Demystifying Financial Risk Management SMBs: A Growth Playbook

Master financial risk management for SMBs with strategies to protect profits, reduce losses, and accelerate growth without complexity.

Most people treat their investments like a set-it-and-forget-it savings account. That approach costs money.

At Sager CPA, we’ve seen firsthand how portfolio financial management separates people who build real wealth from those who watch opportunities slip away. The difference isn’t luck or market timing-it’s having a clear system for building, monitoring, and adjusting your investments.

This guide walks you through exactly how to do that.

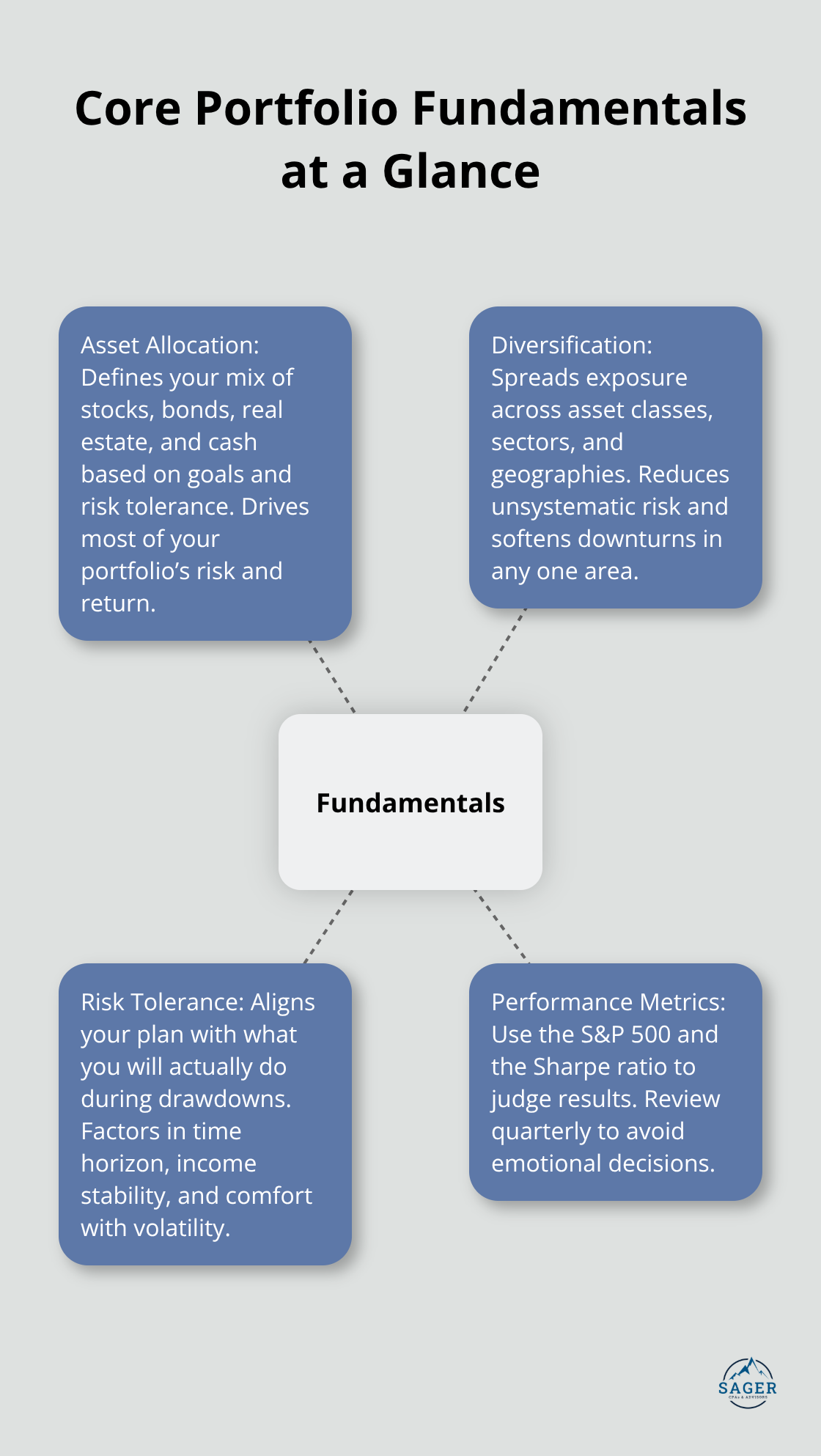

Most investors skip the fundamentals and jump straight to picking stocks or funds. That’s backwards. Asset allocation and diversification are not abstract concepts-they’re the actual mechanics that determine whether your portfolio survives a market downturn or gets crushed by it. Asset allocation defines how you split your money across stocks, bonds, real estate, and cash based on your goals and risk tolerance. Research shows that asset allocation largely drives both your risk and your returns, which means this decision matters more than which individual investments you choose.

Your age and timeline shape everything. If you’re 35 years old with 30 years until retirement, a portfolio weighted heavily toward stocks makes sense because you can weather volatility and benefit from long-term growth. If you’re 65 and need income now, bonds and dividend-paying stocks become more important. The allocation isn’t about finding the perfect mix-it’s about matching your portfolio structure to your actual life situation.

Diversification then protects that allocation by spreading your money across different asset classes, sectors, and geographies. A common benchmark is owning 15 to 20 stocks across various industries, or using index funds like the S&P 500 that give you exposure to hundreds of companies instantly. The reason this matters is that unsystematic risk-the risk tied to a single company or industry-can be eliminated through diversification. Systematic risk, which affects the entire market, cannot be eliminated, but diversification across asset classes like stocks, bonds, real estate, and commodities reduces the overall damage when one area underperforms.

Risk tolerance isn’t what you think you can handle-it’s what you’ll actually handle when your portfolio drops 20 percent in three months. Many investors overestimate their tolerance because they haven’t experienced real losses. Questionnaires combined with honest reflection on your time horizon, income stability, and emotional comfort with volatility help you assess where you truly stand. If you’re five years from retirement, high volatility is painful because you have little time to recover. If you’re 30 years old, a 40 percent market decline is an opportunity to buy more at lower prices.

