Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Tax planning for small business owners can be a daunting task, but it’s essential for financial success. At Sager CPA, we understand the challenges you face in managing your company’s tax obligations.

This guide will walk you through the key aspects of small business tax planning, from understanding your tax obligations to implementing effective strategies. We’ll also cover best practices for record-keeping and financial management to help you stay organized and compliant.

Income tax forms the cornerstone of small business taxation. Your business structure dictates how you’ll pay this tax. Sole proprietors and single-member LLCs report business income on personal tax returns using Schedule C. S corporations and partnerships file informational returns, with profits flowing to owners’ personal returns. C corporations pay corporate income tax directly.

The IRS mandates most businesses to make quarterly estimated tax payments. If you’re a calendar year taxpayer and you file your 2025 Form 1040 by March 2, 2026, you don’t need to make an estimated tax payment if you pay all the tax you owe at the time of filing.

Businesses with employees must handle several employment-related taxes:

Most employers file Form 941 quarterly to report these taxes (due dates: April 30, July 31, October 31, and January 31 of the following year).

Sales tax primarily falls under state and local jurisdiction. If you sell goods or certain services, you may need to collect and remit sales tax. Rules vary widely by location, so understand your specific obligations. Some states have implemented economic nexus laws, potentially requiring you to pay sales tax even without a physical presence in the state.

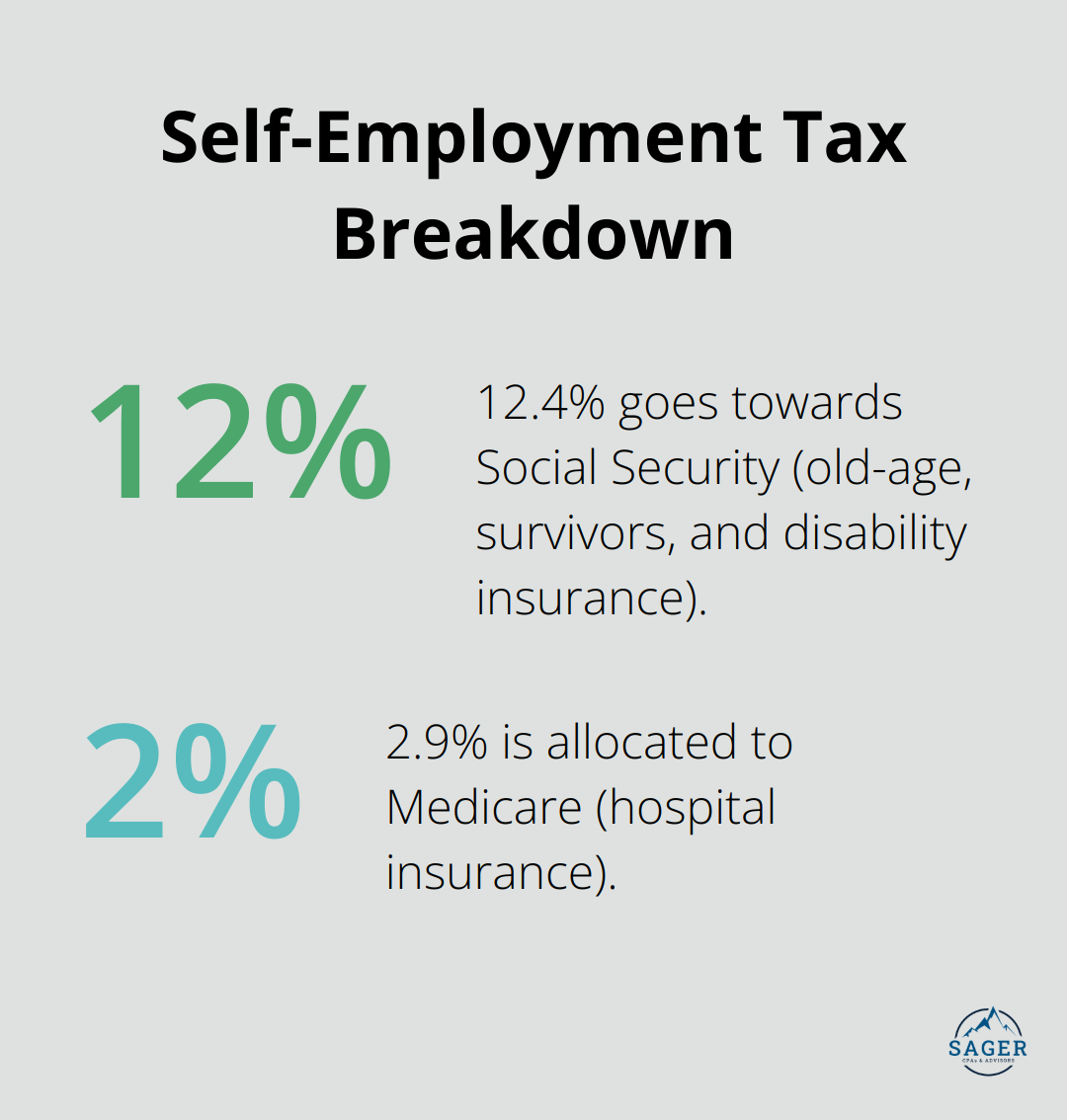

Self-employed individuals bear responsibility for self-employment tax, covering Social Security and Medicare contributions. The self-employment tax rate is 15.3%. The rate consists of two parts: 12.4% for social security (old-age, survivors, and disability insurance) and 2.9% for Medicare (hospital insurance).

Don’t overlook property tax if your business owns real estate or significant personal property (equipment, furniture, etc.). Property tax rates and rules vary by location, so check with your local tax assessor’s office for specific requirements.

