How to Reduce Your Tax Liability Legally

Reduce your tax liability legally with proven strategies. Discover deductions, credits, and planning techniques to lower your tax bill.

Smart investors pay an average of 2-3% less in taxes annually through strategic planning. Tax advantaged investment strategies can significantly boost your long-term wealth accumulation.

We at Sager CPA see clients increase their after-tax returns by 15-25% when they implement proper asset location and tax-loss harvesting techniques. The right approach transforms your investment portfolio into a tax-efficient wealth-building machine.

The IRS sets contribution limits for 2025 that create clear priorities for your tax strategy. Traditional and Roth IRAs allow $7,000 annually, plus $1,000 catch-up for those 50 and older. The key difference lies in tax treatment: traditional IRAs reduce your current taxable income, while Roth IRAs provide tax-free withdrawals in retirement.

Income limits restrict Roth IRA eligibility for high earners. However, backdoor Roth conversions allow wealthy investors to bypass these restrictions and access Roth benefits.

Your 401k deserves priority with its $23,500 annual limit for 2025 (plus $7,500 catch-up contributions for those 50+). Employer match programs deliver an immediate 100% return that no market investment can guarantee. Financial advisors recommend you contribute enough to capture the full match before you consider other investment options.

Traditional 401k contributions can drop you into lower tax brackets. This tax deferral strategy reduces your overall tax burden significantly and leaves more money in your pocket today.

Health Savings Accounts provide the best tax benefits available to investors. Contributions reduce taxable income, growth occurs tax-free, and withdrawals for qualified medical expenses remain untaxed. The 2025 contribution limits reach $4,300 for individuals and $8,550 for families.

After age 65, you can withdraw HSA funds penalty-free for any purpose (though non-medical withdrawals face ordinary income tax). This flexibility transforms HSAs into powerful retirement accounts that masquerade as healthcare tools.

Your current tax bracket determines which accounts offer maximum benefit. High earners in the 32% or 37% brackets should prioritize tax-advantaged accounts to reduce immediate tax liability. Lower earners often benefit more from Roth contributions, especially if they expect higher retirement income.

Tax bracket management becomes even more important when you consider how different withdrawal strategies affect your retirement tax situation.

