How to Reduce Your Tax Liability Legally

Reduce your tax liability legally with proven strategies. Discover deductions, credits, and planning techniques to lower your tax bill.

Freelancers face a unique tax situation that most W-2 employees never encounter. You’re responsible for paying both the employer and employee portions of self-employment tax, tracking your own income, and making quarterly estimated payments to the IRS.

At Sager CPA, we’ve helped hundreds of freelancers navigate tax planning and avoid costly mistakes. This guide walks you through the essentials so you can keep more of what you earn.

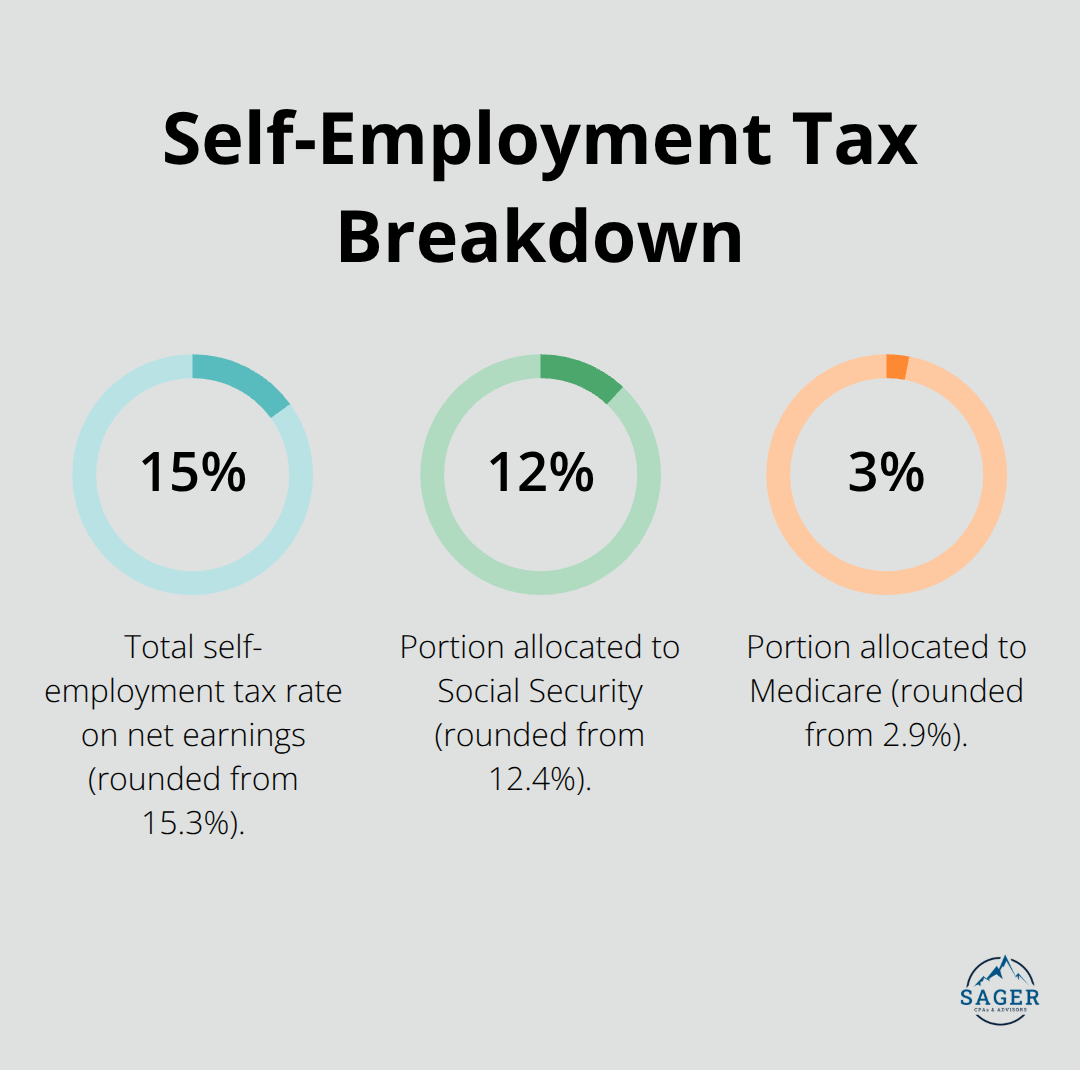

Self-employment tax hits differently than income tax, and most freelancers underestimate the bite. You pay 15.3% on your net earnings-12.4% for Social Security and 2.9% for Medicare. This rate exists because you cover both the employer and employee portions that a traditional employer would split with you.

