Unlocking Business Advisory Insights for SMB Growth

Leverage business advisory insights to accelerate SMB growth, improve decision-making, and build a stronger competitive advantage in your market.

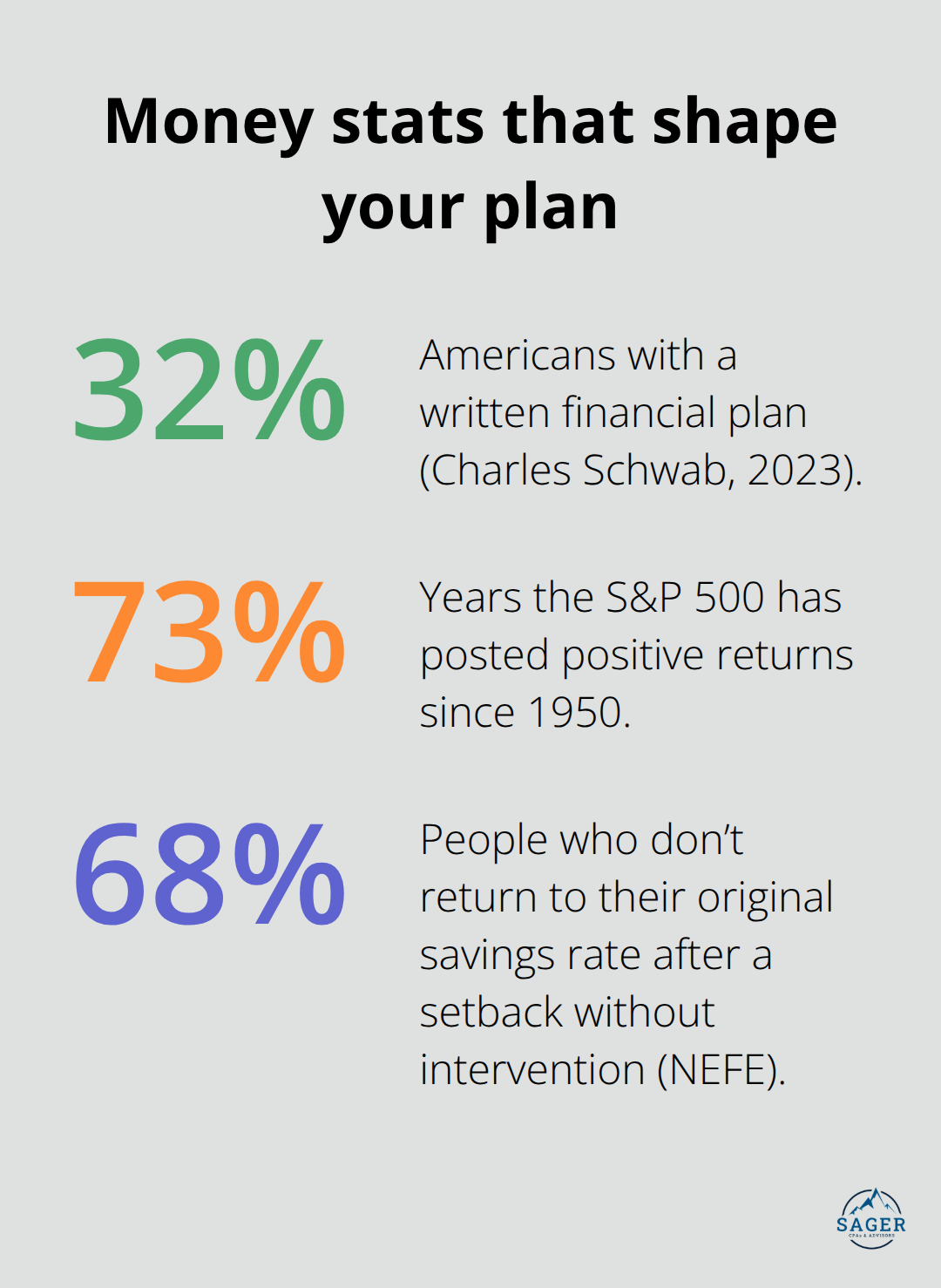

Most Americans struggle to turn their financial dreams into reality. Only 32% of people have a written financial plan, according to Charles Schwab’s 2023 Modern Wealth Survey.

We at Sager CPA see this challenge daily with our clients. The gap between setting financial goals and actually achieving them often comes down to having the right strategy and accountability system in place.

Financial goals fall into three distinct categories that require different strategies and timelines. Short-term objectives span one to three years and include emergency fund creation, high-interest credit card debt elimination, and specific purchase savings like car down payments. These goals need liquid savings accounts rather than investment vehicles.

