How to Reduce Your Tax Liability Legally

Reduce your tax liability legally with proven strategies. Discover deductions, credits, and planning techniques to lower your tax bill.

LLC tax strategies can make or break your business’s financial health. At Sager CPA, we’ve seen firsthand how the right approach can lead to significant savings and growth opportunities.

This guide will walk you through key strategies to optimize your LLC’s tax position, from choosing the right tax classification to maximizing deductions and strategically splitting income. Let’s dive into the essentials of effective LLC tax planning.

The IRS classifies single-member LLCs as disregarded entities for tax purposes. This classification requires the owner to report the business’s income and expenses on their personal tax return (typically on Schedule C). Multi-member LLCs default to partnership taxation. In this case, each member must report their share of profits and losses on individual tax returns.

Many LLC owners choose to elect S Corporation status by filing Form 2553 with the IRS. This strategy can lead to significant savings on self-employment taxes. As an S Corp, owners pay themselves a reasonable salary and take the remaining profits as distributions, which don’t incur self-employment tax.

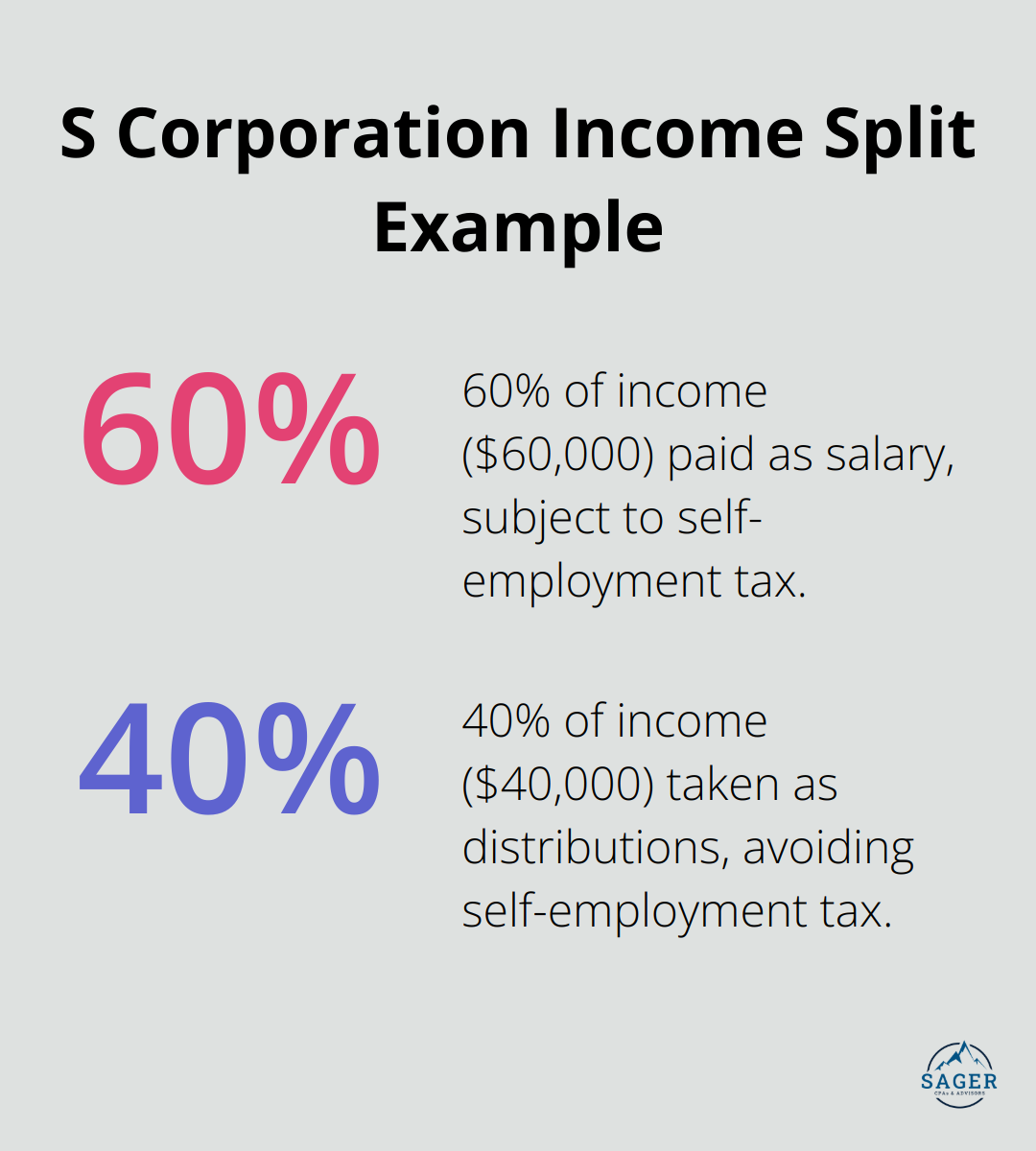

Consider this example: An LLC earns $100,000, and the owner pays themselves a $60,000 salary. Only the salary faces self-employment tax, while the remaining $40,000 (taken as a distribution) avoids this tax. This approach can result in thousands of dollars in tax savings.

