Financial Planning for Founders: Navigating Growth with Confidence

Build a sustainable financial strategy with our guide to financial planning for founders navigating rapid growth and scaling challenges.

Most founders focus on product and growth, leaving financial planning for later. That’s a mistake that costs businesses thousands in missed opportunities and preventable errors.

At Sager CPA, we’ve seen firsthand how early financial discipline separates thriving companies from those that struggle. This guide walks you through the financial decisions that matter most during your growth phase.

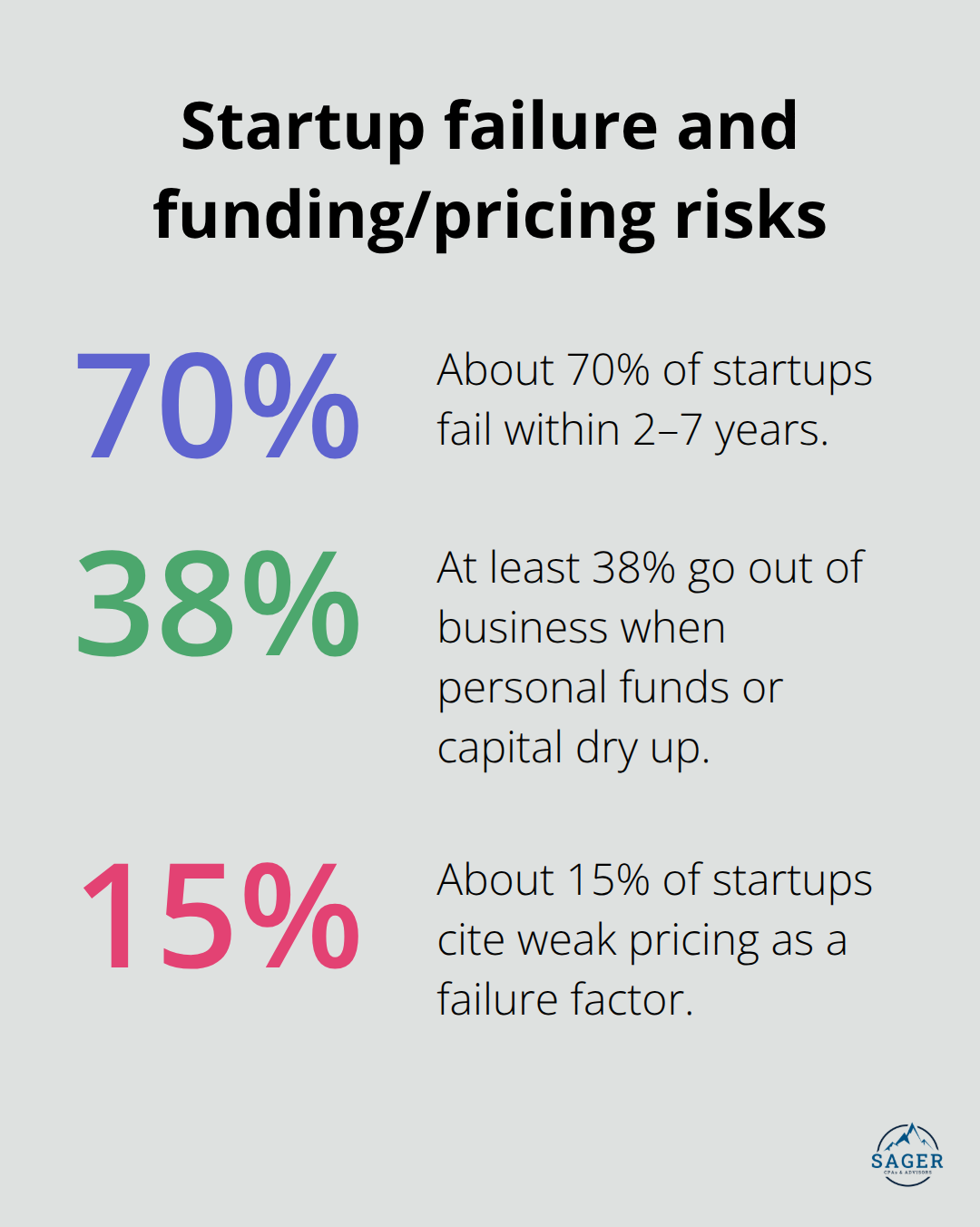

Cash flow timing kills more startups than bad products. About 70% of startups fail within 2–7 years, and funding gaps are a leading reason-at least 38% go out of business when personal funds run dry or capital dries up. The problem isn’t always that founders lack revenue. It’s that they don’t track when cash actually arrives versus when bills are due. During growth phases, this gap widens. You hire staff before revenue scales, buy inventory before customers pay, and rent office space before hitting profitability. Without a cash flow forecast updated weekly or daily, you won’t see the liquidity crunch until it’s too late.

Most founders operate on gut feel, watching their bank balance instead of modeling scenarios. That approach works until it doesn’t. The founders who survive build financial visibility early, separate fixed costs like salaries and rent from variable costs like commissions and software, and calculate their burn rate-how much cash they spend monthly minus revenue. Once you know your burn rate, you