How to Reduce Your Tax Liability Legally

Reduce your tax liability legally with proven strategies. Discover deductions, credits, and planning techniques to lower your tax bill.

At Sager CPA, we know that effective business tax strategies can make or break a company’s financial health. Many business owners overlook the power of smart tax planning, potentially leaving money on the table.

This blog post will guide you through key tax strategies that can help your business thrive. We’ll show you how to implement these strategies and maximize your tax savings, setting your company up for long-term success.

Tax strategies for small business form the cornerstone of financial success for companies of all sizes. These strategies represent carefully planned approaches to manage a company’s tax obligations while maximizing profits. They don’t involve tax evasion; instead, they focus on making smart, legal decisions that benefit your bottom line.

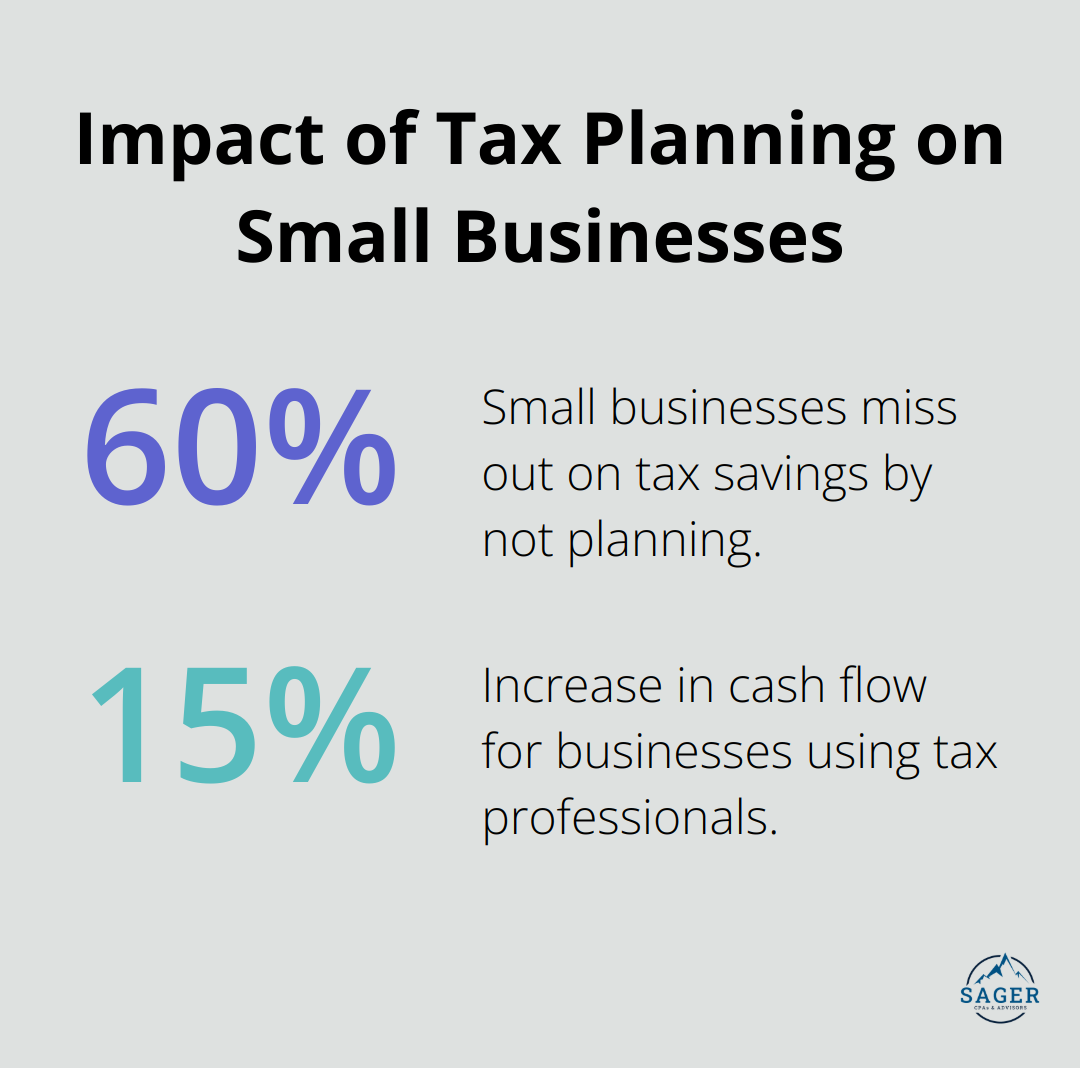

Tax planning isn’t exclusive to large corporations. Small businesses can reap significant benefits from effective tax strategies. Over 60% of small businesses miss out on these savings by not planning. Those who use professionals see 15% more cash flow. Keeping personal and business finances separate is crucial for accurate tax planning.