Long-term objectives extend beyond five years and focus on retirement plans, homeownership, and wealth accumulation through diversified investment portfolios.

Financial experts recommend three to six months of living expenses in emergency savings, but we strongly advocate for the higher end of this range. Start by saving $1,000, then aim to save 3 to 6 months’ worth of essential expenses by funding your emergency savings, as you would for a bill. Prioritize $1,000 in emergency savings as your initial milestone, then build systematically. High-yield savings accounts currently offer rates between 4% and 5% (compared to traditional savings accounts that typically yield under 1%).

High-interest debt elimination should precede most investment activities. Credit card debt averages 21% interest rates according to Federal Reserve data and will always outpace typical investment returns. Focus on debts that exceed 7% interest rates first, then tackle lower-rate obligations. Student loans and mortgages often carry rates below 6%, which makes them lower priorities compared to investment portfolios that historically return 10% annually in stock markets.

Investment goals require specific time horizons to determine appropriate risk levels. Goals within five years demand conservative approaches that use bonds and CDs, while objectives that span decades benefit from aggressive stock allocations. The S&P 500 has delivered positive returns in 73% of all years since 1950, but short-term volatility makes stocks unsuitable for near-term needs. Retirement accounts like 401(k)s and IRAs offer tax advantages that compound wealth creation significantly over time.

Once you establish your financial priorities, the next step involves assessment of your current financial position and creation of a realistic roadmap to achieve these objectives.