can calculate runway: how many months of operations your current cash covers. If you’re burning $50,000 monthly and have $200,000 in the bank, you have four months. That number should terrify you into action, not paralyze you. It should trigger decisions about hiring freezes, marketing spend, or accelerating sales efforts.

Founders often underestimate expenses as they scale. Office space, hiring, R&D, recruitment fees, and marketing spend all climb faster than revenue. Poor pricing decisions compound the problem-about 15% of startups cite weak pricing as a failure factor. If you don’t model how your cost structure changes as you grow, you’ll wake up six months in to discover margins have collapsed.

Customer acquisition cost, or CAC, matters enormously. Calculate it as your total sales and marketing spend divided by new customers acquired. If your CAC is $500 but your customer lifetime value is $1,200, you’re healthy. If CAC exceeds LTV, you’re burning cash for every customer you win. This metric alone should drive your hiring and marketing decisions, yet most early-stage founders don’t track it.

The second mistake is ignoring tax planning. R&D tax credits can materially reduce tax liabilities and improve cash flow for innovation-driven startups, yet founders often discover them too late. Quarterly tax payments sneak up and force emergency fundraising or personal loans. Building a financial plan now means separating what’s truly discretionary spending from what fuels growth, then tracking both relentlessly. This foundation positions you to make smarter decisions about capital allocation and prepares you for the funding conversations ahead.

