Financial Clarity Audits: A Path to Transparent Reporting

Discover how financial clarity audits reveal hidden inefficiencies and transform your reporting into a transparent, actionable foundation.

S Corporation owners face unique tax challenges and opportunities. Optimizing tax strategies for S Corp owners can lead to significant savings and improved financial health for your business.

At Sager CPA, we’ve helped numerous S Corp owners navigate the complexities of tax planning. This guide will explore key tactics to maximize your tax benefits while staying compliant with IRS regulations.

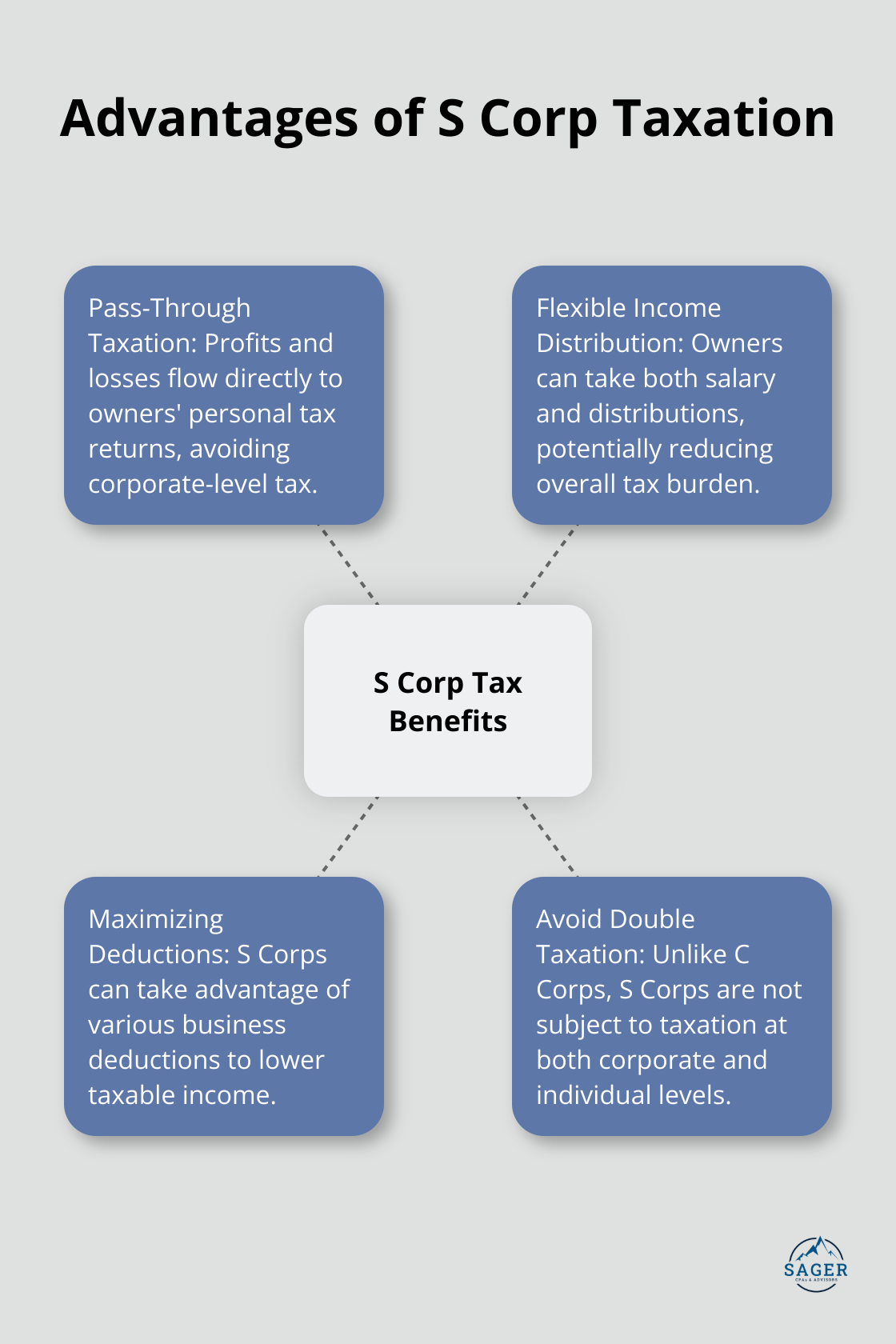

S Corporations offer unique tax advantages that can significantly benefit business owners. These benefits often lead to substantial savings for S Corp owners.

S Corps use a pass-through taxation system. The main advantage of the S corp over the C corp is that an S corp does not pay a corporate-level income tax. Instead, profits and losses “pass through” to the owners’ personal tax returns. This approach eliminates the double taxation issue that C Corporations face, where profits are taxed at both the corporate and individual levels.

For example, if your S Corp earns $500,000 in a year, and you’re the sole owner, that $500,000 will appear on your personal tax return. You’ll pay taxes on this income at your individual tax rate, which could be lower than corporate tax rates.

S Corps provide flexibility in how owners receive income from the business. As an owner, you can take both a salary and distributions. This split can lead to significant tax savings.