Many people mistakenly believe that tax strategies only benefit the wealthy or inherently involve risk. This couldn’t be further from the truth. The IRS actually encourages taxpayers to utilize available deductions and credits. A U.S. Government Accountability Office survey found that 70% of businesses overpay their taxes due to inadequate planning.

Another misconception is that tax planning occurs only once a year. Effective tax strategies require continuous attention and adjustments. The tax code changes frequently (the Tax Cuts and Jobs Act of 2017 introduced over 600 changes), and businesses evolve too. Staying current with these changes can lead to substantial savings.

While some tax strategies appear straightforward, others demand expert knowledge. The complexity of the tax code often means that do-it-yourself approaches leave money on the table. A National Society of Accountants study found that small businesses using professional tax preparers were more likely to take advantage of available deductions and credits.

Professional tax guidance doesn’t just save money on taxes; it also frees up time for business growth. Many business owners report spending 30% less time on tax-related tasks after partnering with tax professionals, allowing them to focus on revenue-generating activities.

As we move forward, let’s explore the key business tax strategies that can help your company thrive and maximize its financial potential.

Your business structure significantly impacts your tax obligations. Sole proprietorships face self-employment taxes, while S corporations can offer tax advantages through salary and distribution combinations. Like sole proprietors, S corporation owners are also eligible for the 20% pass-through tax deduction established under the Tax Cuts and Jobs Act for pass-through entities.

Consider this example: a business earning $100,000 as a sole proprietorship might pay $15,300 in self-employment taxes. The same business as an S corporation could potentially reduce that to $8,000 through strategic salary allocation. However, each structure has its pros and cons, so it’s essential to consult with a tax professional to determine the best fit for your specific situation.

The IRS offers numerous deductions and credits, but many businesses fail to take full advantage of them. Small business owners often overpay in taxes due to the wrong structure, missing out on strategic deductions, or triggering unnecessary tax events.

Some often-overlooked deductions include:

Don’t overlook tax credits either. The Research and Development (R&D) Tax Credit can provide significant savings for businesses engaged in innovation.

Timing plays a critical role in tax planning. You can potentially lower your tax bill by strategically managing when you recognize income and incur expenses.

For instance, if you expect to be in a lower tax bracket next year, consider deferring income to the following year. This could involve delaying billing for services rendered in December until January.

Conversely, if you anticipate being in a higher bracket next year, you might accelerate income into the current year and push deductible expenses into the following year.

These strategies require careful planning and should align with your overall business goals. Working closely with a tax professional can help you develop tailored timing strategies that optimize your tax position while supporting your business objectives.

Implementing employee benefit plans can serve dual purposes: attracting top talent and reducing your tax burden. Contributions to qualified retirement plans (such as 401(k)s) are tax-deductible for your business. Additionally, offering health insurance can provide tax benefits while supporting your employees’ well-being.

Tax laws evolve constantly. The Tax Cuts and Jobs Act of 2017 introduced over 600 changes to the tax code. Staying current with these changes can lead to substantial savings and help you avoid potential penalties. Consider subscribing to reputable tax publications or working with a tax professional who can keep you informed about relevant updates.

As you implement these strategies, you’ll not only save on taxes but also free up resources to invest back into your business and fuel growth. The next section will explore how to put these strategies into action effectively and sustainably.