A freelancer earning $50,000 in net profit owes roughly $7,065 in self-employment tax alone, before income tax. The IRS expects you to pay this throughout the year via quarterly estimated tax payments on Form 1040-ES, not in one lump sum on April 15.

Underpaying your quarterly estimates carries real consequences. If you don’t pay enough by the deadline each quarter, you’ll face penalties and interest, even if you ultimately owe nothing or get a refund at tax time.

The IRS sets four payment deadlines: April 15, June 17, September 16, and January 15 of the following year. To calculate what you owe, use your prior year’s tax return as a baseline and adjust for expected changes in income. If this is your first year freelancing, estimate conservatively-overpaying and receiving a refund beats underpaying and owing penalties.

Income reporting requires meticulous documentation because the IRS cross-references payments made to you against what you report. If a client pays you more than $600 in a year, they’ll likely send you a Form 1099-NEC, and the IRS receives a copy.

Report all income on Schedule C, regardless of whether you received a 1099. Keep detailed records of every invoice, payment, and bank deposit for at least three years. Accounting software like QuickBooks or FreshBooks automates tracking rather than relying on spreadsheets or memory. These tools categorize expenses in real-time, making tax season far simpler.

Separate your business and personal finances completely-open a dedicated business bank account and use it exclusively for client payments and business expenses. This separation proves invaluable if the IRS audits you, as it demonstrates organized record-keeping and reduces the risk of disallowed deductions.

One bright spot exists in the self-employment tax calculation: you can deduct 50% of your self-employment tax on Schedule 1, which lowers your overall tax burden. This deduction applies to all freelancers and reduces both your income tax and self-employment tax liability.

Understanding these obligations sets the foundation for effective tax planning. The next section covers the specific deductions and credits that directly reduce what you owe, turning your business expenses into real tax savings.

The gap between what you earn and what you keep hinges on deductions. Most freelancers leave money on the table by either missing deductions entirely or claiming expenses that don’t qualify. Your home office deduction alone can reduce taxable income by hundreds or thousands of dollars annually.

