Proactive Tax Planning: Stay Ahead of the Tax Curve

Reduce your tax bill with proactive tax planning strategies that work year-round. Learn actionable tips to minimize taxes and keep more of your income.

Most business owners focus on growing their companies but neglect pension planning for business owners. Without a solid retirement strategy, you risk working far longer than you’d like or facing financial stress in your later years.

At Sager CPA, we’ve seen firsthand how the right pension plan transforms a business owner’s financial future. This guide walks you through your options and helps you build a strategy that works for your specific situation.

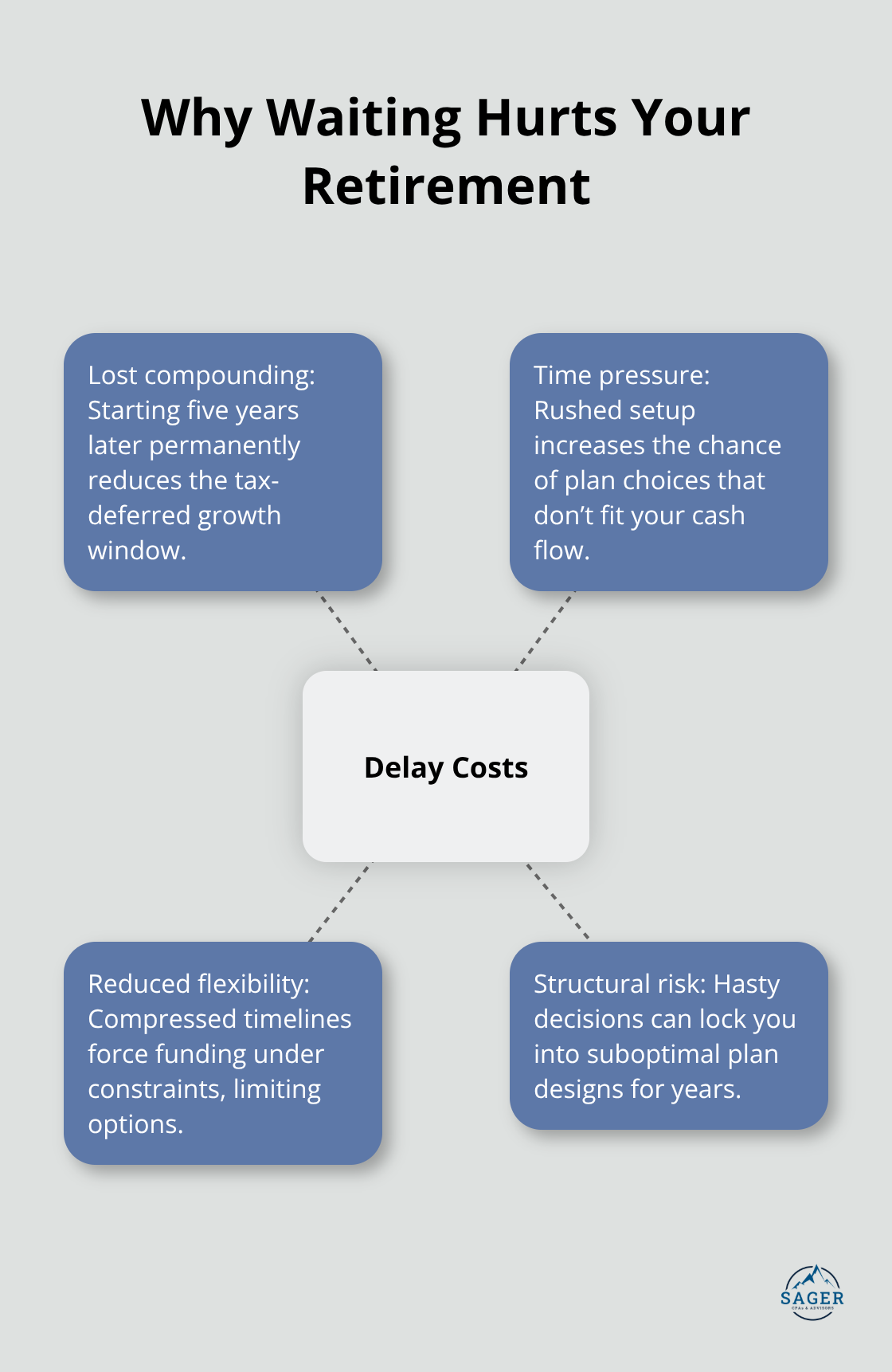

Business owners operate in a fundamentally different retirement landscape than employees. You cannot rely on a traditional employer pension or a steady paycheck in your later years. Your retirement security depends entirely on the decisions you make today, and waiting to plan costs you significantly. IRS data on tax-deferred growth for delayed pension planning shows that business owners who delay pension planning can miss out on significant investment growth. If you earn $150,000 annually as a self-employed professional and delay setting up a SEP-IRA for five years, you forfeit the opportunity to contribute 25% of your net earnings annually into tax-deductible accounts. That amounts to roughly $18,750 per year in lost contributions and compound growth.