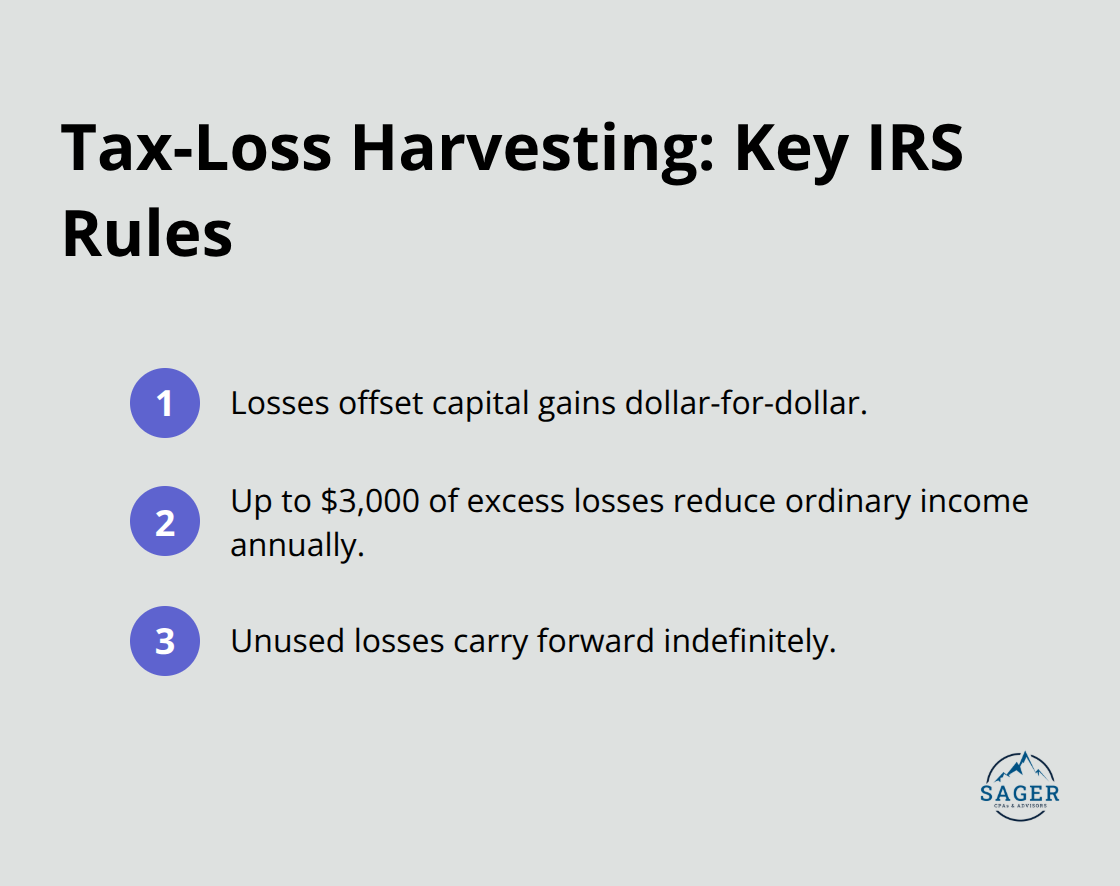

Tax-loss harvesting transforms portfolio declines into immediate tax benefits when you execute it correctly. The IRS allows you to offset capital gains with realized losses dollar-for-dollar, and excess losses can reduce ordinary income by up to $3,000 annually. Unused losses carry forward indefinitely, which creates future tax deductions that compound your savings over time.

December represents the optimal harvesting window because you control the exact timing of gains and losses within the tax year. Smart investors realize losses in declining positions while they simultaneously book gains in winners to balance their tax liability. The key lies in monitoring your net position throughout the year rather than waiting until year-end when your options become limited.

The IRS wash sale rule prohibits claiming losses if you repurchase the same security within 30 days before or after the sale. Violating this rule disallows your tax deduction and adds the loss to your cost basis instead (effectively deferring the benefit). Professional investors avoid this trap when they purchase similar but not identical securities during the waiting period. For example, selling an S&P 500 ETF and buying a total market index fund maintains market exposure while it preserves your tax benefit.

Harvesting allows precise control over your annual tax bracket when you manage when you realize gains and losses. High earners can offset large capital gains distributions from mutual funds when they harvest losses in individual stock positions. This strategy becomes particularly powerful when you can time realizations to keep income below key thresholds like the 3.8% net investment income tax (which applies to individuals with net investment income above applicable threshold amounts).

Strategic asset location works hand-in-hand with tax-loss harvesting to maximize your portfolio’s tax efficiency across different account types.