Each tax classification offers unique advantages and challenges:

The IRS closely scrutinizes S Corporations, particularly regarding reasonable compensation. There are no specific guidelines for reasonable compensation in the Code or the Regulations, underscoring the importance of professional guidance.

When determining the most beneficial tax classification, consider:

Some businesses have saved over $10,000 annually by switching to S Corporation status. However, this decision depends on individual circumstances and requires careful analysis.

Tax classification decisions aren’t permanent. As businesses evolve, so should their tax strategies. Regular reviews with a tax professional help ensure that LLCs always leverage the most advantageous classification for their current situation.

Now that we’ve explored LLC tax classifications, let’s move on to another critical aspect of tax strategy: maximizing deductions. Understanding how to properly claim deductions can further reduce your tax burden and improve your LLC’s financial health.

LLCs can significantly reduce their tax burden through strategic deduction planning. This chapter explores key areas where you can optimize your deductions and potentially save thousands in taxes.

The IRS allows LLCs to deduct ordinary and necessary business expenses. This includes office supplies, professional fees, and marketing costs. However, many LLC owners overlook less obvious deductions. Bank fees, software subscriptions, and even certain entertainment expenses can be deductible if properly documented.

One often-missed deduction is the cost of continuing education related to your business. To be deductible, your expenses must be for education that maintains or improves skills needed in your present work, or is required by your employer or the law.

