Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Tax planning is a powerful strategy for achieving financial success. At Sager CPA, we’ve seen firsthand how effective tax planning tools can significantly reduce tax liabilities and boost overall financial health.

This blog post will explore essential tax planning tools and strategies that can help you optimize your financial situation. We’ll cover everything from retirement accounts to business entity selection, providing practical advice to help you make informed decisions about your taxes.

Strategic tax planning is a holistic process of analyzing your business’s unique financial circumstances, goals, and tax liabilities to make the most tax-efficient decisions. It involves analyzing your financial situation and making decisions that will help you pay the least amount of taxes legally possible. This process extends beyond the annual tax return filing. It’s an ongoing strategy that requires foresight, knowledge of tax laws, and careful financial management.

Successful tax planning hinges on several crucial components:

Making strategic decisions about when to receive income or incur expenses can significantly impact your tax liability. For instance, deferring income to a future tax year or accelerating deductions into the current year can lower your taxable income for the present period.

While often confused, tax planning and tax preparation are distinct processes. Tax preparation is the act of filing your tax return, typically done annually. It’s a reactive process that deals with past financial activities.

Tax planning, on the other hand, is proactive. It’s about making decisions throughout the year that will positively impact your future tax situation. For example, contributing to a 401(k) or IRA can lower your taxable income for the year, a decision that needs to be made well before tax filing season.

Effective tax planning can lead to significant savings and improved financial outcomes. It’s not about evading taxes, but about using the tax code to your advantage within legal boundaries.

Tax planning should be integrated into your overall financial strategy. This integration allows you to make informed decisions that align with your financial goals and minimize your tax burden.

As we move forward, we’ll explore powerful tax planning tools and strategies that can help you optimize your financial situation. From retirement accounts to business strategy, these tools will provide practical ways to make informed decisions about your taxes.

Tax planning strategies can significantly impact your financial success. These strategies extend beyond basic tax preparation and can lead to substantial savings when implemented correctly.

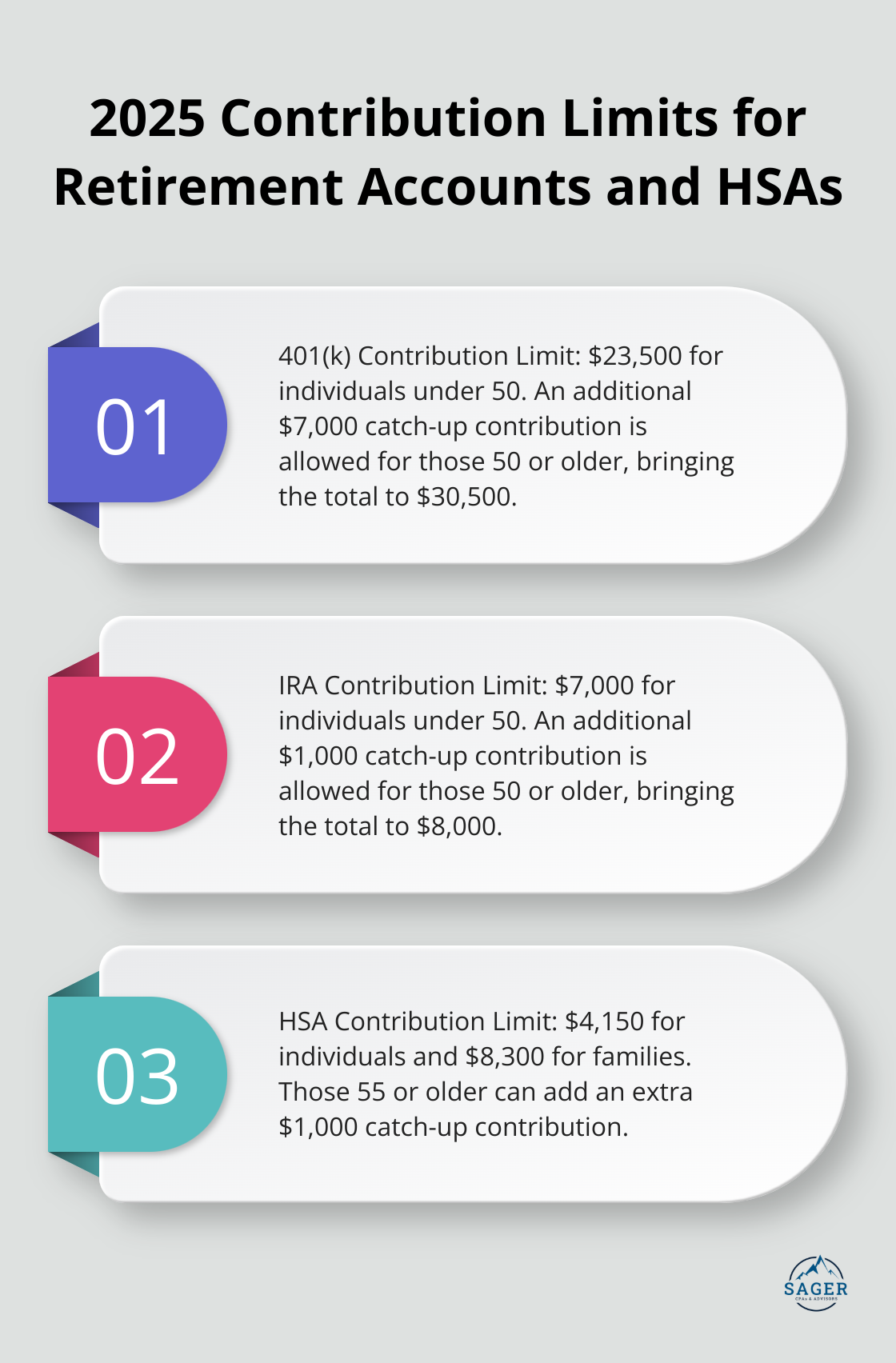

Retirement accounts serve as effective tax planning tools. Traditional 401(k)s and IRAs offer immediate tax benefits by reducing your taxable income in the contribution year. For 2025, you can contribute up to $23,500 to a 401(k), with an additional $7,000 catch-up contribution if you’re 50 or older. IRA contribution limits stand at $7,000, with a $1,000 catch-up allowance.

