Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Financial risk management isn’t optional for business owners-it’s the difference between stability and crisis. Most companies face multiple threats simultaneously: market swings, customer defaults, and cash flow gaps that can derail growth.

At Sager CPA, we’ve seen firsthand how businesses that identify and address these risks early stay competitive and profitable. This guide walks you through the specific risks your business faces and the practical steps to control them.

Market volatility hits harder than most business owners expect. When commodity prices, interest rates, or currency exchange rates swing unexpectedly, your profit margins compress fast. Market volatility and price fluctuations can increase costs, reduce revenue, or reshape pricing strategies, especially for companies with ongoing international operations. The challenge isn’t predicting these moves-it’s building a business structure that survives them.

Diversification across suppliers, geographic markets, and product lines reduces your exposure to any single price shock. Companies that lock in prices through forward contracts or hedging strategies protect themselves from sudden swings. This isn’t speculation; it’s defense.

Credit risk represents a different threat altogether. When customers don’t pay, your cash disappears while expenses continue. According to data from credit agencies, small businesses lose approximately 1.6% of their annual revenue to bad debt on average. That’s real money walking out the door.

The problem intensifies when a single customer represents 20% or more of your revenue-one default creates a crisis. Implement strict credit policies: check customer payment history before extending terms, require deposits for large orders, and monitor aging receivables weekly. Payment terms matter too. Offering 30-day payment windows instead of 60 or 90 days accelerates cash inflow and reduces default risk. Some industries tolerate longer terms, but don’t accept them as inevitable; negotiate shorter windows whenever possible.

Liquidity risk is where financial problems become operational emergencies. Your business can be profitable on paper while drowning in cash flow problems. This happens when you have revenue tied up in inventory or unpaid invoices while bills arrive today. Construction companies and manufacturers know this pain acutely: they pay workers and suppliers upfront but collect from clients weeks or months later.

