Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Fiduciary tax planning presents unique challenges that can significantly impact estate and trust beneficiaries. The IRS collected over $4.2 billion from estate and gift taxes in 2023, highlighting the substantial financial stakes involved.

We at Sager CPA understand that trustees and executors face complex tax obligations with strict deadlines and severe penalties for non-compliance.

Strategic planning can reduce tax burdens by 15-30% while maintaining fiduciary responsibilities and protecting beneficiary interests.

Fiduciaries face distinct tax responsibilities that differ dramatically from personal tax obligations. Trustees must file Form 1041 for trusts that generate over $600 in annual income, while estates require the same form when gross income exceeds $600 or when any beneficiary is a nonresident alien. The American College of Trust and Estate Counsel reports that trusts with income above $14,450 face the top marginal tax rate, which makes income distribution timing essential for tax optimization.

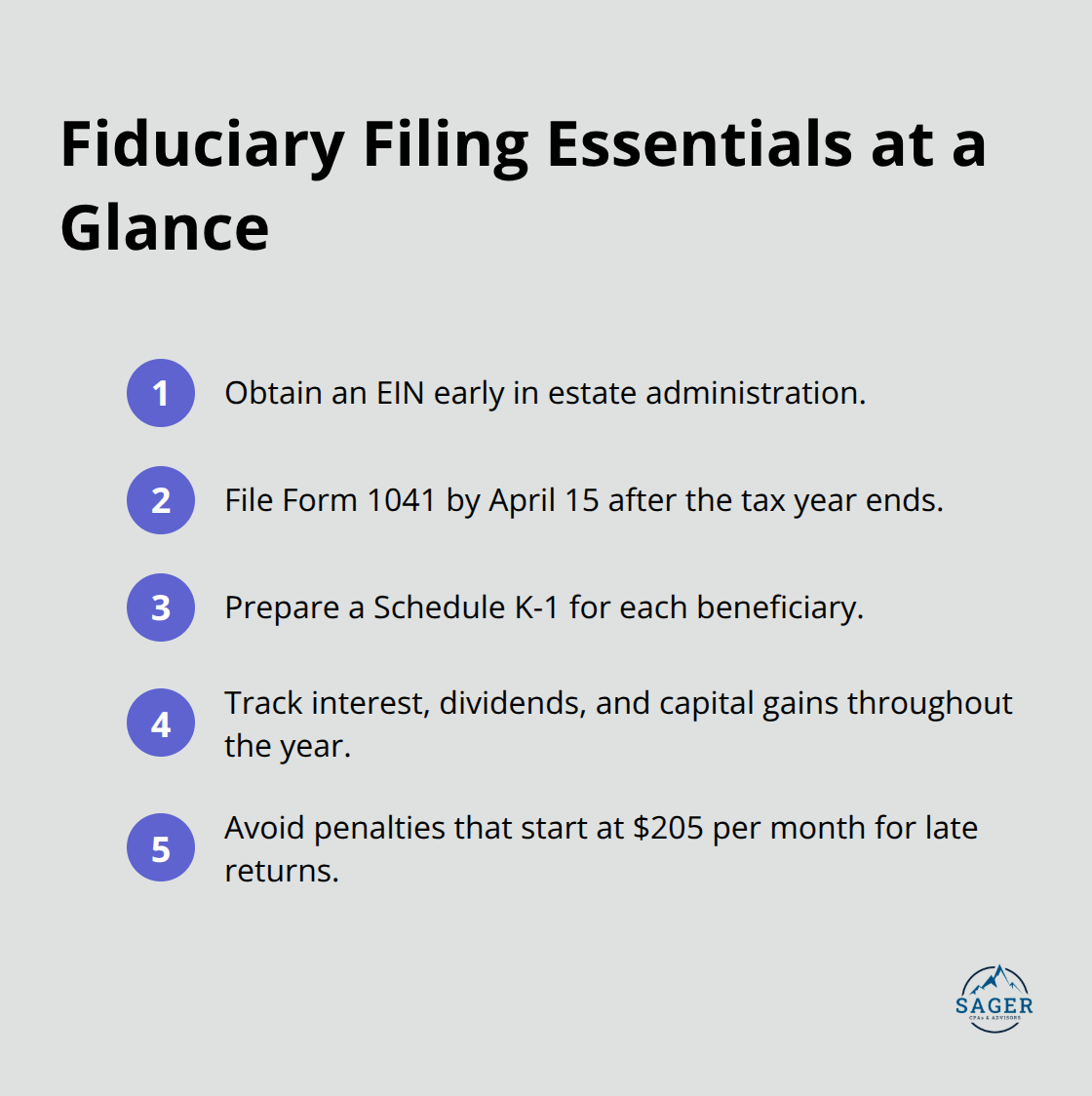

Trust income taxation operates under compressed tax brackets and reaches the highest rate at significantly lower income thresholds than individual returns. Executors must obtain an Employer Identification Number within the first few months of estate administration and file Form 1041 by April 15 after the tax year ends. The IRS imposes average penalties of $9,800 on fiduciaries who neglect tax obligations (according to 2023 reports).

