Financial Advisory for Owners: Strategic Guidance for SMBs

Discover strategic financial advisory for business owners to optimize cash flow, reduce taxes, and grow your SMB profitably.

Most small business owners focus on operations and sales, leaving financial strategy as an afterthought. This gap costs real money-poor financial decisions drain resources that could fuel growth.

Financial advisory for owners isn’t a luxury reserved for large corporations. At Sager CPA, we’ve seen how strategic guidance transforms the way SMBs manage cash, reduce taxes, and scale profitably.

Small business owners face a harsh reality: 45% of businesses fail within five years and 65% fail within ten years, according to the U.S. Bureau of Labor Statistics. The primary culprit isn’t lack of effort or poor products-it’s weak financial management. Most owners operate without a clear picture of their cash flow position, tax exposure, or growth capacity. They mix personal and business finances, miss tax deductions worth thousands annually, and make major decisions based on gut feeling rather than financial data. These aren’t minor inefficiencies. They’re wealth destroyers.

A business without financial clarity hemorrhages money through multiple channels. Owners don’t know their true profit margins because they haven’t separated business and personal expenses. They pay taxes inefficiently because they haven’t planned ahead for quarterly estimates or entity structure optimization. They hold onto cash that could fund growth because they can’t forecast cash flow accurately.

According to research from Equitable in partnership with SCORE, 83% of small business owners recognize the importance of working with a financial professional, yet most wait until crisis hits. This delay is expensive. Owners who lack strategic guidance often overpay taxes, miss growth opportunities, and struggle to attract or retain quality staff because they can’t offer competitive benefits packages. The math is simple: a business owner paying 15% more in taxes than necessary on $500,000 in revenue loses $75,000 annually. Over a decade, that’s $750,000 in lost wealth.

Owners who work with a financial professional retire seven years earlier than those flying solo, according to the same Equitable-SCORE study surveying 728 business owners. This isn’t because advisors wave a magic wand-it’s because strategic guidance creates compounding advantages. A financial professional helps you implement a proper cash flow system, identifying where money actually goes and where it gets stuck. They structure your entity to minimize tax burden legally. They align your salary and distributions with both tax efficiency and retirement savings. They help you evaluate whether to reinvest profits into growth or take distributions.

SMBs working with financial professionals are three times more likely to hire new workers and five times more likely to implement employee retention strategies. They’re twice as likely to offer comprehensive benefits that attract talent. These aren’t accidents-they’re direct results of having someone who understands both your business and your financial goals working alongside you.

The difference between struggling and thriving often comes down to one factor: access to expert financial guidance. When you understand your numbers, you make better decisions about where to invest, how much to pay yourself, and which opportunities to pursue. This clarity transforms how you operate.

