How to Develop an Effective Business Level Strategy

Develop a business level strategy that drives competitive advantage, boosts profitability, and positions your company for sustainable growth in your market.

Small business owners often leave thousands of dollars on the table each year by missing deductions and tax opportunities. At Sager CPA, we’ve seen firsthand how the right small business tax strategy can transform your bottom line.

This guide walks you through actionable tactics to reduce what you owe, from everyday deductions to long-term planning moves that actually work.

Most small business owners capture the obvious write-offs-rent, supplies, payroll-but miss thousands in legitimate deductions that directly reduce taxable income. According to IRS Publication 334, you can deduct any ordinary and necessary business expense, which means the scope is far wider than many owners realize. The difference between a mediocre tax return and a strategic one comes down to knowing exactly what you can deduct.

The standard mileage rate for business vehicle use is 70 cents per mile in 2025, yet many owners either skip mileage tracking entirely or underestimate their actual business miles. If you drive 15,000 business miles annually, that’s $10,500 in deductions you can claim. Vehicle expenses, whether you use actual costs or the standard mileage rate, must be allocated precisely by business versus personal use-guessing here invites audit risk.

Home office deductions follow a strict exclusive-use test: your workspace must be used only for business. The simplified method lets you claim $5 per square foot up to 300 square feet without detailed expense tracking. A 200-square-foot home office generates a $1,000 annual deduction with minimal documentation.

Health insurance premiums for yourself and your family are fully deductible when you’re self-employed, a major advantage over W-2 employees who receive only partial employer coverage. This deduction applies to medical, dental, and vision insurance costs.

Retirement contributions are deductible dollar-for-dollar, and they rank among the highest-impact deductions available. A Solo 401(k) contribution limits 2024 allows up to $69,000 in total contributions, while a SEP IRA caps at 20% of net self-employment income. The key is setting up the plan before December 31 to claim deductions on that year’s return; contributions made after year-end on a tax-filing extension don’t qualify for the prior year.