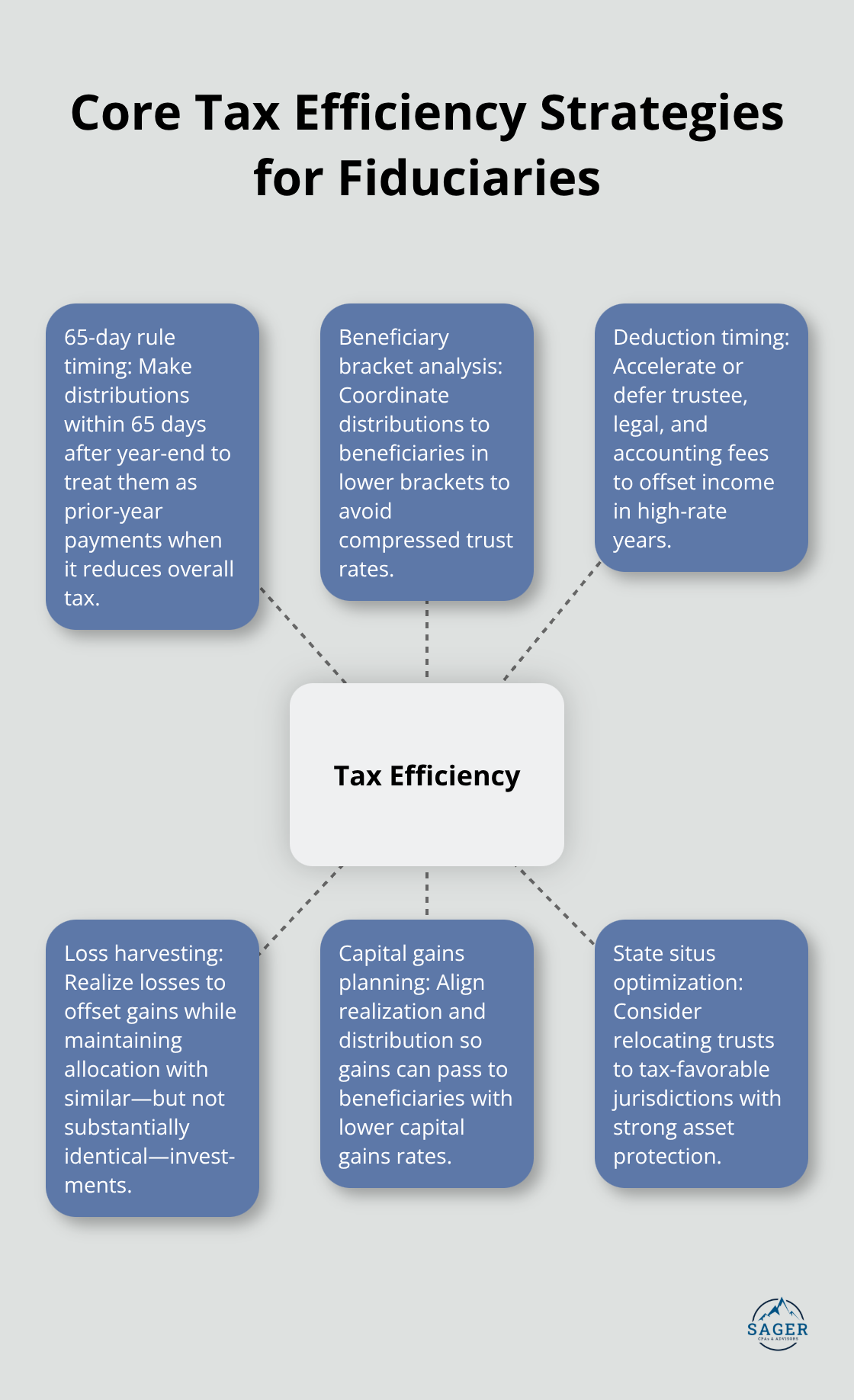

Smart fiduciaries leverage the 65-day rule, which allows distributions made within 65 days after year-end to count as prior-year distributions and provides strategic flexibility for tax planning.

Estate taxes apply to the transfer of wealth at death, while fiduciary income taxes affect trust operations on an ongoing basis. The federal estate tax exemption stands at $13.61 million per person in 2024, but fiduciary income taxes begin immediately when trusts generate income. Active tax planning reduces overall burdens by 15-20% compared to passive approaches through strategic distribution timing and deduction optimization. Fiduciaries must balance current tax minimization with long-term beneficiary tax consequences, particularly when beneficiaries face different tax brackets across various years.

Form 1041 requires detailed reporting of trust income, deductions, and distributions to beneficiaries. Fiduciaries must track all income sources, including interest, dividends, and capital gains throughout the tax year. The form also requires Schedule K-1 preparation for each beneficiary, which reports their share of trust income and deductions. Missing these deadlines triggers automatic penalties that start at $205 per month for returns filed late (with additional penalties for failure to provide beneficiary statements). These compliance requirements set the foundation for implementing effective income distribution strategies that maximize tax efficiency.

The 65-day rule provides fiduciaries with powerful flexibility to optimize tax outcomes across multiple years. Trustees can make distributions within 65 days after year-end and elect to treat them as prior-year distributions, which effectively allows retroactive tax planning. This strategy works best when beneficiaries experience different income levels across various years, as distributions can be timed to coincide with their lower tax brackets.