The longer you wait, the steeper the catch-up becomes. Starting at age 45 versus age 50 means five additional years of tax-deferred compounding that you simply cannot recover later. Waiting also creates administrative pressure, forcing you to establish and fund a plan under time constraints rather than thoughtfully building a strategy aligned with your business cash flow. You lose flexibility when you rush, and rushed decisions often lead to suboptimal plan structures that don’t match your actual business needs.

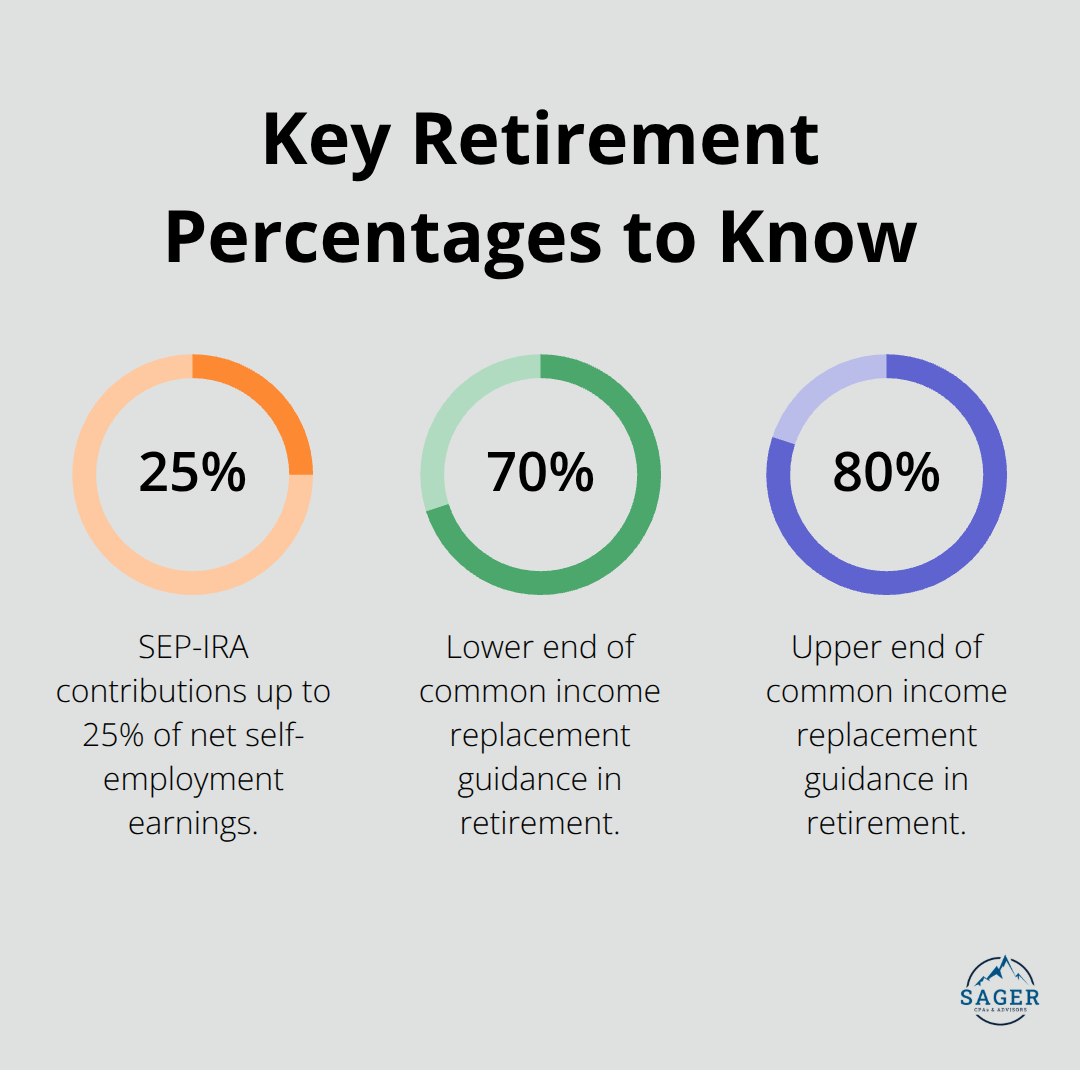

The retirement plan you select directly determines how much you can save annually and how quickly your nest egg grows. A solo 401(k) allows you to contribute up to $24,500 in employee deferrals for 2026, plus up to $72,000 in employer profit-sharing contributions, reaching a combined limit of $72,000. A SEP-IRA lets you contribute up to 25% of your net self-employment earnings, capped at $69,000 for 2024. A defined benefit plan maximum annual benefit contribution limit 2024 can provide significant annual benefits, making it a strong option if you have substantial income and want to catch up quickly on retirement savings.

The difference between these options matters enormously. A business owner earning $200,000 who chooses a SEP-IRA can contribute roughly $50,000 annually. The same owner using a solo 401(k) could contribute significantly more by combining salary deferrals and employer contributions. If that business owner waits until age 55 to start, they’ve missed 10 years of potential contributions and growth.

Your pension plan choice isn’t just about tax deductions, though those matter. It’s about structuring your business to fund your retirement systematically while reducing your current tax burden. This alignment between your business goals and retirement goals is what separates owners who retire comfortably from those who extend their working years out of necessity. The right plan transforms how your business operates financially, creating a systematic path toward the retirement you actually want rather than the one circumstances force upon you.