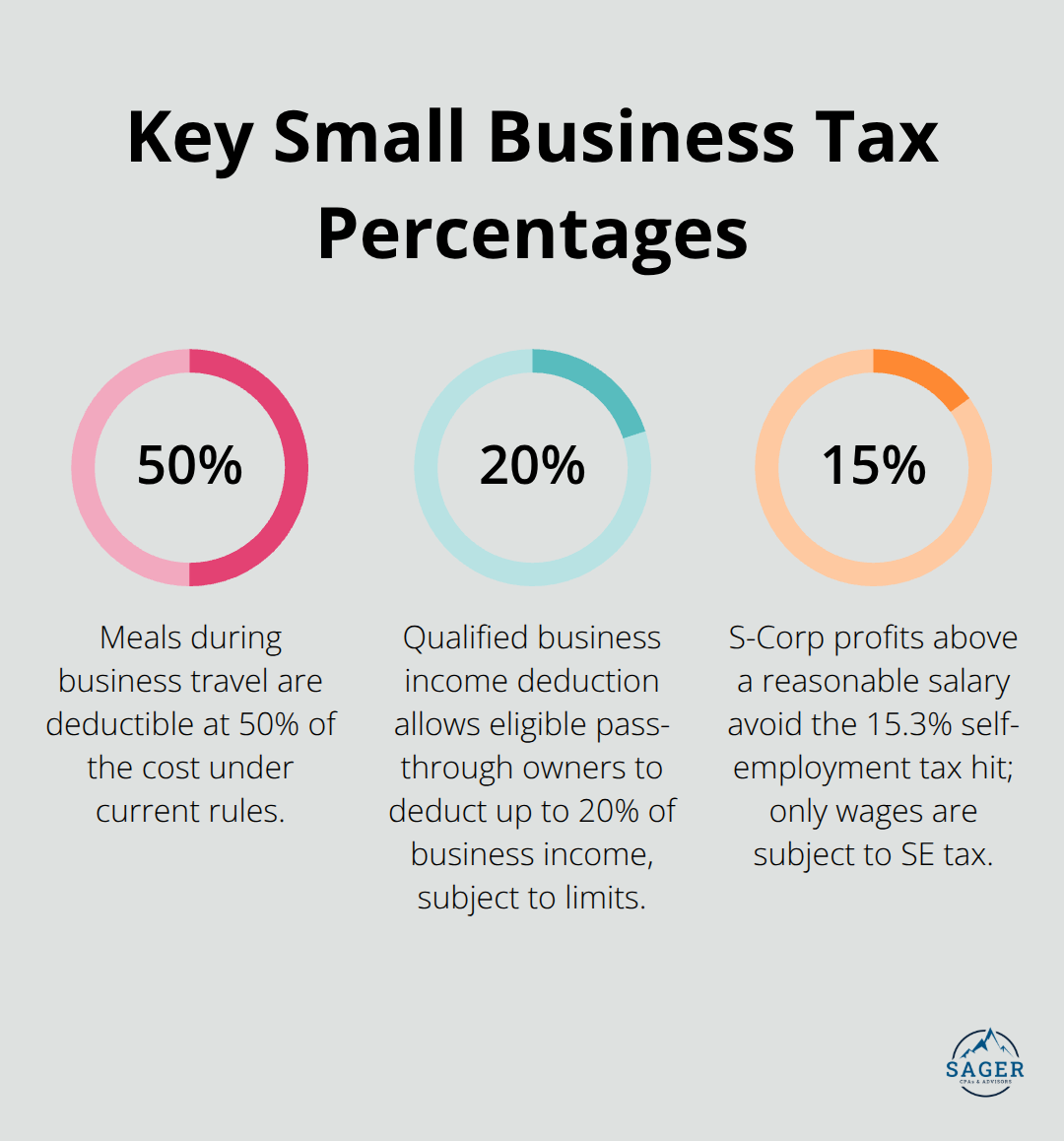

Employee salaries, bonuses, payroll taxes, and benefits are all deductible, but you must issue Forms W-2 and 1099-NEC by January 31 to avoid substantial penalties. Professional development, training, and business travel for employees count too. Meals during business travel are deductible at 50% of the cost under current rules, so tracking lodging and meal receipts separately matters.