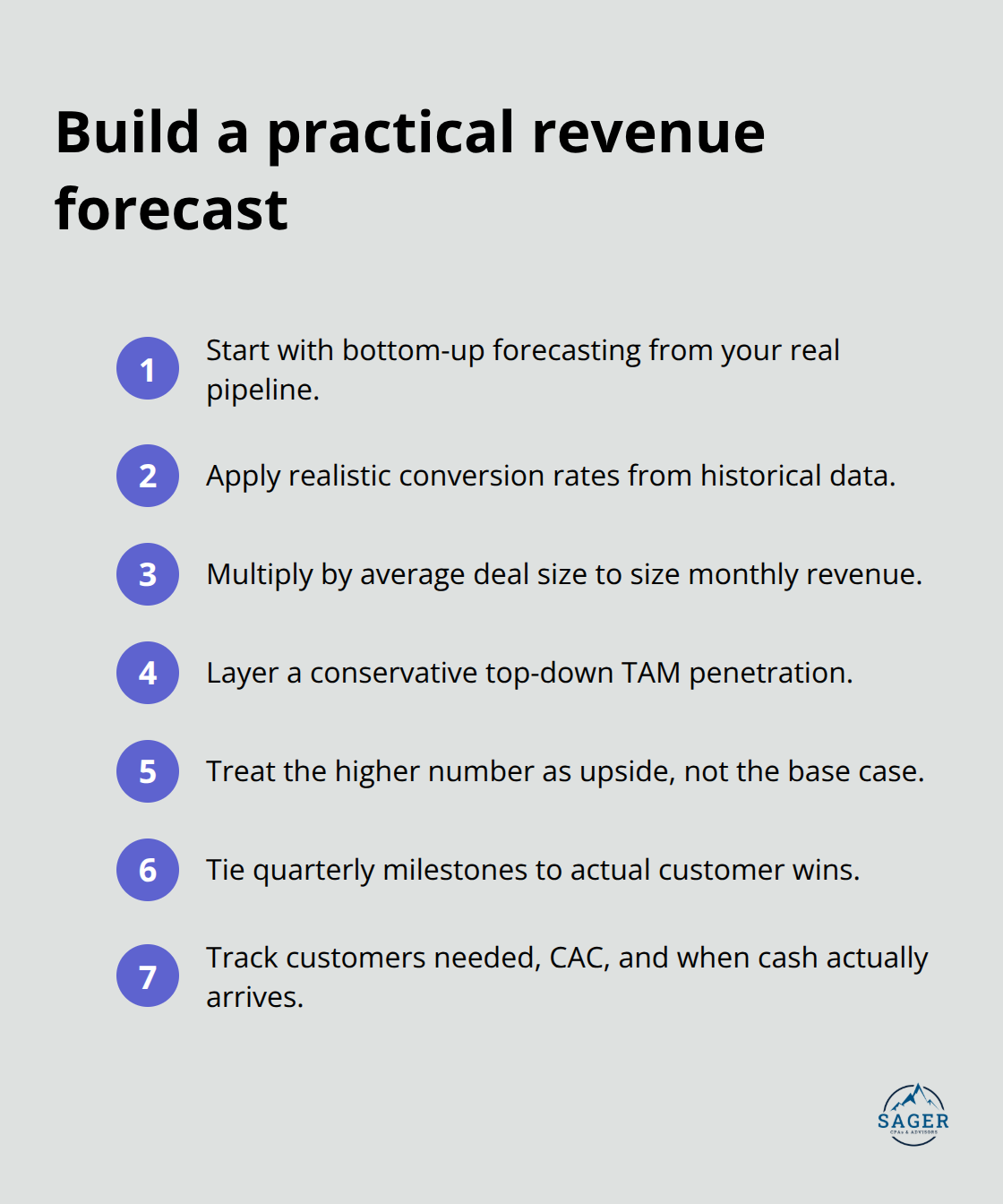

Revenue projections fail because founders mix optimism with guesswork. You need two forecasting methods to sanity-check your numbers. Start with bottom-up forecasting: count your actual sales pipeline, apply realistic conversion rates based on your past data, and multiply by average deal size. If you have 20 qualified leads, close 30% of them, and your average deal is $10,000, that’s $60,000 monthly revenue. That’s concrete.

Now layer top-down forecasting by calculating your total addressable market and applying a conservative market penetration rate. If your TAM is $10 million and you capture 2% in year one, that’s $200,000 annual revenue. If your bottom-up forecast says $720,000 and top-down says $200,000, you have a problem. The gap tells you either your pipeline is inflated or your market assumptions are wrong. Most founders present only the optimistic number to investors. Don’t. The founders who survive use historical data to model revenue month-by-month and treat the higher number as an upside scenario. Set quarterly milestones tied to actual customer wins, not just revenue targets. Track how many customers you need, what they cost to acquire, and when they’ll actually pay. Revenue on paper means nothing if cash arrives six months late.