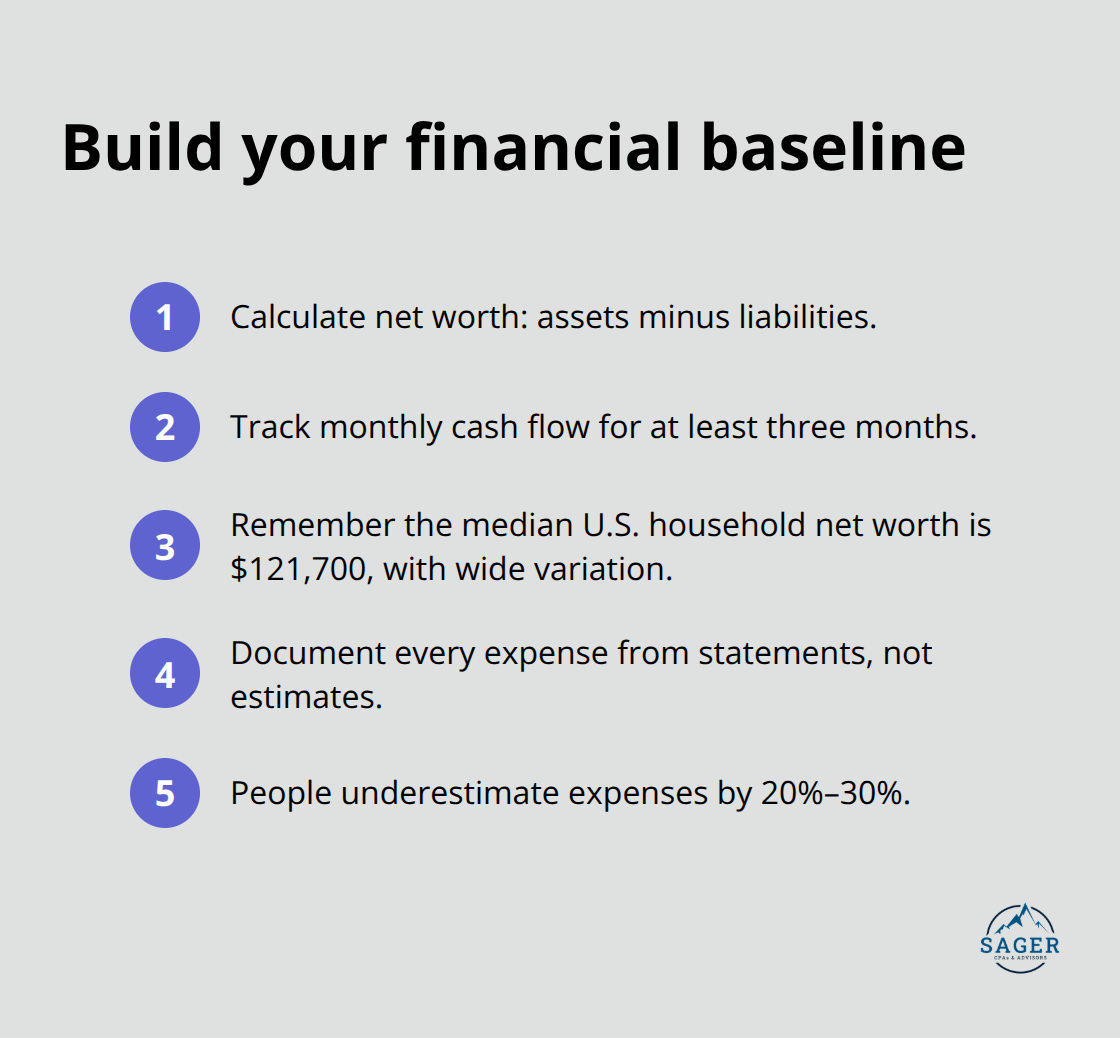

Financial plans without accurate baseline data lead to unrealistic expectations and inevitable failure. Start with a comprehensive net worth calculation that includes all assets minus liabilities, then track monthly cash flow for at least three months. The Federal Reserve’s 2022 Survey of Consumer Finances shows the median American household has a net worth of $121,700, but this figure masks significant variations by age and income level.

Document every expense category with bank statements and credit card records rather than estimates, as people typically underestimate expenses by 20% to 30% according to behavioral finance research.

Vague financial aspirations guarantee mediocre results. Transform general objectives into specific targets with measurable outcomes and fixed deadlines. Instead of retirement savings, commit to accumulate $500,000 by age 50 through monthly contributions of $1,847 (assumes 7% annual returns). Replace debt payoff plans with concrete strategies like elimination of $15,000 in credit card balances within 24 months through the debt avalanche method. The Consumer Financial Protection Bureau reports that people who write down specific financial goals are 42% more likely to achieve them compared to those who keep goals mentally. Set quarterly review dates to track progress and make necessary adjustments.

While the popular 50/30/20 framework allocates 50% of after-tax income to necessities, 30% to discretionary expenses, and 20% to savings, this approach requires modification based on individual circumstances. High-cost-of-living areas often demand 60% or more for housing, transportation, and essential expenses. Consumers are paying more for some of their largest expenses like housing, insurance, car payments, and utilities, according to Bank of America research. Focus on maximization of the savings percentage first, then work backward to optimize expense categories. Automate savings transfers immediately after payday to remove the temptation to spend available cash on non-essential purchases.

