Business Owner Retirement Planning: Strategy for a Secure Exit

Plan your business owner retirement with proven strategies for a secure exit and financial freedom ahead.

Most business owners spend decades building something valuable, then rush the exit without a plan. We at Sager CPA see this mistake repeatedly, and it costs owners hundreds of thousands in unnecessary taxes and lost value.

Business owner retirement planning isn’t just about picking a date to step away. It’s about structuring your exit so you keep more of what you’ve earned.

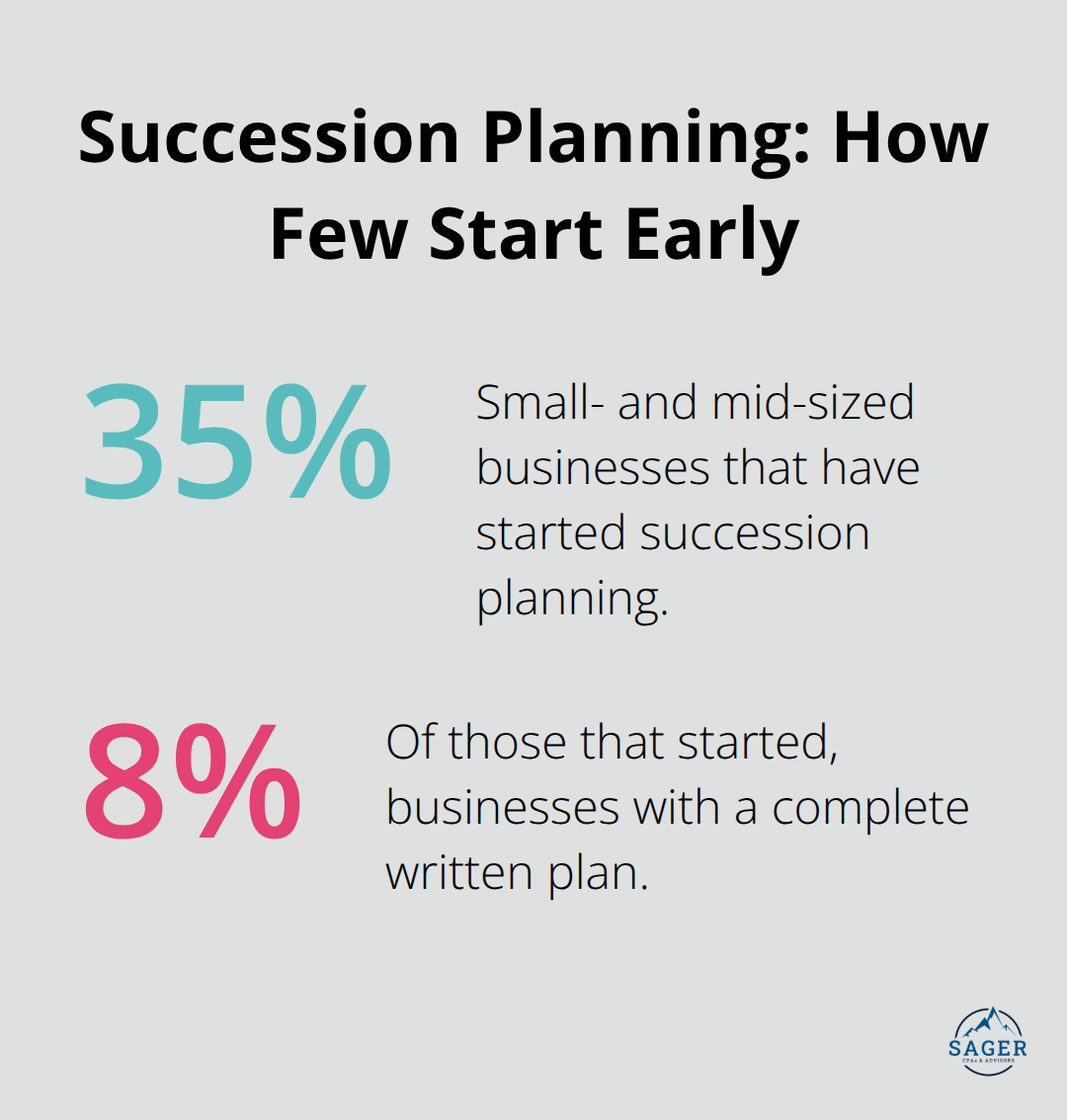

Most business owners wait until their 50s or 60s to think seriously about retirement, and the damage compounds quickly. According to MassMutual research, only 35% of small- and mid-sized businesses have started succession planning at all, and just 8% of those have a complete written plan. This delay costs money immediately. When you postpone planning, you miss years of tax optimization, you cannot groom internal successors, and you face a fire-sale situation when you finally decide to exit.