Your salary is subject to payroll taxes, including Social Security and Medicare taxes. However, distributions are not. A careful balance of your salary and distributions can potentially reduce your overall tax burden.

For instance, if you set your salary at $100,000 and take $400,000 in distributions from a $500,000 profit, you’ll only pay payroll taxes on the $100,000 salary. This strategy could save you tens of thousands in taxes compared to taking all $500,000 as salary.

S Corps can take advantage of various business deductions to lower taxable income. These include expenses like office rent, equipment purchases, and employee benefits.

The home office deduction is one potential deduction for S Corp owners. If you use part of your home exclusively for S Corp business, you may be eligible to deduct a portion of your expenses.

Many S Corp owners (with proper guidance) have identified and maximized these deductions, sometimes reducing their taxable income significantly.

While S Corps offer numerous tax advantages, it’s essential to plan carefully. The IRS scrutinizes S Corps closely, particularly regarding reasonable compensation for owner-employees. Try to strike a balance between salary and distributions that reflects the true value of your work for the company.

Additionally, S Corps must adhere to specific rules and regulations (such as restrictions on the number and type of shareholders). Failure to comply can result in the loss of S Corp status and its associated tax benefits.

As we move forward, we’ll explore how to optimize the balance between salary and distributions to maximize your tax savings while staying compliant with IRS regulations.

S Corp owners must pay themselves a reasonable salary for their work. This salary should reflect what you would pay someone else to perform your job. The IRS scrutinizes S Corp owner salaries, and setting it too low in favor of higher distributions can trigger an audit.

Reasonable compensation is a complex issue, and there are no specific guidelines in the Code or the Regulations. To determine a reasonable salary, you should consider several factors:

The Bureau of Labor Statistics provides salary data for various occupations, which can serve as a helpful benchmark. For example, the median annual wage for chief executives was $179,520 in May 2022.

After you establish a reasonable salary, you can allocate the remaining profits as distributions. This strategy can lead to significant tax savings because distributions aren’t subject to payroll taxes.

Here’s an example:Your S Corp generates $300,000 in profit. You set your salary at $150,000. You could potentially save over $7,000 in Medicare taxes alone by taking the remaining $150,000 as a distribution rather than salary.

However, you must strike the right balance. Taking too little salary could raise red flags with the IRS, while taking too much could result in unnecessary payroll taxes.