Your risk tolerance also depends on whether you have other income sources. A business owner with stable cash flow can take more portfolio risk than someone relying entirely on investment returns.

Once you know your tolerance, performance metrics keep you honest about whether your portfolio is actually working. The S&P 500 is the most common benchmark for U.S. stock portfolios-if your portfolio returns 6 percent while the S&P 500 returns 12 percent, you’re underperforming and need to know why. The Sharpe ratio measures risk-adjusted returns, showing whether you’re getting paid enough for the volatility you’re taking. A higher Sharpe ratio means better returns relative to risk. Track these metrics quarterly, not daily, because daily tracking feeds anxiety and leads to impulsive decisions that destroy long-term results.

With these fundamentals in place, you’re ready to move beyond theory and start selecting the actual investments that will build your wealth.

Once you understand your risk tolerance and asset allocation, the real work starts: turning that framework into actual investments that generate returns. The difference between a mediocre portfolio and one that compounds wealth lies in three decisions: what you buy, when you rebalance, and how you structure it for taxes. Most investors stumble on at least one of these, which is why we see portfolios that underperform despite solid fundamentals.

Investment selection requires discipline, not stock-picking genius. Your goal isn’t to find the next Apple or Tesla. Instead, you build a core holding that matches your allocation. If you’ve decided on a 70 percent stock, 30 percent bond allocation, you need investments that hit those percentages. For the stock portion, a low-cost S&P 500 index fund or total U.S. stock market index fund gives you instant diversification across hundreds of companies at a fraction of the cost of picking individual stocks.

The expense ratio matters more than most investors realize. A fund charging 0.03 percent annually costs roughly $90 per $100,000 invested per year, while an actively managed fund at 0.75 percent costs $2,250. Over 30 years, that difference compounds into tens of thousands in lost returns.

The number 0% seems to be not appropriate for this chart. Please use a different chart type. For bonds, intermediate-term bond funds or bond index funds provide steady income without the complexity of laddering individual bonds unless you have substantial capital.

The mistake most investors make is overcomplicating this step. You don’t need 30 different funds. You need five to eight holdings that cover your allocation and stay put.