The first mistake is timing itself. Planning your exit five to ten years before you want to leave gives you room to restructure, reduce tax exposure, and find the right buyer. Waiting until you’re already burned out means accepting whatever offer comes your way.

The second mistake is mixing personal and business finances. Many owners treat their business bank account like a personal checking account, pulling cash for personal expenses and paying personal bills from the business. This creates three immediate problems: your financial statements become unreliable, buyers lose confidence in your numbers, and the IRS gets suspicious. When you sell, buyers want three to five years of clear P&L statements, balance sheets, and tax returns that reconcile to actual cash flow. If your finances are tangled, you either spend months cleaning them up or you sell at a discount because the buyer cannot trust your profitability numbers.

The third and most expensive mistake is ignoring tax planning during the sale itself. A business sale can trigger capital gains tax at the federal level, plus an additional 3.8% Net Investment Income Tax for higher incomes, and state income taxes on top of that. A $2.5 million sale with $1.45 million in gains can cost over $425,000 in combined federal and state taxes if structured poorly. Structured installment sales, governed by IRS code sections 453 and 453B, let you defer gains over multiple years and often avoid the Net Investment Income Tax entirely, saving over $188,000 in the example above. The difference between a tax-aware exit and a tax-ignorant one is the difference between retiring comfortably and retiring stressed about money.

The longer you wait, the fewer options you have. If you’re under 55 and thinking about exiting in ten years, you can build internal talent, optimize your financials, and structure a sale for maximum tax efficiency. If you’re 62 and want to leave in two years, you’re stuck with whoever is willing to buy quickly. Open a separate business bank account if you haven’t already. Stop using the business to pay personal bills. Document all business expenses. This single step makes your financials attractive to buyers and gives you a clear picture of what your business actually earns.

Talk to a tax advisor two to three years before you plan to exit. Structured installment sales, asset versus stock sales, timing strategies, and depreciation recapture all matter. The right structure can save six figures. Your next step is to determine what your business is actually worth-and that valuation shapes every decision that follows.

Valuation transforms exit strategy from abstract planning into concrete numbers. Without knowing what your business is worth, every other decision lacks direction. Start with earnings or cash flow multiples, the standard approach for most businesses. For retail and grocery operations specifically, valuators typically use EBITDA (earnings before interest, taxes, depreciation, and amortization) or seller’s discretionary earnings as the foundation, then apply multiples that vary by location, profitability, growth rate, and risk. A stable, predictable net income attracts buyers most. If your business shows erratic cash flow or high variance year to year, expect a lower multiple.

Real estate adds another layer to your valuation. If you own the building your business operates from, you may value the property separately using cap rate analysis and comparable sales, then add the business value for total enterprise value. This distinction matters because selling with land versus selling as a tenant with a lease attached changes pricing, buyer type, and financing options entirely.

Organized financials are non-negotiable for credible valuation. Buyers demand three to five years of P&L statements, balance sheets, tax returns, and documentation showing how those numbers reconcile to actual cash flow. Without this documentation, you either spend months cleaning up records or accept a discount because the buyer cannot trust your profitability claims. Hire a professional valuator or broker with experience in your industry to obtain an objective valuation and market feedback. This costs money upfront but prevents thousands in lost value from a low-ball offer or a misaligned asking price.