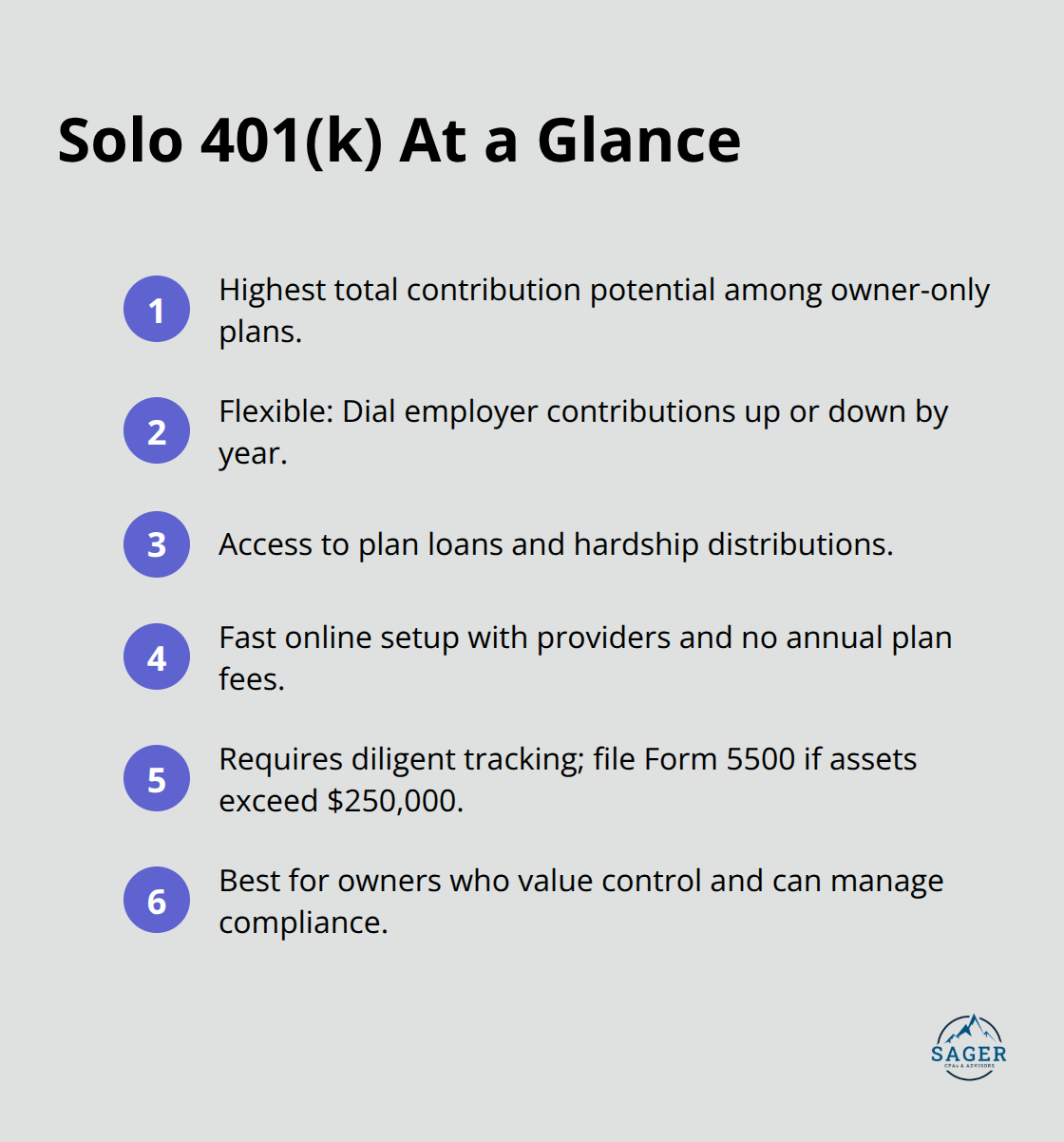

A solo 401(k) works best if you want maximum contribution flexibility and plan to earn over $100,000 annually. For 2026, you can contribute up to $24,500 as an employee deferral, then add employer profit-sharing contributions up to $72,000 total, giving you the highest savings capacity of any plan option. The real advantage emerges when your income fluctuates. In profitable years, you contribute aggressively. In slower years, you reduce employer contributions without penalty. You also gain access to plan loans and hardship distributions, meaning your money stays accessible if business emergencies arise.

Setup takes days online, and providers offer no annual plan fees, only investment costs through your chosen funds. The catch: administration requires discipline. You must track contributions carefully, file Form 5500 if assets exceed $250,000, and maintain accurate records. This plan suits owners who value control and have the operational capacity to manage compliance.

A SEP-IRA serves self-employed professionals who want simplicity over maximum contributions. You contribute up to 25 percent of your net self-employment earnings, capped at $69,000 for 2024, making it ideal for consultants, freelancers, and service providers earning under $150,000. Setup uses Form 5305-SEP through any bank or financial institution and requires minimal paperwork. The real benefit: minimal ongoing administration. No Form 5500 filing, no complex compliance rules, no annual reporting beyond your tax return. You can establish a SEP-IRA as late as your tax filing deadline, including extensions, offering flexibility if you’re uncertain about business income early in the year. However, the 25 percent cap means you contribute less than a solo 401(k) owner earning similar income, and you cannot make catch-up contributions beyond the annual limit. This plan works for owners prioritizing administrative simplicity and those with variable income who need flexibility in contribution amounts.