Distribution timing becomes particularly valuable when trustees manage the compressed tax brackets that trusts face. Since trusts reach high marginal tax rates at relatively low income levels, trustees who distribute income to beneficiaries in lower brackets can generate substantial tax savings. Fiduciaries should analyze each beneficiary’s projected annual income and coordinate distributions to avoid situations that push them into higher tax brackets unnecessarily.

Fiduciaries can claim various deductions that individual taxpayers cannot access, which include trustee fees, legal expenses, and accounting costs directly related to trust administration. These expenses must be ordinary and necessary for trust operation and cannot benefit individual beneficiaries personally. Investment management fees paid by trusts remain fully deductible, unlike the restrictions that apply to individual taxpayers under current tax law.

Administrative expense timing offers additional optimization opportunities. Trustees can accelerate or defer certain expenses to maximize their tax benefit in specific years. Professional fees for tax preparation, legal counsel, and investment management can be strategically timed to offset trust income when tax rates are highest.

Capital gains management requires careful coordination between realization timing and distribution strategies. Trustees should implement tax-loss harvesting throughout the year to offset capital gains, while they consider the step-up in basis benefits for inherited assets. The timing of capital gains realization can be coordinated with distribution plans to pass gains through to beneficiaries who may qualify for lower capital gains rates or have capital losses to offset the income.