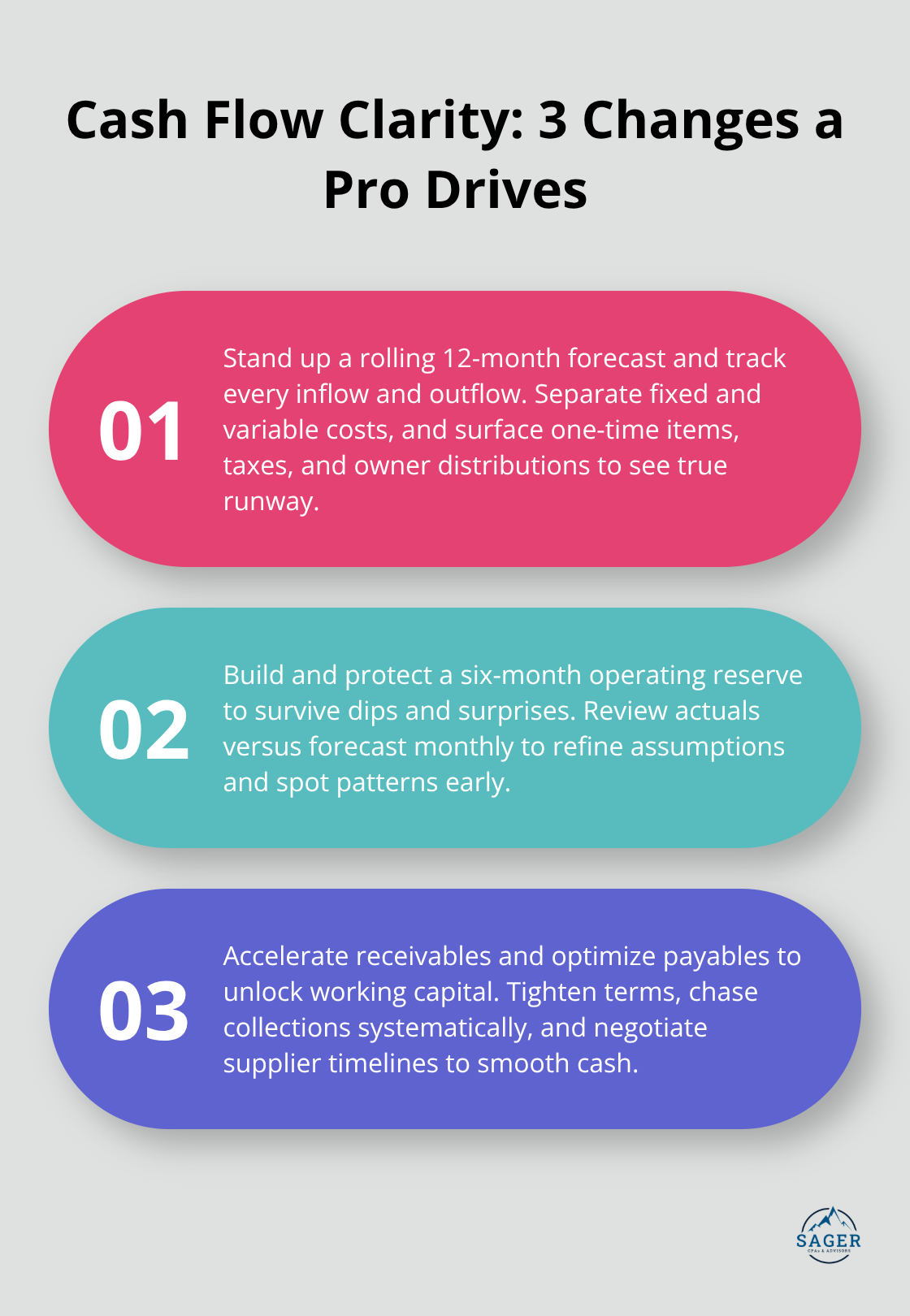

Cash flow is the heartbeat of every business, yet most owners treat it like a mystery. They know revenue comes in and expenses go out, but they can’t answer the critical question: where exactly is the money? This blindness costs thousands monthly. Owners who lack visibility often appear profitable on paper but can’t cover payroll because they haven’t forecasted cash flow beyond the current month.

Start by tracking every dollar in and out across a twelve-month rolling forecast. Separate fixed costs like rent and salaries from variable expenses that fluctuate with revenue. Include one-time purchases, tax payments, and owner distributions in your forecast. Most importantly, build a cash reserve covering at least six months of operating expenses. This isn’t theoretical advice-it’s survival.

When seasonal dips hit or an unexpected cost emerges, that buffer keeps you operational instead of scrambling for emergency financing. Monitor your cash position monthly using actual financial statements, not assumptions. Compare what you forecasted against what actually happened, then adjust next month’s projection. This feedback loop reveals patterns: which months drain cash, which generate surplus, and where you can tighten receivables or negotiate better payment terms with suppliers.

Many owners discover they’re extending credit too generously to customers while paying suppliers immediately. Reversing this dynamic-tightening how long customers have to pay while negotiating longer terms with suppliers-can free up tens of thousands in working capital without raising a single dollar in external financing. This shift alone transforms cash availability for operations and growth.

Tax planning separates owners who keep what they earn from those who overpay the government. Most businesses fail at this because they think tax planning happens in March when they file returns. Effective tax planning runs year-round, starting with understanding your entity structure. An S corporation can save significant money compared to a standard C-corporation or sole proprietorship, but only if set up correctly and maintained properly.

Safe Harbor rules for estimated quarterly tax payments require you to pay either 90% of current year taxes or 100% of prior year taxes (110% if prior year income exceeded $150,000) within the calendar year. Miss these deadlines and penalties compound quickly. Work with a tax professional to evaluate whether your current structure still makes sense as your business grows. Many owners operate in the wrong entity type simply because they never revisited the decision after launching.