A defined benefit plan generates the highest annual contributions if you have substantial income and want to accelerate retirement savings. The IRS allows maximum annual benefits up to $275,000 in 2024, with contributions calculated by an actuary based on your age, income, and years until retirement. A 55-year-old earning $300,000 might contribute $80,000 to $120,000 annually, far exceeding solo 401(k) or SEP-IRA limits. This approach makes sense if you started retirement planning late and need aggressive catch-up. The trade-off is real: you must hire an actuarial firm to design and annually value the plan, costing $1,500 to $3,000 yearly. You also lock in a fixed contribution requirement each year, meaning you cannot reduce contributions during downturns without plan amendment. Form 5500 filing is mandatory. This plan demands stable, predictable income and genuine commitment to retirement funding. For business owners with declining income or uncertain cash flow, the fixed obligation becomes a liability rather than an asset.

Your income level determines which plan actually maximizes your retirement savings. Owners earning under $100,000 find that SEP-IRAs and solo 401(k)s produce similar results, with the SEP-IRA winning on simplicity. Owners earning $100,000 to $250,000 benefit significantly from solo 401(k) flexibility, especially if income varies year to year. Owners earning over $250,000 with stable income should evaluate defined benefit plans, as the contribution capacity often exceeds both other options. The plan you select today shapes your retirement security for decades, making this decision one that warrants careful analysis of your actual income trajectory and business stability.

Create an accurate picture of your net worth today, not an inflated estimate. Pull together your business equity, personal investments, real estate, and liquid savings. Many business owners overestimate their net worth because they count business value as fully liquid retirement income, which it isn’t. Your business might be worth $500,000, but selling it takes time, costs money in transaction fees, and may not happen when you need it most. Separate business assets from personal retirement assets in this calculation. This distinction reveals what you actually have available for retirement versus what remains tied up in your company.