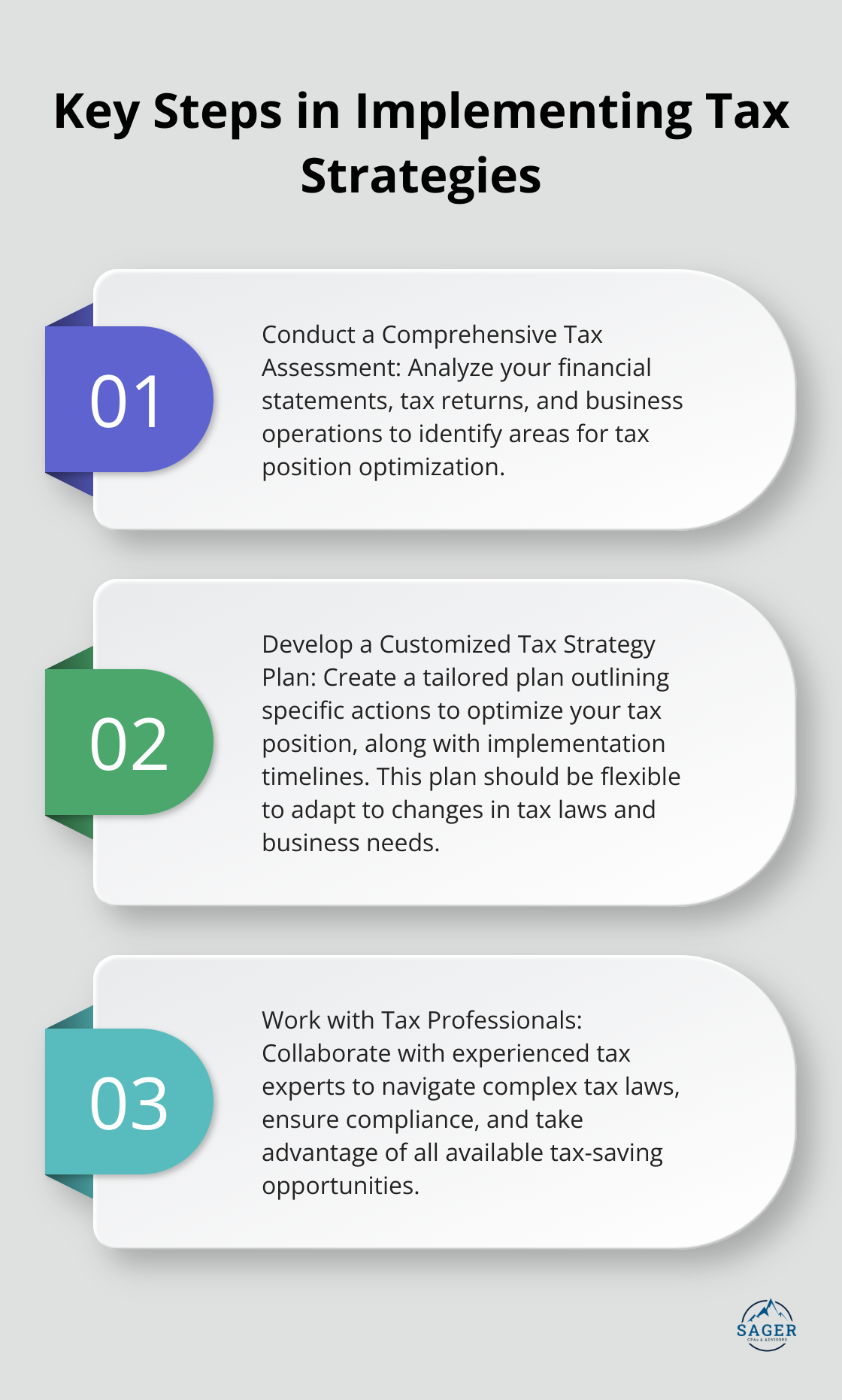

The first step to implement tax strategies requires a thorough assessment of your current tax situation. This process involves an analysis of your financial statements, tax returns, and business operations to identify areas for tax position optimization.

During this assessment, focus on your revenue streams, expense categories, and asset structure. Identify patterns in your cash flow and potential tax inefficiencies. You might discover that you don’t fully utilize available deductions or that your current business structure doesn’t optimize your tax situation.

A comprehensive tax assessment provides procedural guidance for Collection employees when securing, verifying, and analyzing financial information. This process can streamline tax-related tasks and potentially reduce time and resources spent on them.

After your assessment, create a tailored tax strategy plan. This plan should outline specific actions to optimize your tax position, along with implementation timelines.

Your plan might include strategies such as:

Your tax strategy plan should remain flexible. The tax landscape changes constantly, and your business needs may evolve. Prepare to adjust your plan to ensure it stays effective and compliant with current tax laws.

Implementation of some tax strategies on your own is possible, but collaboration with experienced tax professionals can significantly enhance your results. Tax experts provide valuable insights, help navigate complex tax laws, and ensure you take advantage of all available tax-saving opportunities.

When you select a tax professional, look for someone with experience in your industry and a track record of helping similar businesses. They should proactively suggest strategies and keep you informed about relevant tax law changes.

The tax landscape evolves constantly, with new laws, regulations, and court decisions that impact tax strategies regularly. Awareness of these changes proves essential to maintain an effective tax strategy.

Consider a subscription to reputable tax publications, attendance at industry seminars, or membership in professional associations related to your field. These resources can provide valuable insights into emerging tax trends and strategies.

Don’t hesitate to revisit and adjust your tax strategies as your business grows and changes. A startup’s effective strategies may not work for a mature business. Regular reviews of your tax strategy (ideally quarterly) can help ensure continuous optimization of your tax position.

Implementation of effective tax strategies requires dedication and expertise, but the potential benefits are substantial. These steps and work with experienced professionals can create a tax strategy that reduces your tax burden and supports your overall business goals.

Effective business tax strategies create a foundation for long-term financial success. They optimize your business structure, maximize deductions and credits, and time income and expenses strategically. These strategies reduce your tax burden and free up resources for growth and innovation, improving cash flow and enhancing profitability.

A comprehensive tax assessment will give you a clear picture of your current situation and help identify areas for improvement. Develop a customized tax strategy plan that aligns with your business goals and takes advantage of available tax-saving opportunities. Work with experienced tax professionals to navigate complex tax laws and identify opportunities for tax savings.

At Sager CPA, we offer expert financial management and tax planning services tailored for individuals and businesses. Our team can help you develop strategies that support your long-term financial goals. Take the first step today by assessing your current tax situation and exploring opportunities for optimization.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.