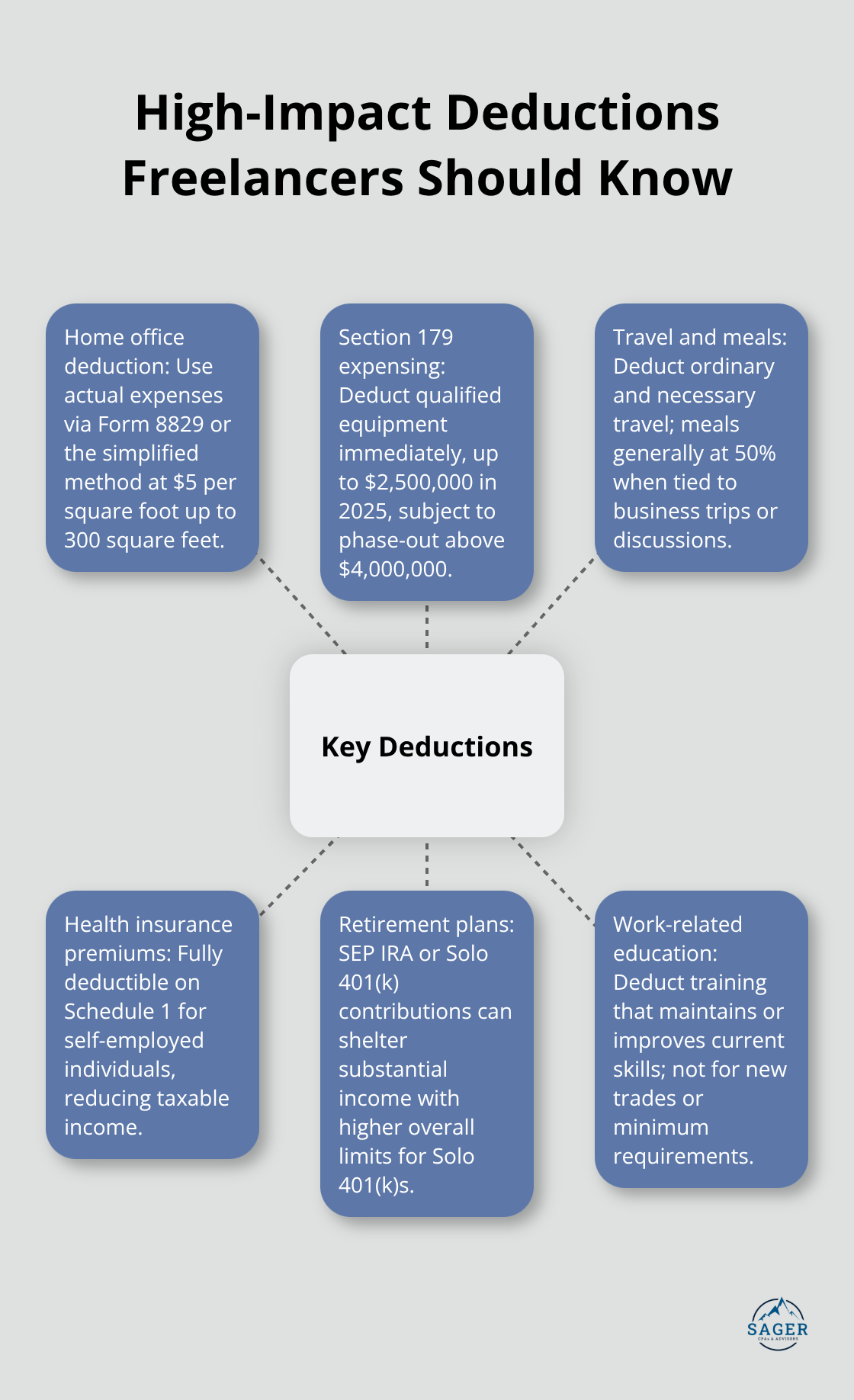

If you use a dedicated space exclusively for business, you can deduct either actual expenses like a portion of rent, mortgage interest, utilities, and internet using Form 8829, or claim the simplified method at $5 per square foot up to 300 square feet. The simplified approach works well if your actual costs are modest, but calculate both methods to see which saves more.

Equipment like computers, furniture, and software depreciates over time. Section 179 expensing allows you to deduct up to $2,500,000 in 2025 for qualified property, though this phases out above $4,000,000 in purchases. Many freelancers miss this because they think equipment must be depreciated over years rather than deducted immediately.

Business travel expenses are deductible if ordinary and necessary for your work, covering airfare, lodging, transportation, and even meals at 50% of actual costs according to IRS rules. The key distinction: the trip’s primary purpose must be business-related, and personal days mixed in don’t disqualify the entire expense.

Meals directly related to business discussions or on business trips qualify at that 50% rate, but entertainment expenses face stricter scrutiny now. Health insurance premiums for self-employed individuals are fully deductible on Schedule 1, which is powerful because it reduces both income tax and self-employment tax liability. For 2025, benchmark silver plans cost around $477 monthly nationally according to Centers for Medicare and Medicaid Services data, though rates vary significantly by state.

Retirement contributions through a SEP IRA or Solo 401(k) are deductible and allow you to shelter substantial income while building retirement savings. SEP IRAs let you contribute up to 25% of net self-employment income, while Solo 401(k)s permit both employee and employer contributions with higher overall limits. Start a retirement plan early to compound your tax savings over time and force discipline around setting aside funds rather than spending all profits.