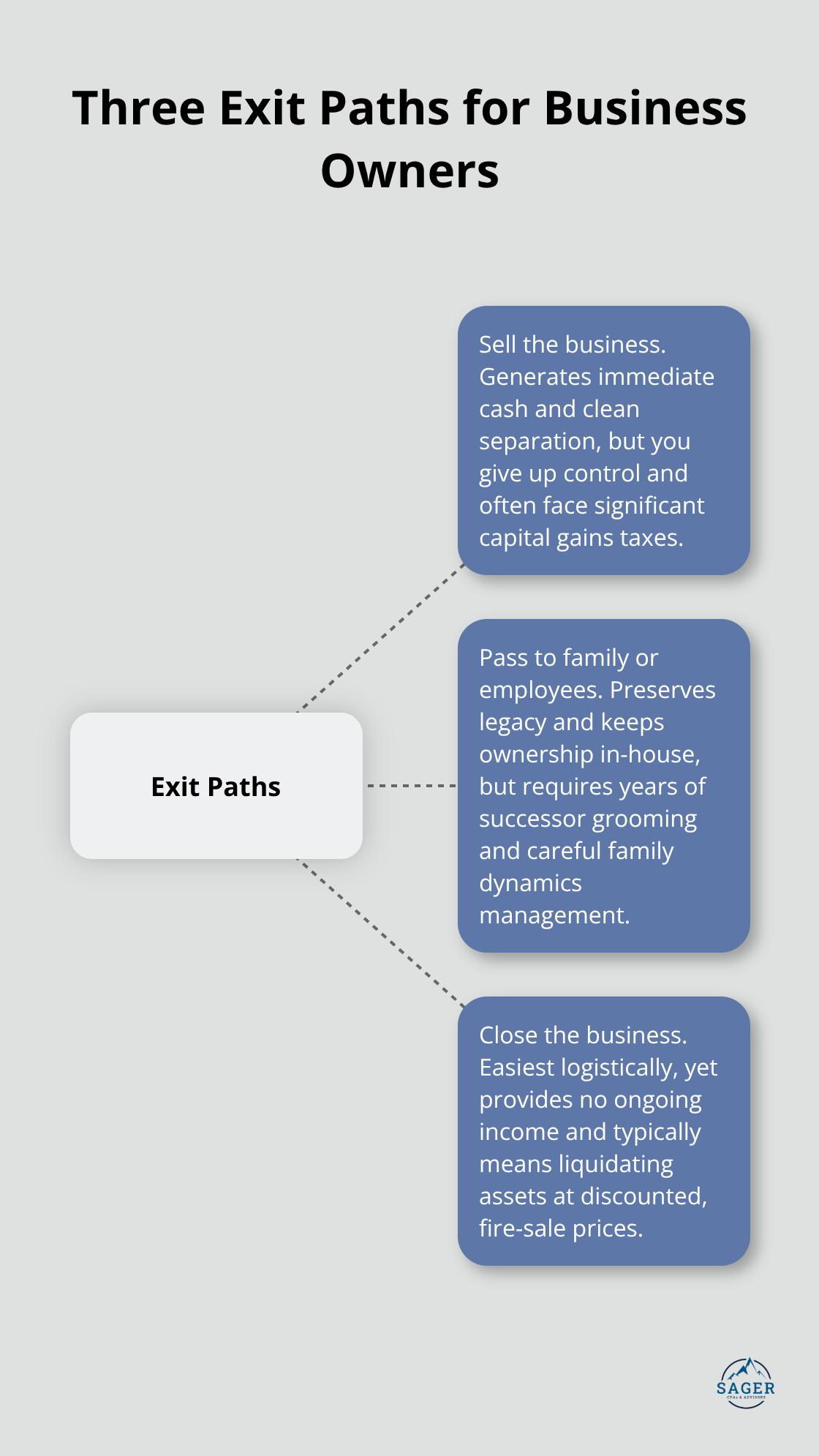

You have three fundamental choices: sell the business, pass it to family or employees, or close it down. A sale generates immediate cash and creates clean separation, but it means losing control and typically triggers significant capital gains tax. Passing the business down preserves legacy and keeps ownership in the family, but requires grooming a successor over years and managing family dynamics around fairness and capability. Closing the business is the easiest logistically but offers no ongoing income and means liquidating assets, often at fire-sale prices.

Most owners assume they want to sell, but that assumption deserves scrutiny. If you have a family member or key employee capable of running the operation and willing to buy in, a transition to them may preserve more wealth than selling to an outside buyer. If you have no capable successor and no buyer interest emerges after reasonable effort, closing becomes the realistic path, though you should start that process two years out to wind down operations methodically rather than abruptly.

The difference between retiring on your terms and retiring because you burned out is often just five years of planning. Start now, whatever your age. If you’re under 55 with a ten-year horizon, your timeline should include two to three years of financial cleanup and operational optimization, three to five years of successor development if you’re considering a family or employee transition, and two to three years of active marketing and negotiation if you’re selling. If you’re 60 and want to exit in five years, compress the optimization phase to one year and begin identifying buyers immediately.

Write the timeline down with specific milestones: in year one, clean up financials and separate personal from business accounts; in year two, optimize margins and document all systems; in year three, identify potential buyers or successors; in year four, begin active negotiations. A written timeline keeps you accountable and forces realistic assessment of whether your target date is actually achievable given your current situation.

The timeline you establish shapes which exit path is viable. A ten-year horizon gives you time to build internal talent, optimize operations, and attract serious buyers. A two-year horizon eliminates the succession option and forces either a quick sale or closure. Define your target retirement date first, then work backward to determine which exit path actually fits your circumstances. Once you know what your business is worth and which path you’ll take, the next critical step is structuring that exit to keep as much money as possible in your pocket.