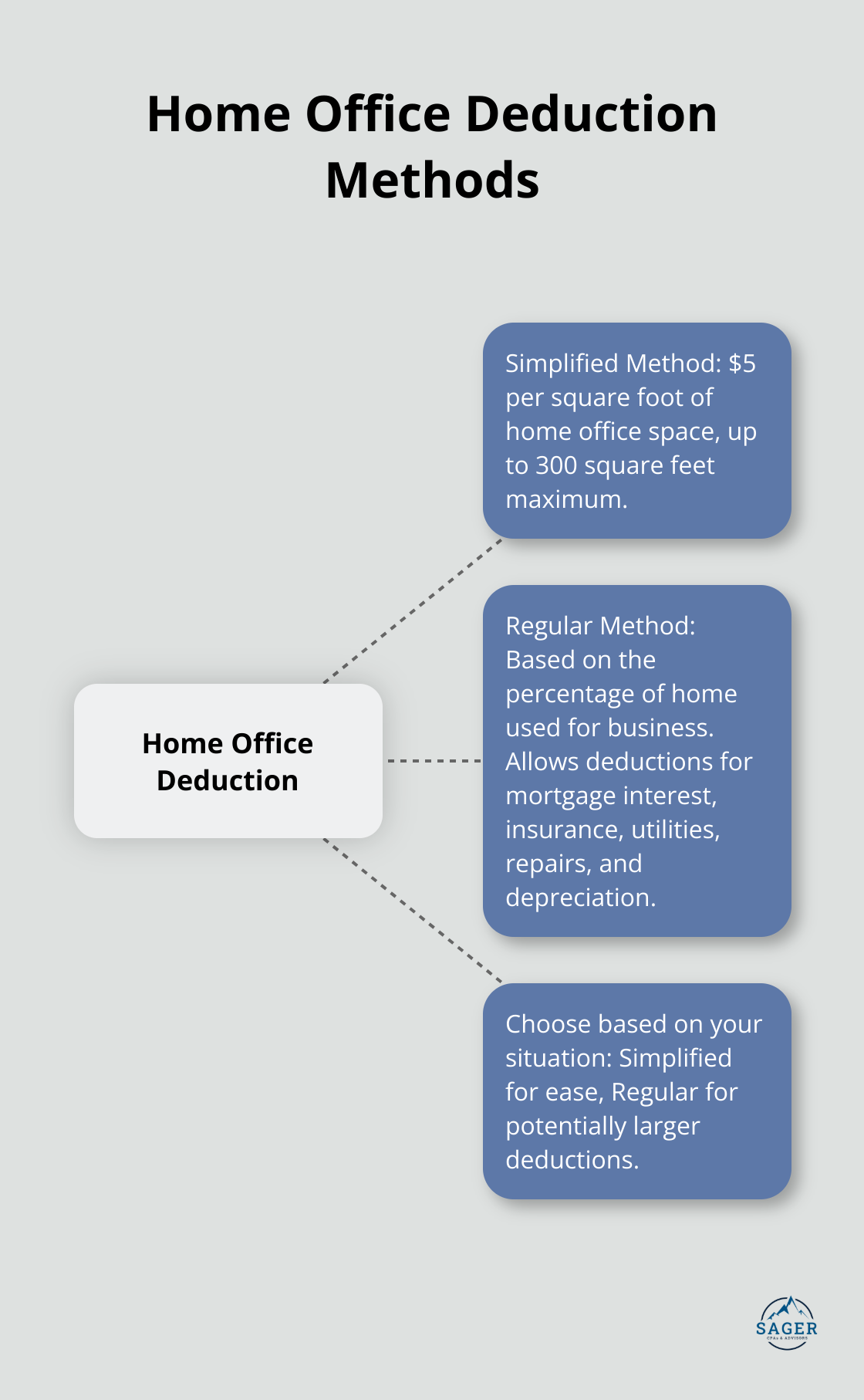

For LLC owners who work from home, the home office deduction can lead to substantial savings. The IRS allows you to deduct a portion of your mortgage interest, property taxes, utilities, and home insurance based on the percentage of your home used exclusively for business.

There are two methods to calculate this deduction:

The regular method is based on the percentage of the home devoted to business use. Taxpayers who use this method may be able to deduct mortgage interest, insurance, utilities, repairs, and depreciation.

Vehicle expenses can be a significant deduction for many LLC owners. The IRS offers two methods for claiming these expenses:

While the standard mileage rate is simpler, the actual expense method often yields higher deductions, especially for newer vehicles or those with high operating costs. Some businesses save up to $3,000 more annually using the actual expense method.

The IRS scrutinizes vehicle deductions closely, so accurate documentation is essential. Keep detailed logs of your business mileage and expenses to support your claims.

Tax laws are complex and ever-changing. A knowledgeable tax professional can help you take advantage of all available deductions while staying compliant with IRS regulations. They can also provide insights into industry-specific deductions you might not be aware of.

The next chapter will explore strategic income splitting for LLC owners, another powerful tool in your tax optimization arsenal.

For LLCs taxed as S corporations, finding the right balance between salary and distributions is essential. The IRS requires S corp owners to pay themselves a reasonable salary. To define “reasonable,” compare your salary to what you’d pay someone else to do your job.

Example: If the market rate for your position is $80,000, but your LLC earns $200,000, you might set your salary at $80,000 and take the remaining $120,000 as distributions. This strategy could save you thousands in self-employment taxes.

Timing plays a key role in tax planning. If you expect to be in a lower tax bracket next year, consider deferring income to that year. Conversely, if you anticipate being in a higher bracket, accelerate income into the current year.

For expenses, apply the opposite approach. Accelerate deductions into high-income years and defer them in low-income years when possible. This method can lead to substantial tax savings over time.