As we move forward, let’s explore effective strategies to manage these tax obligations and optimize your business’s financial position.

Your business structure significantly impacts your tax obligations. Sole proprietorships and partnerships offer simplicity but expose owners to personal liability. S corporations can provide tax advantages through income splitting, potentially reducing self-employment taxes. C corporations, while subject to double taxation, might benefit larger businesses through lower corporate tax rates and more extensive deductions.

We recommend an annual reassessment of your business structure. As your company grows, a transition from a sole proprietorship to an S corporation could yield substantial tax savings. For example, a business earning $200,000 annually could save over $10,000 in self-employment taxes by electing S corporation status (according to a study by the National Association of Tax Professionals).

Utilizing available deductions and credits is essential to minimize your tax burden. Common deductions include home office expenses, vehicle use, and equipment purchases. The Section 179 deduction allows businesses to deduct the full purchase price of qualifying equipment and software purchased or financed during the tax year (up to $1,250,000 for 2025).

Industry-specific tax credits can provide substantial savings. The Research and Development (R&D) Tax Credit, for instance, can benefit businesses investing in innovation. A recent survey by Alliantgroup found that the average federal R&D tax credit for small and medium-sized businesses was $230,000.

The timing of your income and expenses can significantly impact your tax liability. If you operate on a cash basis, consider delaying billing for services until January to push income into the next tax year. Conversely, accelerate expenses by purchasing necessary supplies or equipment before year-end.

For businesses anticipating a higher tax bracket in the coming year, it might be advantageous to accelerate income into the current year. This strategy can be particularly effective if you expect tax rates to increase, as projected for some brackets after 2025 when certain provisions of the Tax Cuts and Jobs Act expire.

Establishing a retirement plan secures your financial future and offers immediate tax benefits. A SEP IRA allows contributions of up to 25% of compensation or $69,000 for 2025, whichever is less. These contributions are tax-deductible, potentially reducing your current year tax liability significantly.

For businesses with employees, a SIMPLE IRA or 401(k) plan can provide tax advantages while helping attract and retain talent. Employer contributions to these plans are tax-deductible, and employees benefit from tax-deferred growth on their savings.

The implementation of these strategies creates a robust tax plan that aligns with your business goals and maximizes your financial resources. Tax laws are complex and ever-changing, so working with a knowledgeable tax professional ensures you leverage all available opportunities while remaining compliant with current regulations. As we move forward, let’s explore the importance of proper record-keeping and financial management in maintaining an effective tax strategy.

Create a system to organize and store crucial financial documents. These include bank statements, credit card statements, receipts for business expenses, invoices, payroll records, and any documentation related to business income. The IRS requires businesses to keep records for at least three years from the date of tax return filing.

A study by the National Small Business Association revealed that 40% of small business owners spend over 80 hours per year dealing with federal taxes. An organized record-keeping system can significantly reduce this time and stress.

Accurate bookkeeping is essential for tax compliance and financial management. Without it, you risk making decisions based on incomplete or outdated information, which can lead to financial missteps. Update your books regularly, ideally weekly, to maintain an up-to-date view of your financial position. This practice allows for timely identification of discrepancies and provides a solid foundation for tax preparation.

Consider using the double-entry bookkeeping method, which records each transaction in at least two different accounts. This system provides a more comprehensive view of your finances and helps catch errors. A survey by Wasp Barcode Technologies found that 65% of small business owners who use double-entry bookkeeping report feeling very knowledgeable about their company’s finances.

Embrace technology to streamline your record-keeping and tax preparation processes. Cloud-based accounting software (like QuickBooks Online or Xero) can automate many aspects of bookkeeping, offering benefits such as cost savings, scalability, real-time data access, and enhanced financial management.

A report by Sage found that businesses using cloud accounting software spend 15% less time on administrative tasks compared to those using traditional methods. This time savings allows you to focus more on growing your business and less on paperwork.

Maintain separate bank accounts and credit cards for business and personal use. This separation simplifies expense tracking and helps prevent the commingling of funds, which can raise red flags during an audit.

The IRS reports that poor record-keeping is one of the top reasons small businesses fail audits. Keeping business finances separate creates a clear audit trail and demonstrates the legitimacy of your business expenses.

Set aside time each month to review key financial reports such as profit and loss statements, balance sheets, and cash flow statements. This practice helps you understand your business’s financial health and identify potential tax-saving opportunities throughout the year.

A study by the Small Business Administration found that businesses that regularly review their financial statements are 30% more likely to be profitable than those that don’t. This regular review also ensures you’re prepared for tax season well in advance, reducing last-minute stress and potential errors.

Meticulous record-keeping is crucial for maintaining detailed records of all financial activities, which can significantly impact your bottom line and tax strategies.

Tax planning for small business owners requires a strategic approach to optimize financial success. Understanding tax obligations, implementing effective strategies, and maintaining accurate records will help you minimize tax liabilities and maximize growth opportunities. Professional guidance from a qualified tax advisor can provide personalized strategies, ensure compliance, and navigate complex situations, potentially saving you significant time and money.

We at Sager CPA specialize in expert financial management and tax planning services for individuals and businesses. Our comprehensive approach includes precise accounting, strategic advisory services, and tax planning to reduce liabilities. We develop proactive strategies and customized action plans to provide our clients with the financial clarity needed for informed decision-making.

Professional tax planning transforms a daunting task into a powerful tool for financial success. Take control of your business’s tax strategy today to pave the way for a more prosperous future. Our team stands ready to assist you in optimizing your tax position and achieving your financial goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.