Separate your fixed costs from variable costs, then build a monthly expense forecast for the next 18 months. Fixed costs-salaries, rent, insurance, software licenses-don’t change when revenue fluctuates. Variable costs like commissions, payment processing fees, and inventory scale with sales. Most founders underestimate fixed costs by 20–30% because they forget annual expenses, renewal fees, and hiring ramp-up. Calculate your net burn rate monthly: subtract your revenue from total operating expenses. If you spend $80,000 monthly and earn $20,000, your burn is $60,000. Multiply that by 12 and you’re burning $720,000 yearly. Now divide your current cash by your monthly burn to find runway. With $300,000 in the bank and $60,000 monthly burn, you have five months. That’s your hard deadline to either cut costs, accelerate revenue, or raise capital. Weekly cash flow monitoring catches spending creep early. As you scale, expect fixed costs to climb faster than you think. Hiring a single salesperson adds $60,000–$100,000 annually in salary plus benefits, equipment, and onboarding costs. A new office location adds rent, utilities, and setup expenses. Model these hiring and expansion decisions into your forecast six months ahead so you avoid surprises.

Quarterly tax payments shock founders because they don’t separate taxes from cash flow planning. The IRS expects estimated tax payments four times yearly. If you’re profitable, you owe federal income tax, self-employment tax if you’re a sole proprietor or partnership, and state taxes depending on where you operate. Set aside 25–30% of net profit quarterly rather than spending it all. Open a separate tax savings account and automate transfers so the money isn’t tempting. Many founders miss R&D tax credits because they assume credits only apply to biotech or software companies. If you’re building anything new-refining a product, testing features, solving technical problems-you likely qualify. R&D credits can reduce your tax liability significantly and improve cash flow for innovation-driven startups. Work with a tax professional to document your R&D spending before year-end because retroactive claims become harder. Nexus and state tax obligations matter too. If you sell across multiple states or hire remote workers in different states, you may owe payroll taxes or sales tax in those jurisdictions. Ignoring this creates massive liabilities later.

Plan quarterly: calculate estimated taxes, update your cash flow forecast to account for tax payments, and confirm your hiring and spending decisions don’t create unexpected tax exposure. But don’t stop there. The founders who maintain control track cash weekly, not monthly. Weekly monitoring catches problems before they become emergencies. Most founders operate reactively, watching their bank balance spike and dip without understanding why. You need visibility into what’s actually happening: which customers paid, which invoices remain outstanding, and where spending exceeded budget. This weekly discipline transforms financial planning from a theoretical exercise into a tool that shapes real decisions. When you see cash tightening in week two of the month, you can adjust marketing spend or delay a hire before it becomes a crisis. When you spot a customer paying 60 days late instead of 30, you can adjust your cash flow forecast and plan accordingly. The founders who build this habit early find that funding conversations become easier because investors see a team that understands its numbers. They also find that scaling becomes less chaotic because they’re not constantly surprised by cash shortfalls or unexpected expenses. With this foundation in place, you’re ready to explore how different funding options align with your growth trajectory and financial needs.