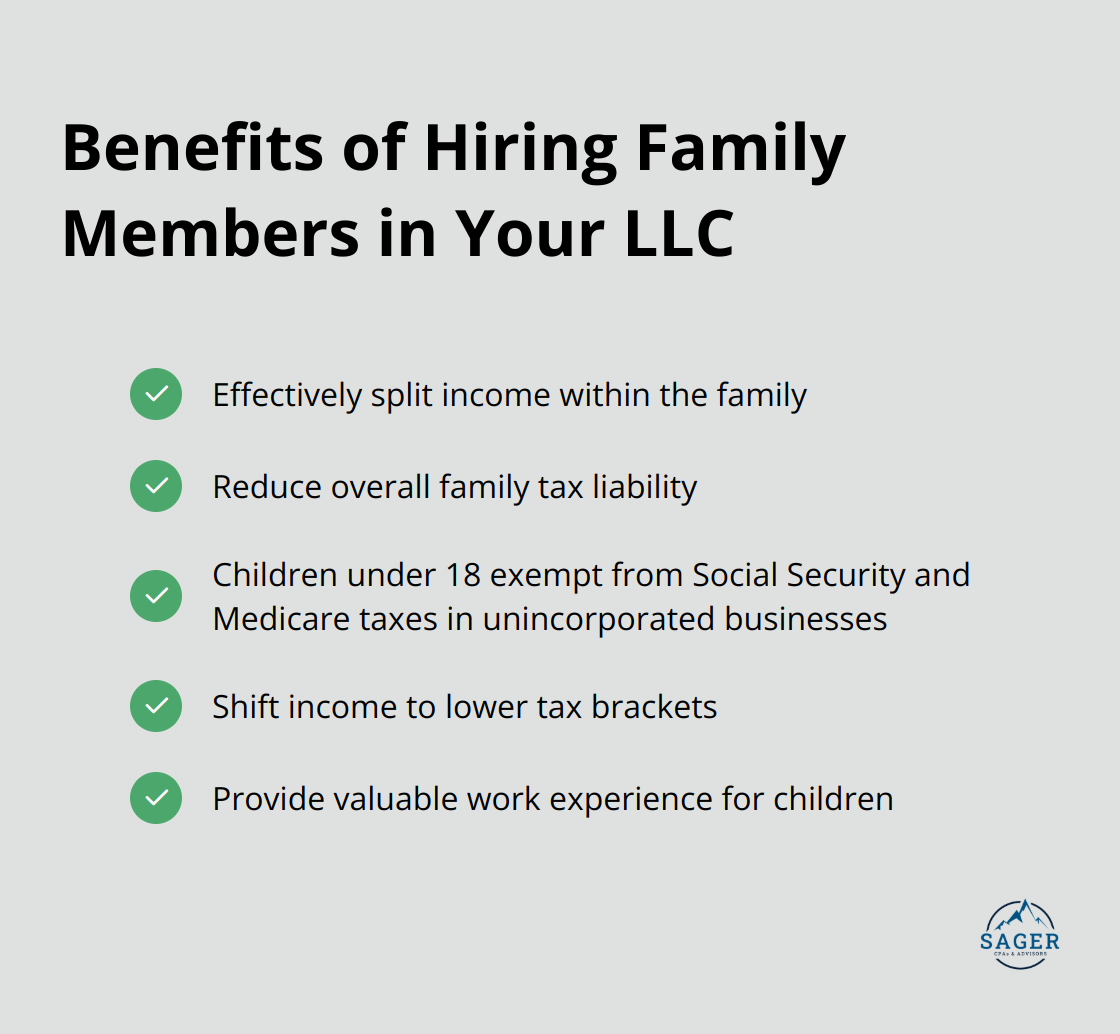

Hiring family members can effectively split income and reduce overall family tax liability. Children under 18 employed by their parents’ unincorporated business are exempt from Social Security and Medicare taxes. This strategy can shift income to a lower tax bracket while providing valuable work experience for your children.

It’s important to ensure that family members perform actual work and receive reasonable compensation. The IRS scrutinizes these arrangements closely, so maintain detailed records of hours worked and tasks performed.

Strategic use of retirement accounts can help LLC owners split income and reduce their tax burden. Consider setting up a Solo 401(k) or SEP IRA for your business. These accounts allow you to contribute significant amounts on a pre-tax basis. Contributions can be made to the plan in both capacities. The owner can contribute both elective deferrals up to 100% of compensation and employer nonelective contributions.

By maximizing contributions to these accounts, you can reduce your taxable income in high-earning years and defer taxes until retirement (when you may be in a lower tax bracket).

Implement income shifting techniques to potentially reduce your taxable income. While you’re responsible for self-employment taxes, LLC income provides opportunities to deduct business expenses. This can help lower your overall tax liability.

For example, if you own rental properties through your LLC, you could gift shares of the LLC to your children (subject to gift tax rules). The rental income would then be taxed at their (potentially lower) tax rates.

Effective LLC tax strategies can significantly impact your business’s financial health and growth potential. Understanding tax classifications, maximizing deductions, and strategically splitting income will optimize your LLC’s tax position. These strategies can potentially save you thousands of dollars annually, which you can reinvest in your business’s growth.

Professional tax advice proves invaluable when navigating the complex landscape of LLC tax strategies. Tax laws change frequently, and what works for one business may not be optimal for another. Sager CPA specializes in creating tailored tax strategies that align with your unique business goals and circumstances.

Successful LLC tax strategies focus on smart, legal tax optimization rather than aggressive tax avoidance. Staying informed, seeking professional guidance, and consistently applying these strategies will position your LLC for financial success both now and in the future. The long-term benefits of effective tax planning for LLCs extend beyond immediate savings (providing financial flexibility for business expansion and increasing your competitive edge).

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.