The moment you sell your business, the tax bill arrives whether you’re ready or not. A $2.5 million sale with $1.45 million in gains triggers roughly $239,493 in federal capital gains tax, approximately $45,600 in Net Investment Income Tax for higher earners, and potentially over $141,000 in state income tax depending on where you live, totaling more than $425,000 in taxes if you structure the deal poorly. Structured installment sales change this equation entirely. Instead of receiving the full payment upfront and paying taxes on the entire gain in year one, you can have the buyer’s payments flow to an assignment company, which funds an annuity with the lump sum and then pays you according to a schedule you define.

This approach, governed by IRS sections 453 and 453B, defers your capital gains tax across multiple years and often eliminates the Net Investment Income Tax entirely because your annual income drops below the thresholds that trigger it. In the same $2.5 million example, spreading payments over 20 years reduces your annual federal capital gains tax to roughly $5,819, eliminates NIIT completely, and lowers state taxes to about $6,061 per year, saving over $188,000 compared to a lump-sum sale.

The insurer funding your annuity must have strong financial strength to guarantee payouts decades from now. Verify ratings from agencies like A.M. Best, Moody’s, and Fitch before committing. Metropolitan Tower Life, for instance, carries ratings of A+ from A.M. Best, Aa3 from Moody’s, AA- from Fitch, and AA- from S&P, reflecting the stability you need for long-term payouts. Consult IRS Topic No. 409 and Publication 537 for tax-specific guidance, and work with a tax advisor to determine whether your assets qualify for installment treatment, since inventory and securities traded on established markets do not qualify.

The structured sale process requires coordination with your legal and tax advisors at least 18 months before closing to identify eligible assets, decide your payout schedule, and finalize the agreement. This isn’t just tax optimization; it’s the difference between a retirement income stream that covers your expenses and one that leaves you stressed about money.

Your retirement security depends on assets that aren’t tied to one operation. Most business owners concentrate 70 to 80 percent of their net worth in the business, leaving little cushion if market conditions shift or unexpected expenses arise. Start building diversified retirement savings now through plans suited to your business structure. A solo 401(k) lets you and your spouse contribute up to $69,000 each in 2024 if your business has few or no employees, offering higher contribution limits than a SEP IRA and lower administrative burden than a traditional 401(k). A SEP IRA works well for self-employed individuals and businesses with employees, letting you contribute up to 25 percent of net self-employment income with a $69,000 annual cap in 2024. A traditional 401(k) provides the highest contribution limits and flexible plan design that attracts employees, though administrative costs run higher.

Diversify investments within these accounts using low-cost mutual funds and ETFs rather than concentrating in company stock or real estate alone. This strategy reduces your exposure to any single asset and creates multiple income streams in retirement.

Healthcare costs after retirement demand specific planning because Medicare doesn’t cover long-term care, and nursing home costs average $100,000 to $150,000 annually depending on your location and care level. Long-term care insurance purchased before age 60 costs significantly less than waiting until 65 or 70, so evaluate policies now while you’re still healthy and insurable. If you own real estate alongside your business, a sale-leaseback arrangement where you sell the property to the buyer but lease it back can provide ongoing passive income while eliminating the property management burden, creating a second revenue stream in retirement that reduces reliance on investment returns alone.

Business owner retirement planning succeeds when you act now, not when retirement feels imminent. The three mistakes we covered-waiting too long, mixing personal and business finances, and ignoring tax structure-cost owners hundreds of thousands in avoidable taxes and lost value. You cannot undo these mistakes after the sale closes, so the time to address them is today.

Your exit strategy rests on three concrete decisions: knowing what your business is worth, choosing between selling, passing it down, or closing, and structuring that exit to minimize taxes. A professional valuation gives you the numbers to work with, a written timeline with specific milestones keeps you accountable, and structured installment sales can save six figures in capital gains and Net Investment Income Tax. Diversified retirement savings beyond your business reduce your exposure to a single asset, while long-term care planning protects your retirement income from unexpected healthcare costs.

Start building your succession plan now if you have a family member or key employee capable of running the business, separate your personal and business finances immediately if you haven’t already, and talk to a tax professional about whether a structured installment sale makes sense for your situation. We at Sager CPA work with business owners to build exit strategies that protect their wealth and create the retirement they’ve earned. Schedule a consultation with us to create a personalized financial strategy tailored to your business, your timeline, and your retirement goals.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.