How to Develop an Effective Business Level Strategy

Develop a business level strategy that drives competitive advantage, boosts profitability, and positions your company for sustainable growth in your market.

High-income earners face a unique tax burden that most people never encounter. The difference between a generic tax approach and a strategic one can mean tens of thousands of dollars in your pocket each year.

At Sager CPA, we’ve helped countless high earners implement tax reduction strategies that actually work. Below, we’ll walk you through proven methods to lower your tax bill without taking unnecessary risks.

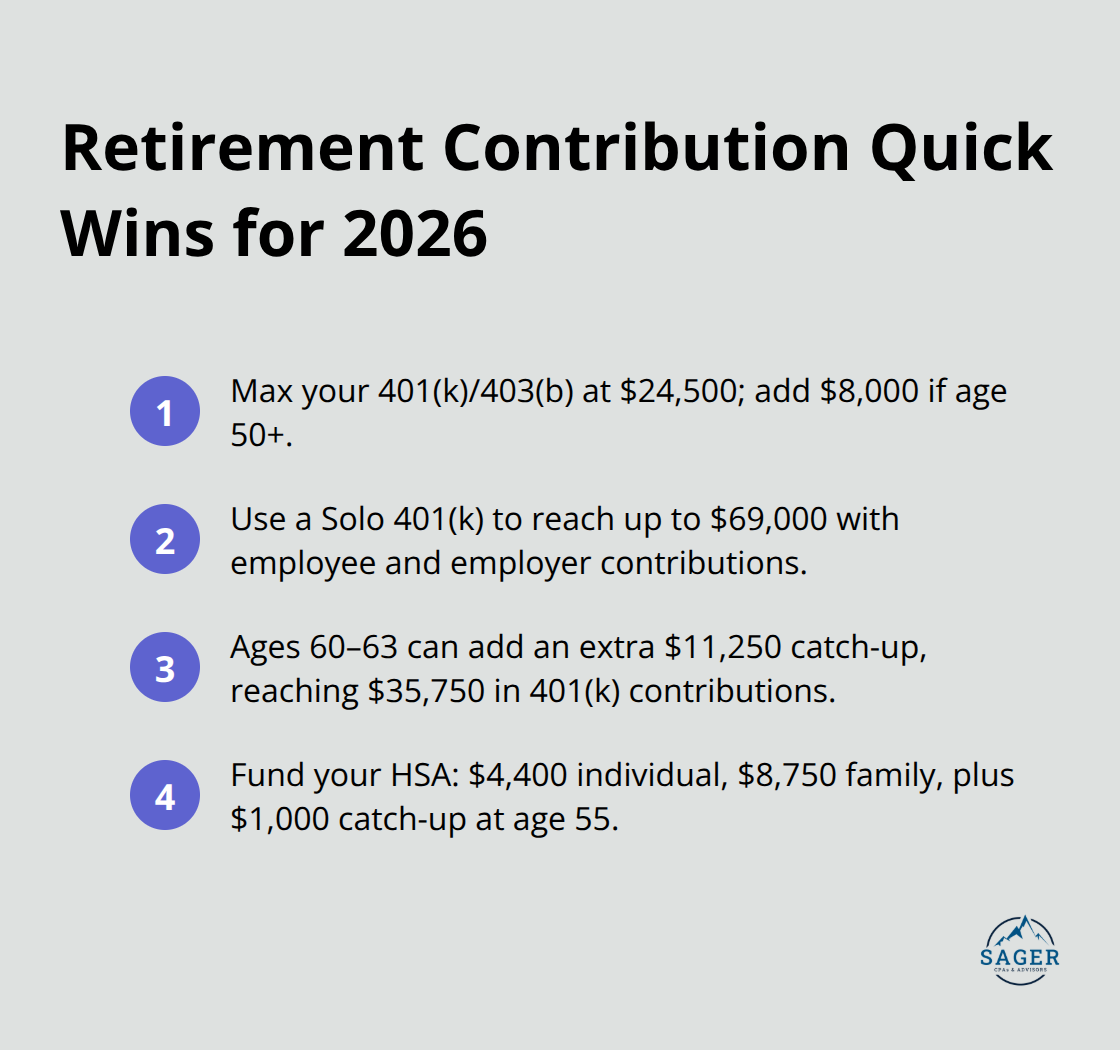

The 2026 contribution limits reveal where high earners should focus first. A 401(k) or 403(b) allows you to set aside $24,500 this year, and if you’re 50 or older, you add another $8,000 catch-up contribution-totaling $32,500 in pre-tax deductions for a single year. Self-employed individuals or business owners can use a Solo 401(k) to contribute both as an employee and employer, potentially reaching $69,000 total for 2026. These aren’t theoretical numbers. They represent concrete tax reductions that hit your return immediately.