Loss harvesting becomes particularly effective when trustees maintain diversified portfolios that generate both gains and losses throughout the year. Trustees can realize losses strategically to offset gains, then reinvest proceeds in similar (but not substantially identical) assets to maintain portfolio allocation while capturing tax benefits.

These foundational strategies set the stage for more sophisticated techniques that can further enhance tax efficiency through charitable vehicles and advanced trust structures.

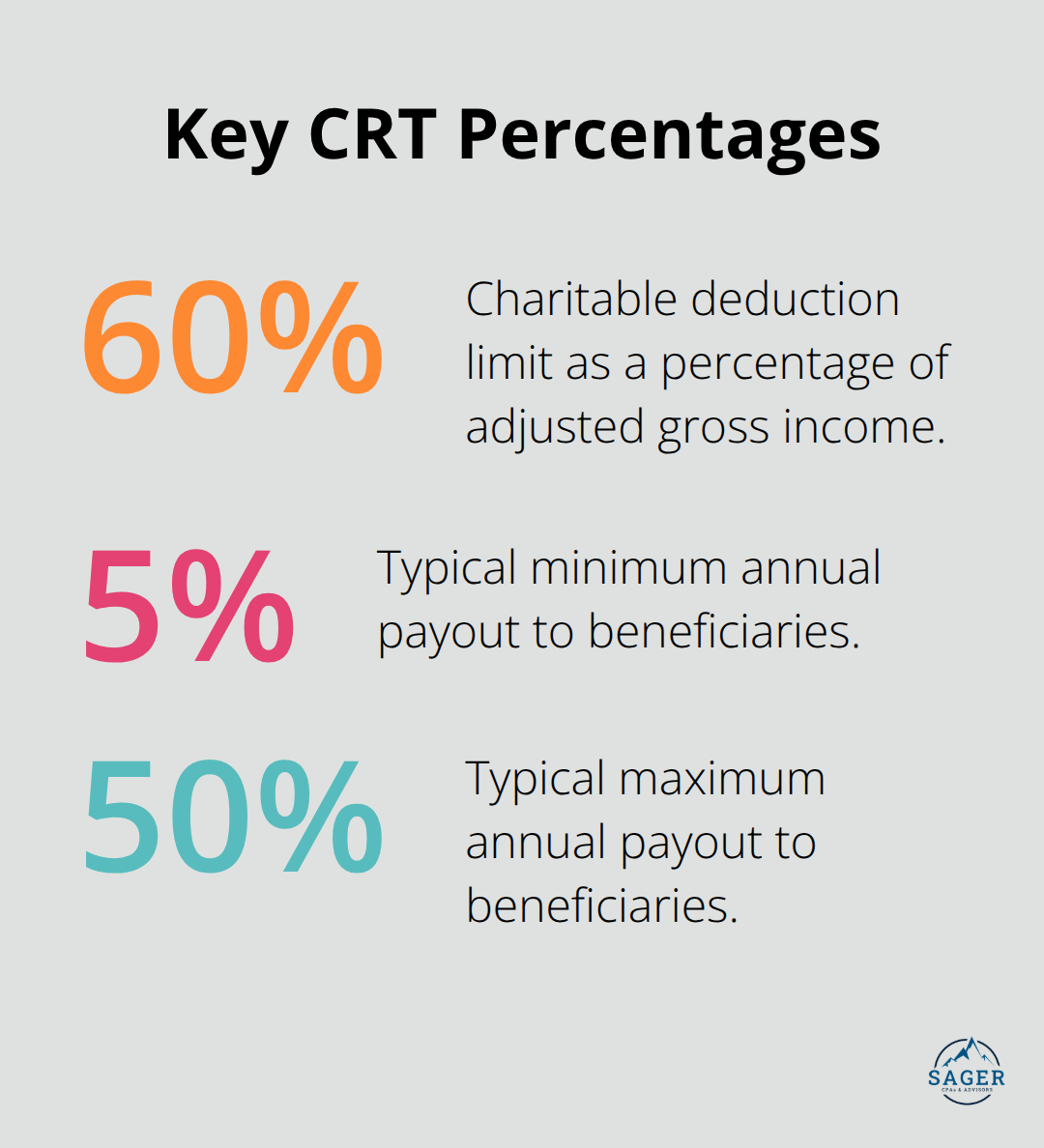

Charitable remainder trusts provide immediate tax deductions while they deliver lifetime income streams and substantial estate tax reductions. CRTs allow fiduciaries to donate appreciated assets worth millions while they avoid capital gains taxes on the transfer and receive charitable deductions up to 60% of adjusted gross income. The remainder interest passes to charity tax-free, while beneficiaries receive annual payments that typically range from 5% to 50% of trust assets.

These trusts work particularly well for highly appreciated assets that would otherwise trigger significant capital gains taxes. Donors can diversify concentrated stock positions through CRT structures while they maintain income streams and support charitable causes. The charitable deduction reduces current income taxes, and the trust pays no capital gains tax on asset sales within the structure.

Generation-skipping transfer tax planning becomes essential for wealthy families who transfer assets beyond one generation, as the GST tax rate reaches 40% on transfers that exceed the $13.61 million exemption in 2024. Dynasty trusts established in states without perpetuity rules allow wealth transfers that avoid GST taxes for multiple generations while they maintain asset protection benefits.

Families can allocate GST exemption amounts strategically across multiple trusts to maximize tax efficiency. Early allocation of exemption to assets with high growth potential multiplies the tax benefits over time. Trustees should coordinate GST planning with annual gift tax exclusions (currently $18,000 per recipient) to maximize wealth transfer opportunities.

State tax considerations create substantial planning opportunities since 34 states enacted tax changes that affect income and business taxes in 2024. Trust situs selection impacts tax liability dramatically – Nevada, Delaware, and South Dakota impose no state income taxes on trust income while they provide strong asset protection laws.