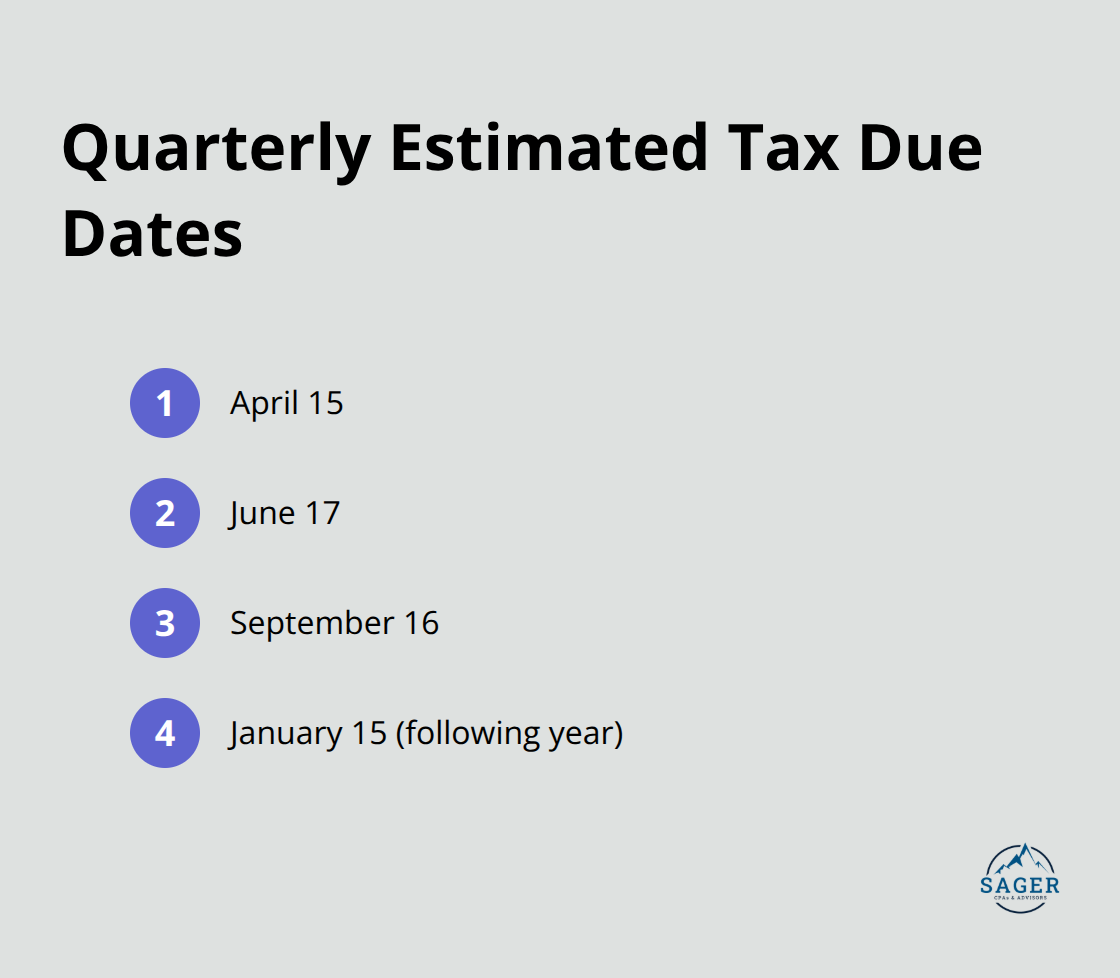

Most owners treat retirement plan setup as a tax-time afterthought rather than a year-round strategy. If you expect to owe $1,000 or more in tax, the IRS requires quarterly estimated payments using Form 1040-ES. You should adjust those payments mid-year if business income swings significantly. This is where proactive planning beats reactive filing-knowing your tax obligation quarterly lets you stash cash and make strategic expense decisions before year-end rather than scrambling in January.

Most small business owners treat estimated taxes as a chore they handle once a year, but the IRS demands quarterly payments if you expect to owe $1,000 or more in tax. These payments are due April 15, June 17, September 16, and January 15 of the following year. Missing even one deadline triggers penalties and interest that compound quickly. The real power of quarterly planning, though, isn’t compliance-it’s control. When you calculate what you actually owe every three months, you stop guessing about cash flow and start making deliberate decisions about expenses and income timing.

If your business had a strong Q1, you know exactly how much to set aside for taxes rather than spending profits that aren’t yours. If Q2 slowed down, you can adjust your Q3 payment downward using Form 1040-ES to avoid overpaying.

Estimated tax payments cover both income tax and self-employment tax. Self-employment tax includes Social Security taxes capped at $184,500 of combined wages and net earnings in 2026, though Medicare tax has no cap. If you earn $80,000 in net self-employment income, you owe roughly $12,240 in self-employment tax alone before income tax. Most owners underestimate this number because they forget to include it when calculating quarterly payments.

Use Form 1040-ES to work backward from your projected annual income, then divide by four. The math is straightforward: if you project $120,000 in net profit for the year, your federal income tax obligation might be $18,000 to $24,000 depending on other income and deductions, plus $12,240 in self-employment tax. Divide that total by four and you get your quarterly payment target. Pay through EFTPS or Direct Pay rather than checks-both are faster, documented automatically, and harder to lose.

Income doesn’t flow evenly across twelve months for most small businesses. Seasonal companies, consultants with lumpy project cycles, and retail owners all face months of feast and months of famine. Recalculate your estimated tax payment every quarter based on actual year-to-date income, not your January projection. If you run a landscaping business and Q1 generated $8,000 in revenue while Q2 brought in $45,000, your Q3 payment should reflect that actual trend, not a flat quarterly average.

The IRS allows you to use the annualized income installment method on Form 2210 if your income fluctuates significantly, which can lower penalties if you underpaid early quarters but overcompensated later. More importantly, adjusting mid-year gives you a concrete number to work with when deciding whether to accelerate a big client invoice or defer a discretionary expense. If you’re tracking toward a $150,000 profit year instead of your original $100,000 projection, you can front-load equipment purchases under Section 179 in November to reduce that tax hit. If business has slowed and you’re heading toward $70,000 instead, you might delay paying a vendor invoice or accelerate client collections to smooth cash across quarters.

Quarterly adjustments transform tax payments from a penalty you endure into a tool you control. Once you master this rhythm, you move from reactive filing to proactive planning-and that shift opens the door to the strategic moves that actually move the needle on your bottom line.

Your business structure is not a one-time decision you make when filing incorporation paperwork-it’s a tax lever you pull throughout the year. The structure you choose directly determines what you pay in self-employment tax, how much you can shelter in retirement plans, and whether you qualify for the 20% qualified business income deduction available to pass-through entities under current law. Most small business owners default to a sole proprietorship or basic LLC without understanding that a strategic shift to an S-Corp could save them $5,000 or more annually for businesses earning over $60,000 profit consistently.