Roth accounts provide tax-free growth and withdrawals in retirement. While you make contributions with after-tax dollars, the long-term tax savings can be substantial, especially if you expect to be in a higher tax bracket in retirement.

Health Savings Accounts (HSAs) offer a triple tax advantage: contributions go into the HSA tax-free, and if you make contributions through payroll deductions, they are also not subject to Social Security or Medicare taxes. In 2025, individuals can contribute up to $4,150, and families can contribute up to $8,300. If you’re 55 or older, you can add an extra $1,000 catch-up contribution.

Tax-loss harvesting involves offsetting capital gains with capital losses, which can lower your tax bill and better position your portfolio going forward. This technique can help reduce your overall tax liability. For example, if you have $10,000 in capital gains and $8,000 in realized losses, you’ll only pay taxes on the net $2,000 gain. Any excess losses can carry forward to future years (up to $3,000 per year against ordinary income).

Charitable giving can serve as a powerful tax planning tool. Donor-advised funds (DAFs) allow you to make a large charitable contribution in one year for an immediate tax deduction, while spreading out the actual charitable gifts over time. This strategy can be particularly effective in high-income years.

Another option involves donating appreciated securities directly to charity. This approach allows you to avoid capital gains taxes on the appreciation while still claiming a deduction for the full market value of the securities.

For business owners, selecting the right business entity can have significant tax implications. S corporations, for instance, can provide tax advantages through the ability to split income between salary and distributions, potentially reducing self-employment taxes. However, the optimal choice depends on various factors, including your business’s specific circumstances and long-term goals.

These strategies require careful planning and expertise. While they can lead to substantial tax savings, it’s important to ensure they align with your overall financial goals and comply with current tax laws. The next section will explore how to maximize deductions and credits, further enhancing your tax planning efforts.

The decision between standard and itemized deductions can significantly impact your tax bill. For the 2025 tax year, the standard deduction stands at $14,600 for single filers and $29,200 for married couples filing jointly. However, itemizing might prove more beneficial if your qualifying expenses exceed these amounts.

Common itemized deductions include mortgage interest, state and local taxes (capped at $10,000), and charitable contributions. Medical expenses that surpass 7.5% of your adjusted gross income also qualify for deduction. Maintain detailed records of these expenses throughout the year to ensure you don’t miss out on potential savings.

Many taxpayers fail to take advantage of valuable deductions. Self-employed individuals can deduct health insurance premiums for themselves and their families. Educators may deduct up to $300 for unreimbursed classroom expenses. If you’ve relocated for a new job, certain moving expenses might qualify for deduction.

Investment-related deductions often go unnoticed. Investment advisory fees, safe deposit box fees, and subscriptions to financial publications can be deductible if they exceed 2% of your adjusted gross income.

Tax credits offer even greater value than deductions as they directly reduce your tax bill dollar-for-dollar. The Child Tax Credit provides significant benefits for families. You can claim this credit for each qualifying child who has a Social Security number that is valid for employment in the United States. The American Opportunity Tax Credit offers up to $2,500 per eligible student for college expenses.

Businesses can benefit from the R&D Tax Credit, which rewards companies investing in innovation. This credit is one of the most significant domestic tax credits remaining under current tax law.

Timing plays a key role in effective tax planning. If you’re close to the next tax bracket, consider deferring income to the following year. This strategy might involve delaying year-end bonuses or postponing the sale of appreciated assets.

Conversely, you can accelerate deductions into the current year. For example, you could make your January mortgage payment in December to claim the interest deduction in the current tax year. Similarly, bunching charitable donations in alternating years can help you exceed the standard deduction threshold and itemize in those years.

Tax laws change frequently, and strategies that work one year might not be optimal the next. Working with experienced professionals ensures you stay up-to-date with the latest tax laws and develop a personalized strategy to maximize your deductions and credits. This approach helps you keep more of your hard-earned money and achieve your financial goals.

Tax planning tools play a vital role in achieving financial success and minimizing tax liabilities. These strategies can significantly impact your financial well-being, from leveraging retirement accounts to implementing tax-loss harvesting. Your unique financial situation requires a personalized strategy, as what works for one individual or business may not be optimal for another.

Professional tax advisors provide invaluable expertise to ensure your tax planning strategy aligns with current laws and regulations. They help you navigate complex tax codes, identify savings opportunities, and avoid costly mistakes. Experienced professionals also offer ongoing support to adapt your strategy as your financial situation evolves.

We at Sager CPA specialize in providing expert financial management and tax planning services tailored to individuals and businesses. Our comprehensive approach includes precise accounting, strategic advisory services, and proactive tax planning (to reduce liabilities). We work closely with our clients to develop customized action plans, enhance financial clarity, and foster long-term financial stability and growth.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.