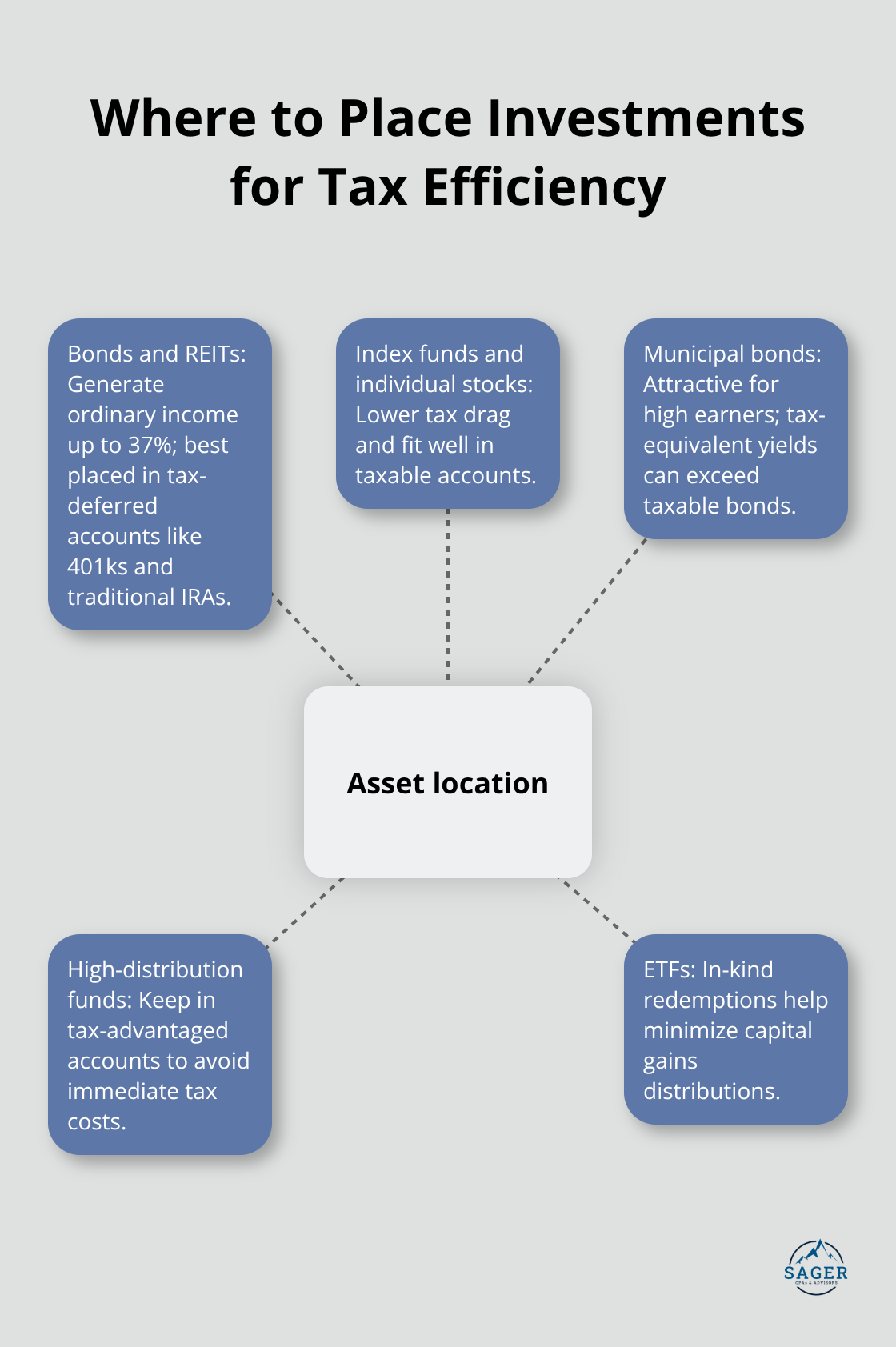

Asset location strategy determines which investments belong in taxable versus tax-advantaged accounts, and this decision impacts your portfolio returns more than most investors realize. Bond funds and REITs generate ordinary income taxed at rates up to 37%, which makes them perfect candidates for tax-deferred accounts like 401ks and traditional IRAs. Meanwhile, tax-efficient investments like index funds and individual stocks belong in taxable accounts where their lower tax burden won’t waste your tax shelter space. This strategic placement can boost your portfolio’s aftertax performance.

Investors in the 32% or 37% tax brackets should prioritize municipal bonds for their taxable accounts because the tax-equivalent yield often exceeds corporate bonds. A 4% municipal bond yield equals a 6.25% taxable yield for someone in the 37% bracket, plus you avoid the 3.8% net investment income tax on municipal interest. State-specific municipal bonds provide additional tax benefits when you live in high-tax states like California or New York (where combined federal and state rates can exceed 50%).

Broad market index funds and ETFs generate minimal taxable distributions, which makes them ideal for taxable accounts where you want to minimize annual tax drag. The Vanguard Total Stock Market ETF distributed just 1.23% in 2023, while actively managed funds averaged 3-5% distributions. ETFs provide superior tax efficiency because their structure allows in-kind redemptions that avoid capital gains triggers.

Dividend-focused funds and sector ETFs generate higher ordinary income that gets taxed at your marginal rate rather than the preferential capital gains rate. These investments belong in tax-advantaged accounts where the tax shelter protects you from immediate tax consequences. High-yield bond funds and REITs can destroy your after-tax returns when held in taxable accounts (especially for investors in higher tax brackets).

Tax-advantaged investment strategies require systematic implementation across multiple account types to maximize your wealth accumulation potential. The combination of proper asset location, strategic tax-loss harvesting, and optimal account selection can boost your after-tax returns by 15-25% over time. Success depends on understanding how different investments interact with various tax treatments.

Municipal bonds belong in taxable accounts for high earners, while bond funds and REITs perform better in tax-sheltered spaces. Index funds and ETFs provide the tax efficiency needed for taxable account growth. Professional guidance becomes essential as tax laws evolve and your financial situation changes (especially when managing complex portfolios across multiple account types).

The compound effect of tax savings over decades creates substantial wealth differences. We at Sager CPA help clients navigate complex tax decisions through customized strategies that align with individual goals. Schedule a consultation with Sager CPA to develop your personalized tax-efficient investment strategy.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.