The catch-up contributions for those ages 60 to 63 starting in 2026 allow an additional $11,250 on top of the standard $24,500 limit. If you fall into that window, you’re looking at $35,750 in 401(k) contributions alone. Most high earners miss these expanded opportunities because they assume their standard contribution covers their needs. It doesn’t.

For those with income over $153,000 as a single filer or $242,000 married filing jointly, direct Roth IRA contributions phase out entirely. A backdoor Roth conversions sidesteps that limit completely. You contribute $7,500 to a Traditional IRA and convert it to a Roth within days, regardless of income level. The conversion itself triggers taxes on any pre-tax IRA balance you hold, so this strategy works best when you have no existing Traditional IRAs.

Timing matters significantly with IRA contributions. Contributions to 401(k)s and Solo 401(k)s must be made by December 31 for that tax year, though employer contributions can sometimes extend until the business tax return deadline. IRA contributions have until April 15 of the following year, which gives you extra time to plan. If you expect your income to be lower in a particular year due to a business slowdown or sabbatical, that’s your window to execute backdoor Roth conversions at a lower tax cost.

Health Savings Accounts deserve far more attention than they typically receive. The 2026 limit is $4,400 for individual coverage and $8,750 for family coverage, plus a $1,000 catch-up at age 55. Unlike a 401(k), HSA funds never expire, they can be invested in the market, and withdrawals for qualified medical expenses remain completely tax-free. Most high earners treat HSAs as emergency savings vehicles rather than retirement accounts, which leaves thousands in tax benefits unused.

If you’re maximizing a 401(k), backdooring a Roth, and funding an HSA to the limit, you’ve reduced your taxable income by roughly $45,000 to $50,000 annually without touching business income or investment strategies. When you leave an employer, maximize your 401(k) contributions before you go-you won’t get that contribution room back. The gap between what you can contribute and what most people actually contribute represents your biggest, easiest tax reduction opportunity. Strategic tax planning decisions amplify these savings even further.

Your choice of business entity stands as one of the few tax decisions you cannot reverse easily, yet most high earners make it based on convenience rather than tax consequence. An S-corporation, LLC taxed as an S-corp, partnership, or sole proprietorship each produce wildly different tax outcomes. If you operate as a service provider earning $200,000 annually as a sole proprietor, you pay 15.3% self-employment tax on nearly all of that income. The same income through an S-corporation structure lets you split earnings into a reasonable W-2 salary and distributions taxed only as income, potentially saving $10,000 to $15,000 annually. That’s not theoretical-the IRS expects this strategy, and it’s fully legal when executed correctly.

The threshold where an S-corp makes sense typically sits around $60,000 to $80,000 in net business income, though the exact number depends on your specific situation and accounting costs. Many high earners wait years before making this switch, leaving six figures in cumulative tax savings on the table.

Cost segregation studies real estate and equipment by breaking down asset costs into components with shorter useful lives. A $500,000 commercial property might generate $10,000 in standard annual depreciation. A cost segregation study can identify $150,000 to $200,000 in assets that depreciate over five to seven years instead of 27.5 years, creating an immediate $30,000 to $40,000 deduction in year one. The study costs $3,000 to $5,000, making the ROI obvious in the first year alone.

Bonus depreciation phases down starting in 2026, dropping from 100% to 80% in 2026, then declining further to zero by 2030. If you own real estate, 2026 is your final year to maximize this benefit before it shrinks significantly.

Pass-through entity elections at the state level offer another lever for tax reduction. Some states allow S-corps and partnerships to elect to pay state income tax at the entity level rather than passing it through to owners. This election can improve federal deductibility of state taxes and reduce the impact of federal SALT caps that limit deductions to $40,000 for married couples. A high-earning owner in California or New York might recapture $5,000 to $10,000 in state tax benefits through this election alone.

These three strategies compound when you combine them. A business owner using the right entity structure, deploying cost segregation on real estate holdings, and leveraging state-level elections can reduce annual tax liability by $25,000 to $50,000 without changing underlying income or business operations. Your next opportunity lies in how you manage investment income and capital gains-a category where timing and strategy create outsized tax savings.