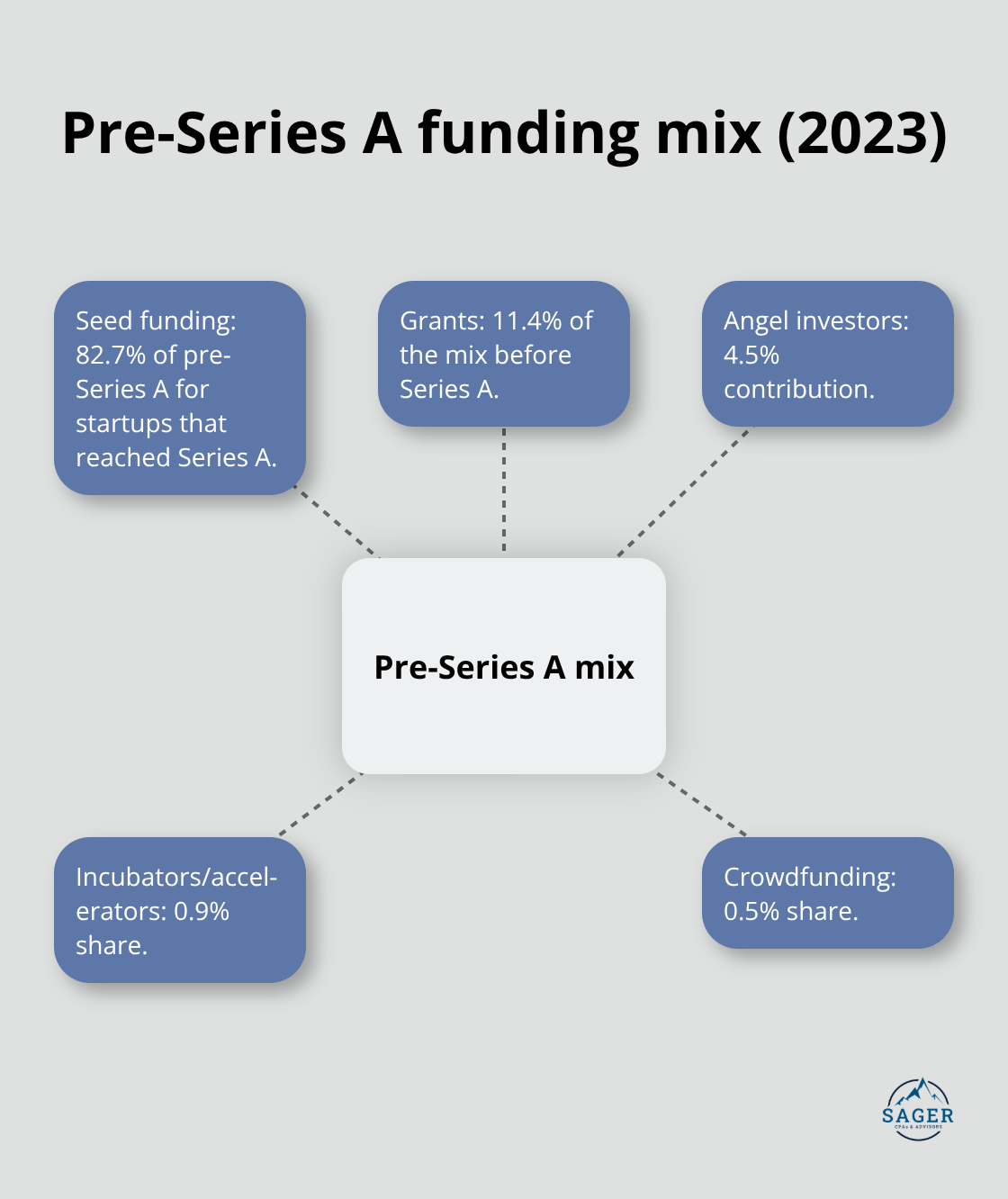

Seed funding accounts for 82.7% of pre-Series A funding for startups that reached Series A in 2023, according to PitchBook data. The remaining pre-Series A mix includes grants at 11.4%, angel investors at 4.5%, incubators and accelerators at 0.9%, and crowdfunding at 0.5%. Before you chase seed funding, understand what each stage actually funds. Seed rounds pay for initial hires, MVP development, and early commercialization.

If you still figure out product-market fit, seed investors will question your readiness. You need traction first: real customers, revenue data, or at minimum strong validation that a market exists for what you build.

Most founders underestimate how long fundraising takes. Plan for 24 to 30 months from your first conversations to final capital deployment across multiple rounds. This means you should start thinking about Series A requirements while you close your seed round. Convertible notes and SAFEs are common seed instruments because they defer valuation until later rounds, which reduces negotiation friction early on. A convertible note is essentially a loan that converts to equity at a discount when you raise Series A. A SAFE is a simpler agreement without interest or maturity dates. Both protect early investors and give founders more runway to prove traction before you assign a company valuation.