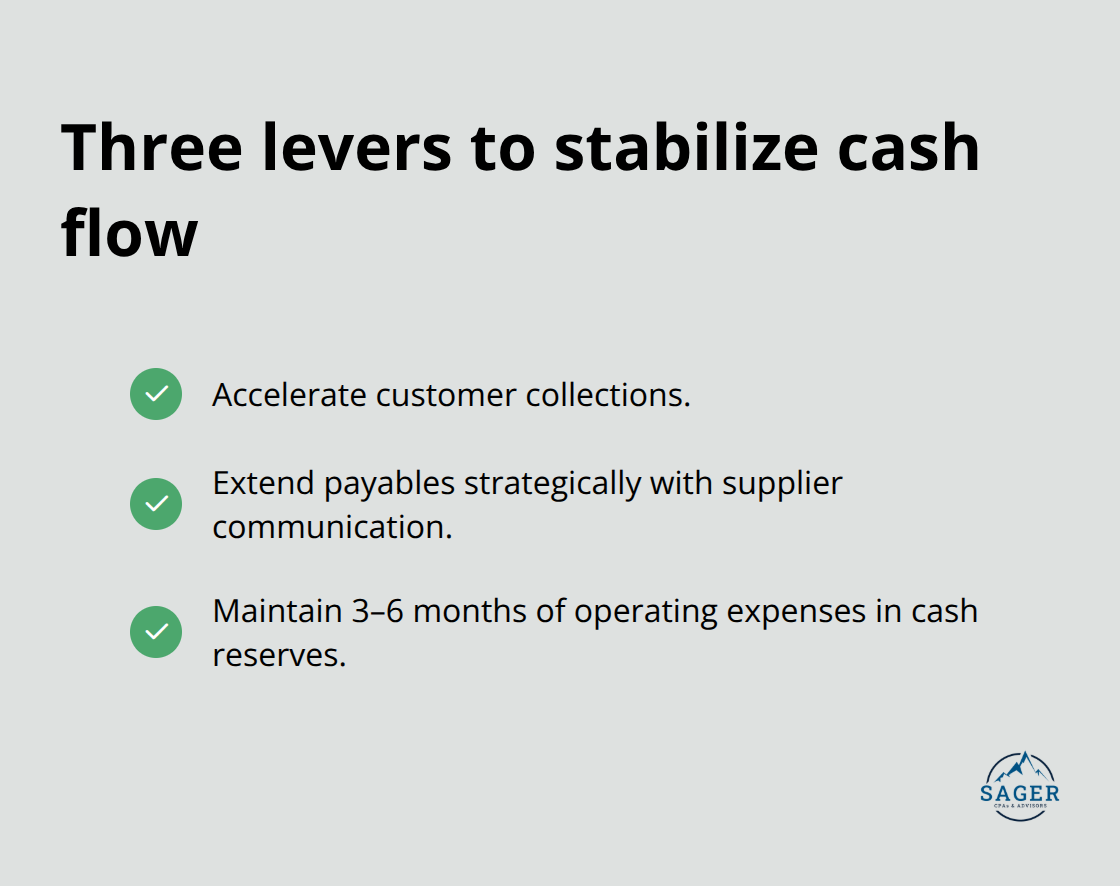

The solution requires discipline around three levers: accelerate collections, extend payables strategically, and maintain a cash reserve equal to 3–6 months of operating expenses. That reserve isn’t conservative-it’s mandatory. Without it, a single lost customer or delayed payment forces you to choose between paying employees and paying suppliers.

Working capital management determines survival more than profitability does. Track your cash conversion cycle obsessively-measure the days between paying suppliers and collecting from customers. If that number is 45 days, you need enough cash on hand to fund 45 days of operations. Many businesses fail not because they’re unprofitable but because they run out of cash before profitability arrives.

Understanding these three risks positions you to take action. The next section shows you exactly how to identify and assess which risks pose the greatest threat to your specific business.

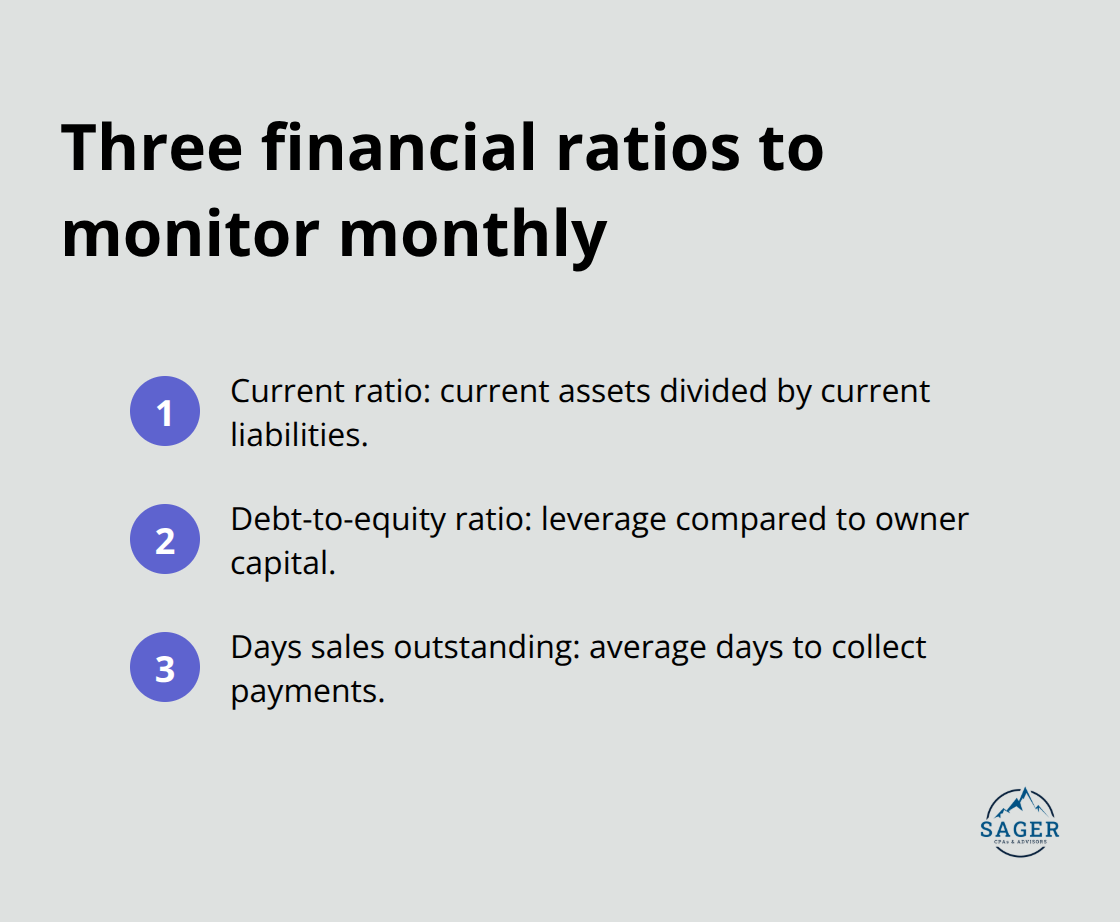

Identifying financial risks requires more than glancing at your bank balance each month. You need a systematic approach that surfaces threats before they become crises. Start with your financial statements themselves. Pull your last 12 months of profit and loss statements, balance sheets, and cash flow statements, then calculate three critical ratios: your [current ratio](https://www.investopedia.com/terms/c/currentratio.asp] (current assets divided by current liabilities), your debt-to-equity ratio, and your days sales outstanding (how long it takes to collect customer payments).