Investment income represents where most high earners leave substantial tax savings on the table. Unlike retirement contributions and business structure decisions that happen once, your investment approach determines your tax bill year after year. The difference between reactive investing and strategic tax-aware investing can easily reach $15,000 to $30,000 annually for someone with a $500,000 portfolio. Tax-loss harvesting alone can offset $3,000 of ordinary income per year, plus unlimited capital gains, which compounds significantly over a decade. High earners typically focus on investment returns and ignore tax drag, treating taxes as an afterthought rather than a central planning factor. That mindset costs you substantially.

Tax-loss harvesting works by intentionally selling securities at a loss to offset gains elsewhere in your portfolio or ordinary income. If you realized $40,000 in capital gains from selling appreciated stocks this year, you can harvest losses from underperforming positions to reduce that gain dollar-for-dollar. The math favors aggressive harvesting. A $10,000 loss eliminates $10,000 in capital gains, which would normally cost you $1,500 to $2,000 in federal taxes alone at the highest long-term capital gains rate of 20%, plus an additional 3.8% Net Investment Income Tax for high earners on gains over certain thresholds. The wash-sale rule prevents you from repurchasing the same security within 30 days before or after the sale, but you can immediately purchase a similar fund or security to maintain your market exposure. Most high earners never harvest losses because their advisors operate on commission and avoid portfolio activity, or they lack the discipline to track positions throughout the year. You should harvest losses systematically, particularly in November and December when year-end gains become clear.

Capital gains recognition timing involves deliberately choosing when to realize gains rather than letting them happen randomly. If you anticipate a lower-income year due to a sabbatical, a business slowdown, or early retirement, that year becomes your window to harvest gains at favorable rates. In 2026, the 0% long-term capital gains rate applies to married couples with taxable income up to roughly $96,700, meaning you can realize capital gains in that range completely tax-free. Most high earners never utilize this rate because they assume their income will always be high. A strategic year where you realize $50,000 in gains at the 0% rate saves you $7,500 to $10,000 compared to realizing those same gains in a high-income year. If you’re considering a business sale, executive transition, or other major life change, the timing of that event relative to your tax year matters enormously. Coordinate the sale closing date with your tax advisor rather than letting business timing drive tax consequences. This single decision often saves $20,000 to $50,000 on a major transaction.

Donor-Advised Funds offer the most tax-efficient charitable structure available to high earners. You contribute appreciated securities directly into a DAF, receive an immediate charitable deduction for the full fair market value, and avoid capital gains tax on the appreciation entirely. If you own $100,000 in appreciated stocks with a $60,000 cost basis, donating them through a DAF generates a $100,000 deduction while eliminating $40,000 in capital gains taxes that would otherwise cost $6,000 to $8,000 at the highest rates. You then distribute funds from the DAF to charities over multiple years, giving you time to decide where the money goes while the deduction locks in immediately. The IRS permits DAF contributions up to 30% of adjusted gross income for appreciated securities, with a five-year carryforward for excess amounts. High earners should fund DAFs in years with concentrated gains, significant bonuses, or business income spikes.

Qualified Charitable Distributions from IRAs work powerfully for those over 70 and one-half, allowing direct distributions to charities up to $108,000 annually that count toward required minimum distributions without triggering taxable income. This strategy specifically benefits retirees who need to take RMDs but don’t need the income. A $50,000 QCD eliminates $50,000 from your taxable income while satisfying your RMD obligation, potentially saving $10,000 to $15,000 in federal and state taxes combined. The distribution must transfer directly from your IRA custodian to the charitable organization-you cannot take the distribution yourself and then donate it. Request the QCD before year-end to ensure it processes in time for your current tax year.

The number 0% seems to be not appropriate for this chart. Please use a different chart type.

The tax reduction strategies for high-income earners outlined above represent your most direct path to keeping more of what you earn. Maximizing retirement contributions, structuring your business correctly, and managing investment income strategically can reduce your annual tax bill by $50,000 to $100,000 or more. These strategies compound year after year, creating substantial wealth preservation over a decade or longer.

What separates high earners who pay far too much in taxes from those who don’t comes down to one factor: intentional planning. Generic tax approaches treat your return as a compliance exercise, while strategic tax planning treats it as a financial opportunity. The difference shows up directly in your bank account, and every business structure, investment portfolio, and life circumstance creates different planning windows that you can exploit.

We at Sager CPA have worked with countless high earners to implement these strategies and customize them to their specific situations. Contact Sager CPA today to review your current tax situation and identify which strategies apply to you-the consultation itself often reveals opportunities you’ve overlooked, and the savings typically exceed the cost of professional guidance within the first year.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.