Rebalancing is where discipline separates winners from losers. When stocks rally and bonds stagnate, your 70/30 allocation drifts to 80/20 or higher, concentrating risk without you realizing it. Rebalancing forces you to sell what’s performed well and buy what hasn’t, which feels wrong but is exactly right.

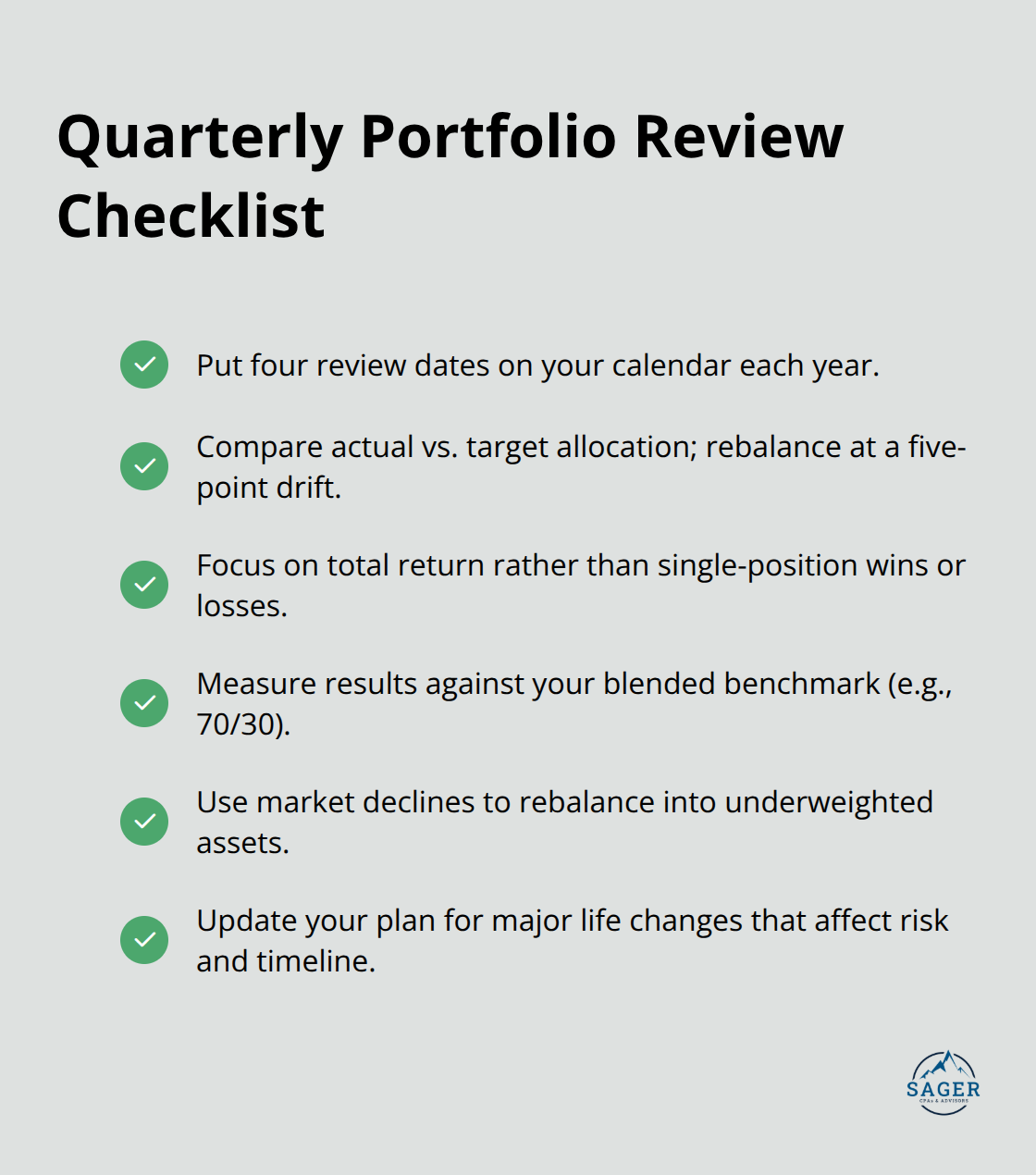

Rebalance once yearly or when your allocation drifts more than five percentage points from target, not monthly or quarterly. Frequent rebalancing triggers trading costs and taxes that erode returns.