Beyond entity structure, tax planning means identifying every legitimate deduction. Business owners commonly miss deductions for home office space, vehicle mileage, equipment depreciation, and health insurance premiums. The IRS allows these deductions, yet owners leave money on the table because they don’t track them systematically.

Growth strategy demands clarity on business valuation. You need to know what your business is actually worth, not just what you think it might fetch someday. A professional valuation identifies your true earning power, reveals which revenue streams are most profitable, and shows where you’re inefficient. This insight guides where to invest for growth.

If your margins in one service line are 40% while another sits at 15%, your growth capital should flow to the 40% business. Many owners waste resources chasing growth in the wrong areas simply because they never measured profitability by segment. Understanding these numbers transforms how you allocate capital and which opportunities you pursue next.

Choosing a financial advisor is not like hiring a plumber. A plumber fixes a specific problem and leaves. An advisor becomes a strategic partner in decisions that shape your business and personal wealth for decades. This means credentials matter, but they’re only the starting point. You need someone who has worked with businesses like yours, understands the tax environment you operate in, and charges in a way that aligns their incentive with your success. Most owners make this choice poorly because they focus on the wrong criteria or settle for whoever they meet first.

Start with credentials that carry real weight. A CPA designation requires passing a rigorous exam and maintaining continuing education, which matters far more than generic financial advisor titles that carry minimal requirements. If your business operates in a specific industry, find someone with documented experience in that sector. An advisor who has worked with construction companies understands job costing and lien issues. One who serves professional service firms knows how to structure owner compensation around client concentration risk.

When you interview potential advisors, ask directly: How many clients do you serve in my industry? What are the three most common financial mistakes you see owners in my space make? If they can’t answer specifically, they lack the depth you need.