A current ratio below 1.5 signals liquidity trouble ahead. A debt-to-equity ratio above 2.0 means creditors own more of your business than you do. Days sales outstanding climbing above your stated payment terms reveals customers who pay late, which directly impacts cash flow. These numbers tell you exactly where pressure points exist.

Compare your ratios month-to-month and year-to-year; trends matter more than single snapshots. If your current ratio dropped from 2.1 to 1.8 in six months, that’s a warning signal worth investigating immediately.

Industry benchmarks provide the context that makes your numbers meaningful. If your days sales outstanding averages 35 days but competitors average 22 days, you’re carrying excess customer receivables that drain working capital. Access industry benchmarks through your trade association, accounting software analytics, or financial databases like Risk Management Association data.

Once you identify gaps between your performance and industry standards, investigate the cause. Is your sales team extending credit too freely? Are your collection processes weak? The difference between your metrics and industry norms points directly to the problem.

Beyond ratios, establish key risk indicators specific to your business: customer concentration (what percentage of revenue comes from your top five customers), inventory turnover (how quickly you convert inventory to sales), and supplier concentration (reliance on a single vendor). If one customer represents 30% of revenue and they disappear, your business faces a genuine crisis.

Track these indicators monthly and set threshold alerts. When customer concentration exceeds 25%, treat it as a red flag requiring immediate attention through customer diversification or contract renegotiation. This disciplined monitoring transforms abstract financial data into actionable intelligence about which risks demand your focus right now.

With your risks identified and assessed, you’re ready to move into the practical work of controlling them. The next section shows you the specific mitigation strategies that protect your cash flow and stabilize your business.

Stop thinking about risk mitigation as a single action and start treating it as a system of overlapping defenses. The strongest protection comes from spreading risk across multiple channels so no single failure point destroys your business.