Work-related education that maintains or improves your current skills is deductible as a business expense, so professional certifications, software training, or industry conferences qualify. Education that prepares you for a new trade or meets minimum job requirements doesn’t qualify, so verify the purpose before claiming it.

The foundation of maximizing deductions is documentation. Keep receipts, invoices, mileage logs, and bank statements for three years minimum because the IRS will ask for proof if audited. Tools like QuickBooks automatically categorize expenses and flag deductible items, reducing the mental load of remembering what qualifies.

Many freelancers operate on thin margins where a few hundred dollars in missed deductions translates directly to taxes owed. The self-employed health insurance deduction particularly matters because it applies to premiums up to your net business profit, meaning high-income freelancers can shield significant income from taxation.

Bad debts from unpaid client invoices are deductible if you previously included the income in your tax return, though you must have used the accrual method to qualify. This protection matters for freelancers who chase late payments or deal with clients who disappear. The difference between claiming deductions strategically versus haphazardly can easily amount to thousands in annual tax savings.

Treating tax planning as a year-round process rather than a spring scramble fundamentally changes your financial outcome. The next section covers how to organize your finances so that deductions flow naturally from your business records rather than requiring frantic searches through old receipts.

A separate business bank account is non-negotiable, yet many freelancers skip this step and mix personal and business money in one account. The IRS views commingled finances as a red flag during audits, and auditors will scrutinize whether expenses were truly business-related or personal spending disguised as deductible costs. Open a dedicated business account immediately, even before your first client payment arrives. Use it exclusively for client invoices and business expenses, never for groceries, rent, or personal bills. This single decision eliminates the tedious work of separating transactions later and provides clear evidence that you run an organized operation. Most banks offer free or low-cost business checking accounts, so cost isn’t a barrier.

Tracking income and expenses year-round transforms tax season from chaos into routine. Most freelancers wait until February or March to gather receipts, invoices, and bank statements, then frantically try to reconstruct nine months of financial activity. This approach guarantees missed deductions and errors that cost real money. Instead, spend 15 minutes weekly logging expenses into QuickBooks or FreshBooks as they occur. These tools automatically categorize transactions, flag deductible items, and generate reports that feed directly into your tax return.