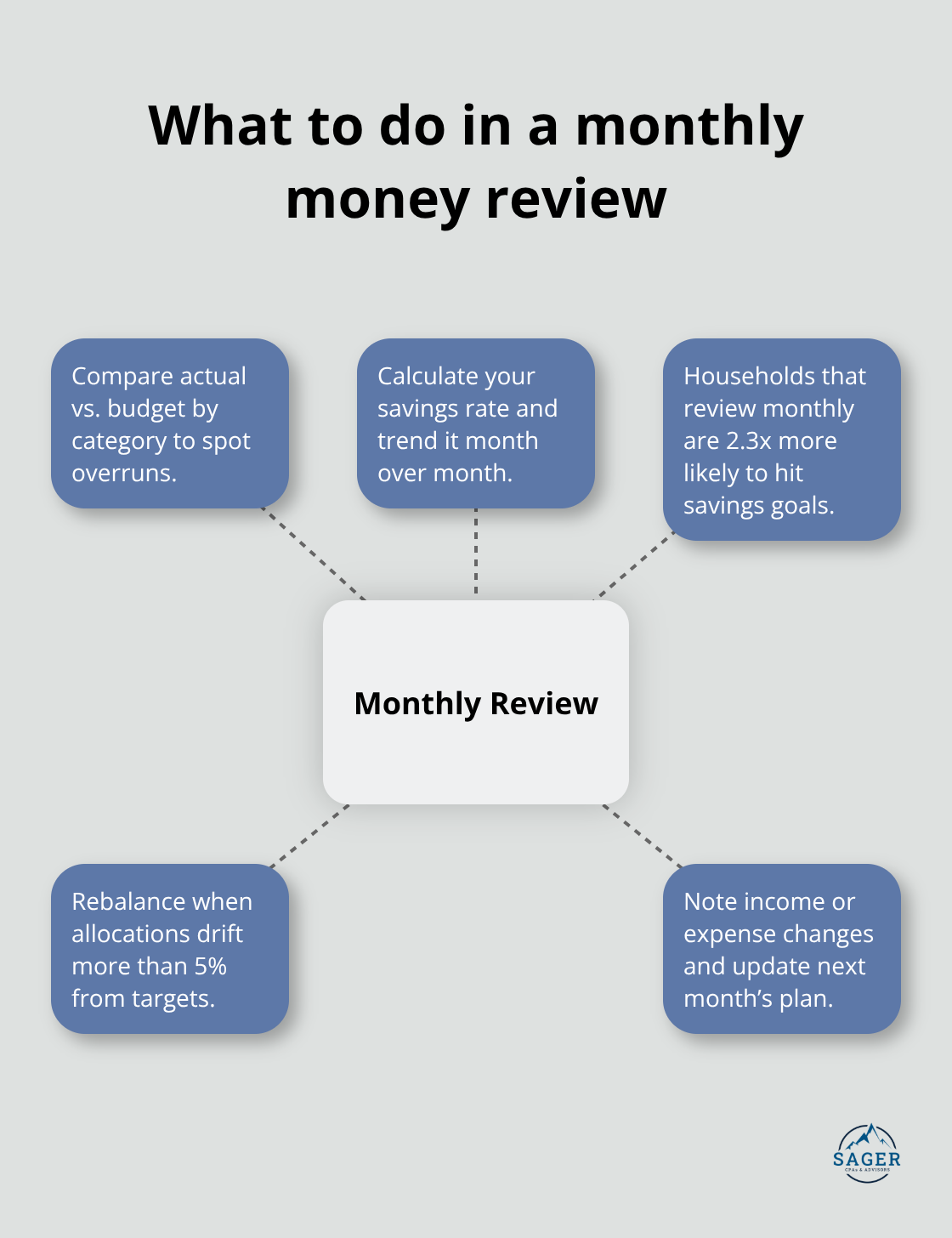

Monthly financial check-ins prevent small problems from becoming major setbacks. Compare actual expenses against your budget categories and identify areas where you exceeded planned amounts. Calculate your savings rate each month and adjust contributions if you fall short of targets. These regular reviews help you spot trends in your expenses and make proactive adjustments before they derail your financial goals.

Once you establish this foundation and create specific targets, the next challenge involves maintenance of momentum and navigation of obstacles that threaten to derail your progress.

Automation eliminates the willpower required to save consistently and removes emotional decisions from your financial plan. Set up automatic transfers from checking to savings accounts immediately after each paycheck arrives. Treat savings like any other fixed expense. Configure automatic investment contributions to retirement accounts and taxable investment portfolios to capture dollar-cost averaging benefits, which reduce the impact of market volatility over time. Most financial institutions allow you to schedule transfers for specific dates, amounts, and frequencies without monthly fees.

Monthly financial assessments catch problems before they become disasters and keep you accountable to your targets. Compare actual expenses against budgeted amounts in each category and calculate your monthly savings rate to identify trends. Bank of America Institute data reveals that households who conduct monthly financial reviews are 2.3 times more likely to achieve their savings goals compared to those who check annually.

Review investment performance and rebalance portfolios when allocations drift more than 5% from target percentages. Document any unexpected expenses or income changes and adjust future month budgets accordingly.

When financial emergencies arise, prioritize essential expenses first and temporarily reduce discretionary expenses rather than abandon your savings plan entirely. Research from the National Endowment for Financial Education indicates that 68% of people who experience financial setbacks never return to their original savings rate without intervention. If you must pause retirement contributions, restart them within 90 days at a reduced amount rather than wait until finances completely stabilize.

Use your emergency fund for true emergencies like medical bills or job loss (not vacation expenses or holiday gifts), then immediately create a replenishment plan with specific monthly targets to restore the depleted balance. Calculate the exact amount needed to rebuild your fund and divide it by a realistic timeframe. If you used $3,000 from your emergency fund, commit to replace it within six months through additional monthly savings of $500. This focused approach prevents your emergency fund from remaining permanently depleted. Consider implementing the 50/30/20 rule to structure your recovery budget effectively.

Financial success requires three fundamental steps: accurate assessment of your current situation, creation of specific targets with deadlines, and consistent execution through automation and regular reviews. The data shows that only 32% of Americans maintain written financial plans, which explains why most people struggle to build wealth effectively. Professional guidance accelerates your progress and helps you avoid costly mistakes that derail your financial goals.

We at Sager CPA provide strategic tax planning and comprehensive advisory services that reduce tax liabilities while we create customized action plans for long-term financial stability. Our clients benefit from proactive strategies and regular communication that keeps them accountable to their objectives. We help you develop approaches that align with your specific circumstances and timeline.

The difference between financial success and mediocrity comes down to immediate action rather than waiting for perfect conditions. Start with emergency fund creation, automate your savings transfers, and schedule monthly progress reviews. Sager CPA offers personalized consultations to help you develop a strategic approach that fits your needs (contact us today to get started).

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.