If you’re netting over $60,000 per year and haven’t modeled an S-Corp election, you’re likely overpaying self-employment tax. An S-Corp requires you to pay yourself a reasonable salary, but profits above that salary avoid the 15.3% self-employment tax hit. A $100,000 net profit split as $50,000 salary and $50,000 distribution saves roughly $7,650 in self-employment taxes compared to a sole proprietorship. The IRS scrutinizes unreasonably low salaries, so you can’t pay yourself $20,000 and distribute $80,000, but a legitimate split based on industry standards and actual work performed holds up.

The setup cost is real-accounting fees run $1,500 to $3,000 annually for proper S-Corp administration-but the math works decisively for owners clearing $80,000 or more.

Pass-through entities also unlock access to the qualified business income deduction, which allows eligible owners to deduct up to 20% of business income, though service businesses like accounting, legal, and consulting face restrictions above certain income thresholds. If you’re in a restricted service business and hitting high income, a C-Corp might actually make sense despite the double-taxation concern, particularly if you’re planning an exit within five to ten years and can leverage the lower corporate rate strategically.

Timing income and expenses is where most owners fumble, treating it as an afterthought rather than a core planning tool. If you’re on the cash basis-which applies to most small businesses under $30 million in annual receipts-you control when income hits your tax return and when expenses reduce it. A client invoice sent December 28 that doesn’t get paid until January creates a full year of tax deferral on that income if you hold off on invoicing until January. Conversely, if you’re tracking toward a particularly strong year, accelerate discretionary vendor payments into December and front-load equipment purchases under Section 179 expensing or the 100% bonus depreciation now available for equipment placed in service after January 19, 2025. This directly reduces that year’s taxable income.

Section 179 lets you immediately deduct equipment purchases, with the threshold adjusted annually for inflation, meaning a $40,000 software system or machinery purchase can vanish from taxable income rather than depreciating over five years. The 100% bonus depreciation available through 2025 makes this year particularly attractive for equipment-heavy businesses. If your business is having a slower year and profits are expected to drop, the inverse strategy applies: delay vendor payments into January, accelerate customer collections, and postpone discretionary expenses to shift income recognition forward. The timing game works only if you’re disciplined about it and have visibility into your year-to-date performance by November. This is where quarterly planning directly feeds into year-end strategy-you already know your Q1 through Q3 numbers, so projecting Q4 and making deliberate moves beats guessing in December.

A CPA or tax strategist who meets with you quarterly catches opportunities you’d miss, flags audit risks before they happen, and models different scenarios before year-end when you still have time to act. Too many owners treat their accountant as a tax-return processor they see once a year, then wonder why they paid more than expected. A proactive engagement means your CPA reviews your profit-and-loss statement in October, identifies that you’re heading toward a higher-income year than projected, and recommends specific moves-perhaps maxing out a Solo 401(k) contribution with a profit-sharing component, or strategically timing a large equipment purchase.

The cost of quarterly advisory work typically runs $200 to $500 per month, but a single well-timed recommendation often pays for an entire year of engagement. Your tax professional also knows your industry’s benchmarks and can flag if your expense ratios look off, which often reveals either missed deductions or overspending. If other landscaping companies in your region are running 35% labor costs and you’re at 50%, that gap matters-it either means you’re missing deductions or you have an operational problem worth solving. The right CPA also stays current on law changes and knows which new incentives apply to your situation. The 2025 changes to bonus depreciation and Section 179 limits, the expansion of qualified small business stock eligibility, and shifts in charitable deduction rules for corporations all create planning opportunities that disappear if you’re not actively monitoring them.

Small business tax strategy compounds throughout the year when you implement it consistently, turning missed deductions into captured ones and reactive filing into deliberate planning. The tactics in this guide-tracking mileage precisely, timing equipment purchases around bonus depreciation rules, adjusting quarterly payments based on actual income, and choosing the right business structure-work only when you execute them month after month. Start with organized financial records so every deduction stands up to scrutiny, then move to quarterly planning so you know exactly what you owe and can make strategic decisions before year-end.

We at Sager CPA have watched owners recapture $8,000 to $15,000 annually simply by implementing quarterly planning and catching deductions they’d been missing for years. The gap between what you currently pay in taxes and what you could legitimately owe often runs into thousands of dollars, and that gap closes through consistent execution rather than one-time moves. Better records lead to better deductions, which free cash for growth, which creates more income to optimize strategically.

Your next step is straightforward: schedule a consultation with Sager CPA to build a personalized plan tailored to your business. We’ll review your current structure, identify immediate opportunities, and map out a year-round small business tax strategy that actually works. Transform your tax position from a burden into a competitive advantage.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.