Trust migration to tax-friendly jurisdictions can save thousands annually for high-income trusts. Trustees must follow proper legal procedures when they relocate trusts, including court approval in some states and careful documentation of the administrative change.

Multi-state issues arise when trustees, beneficiaries, and trust assets span different jurisdictions, which requires careful analysis of each state’s taxation rules and potential conflicts. Fiduciaries who manage multi-state trusts should establish clear documentation that shows trust administration location and consider trust relocation to tax-friendly states when legally permissible.

Some states tax trusts based on beneficiary residence, while others focus on trustee location or asset situs. Professional guidance becomes essential for navigation of these complex interactions between federal regulations and varying state tax structures that can significantly impact overall tax liability.

Effective fiduciary tax planning requires mastery of income distribution timing, deduction optimization, and capital gains management to achieve the 15-30% tax savings that strategic planning delivers. The 65-day rule provides powerful flexibility for retroactive tax planning, while charitable remainder trusts and generation-skipping strategies offer sophisticated wealth transfer opportunities for high-net-worth families. State tax considerations add another layer of complexity, with 34 states that implemented tax changes in 2024 affecting trust taxation.

Multi-state coordination becomes essential when trustees, beneficiaries, and assets span different jurisdictions. Professional guidance proves invaluable given the compressed tax brackets trusts face and the $9,800 average penalties the IRS imposes on non-compliant fiduciaries (according to 2023 reports). The stakes remain high with over $4.2 billion collected from estate and gift taxes in 2023, which makes expert fiduciary tax planning essential for protection of beneficiary interests while tax burdens decrease.

We at Sager CPA provide comprehensive tax planning services that reduce liabilities through proactive strategies and customized action plans tailored for complex fiduciary situations. Our team understands the intricacies of trust taxation and helps fiduciaries navigate these complex requirements. Strategic fiduciary tax planning protects wealth and maximizes after-tax distributions for beneficiaries across multiple generations.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.