On the tax front, location matters as much as selection. Tax-advantaged accounts like 401(k)s and IRAs should hold your highest-returning, most tax-inefficient investments: growth stocks and bonds. Taxable accounts should hold index funds and tax-efficient strategies. Tax-loss harvesting is when you sell investments at a loss and use those losses to offset gains in other investments, which can enhance after-tax returns.

Long-term capital gains taxed at 15 or 20 percent beat short-term gains taxed as ordinary income at your marginal rate, so hold investments beyond one year when possible. These three moves-simple core holdings, annual rebalancing, and tax-aware placement-eliminate most of the friction that destroys returns and position you to monitor whether your portfolio actually performs as intended.

Quarterly reviews keep your portfolio honest without feeding the anxiety that daily market watching creates. Set a specific date each quarter-say the first week of January, April, July, and October-and spend an hour reviewing your holdings, returns, and allocation. Pull your latest statements and compare your actual allocation to your target. If stocks have rallied and now represent 78 percent of your portfolio instead of 70 percent, that’s your signal to rebalance.

A five percentage point drift is your trigger to act.

Track your total return, not individual stock performance. Most people fixate on whether their Apple holding beat the S&P 500, which misses the point entirely. Your S&P 500 index fund should slightly underperform the actual index because of the expense ratio, typically around 0.03 percent annually. That’s not a problem; that’s the cost of instant diversification.

Compare your total portfolio return to a blended benchmark that matches your allocation. If you’re 70 percent stocks and 30 percent bonds, your benchmark should be roughly 70 percent of the S&P 500’s return plus 30 percent of a bond index return. If you’re consistently beating that benchmark, excellent. If you’re underperforming by more than one percentage point annually, something’s wrong and needs investigation.

Market swings test your discipline harder than anything else. When the market dropped roughly 20 percent in 2022 according to S&P 500 data, panic selling destroyed returns for thousands of investors who violated their own allocation plans. Your quarterly review is when you ask the hard question: does my current allocation still match my risk tolerance and time horizon?

If you’re still 30 years from retirement, a market decline is a rebalancing opportunity, not a crisis. Sell some bonds that held steady and buy stocks at lower prices, which is exactly what your plan should have told you to do. This mechanical approach removes emotion from the equation and keeps you aligned with your long-term strategy.

Life changes demand portfolio adjustments too. Getting married, having children, receiving an inheritance, or changing jobs shifts your risk tolerance and time horizon. A promotion that doubles your income might justify taking more investment risk. A job loss requires the opposite.

Turning 50 or 55 is a logical checkpoint to gradually shift your allocation toward stability. Don’t make these shifts emotionally; make them mechanically. If your circumstances genuinely changed, adjust your target allocation and execute the rebalancing that brings you back into alignment. The investors who fail aren’t those who monitor too closely; they’re those who ignore their portfolio for five years and watch it drift completely off course.

Portfolio financial management succeeds when you stop treating it as a one-time decision and start treating it as a system. The three principles that separate successful investors from struggling ones are straightforward: build an allocation that matches your life, rebalance mechanically when drift occurs, and monitor quarterly without obsessing. These aren’t complicated-they’re boring, which is exactly why they work.

The mistakes that destroy returns are equally predictable. Overcomplicating your holdings with too many funds or individual stocks creates unnecessary costs and tracking burden. Panic selling during market declines violates your own plan and locks in losses at the worst possible time. Ignoring your portfolio for years lets allocation drift silently until your risk exposure no longer matches your tolerance. Tax inefficiency through poor account placement and frequent trading in taxable accounts silently erodes returns that compound over decades.

If building this system feels overwhelming or you’re uncertain about your allocation, that’s normal. Portfolio financial management involves tax considerations, risk assessment, and strategic decisions that benefit from professional guidance. We at Sager CPA help individuals and businesses create customized financial strategies that reduce tax liabilities and clarify your path forward. Schedule a consultation to develop a personalized plan tailored to your specific situation and goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.