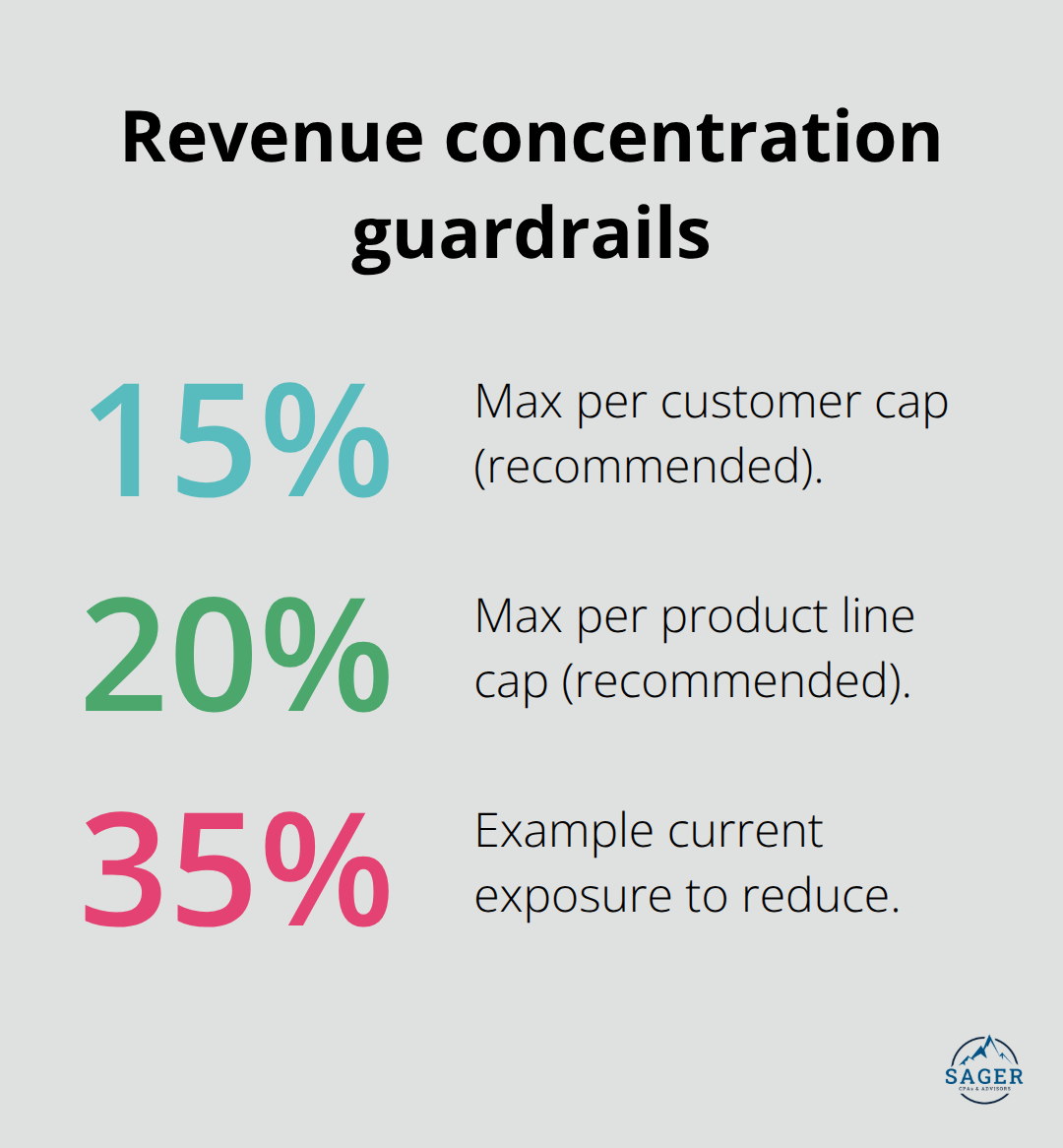

Revenue concentration is lethal. When 40% of your income flows from one customer or product line, that customer’s decision to switch vendors or that product’s market decline becomes an existential threat. Cap any single customer at 15% of annual revenue and any single product line at 20%. This forces intentional diversification.

If you’re currently overexposed, create a 12-month plan to reduce that concentration through targeted new customer acquisition or product expansion. The math is straightforward: if customer A represents 35% of revenue and you want to cap them at 15%, you need to add enough new revenue from other sources to shift that ratio. This takes discipline and planning, but it’s non-negotiable for long-term survival.

The second defense layer pairs cash reserves with accessible credit. Financial institutions recommend maintaining 3–6 months of operating expenses in liquid reserves, but this represents a floor, not a ceiling. Manufacturing and construction businesses operating with longer payment cycles need 6–9 months. Retail and service businesses with faster cash conversion can operate closer to 3–4 months.

Calculate your monthly burn rate (total operating expenses) and multiply by your recovery timeline. If an unexpected crisis hits and your largest customer defaults, how many months until you generate replacement revenue? That’s your minimum reserve target. Pair this reserve with an established credit line before you need it. Banks approve credit lines based on historical performance, not desperation. A $50,000 line of credit obtained when your business is healthy costs nothing if unused but becomes invaluable during a cash crunch. Apply for credit capacity now, while lenders view your business as low-risk.

The third layer is operational control. Weak documentation and unclear approval processes create opportunities for fraud, errors, and financial leaks that compound other risks. Segregate financial duties so no single person controls cash from receipt through deposit and reconciliation. Require written approval for expenses above a threshold you set (typically $2,500–$5,000 for small businesses).

Reconcile bank statements within five business days of receipt, not monthly. Monthly reconciliation delays fraud detection by weeks, which means losses compound. Weekly or twice-weekly cash position reviews during high-transaction periods catch discrepancies while they’re still small. Document your accounts receivable aging weekly and follow up on invoices exceeding your payment terms by 10 days. Most businesses wait 30+ days past due date before taking action, which means they’ve already lost negotiating leverage and cash flow has deteriorated significantly.

Financial risk management isn’t a project you complete and forget-it’s an ongoing discipline that separates businesses that survive downturns from those that collapse under pressure. The three risks we covered (market volatility, credit defaults, and liquidity crises) hit every business differently depending on your industry, customer base, and operational structure. What matters is that you’ve now identified which risks pose the greatest threat to your specific situation and understand the practical defenses that address root causes, not symptoms.

Your next step is to assess your current position honestly by calculating your financial ratios, identifying your biggest concentration risks, and determining whether your cash reserves match your actual needs. Then build a 12-month action plan that addresses the gaps you uncover. This isn’t theoretical work-it’s the foundation of business survival, and the companies that monitor their financial ratios monthly, benchmark against industry standards, and track key risk indicators catch problems early when solutions are cheaper and easier.

We at Sager CPA help businesses move from financial uncertainty to clarity through strategic financial planning and advisory services. If you’re ready to strengthen your financial position and build a resilient strategy tailored to your business, schedule a consultation to create your personalized approach.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.