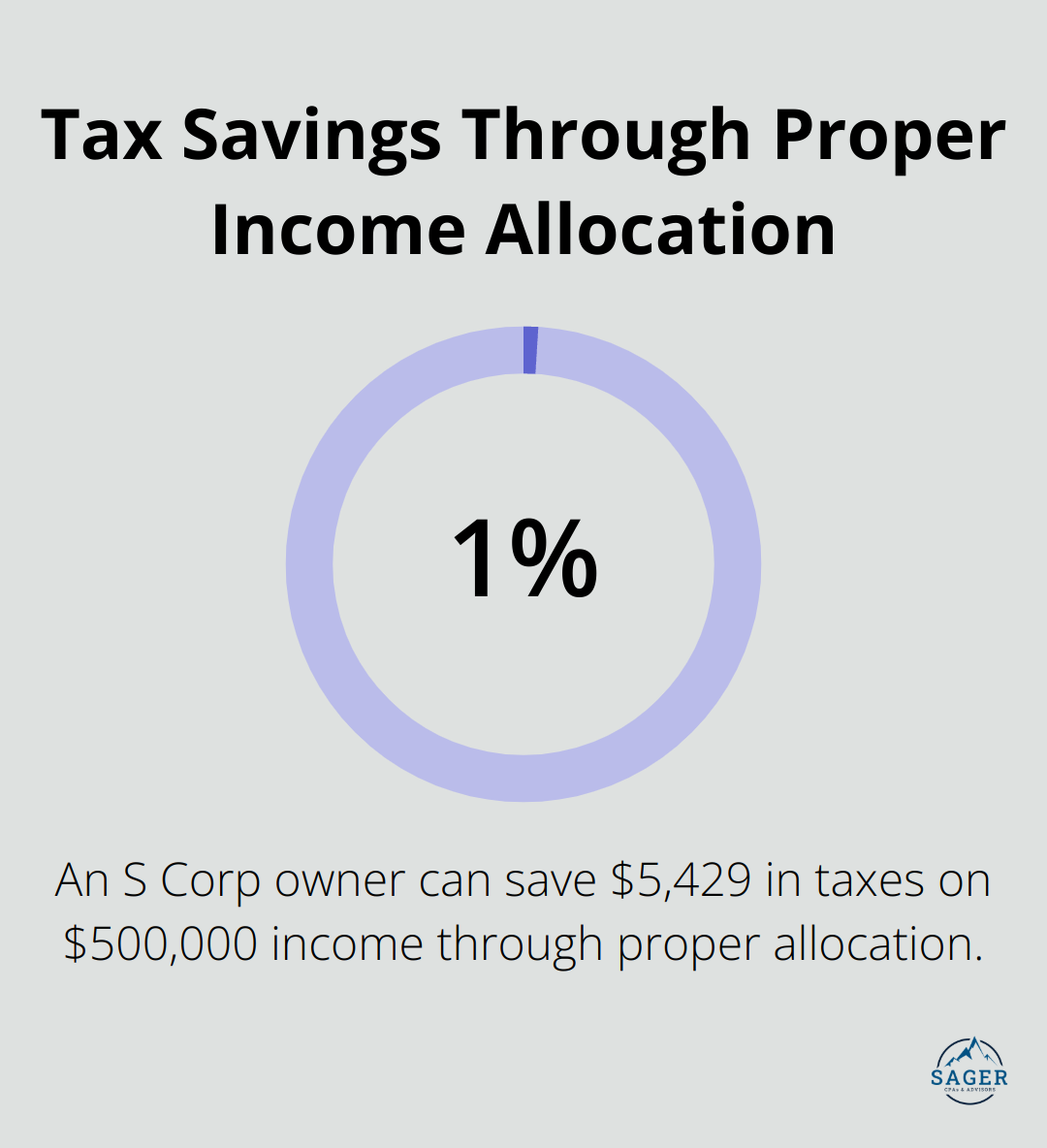

A well-executed salary and distribution strategy can lead to substantial tax savings. Consider this example:

An S Corp owner with $500,000 in business income could save $5,429 in taxes by taking a $200,000 salary and $300,000 in distributions, compared to taking the entire amount as salary.

Moreover, proper allocation can help you maximize other tax benefits. For instance, contributions to certain retirement plans are based on W-2 wages. By setting an appropriate salary, you can optimize your ability to contribute to these plans while still benefiting from the tax advantages of distributions.

The right strategy depends on your specific circumstances, including:

You should review and adjust your salary and distribution strategy regularly as your business grows and evolves. This approach ensures you maximize your tax savings while remaining compliant with IRS regulations.

As we move forward, we’ll explore how S Corp owners can leverage deductions and credits to further reduce their tax burden and improve their overall financial position.

S Corp owners have numerous opportunities to reduce their tax burden through strategic use of deductions and credits. These strategies can significantly impact a company’s bottom line.

S Corps can deduct a wide range of business expenses to lower their taxable income. Some often-overlooked deductions include:

Home office expenses: S Corp owners who use part of their home exclusively for business may deduct a portion of their mortgage interest, property taxes, utilities, and maintenance costs.

Vehicle expenses: S Corps can deduct costs related to business use of vehicles, including mileage, gas, maintenance, and depreciation. (In 2023, the standard mileage rate for business use is 65.5 cents per mile.)

Professional development: Costs for conferences, workshops, and continuing education related to the business are fully deductible.

Health insurance premiums: S Corps can deduct 100% of health insurance premiums paid for employees (including owner-employees).

Many S Corps overlook valuable tax credits specific to their industry. For example:

Research and Development (R&D) Credit: This credit is one of the most significant domestic tax credits remaining under current tax law.

Work Opportunity Tax Credit (WOTC): S Corps that hire individuals from certain target groups can receive a credit. The maximum tax credit is generally $2,400.

Energy-Efficient Commercial Buildings Deduction: S Corps can deduct up to $1.88 per square foot for installing energy-efficient lighting, HVAC, or building envelope systems.

Implementing retirement plans can provide significant tax benefits for S Corp owners. Some effective options include:

SEP IRA: In 2023, S Corps can contribute up to 25% of an employee’s compensation or $66,000 (whichever is less). This reduces the company’s taxable income while providing retirement savings for employees.

Solo 401(k): For S Corps with no employees other than owners and spouses, this plan allows for both employee and employer contributions. In 2023, the total contribution limit is $66,000 ($73,500 if age 50 or older).

Cash Balance Plan: This defined benefit plan can allow for even higher contributions, potentially reducing taxable income by hundreds of thousands of dollars for high-earning S Corp owners.

Tax laws are complex and constantly changing. Working with a knowledgeable tax professional can help ensure S Corp owners maximize their tax savings while remaining compliant with IRS regulations. Sager CPA and Advisors offers expert financial management and tax planning services tailored for individuals and businesses, making them an excellent choice for S Corp owners seeking to optimize their tax strategies.

Tax strategies for S Corp owners require careful planning and execution. S Corp owners can reduce their tax burden while complying with IRS regulations through pass-through taxation, balanced salary and distributions, and maximized deductions and credits. Professional tax advice proves invaluable in navigating the complex landscape of tax laws and regulations, as strategies must be tailored to specific business situations.

Sager CPA offers expert financial management and tax planning services for S Corp owners. Our team can help you navigate S Corp taxation complexities, ensure IRS compliance, and identify tax-saving opportunities. Effective tax strategies can reduce your tax liability, increase after-tax income, and free up resources for business growth and personal wealth accumulation.

Tax planning is an ongoing process that should evolve with your business. Regular review and adjustment of your tax planning approach (with guidance from experienced professionals) will help maximize your tax benefits. This approach aligns with your overall business and personal financial goals, providing a solid foundation for long-term financial stability and success.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.