Determine your annual retirement expenses by reviewing three years of actual spending. Most financial planners suggest replacing 70 to 80 percent of pre-retirement income, but that generic advice misses your reality. If you spend $120,000 annually today and plan to travel extensively in retirement, you might need $150,000 or more.

If you plan to downsize your home and simplify, you might need only $80,000. The gap between what you’ll need and what you’ll have from Social Security and existing investments is exactly what your pension plan must fund.

For a business owner expecting $2,000 monthly from Social Security and needing $10,000 monthly in retirement, you need to generate $8,000 monthly from your pension plan. You add up all of your investments and withdraw 4% of that total during your first year of retirement. That requires roughly $240,000 in annual income from accumulated retirement assets, which means you need $6 million saved. That number feels enormous until you work backward. If you’re 45 years old with 20 years until retirement and can contribute $50,000 annually to a SEP-IRA or solo 401(k), compound growth at 7 percent annually produces roughly $2.3 million. Add catch-up contributions at age 50 and 60, and you’re approaching $3 million. That gap between $3 million and $6 million tells you whether your current plan structure works or whether you need a defined benefit plan’s more aggressive contributions.

Coordinate your pension strategy with your business succession plan because these decisions affect each other directly. If you plan to sell your business at age 60, you need retirement income starting then, not at 65. If you plan to pass the business to family members and receive distributions over 10 years, your pension plan must bridge the gap between retirement and when those distributions begin. Some business owners reduce pension contributions in their final five working years to preserve cash for the business sale or transition, which is a mistake that costs tens of thousands in lost contributions and growth. Instead, consider increasing contributions in those final years when you know business cash flow will improve post-transition.

If you’re selling the business, negotiate the sale price to include a retirement bonus or consulting agreement that extends your income and allows continued pension contributions. Document your succession plan in writing and share it with your pension plan administrator and tax advisor. The IRS allows you to modify contribution amounts within limits, but modifications require plan amendments that take time. Anticipate these changes three to five years before they happen to gain the flexibility to adjust your plan structure without scrambling. Some business owners discover too late that their chosen plan doesn’t accommodate their actual business transition, forcing them to establish a second retirement plan or accept lower retirement contributions.

A defined benefit plan might be perfect for your situation if you’re 50, have 15 years until retirement, and expect to sell your business for a significant gain. A solo 401(k) with loan provisions makes sense if you might need access to funds for business expansion or emergency capital. Your pension plan isn’t just about tax deductions or annual contributions. It’s a structural decision that shapes your business finances, your retirement security, and how smoothly you transition into the next phase of your life.

Pension planning for business owners isn’t a one-time task you complete and forget about. It shapes your financial independence and determines whether you work because you want to or because you have to. The three plan types we covered-solo 401(k)s, SEP-IRAs, and defined benefit plans-each solve different problems, and you must match the right solution to your actual situation, not the situation you think you should have.

Start by calculating your retirement income gap: subtract what Social Security will provide from what you actually need to spend annually, then work backward to determine which plan structure gets you there given your current age, income, and business stability. Your pension plan must also coordinate with your business succession strategy because if you’re selling in five years, your contribution timeline changes, and if you’re passing the business to family, your income expectations shift. These aren’t separate decisions-they’re interconnected, and treating them separately costs you money.

Pension planning involves tax strategy, business structure analysis, and retirement projections that interact in ways most business owners don’t anticipate, and the IRS rules change while your business circumstances evolve. We at Sager CPA work with business owners to build personalized financial strategies that align retirement planning with business goals, reduce tax liabilities, and create the clarity you need to make confident decisions.

Phone: (208) 939-6029

Email: info@sager.cpa

Privacy Policy | Terms and Conditions | Powered by Cajabra

At Sager CPAs & Advisors, we understand that you want a partner and an advocate who will provide you with proactive solutions and ideas.

The problem is you may feel uncertain, overwhelmed, or disorganized about the future of your business or wealth accumulation.

We believe that even the most successful business owners can benefit from professional financial advice and guidance, and everyone deserves to understand their financial situation.

Understanding finances and running a successful business takes time, education, and sometimes the help of professionals. It’s okay not to know everything from the start.

This is why we are passionate about taking time with our clients year round to listen, work through solutions, and provide proactive guidance so that you feel heard, valued, and understood by a team of experts who are invested in your success.

Here’s how we do it:

Schedule a consultation today. And, in the meantime, download our free guide, “5 Conversations You Should Be Having With Your CPA” to understand how tax planning and business strategy both save and make you money.