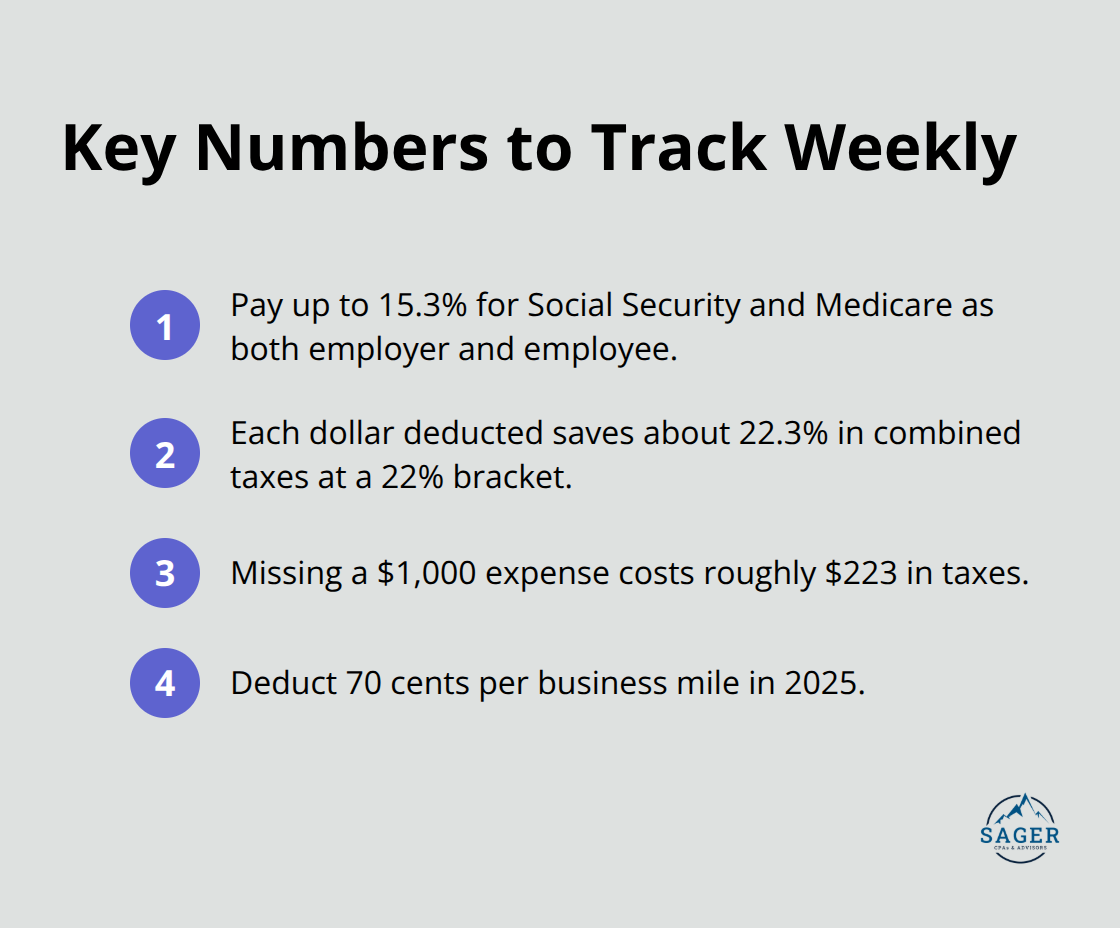

As a self-employed individual, you’ll pay up to 15.3% for Social Security and Medicare taxes, since you’re considered both employer and employee. Every deduction you capture saves you roughly 22.3% of that amount in combined federal and self-employment taxes (assuming a 22% marginal income tax bracket). A $1,000 expense you miss costs approximately $223 in taxes. Track mileage in real-time using a simple spreadsheet or app like MileIQ, because the 70 cents per mile deduction for 2025 adds up quickly if you drive for client meetings, errands, or site visits.

Keep receipts digitally by photographing them or using expense-scanning apps that attach files directly to transactions. This approach eliminates the cardboard box of crumpled receipts and creates an audit trail that satisfies IRS requirements. Digital records prove far easier to organize, search, and present if the IRS requests documentation. Your accounting software becomes the single source of truth for your finances, reducing confusion and preventing duplicate entries or missed transactions.

A tax professional who understands freelance income transforms your entire tax strategy. A CPA or tax advisor familiar with self-employment can identify deductions you’d never find on your own, structure your business entity to minimize taxes, and advise on estimated payment adjustments when your income changes mid-year. The cost of professional help typically ranges from $1,500 to $3,500 annually for straightforward freelance situations, but that investment often pays for itself through deductions and strategies a professional identifies.

Many freelancers resist hiring a professional because they fear the expense, but the alternative is leaving thousands in tax savings unclaimed and exposing yourself to audit risk from missed deductions or incorrect estimated payments. A qualified tax advisor provides peace of mind and ensures you comply with all filing requirements while maximizing your after-tax income.

Tax planning for freelancers isn’t a once-a-year scramble in March-it’s a continuous process that starts the moment you land your first client and continues through December. Self-employment tax will consume 15.3% of your net income whether you plan for it or not, and quarterly estimated payments prevent penalties and interest that compound your tax burden. A separate business bank account and weekly expense tracking eliminate the chaos of tax season and prove your legitimacy if audited.

Every deduction you capture saves roughly 22% in combined federal and self-employment taxes, so missing a $5,000 deduction costs you $1,115 in taxes. Home office deductions, business travel, health insurance premiums, and retirement contributions aren’t optional extras-they form the foundation of reducing what you owe. Proactive tax management also reduces stress and audit risk because you know exactly what you owe each quarter and face no surprises on April 15.

Open a business bank account this week, set up QuickBooks or FreshBooks, and schedule a consultation with a tax professional who understands freelance income. We at Sager CPA specialize in helping freelancers and self-employed individuals build tax strategies that work and start keeping more of what they earn.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.