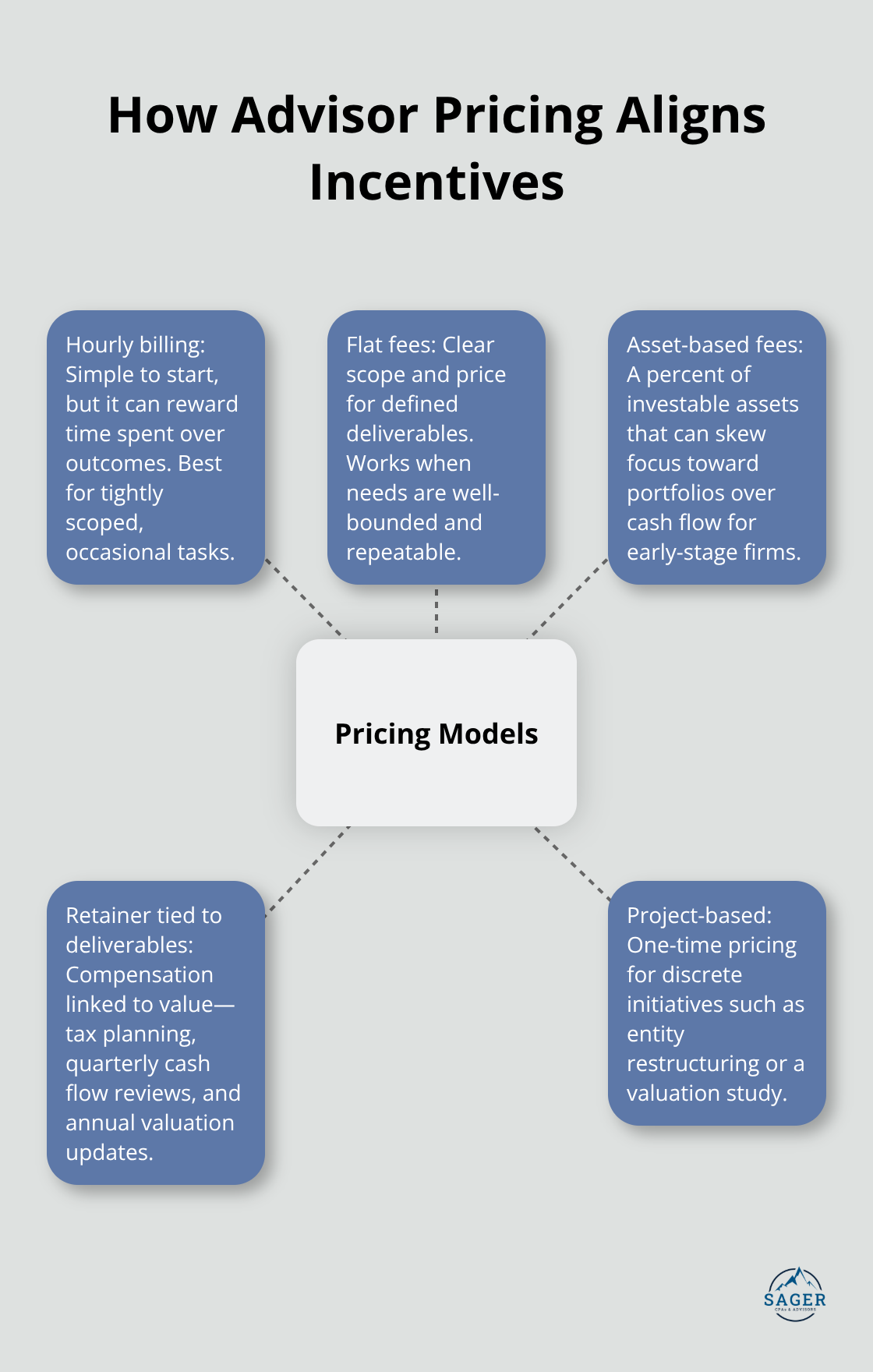

Pricing structure reveals whether an advisor’s interests align with yours. Hourly billing incentivizes lengthy meetings without necessarily delivering results.

Flat fees for specific services work well if your needs are defined, but ongoing advisory relationships function best under a model where the advisor’s compensation grows as your business grows and your financial complexity increases.

Asset-based fees charged as a percentage of investable assets can work, though they sometimes discourage advisors from prioritizing cash flow improvements that matter more than investment management for early-stage businesses. The clearest alignment happens when your advisor charges a retainer tied to specific deliverables: tax planning optimization, quarterly cash flow reviews, annual valuation updates, and strategic planning sessions. This structure means they profit when they help you succeed, not when they bill more hours.

Building the right advisory relationship requires clarity about what you actually need. Many owners think they need investment management when what they really need is tax planning and cash flow forecasting. Others need succession planning but settle for basic bookkeeping. Before you hire anyone, write down the three financial problems keeping you awake at night. Are you uncertain whether you’re paying yourself correctly? Do you lack visibility into true profitability? Are you worried about tax liability? Is retirement planning nonexistent?

Once you identify your real problems, find someone who specializes in solving those specific issues. A long-term advisory partnership works because the advisor learns your business deeply over time, spotting opportunities and risks you’d never see alone.

This depth takes years to develop, which is why switching advisors frequently costs you money through lost institutional knowledge and repeated discovery conversations. Try a three-year commitment before evaluating whether the fit is right. In that time, a quality advisor should help you implement systems that weren’t there before, identify tax savings worth more than their annual fee, and give you confidence in decisions you make. If after three years they haven’t delivered measurable improvements to your financial position, your cash flow visibility, or your tax efficiency, the relationship isn’t working.

Strategic financial guidance transforms how business owners operate. The owners who retire earlier, hire more confidently, and scale profitably aren’t smarter than those struggling-they simply have someone helping them see the numbers clearly. Financial advisory for owners isn’t about complex investment strategies or theoretical planning; it’s about understanding where your money actually goes, paying only the taxes you legally owe, and making growth decisions based on data instead of instinct.

The real impact shows up in your bank account and your peace of mind. When you implement proper cash flow tracking, you stop wondering whether you can make payroll. When you optimize your entity structure and plan taxes year-round, you keep thousands that would otherwise flow to the government. When you measure profitability by business segment, you invest growth capital where it actually generates returns.

Write down the three financial problems that worry you most and find an advisor who specializes in solving those specific issues. Look for a CPA credential, ask about their experience in your industry, and align on a pricing structure where their success depends on your success. Schedule a consultation with Sager CPA to discuss your specific situation and create a personalized financial strategy.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.