If you choose preferred stock for seed funding, expect higher governance requirements and investor board seats. The tradeoff: you get larger capital checks and investor credibility, but you lose autonomy faster. Whichever instrument you choose, model the dilution carefully. If you raise $1 million at a $5 million post-money valuation, you give up 16.7% of your company. Add a Series A round at $10 million on a $40 million post-money valuation, and your original stake drops to 13.9%. Founders often ignore dilution math and wake up owning minimal equity by Series B. Calculate your ownership after three rounds before you sign anything.

Your budget must align revenue growth with expense growth, which means you separate what scales with customers from what doesn’t. Fixed costs like salaries and rent stay constant regardless of revenue. Variable costs like commissions, customer support, and payment processing fees rise as you acquire more customers. When you raise funding, founders often increase fixed costs immediately: they hire five engineers, two marketers, and rent a bigger office. Then revenue doesn’t scale as fast as expected and suddenly burn rate accelerates.

The disciplined approach is to phase hiring against concrete revenue milestones. If you raise $1 million and your burn is $80,000 monthly, you have 12.5 months of runway. Don’t spend it all on headcount in month one. Instead, tie each hire to a revenue target or customer acquisition milestone. Your first salesperson should start when you have pipeline to justify it, not when you have cash. Your first marketing hire should start when you have product-market signals worth amplifying. This discipline separates founders who build sustainable businesses from those who waste capital.

Incubators and accelerators offer non-financial benefits beyond capital: mentorship from experienced operators, subject-matter expertise in areas where you’re weak, shared workspaces that reduce overhead, and networks that accelerate customer discovery and hiring. If you’re bootstrapped or pre-seed, accelerators like Y Combinator or TechStars provide capital, structure, and credibility that helps you raise your first institutional round faster. The downside is equity dilution, typically 6 to 10%. Evaluate whether the mentorship and network are worth it for your specific situation.

You need a tax professional and a financial advisor aligned with startup realities, not traditional business accounting. A startup’s financial strategy looks nothing like a mature company’s. You manage multiple funding rounds, equity structures, tax credits, and growth-driven spending that standard bookkeepers don’t understand. Professional advisors integrate tax planning with financial forecasting so you avoid surprises from quarterly payments or missed credits. R&D tax credits can materially reduce your tax liability and improve cash flow, but only if you document the work properly throughout the year.

Engage an advisor who reviews your data monthly, not annually. Monthly reviews catch spending drift, identify cost reduction opportunities, and keep your forecast aligned with reality. If your expenses track 30% above forecast, you need to know in month two, not month twelve. The advisor relationship should also include scenario planning. Model what happens if a major customer churns, if a fundraising round takes longer than expected, or if market conditions tighten. These scenarios aren’t pessimism; they’re prudence. Founders with scenarios built into their plans respond faster to reality because they’ve already thought through options.

Choose an advisor who works with founders at your stage and who understands your industry. A tax professional who specializes in SaaS startups will spot opportunities and risks that a generalist misses. The cost of professional guidance pays for itself through avoided mistakes, tax savings, and smarter capital decisions that extend your runway and improve your odds of reaching the next milestone.

Financial planning for founders operates as your business’s operating system during growth. You now understand how cash flow timing kills companies faster than bad products, why burn rate and runway demand constant attention, and how revenue projections need both bottom-up and top-down validation to hold weight. Tax strategy integrated with growth planning extends your runway and protects cash that founders often waste through missed credits and surprise quarterly payments.

The real protection comes from professional guidance aligned with startup realities. We at Sager CPA work with founders who treat financial planning as the foundation for every decision: which customers to pursue, when to hire, how much to spend on marketing, and when you’re ready to raise capital. Monthly reviews catch problems before they spiral into crises, and scenario planning prepares you for the uncertainty that all founders face.

Start this week by calculating your current burn rate and runway, then separate your fixed costs from variable costs and build a revenue forecast using both methods. Set up weekly cash flow monitoring so you see problems before they become emergencies. Sager CPA offers strategic tax planning and financial advisory tailored to help founders build sustainable growth, and the investment in professional guidance pays for itself through avoided mistakes and smarter capital decisions.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.