation found that last-minute tax planning costs Americans $133 billion annually in compliance costs and missed opportunities. December planning limits your options to basic moves like retirement contribution maximization or rushed charitable donations, while strategic moves require months of preparation.

Required minimum distributions must start by December 31st for those 73 and older, but December delays create a 25% penalty risk if you miss the deadline. Smart taxpayers make their largest charitable donations in January to maximize the full year for investment growth before they claim deductions.

The average household leaves money in deductions unclaimed each year according to IRS statistics, primarily from overlooked business expenses and charitable contribution strategies. Appreciated securities donations provide larger tax benefits than cash donations since you deduct the full fair-market value while you avoid capital gains taxes entirely.

Health Savings Account contributions of $4,300 for individuals and $8,550 for families provide triple tax advantages that most people ignore completely. State and local tax deductions increased to $40,000 through 2029 under recent legislation, yet high earners in tax-heavy states still miss this opportunity (despite potential savings of thousands annually).

Marriage, divorce, job changes, and retirement trigger major tax implications that require immediate strategy updates, yet most people continue outdated approaches for years. A promotion that pushes income over Roth IRA limits of $153,000 for singles requires an immediate switch to backdoor Roth strategies.

Business owners who hit $60,000 in annual profit should elect S-Corp status to slash self-employment taxes, but many delay this decision and lose thousands. Each Roth conversion follows its own five-year rule, so major life changes that affect income levels require conversion timing recalculation to avoid penalties (making professional guidance essential for complex situations).

The benefits of tax planning extend far beyond simple compliance and create substantial wealth preservation opportunities for those who act strategically. Effective tax planning reduces your overall tax burden by 15-25% annually through retirement account optimization, strategic deduction timing, and proper business structure selection. Professional guidance becomes essential when you navigate complex strategies like Roth conversions, tax-loss harvesting, and business structure elections.

The Tax Foundation reports that Americans spend $133 billion annually on compliance costs, much of which stems from missed opportunities and last-minute mistakes. Most taxpayers lose thousands because they treat tax strategy like a December fire drill instead of a year-round approach. Smart tax moves require months of preparation and consistent attention throughout the tax year (not rushed decisions in the final weeks).

We at Sager CPA help clients maximize deductions while they avoid costly penalties through proactive strategies and customized action plans. Our approach focuses on year-round planning rather than December emergencies. Schedule a consultation with Sager CPA to create a personalized financial strategy that aligns with your specific situation and goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.